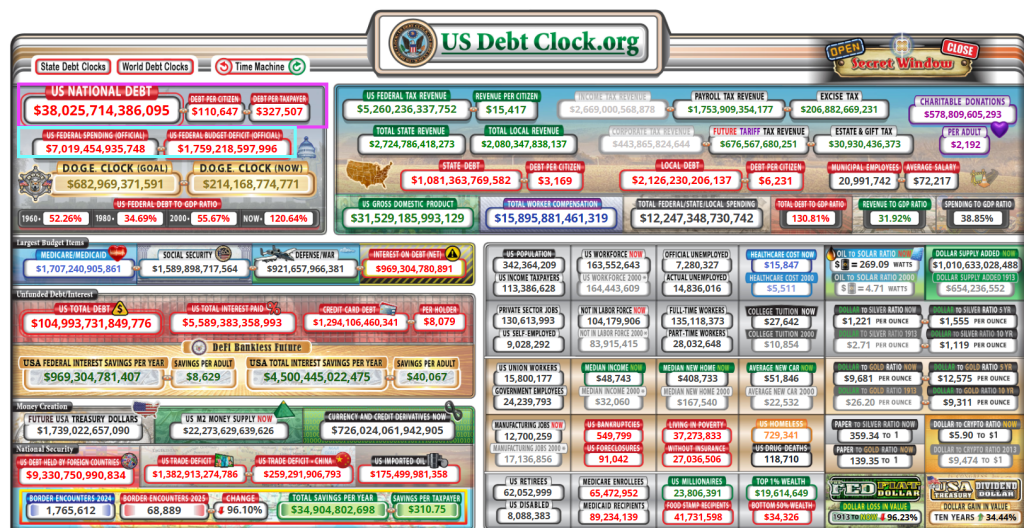

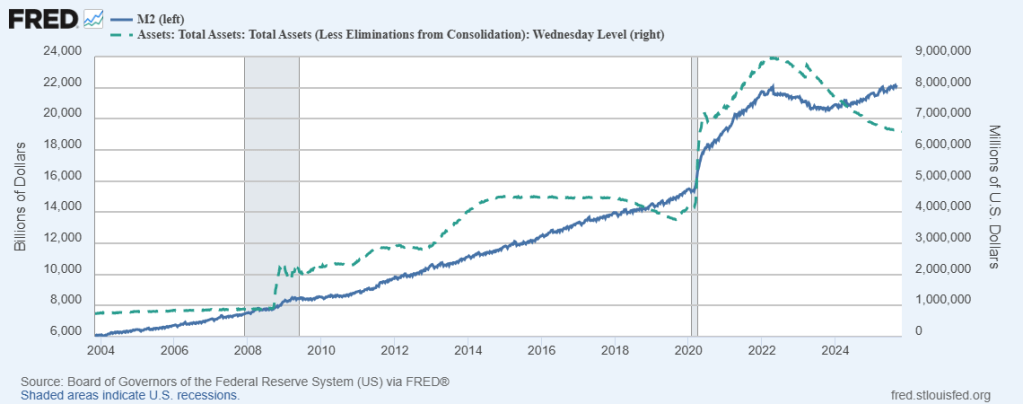

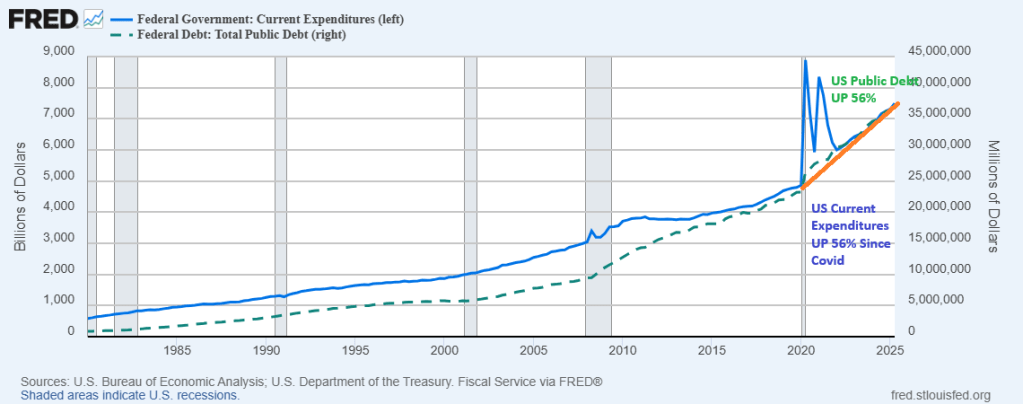

Of course, CPI data release has been delayed thanks to the US Federal government shutdown (aka, the Schumer Shutdown). But never fear, the Federal government is continuing to spending like the proverbial drunken sailors in port. The Federal debt just breached the $38 trillion mark.

And the Federal budget deficit just breached the $7 trillion mark. Why? Too much Federal spending! The Federal government COULD raises taxes, but that would strangle the economy. But politicians in DC are terrified of not being re-elected, so they are terrified of cutting spending.

Can we ask the US House and Senate if they will ever return US Federal government spending to pre-Covid levels? Both US Federal government spending and public debt are up 56% since the Covid outbreak in 2020.

The answer is no. Politicians thrive on Federal spending.

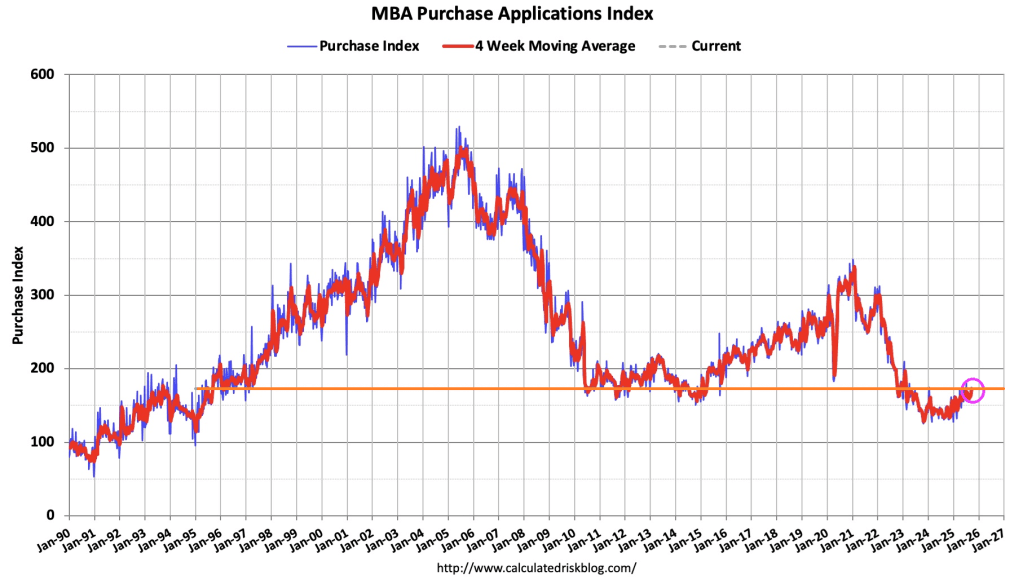

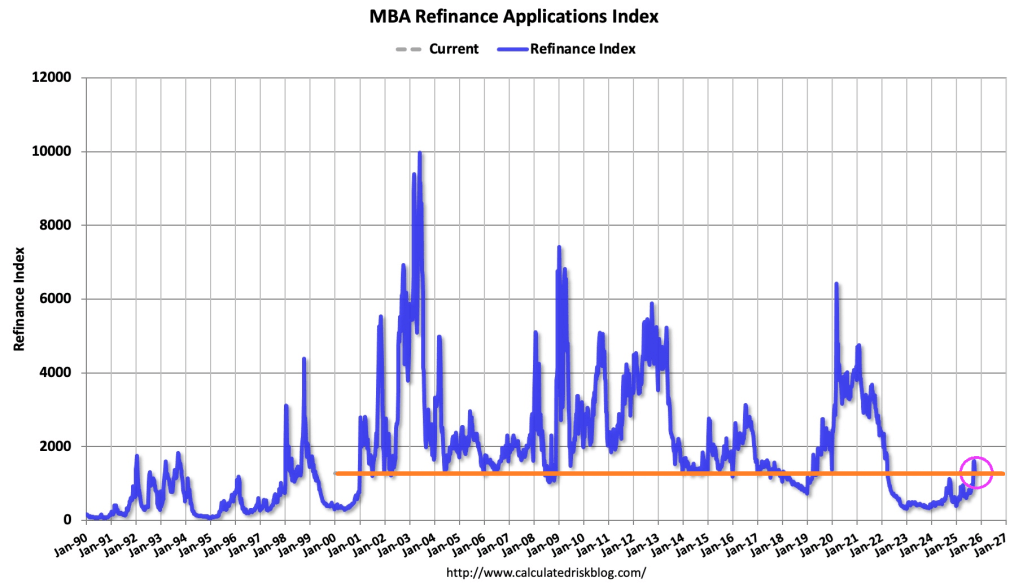

Mortgage applications decreased 4.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 3, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 14 percent higher than the same week one year ago.

The Refinance Index decreased 8 percent from the previous week and was 18 percent higher than the same week one year ago.

With mortgage rates on fixed-rate loans little changed last week, refinance application activity generally declined, with the exception of a modest increase for FHA refinance applications.

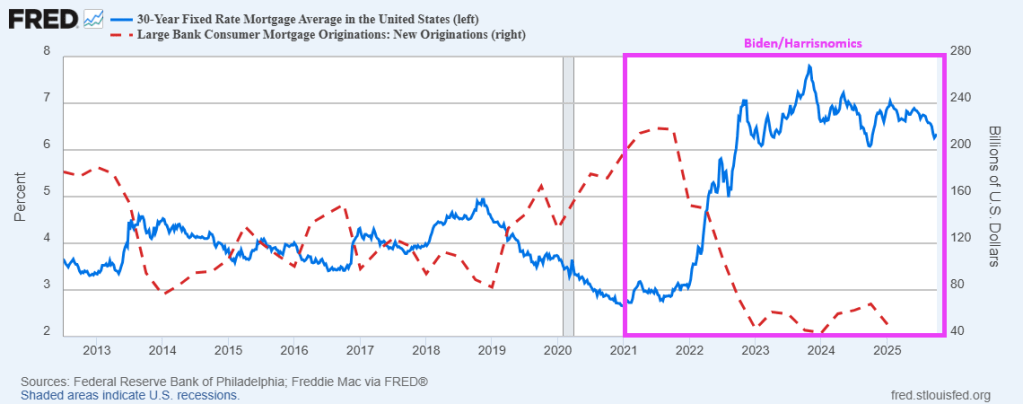

Mortgage demand dwindled since Covid and Biden/Powell and hasn’t recovered.

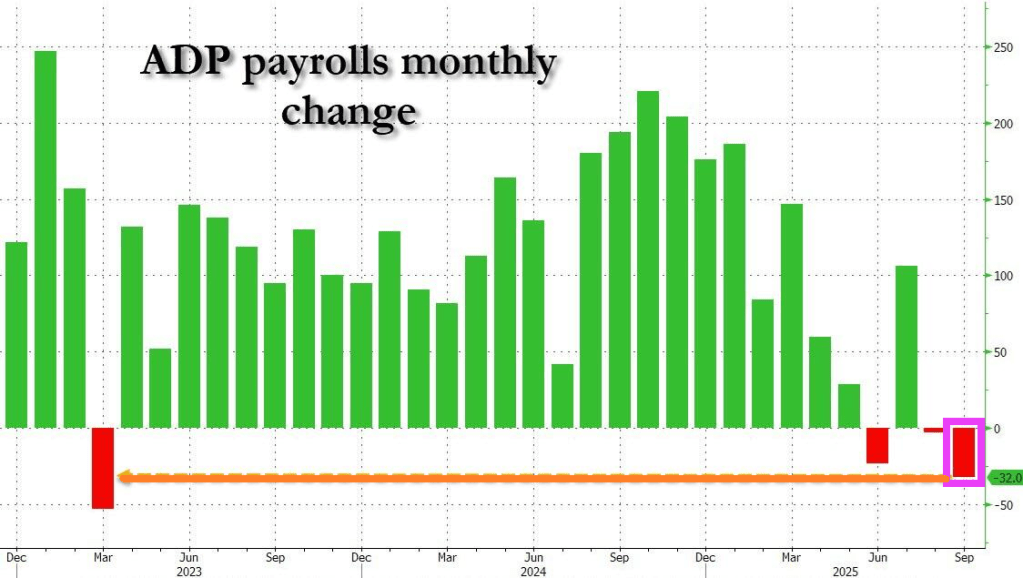

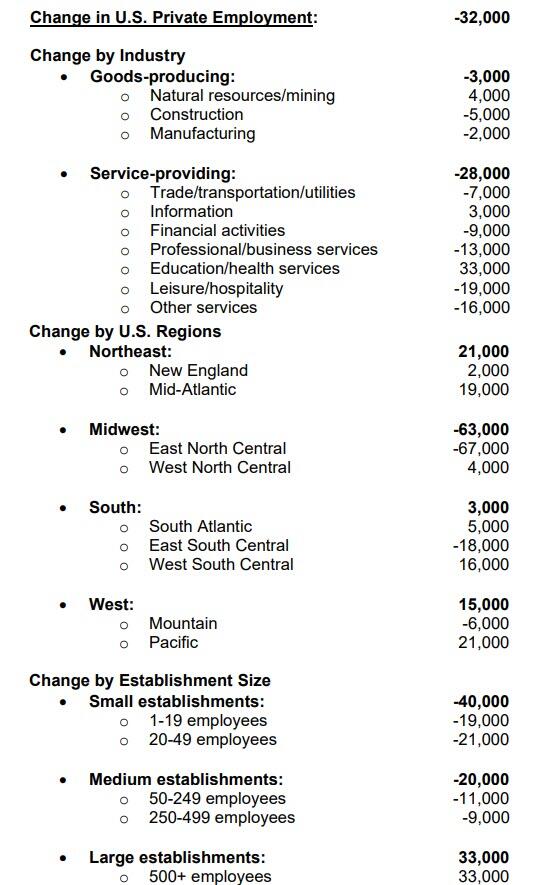

Due to the ongoing government shutdown – now in its third day – the BLS did not release the September jobs report this morning forcing traders and the Fed to “fly blind.” Or blinder than usual. And with ADP reporting earlier this week that some 32,000 jobs had been lost in September, putting markets and economists on edge and the US economy on the verge of a labor recession, the lack of data could not have come at a worse time. Luckily, private sector alternatives to the BLS do exist and, in many cases, are far more accurate and certainly less politicized.

Mortgage applications decreased 12.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 26, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 12.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 13 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 16 percent higher than the same week one year ago.

The Refinance Index decreased 21 percent from the previous week and was 16 percent higher than the same week one year ago.

Mortgage rates increased to its highest level in three weeks as Treasury yields pushed higher on recent, stronger than expected economic data. After the burst in refinancing activity over the past month, this reversal in mortgage rates led to a sizeable drop in refinance applications, consistent with the view that refinance opportunities this year will be short-lived.

August data for the US housing market has been ‘mixed’ to say the least with a surge in new home sales (thanks to a massive rise in incentives from homebuilders) and a small decline (near multi-year lows), leaving this morning’s pending home sales data as the tie-breaker (with expectations of an ‘unch’ shift MoM).

It appears the drop in mortgage rates is driving some purchase activity as pending home sales soared 4.0% MoM in August – the most since March – dragging sales up 0.5% YoY.

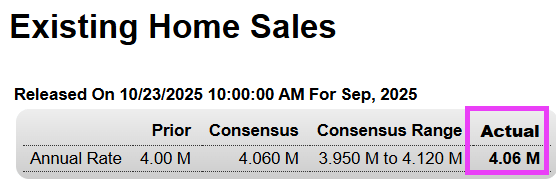

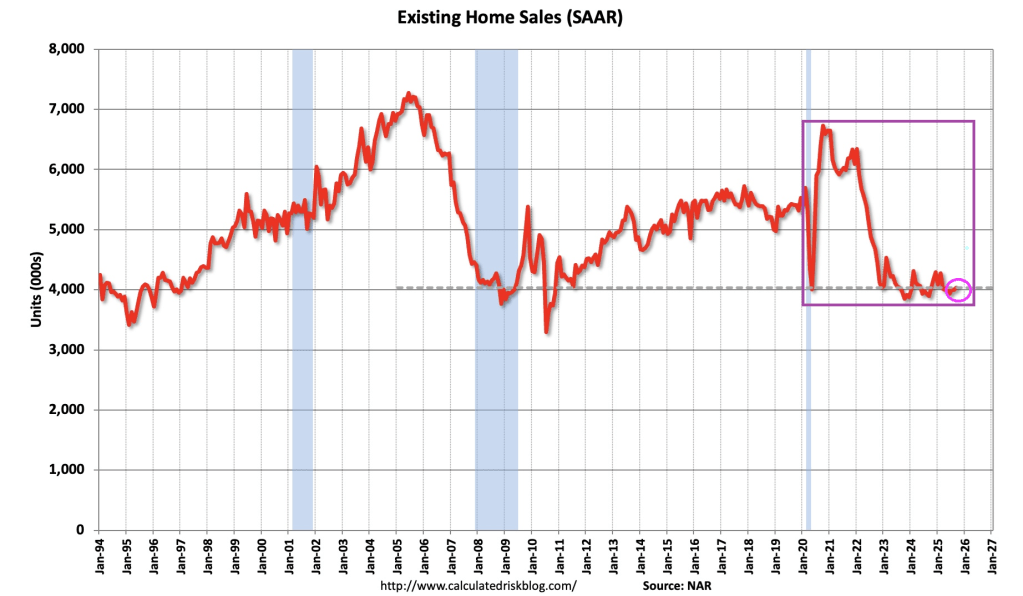

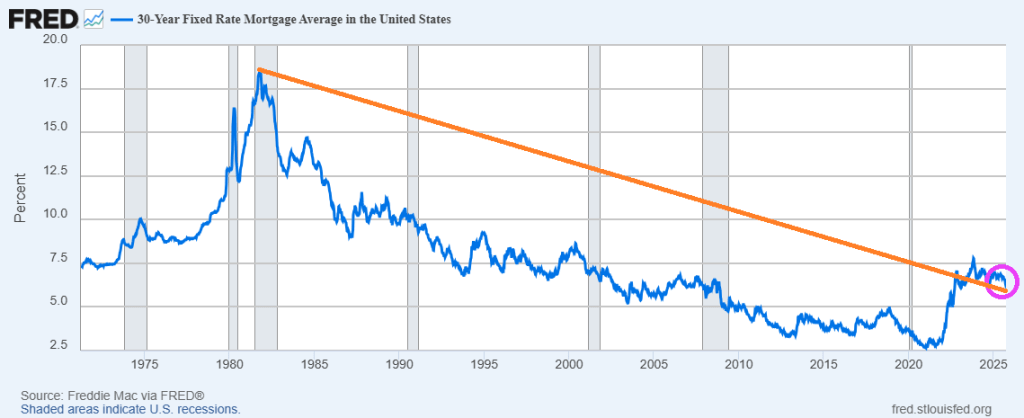

Mortgage rates are falling, helping existing home sales. Note that the 30-year mortgage rate peaked at 18.63% in 1981.

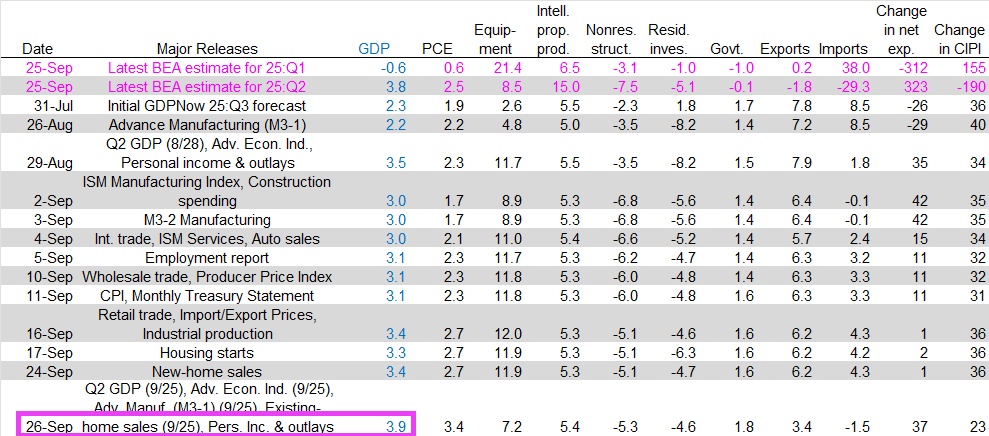

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2025 is 3.9 percent on September 26, up from 3.3 percent on September 17. After recent releases from the US Census Bureau, the US Bureau of Economic Analysis, and the National Association of Realtors, a decrease in the nowcast of third-quarter real gross private domestic investment growth from 6.4 percent to 4.1 percent was more than offset by increases in the nowcast of third-quarter real personal consumption expenditures growth from 2.7 percent to 3.4 percent and the nowcast of the contribution of net exports to third-quarter real GDP growth from 0.08 percentage points to 0.58 percentage points.

Existing home sales helped drive higher GDP growth.

You must be logged in to post a comment.