Tavi Costa at Crescat Capital (founded by my former MBA student at University of Chicago Kevin Smith) produced this excellent chart of silver prices showing the cup and handle of silver prices.

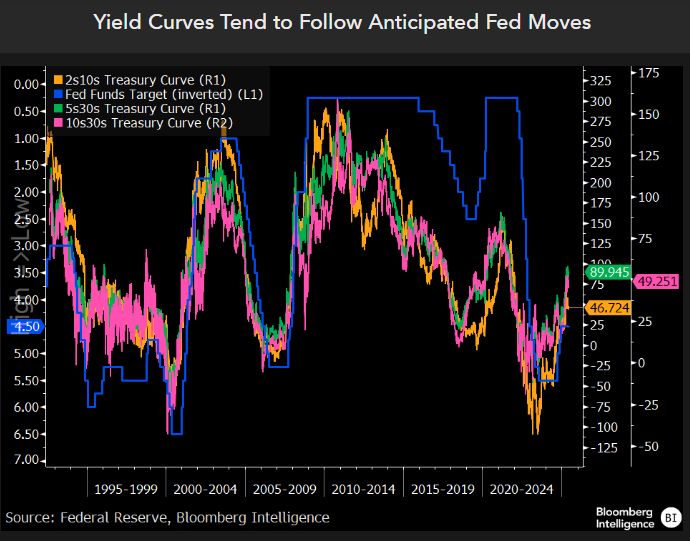

The rise in silver prices corresponds with a deterioration of the US bond market. Look at Treasury futures courtesy of Bravos Research.

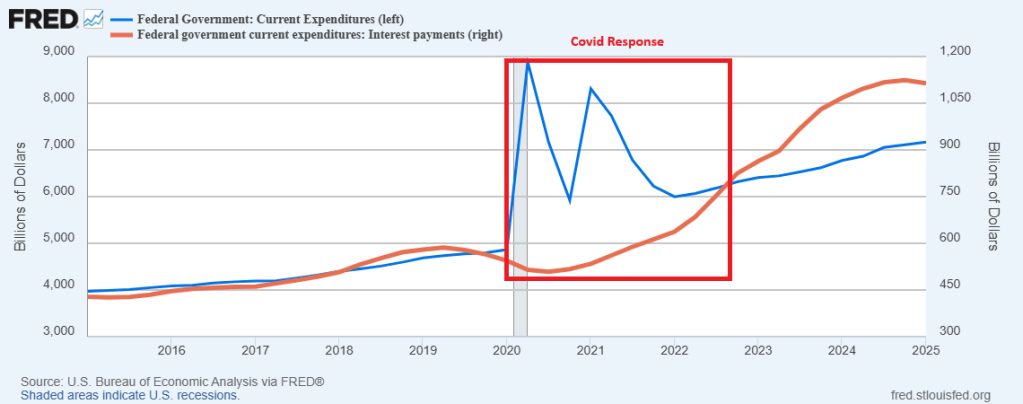

Of course, Washington DC’s insane spending has led to insane money printing by The Feral Reserve.

Everyone in Washington DC deserves a “Silver Cup of Failure” for uncontrolled government waste and spending and mismanagement by The Feral Reserve.

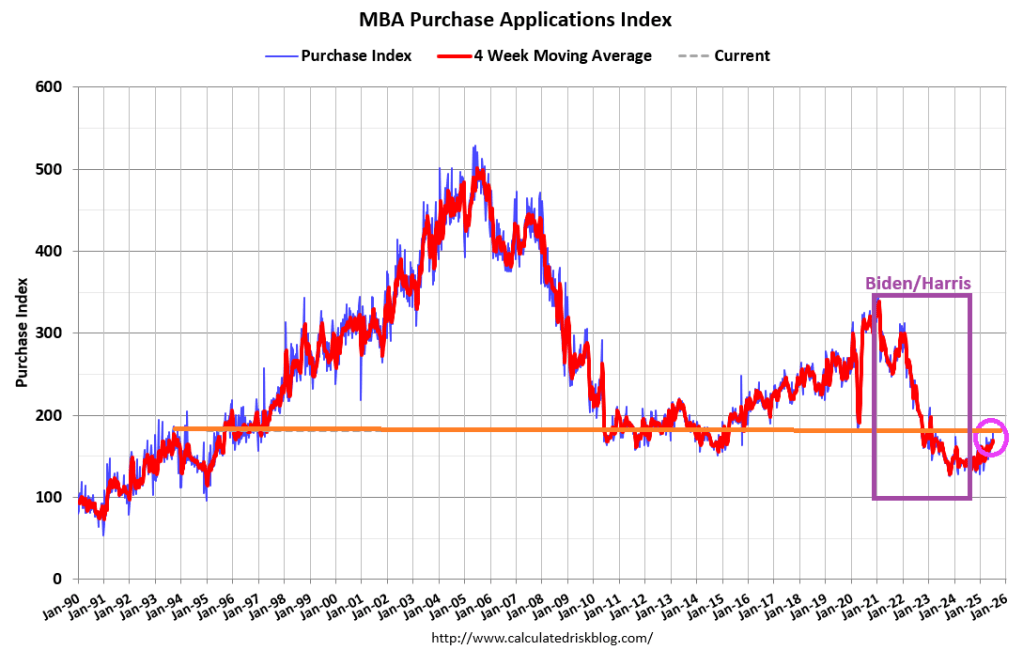

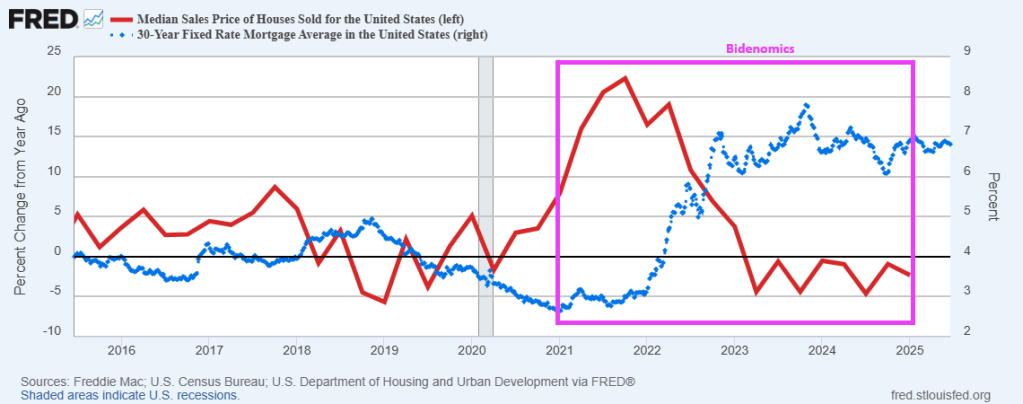

Thank goodness “Statist Joe” Biden is gone. Kamala Harris is still lingering around the edges, while the mortgage and housing markets are still suffering from the Biden/Harris regulatory overreach.

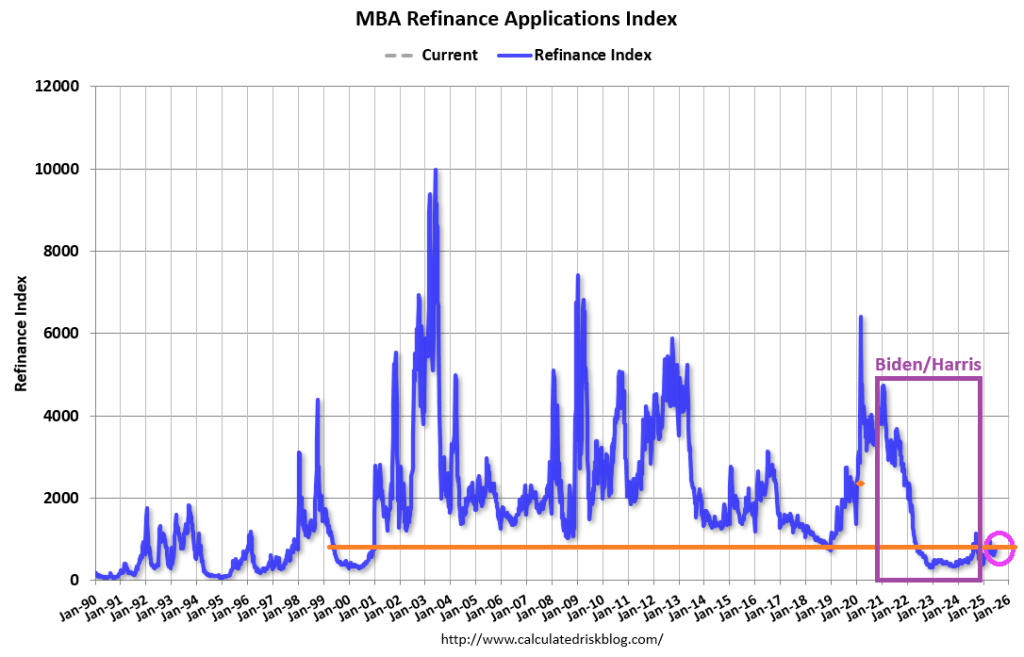

Mortgage applications increased 9.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 4, 2025. Last week’s results included an adjustment for the July 4th holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 9.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 13 percent compared with the previous week. The seasonally adjusted Purchase Index increased 9 percent from one week earlier. The unadjusted Purchase Index decreased 13 percent compared with the previous week and was 25 percent higher than the same week one year ago.

The Refinance Index increased 9 percent from the previous week and was 56 percent higher than the same week one year ago.

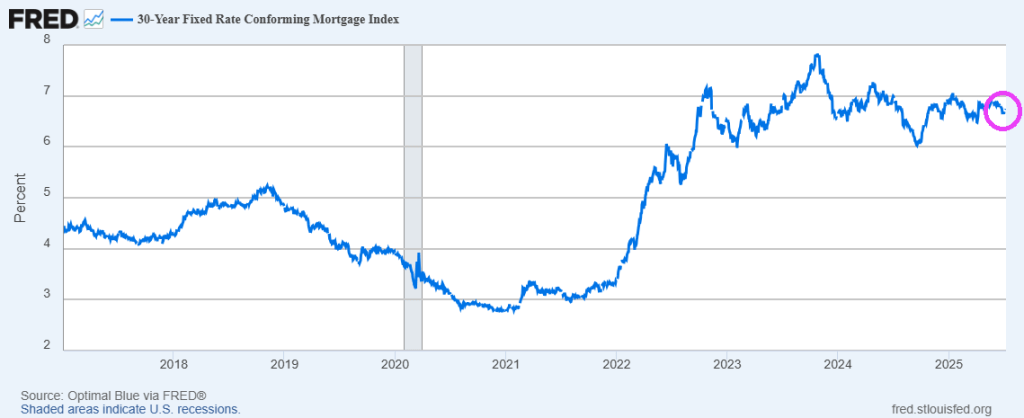

Mortgage rates moved lower last week, with the 30-year fixed rate decreasing to 6.77 percent, its lowest level in three months. After adjusting for the July 4th holiday, purchase applications increased to the highest level of activity since February 2023 and remained above year-ago levels.

Biden claims the foreign leaders have been calling him for advice. Here is one example.

Finally, US government debt growth (YoY) was approximately equal to US nominal GDP growth in Q1 2025.

Unfortunately, the BBB (Big Beautiful Bill) is projected to add $3.9 trillion of debt. Unfortunately, there are insufficient spending cuts in the BBB. And the Senate just nixed kicking illegal immigrants off of Federal healthcare programs.

Unfortunately, GDP growth is only expected to be modest with debt growth once again rising faster than GDP growth. As Diane Feinstein once said, politicians are elected to spend money. This, of course, was a ridiculous statement embraced by spend-crazy Democrats and RINOs.

So, Congress has committed American taxpayers to debt slavery.

So much for the doom porn from the media about the US economy collapsing due to Trump’s tariffs! The US economy (real GDP) in Q2 is still growing at 2.9%.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2025 is 2.9 percent on June 27, down from 3.4 percent on June 18. After recent releases from the US Census Bureau and the US Bureau of Economic Analysis, an increase in the nowcast of the contribution of net exports to second-quarter real GDP growth from 2.07 percentage points to 3.49 percentage points was more than offset by a decrease in the nowcasted GDP growth contribution of inventory investment from -0.42 percentage points to -2.22 percentage points.

Here is the data.

And with Democratic Socialist (aka, Communist) Zohran Mamdani winning the Democratic nomination for mayor, New York City will likely become the new Detroit.

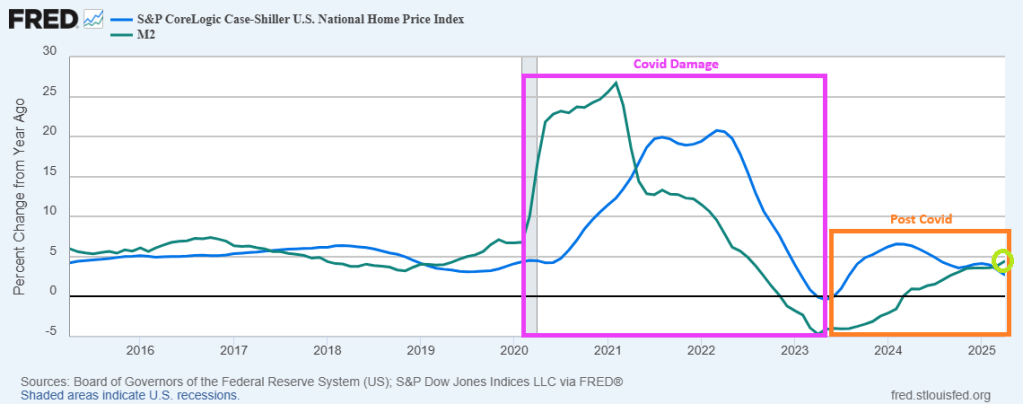

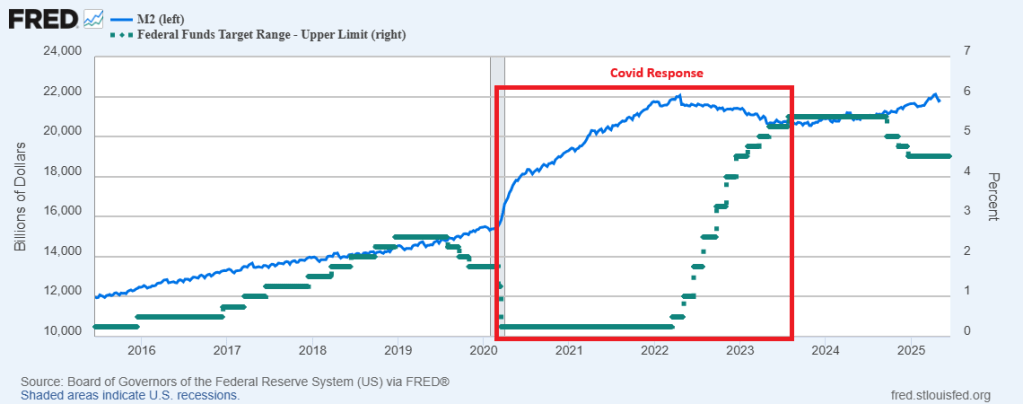

The Fed continues printing money! And home prices continue to rise on year-over-year basis, but falling on a month-over-month basis.

Home prices in April tumbled 0.31% MoM (-0.02% exp) – the biggest MoM drop since Dec 2022.

But if we look at the national home prices via S&P Case-Shiller and YoY rather than MoM, home prices ROSE 2.64% YoY.

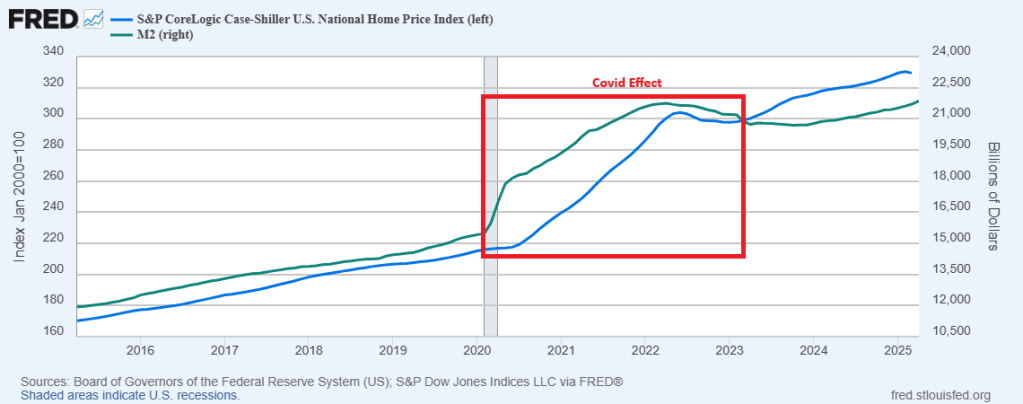

You can see the damage to homeownership caused by Covid and The Fed. The massive expansion of M2 Money in 2020 was followed shortly by rapid increases in home prices. This was followed by a normalization in Fed M2 Money printing. Consequently, home price growth has slowed.

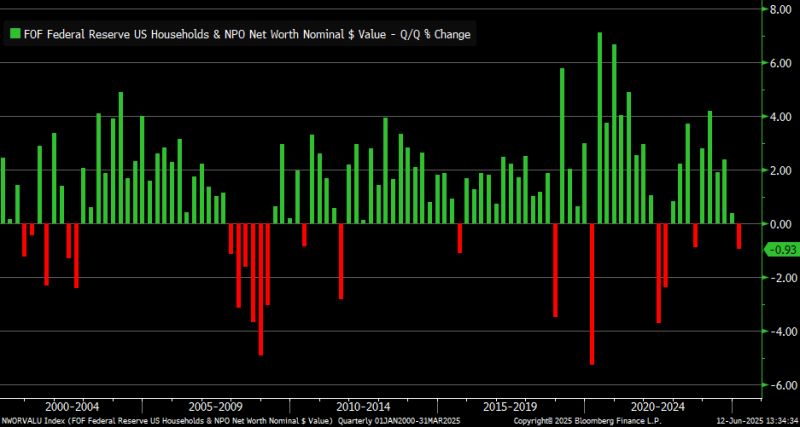

The housing markets is in bits and pieces following The Fed’s fickle management of interest rates and Biden’s disastrous spending policies. U.S. household net worth fell by 0.93% in 1Q2025 … largest decline since 3Q2022, but not necessarily comparable to that quarter in terms of magnitude.

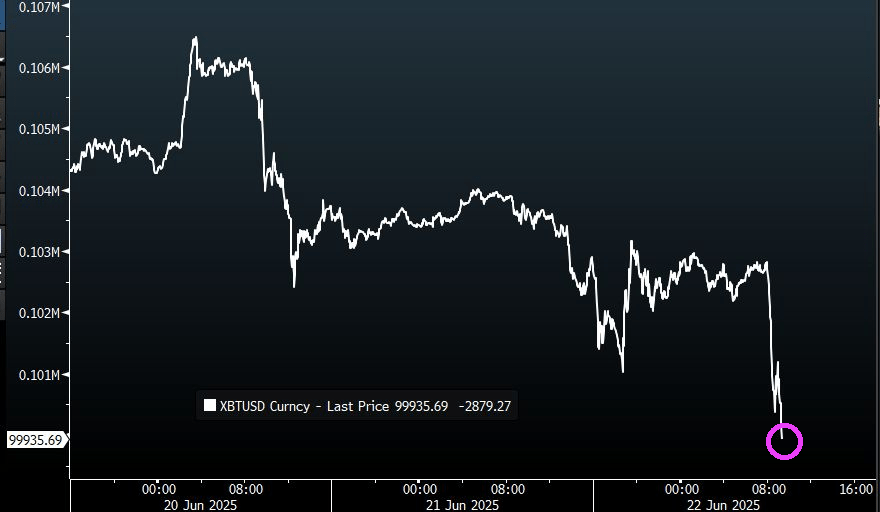

Bitcoin just broke below $100k.

What will The Fed? As I have said over and over again, The Fed needs to cut rates.

Thanks a lot Fed! Home prices rose dramatically after Covid as The Fed printed billions of dollar of currency (M2). Making housing unaffordable for much of America.

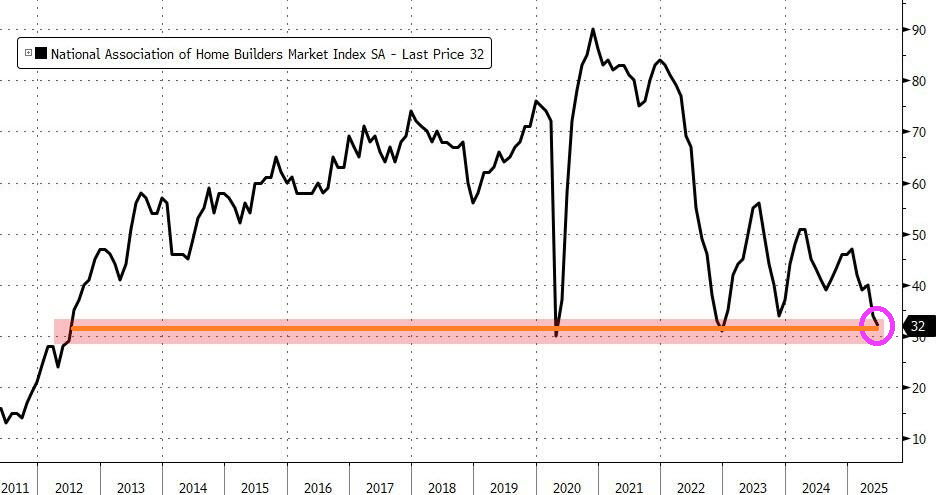

As a result of higher mortgage rates and higher home prices, homebuilder confidence is at a 13 year low (back to 2012).

You must be logged in to post a comment.