So much for the “Trump has ruined the economy” mantra of politicians and celebrities.

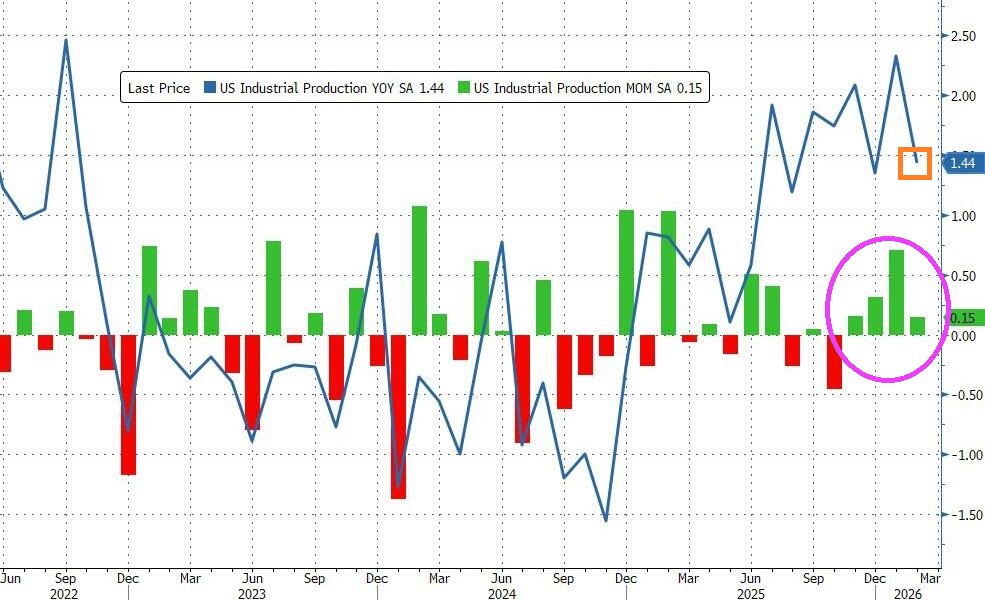

After a strong gain in January, US Industrial Production continued to expand in February, rising 0.2% MoM (better than expected +0.1%) – the fourth straight month of gains with Production up 1.44% YoY.

Source: Bloomberg

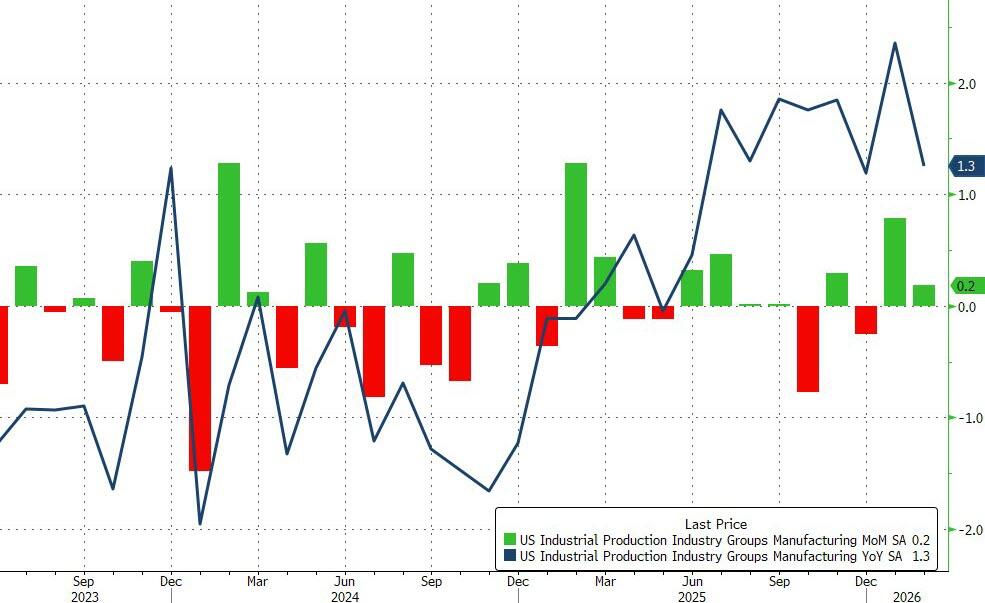

Manufacturing output also beat expectations, rising 0.2% MoM in February.

Durable manufacturing output edged up 0.1 percent, with mixed results across categories; the index for motor vehicles and parts posted the largest gain, and the index for machinery posted the largest loss.

Nondurable manufacturing output rose 0.2 percent, with gains in the production of chemicals, of plastic and rubber products, and of paper products outweighing declines in the output of petroleum and coal products and of food, beverage, and tobacco products. The output of other manufacturing (publishing and logging) rose 1.3 percent.

Mining output increased 0.8 percent in February, following a 0.9 percent increase in January. The output of utilities fell 0.6 percent in February, reflecting no change in the index for electric utilities and a 4.7 percent drop in the index for natural gas utilities.

Source: Bloomberg

Capacity Utilization printed 76.3 (better than expected)…

…maintaining the positive trend since Trump’s second term began.

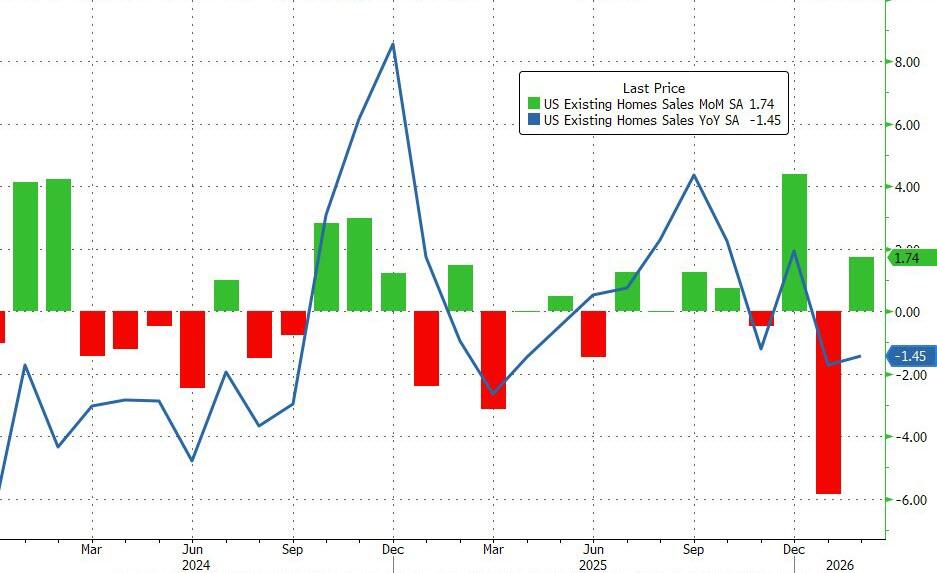

Existing homesales actually surprised to the upside, rising 1.7% MoM in February. Perhaps even more notably, January’s 8.4% MoM plunge was revised up to a slightly less crazy 5.9% MoM drop.

With the beat and upward revision, existing home sales were down just 1.45% YoY but SAAR topped 4mm (4.09mm) once again.

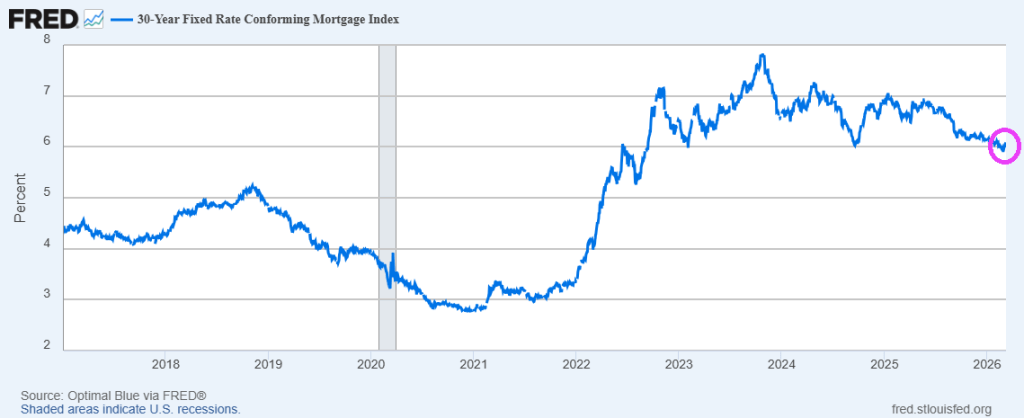

On the bright side, with mortgage rates at their lowest since 2022, existing home sales look set to continue to improve (unless Trump’s war triggers more panic in rates).

The NAR report showed the median selling price rose 0.3% from a year earlier — one of the smallest advances since the pandemic housing frenzy — to $398,000 last month.

The inventory of previously owned homes increased 4.9% from a year ago to 1.29 million — the most for any February since 2020.

Mortgage rates? Up yesterday, but near lowest since 2023.

Trump has been President for 1 year and fighting against Biden and the Democrats economic misery.

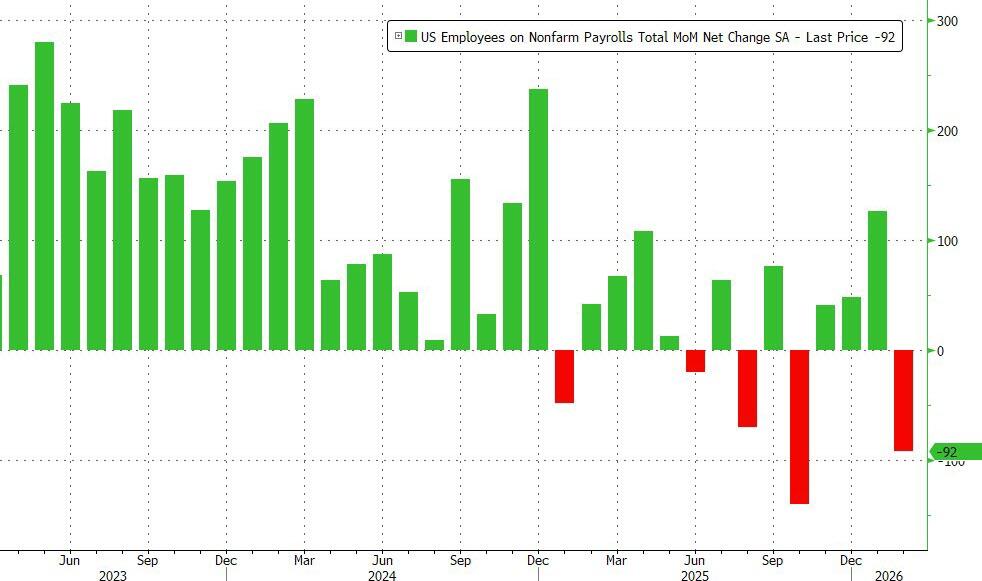

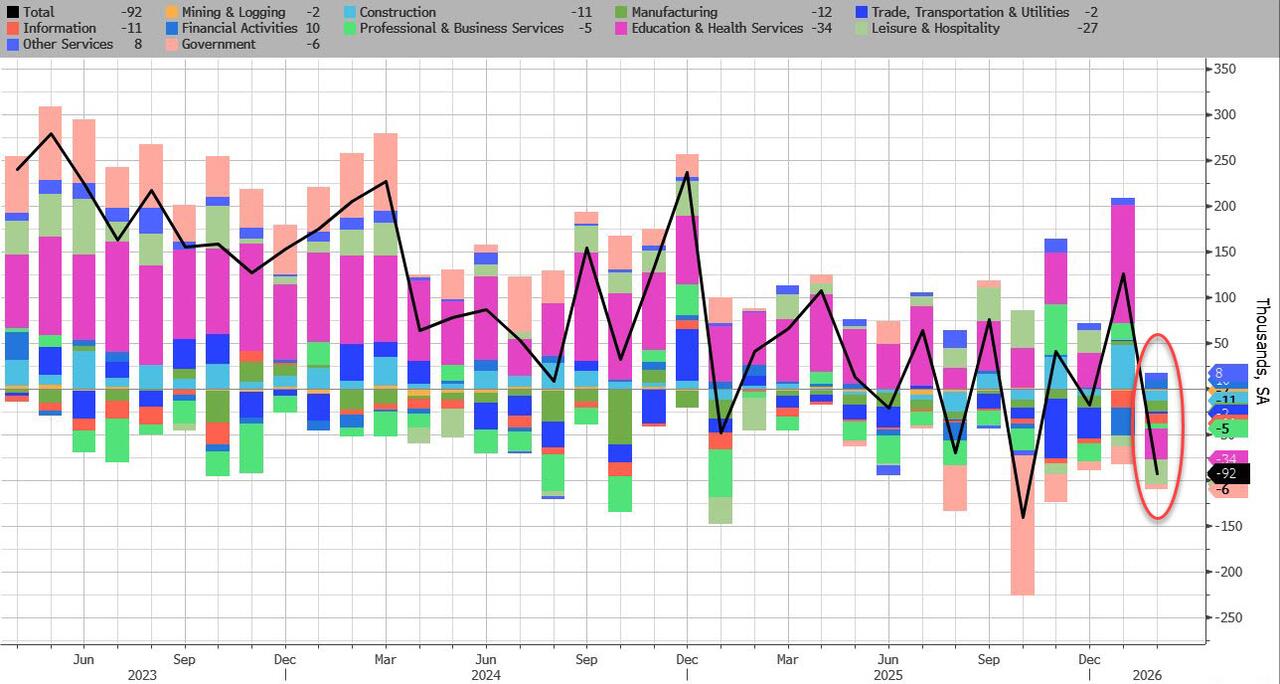

In February, the US lost 92,000 jobs, a huge drop from the downward revised 126K in January, and the second worst print since 2020 (only October’s shock -140K was worse), and this time, the massive drop can’t be dismissed as a one-time drop in government payrolls. The number of private payrolls dropped by 86K, also a huge miss to estimates of a 60K increase.

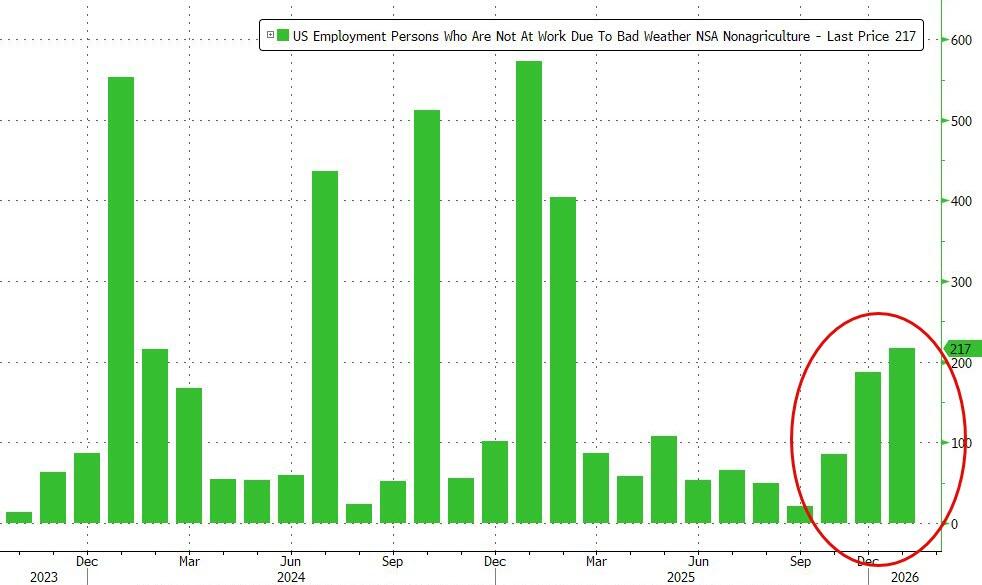

One potential mitigating factor: the number of people who were unable to work due to weather surged to 228K in February, well above last year’s level 167K, due to the powerful winter storms hitting the US.

The number of long-term unemployed (those jobless for 27 weeks or more) changed little at 1.9 million in February but is up from 1.5 million a year earlier. The long-term unemployed accounted for 25.3 percent of all unemployed people in February.

The number of people employed part time for economic reasons decreased by 477,000 to 4.4 million in February. These individuals would have preferred full-time employment but were working part time because their hours had been reduced or they were unable to find full-time jobs.

The number of people not in the labor force who currently want a job changed little in February at 6.0 million. These individuals were not counted as unemployed because they were not actively looking for work during the 4 weeks preceding the survey or were unavailable to take a job.

Among those not in the labor force who wanted a job, the number of people marginally attached to the labor force changed little at 1.6 million in February. These individuals wanted and were available for work and had looked for a job sometime in the prior 12 months but had not looked for work in the 4 weeks preceding the survey. The number of discouraged workers, a subset of the marginally attached who believed that no jobs were available for them, decreased by 109,000 in February to 366,000.

Turning to the establishment survey, which unveiled the shocking February drop, the BLS reported a broad-based decline, driven by striking employment workers:

Employment in health care decreased in February, reflecting strike activity. Employment in information and federal government continued to trend down. Payroll employment changed little on net in 2025.

Health care employment declined by 28,000 in February, following a large increase in January (+77,000). Offices of physicians lost 37,000 jobs in February, primarily due to strike activity. Hospitals added 12,000 jobs. Over the prior 12 months, health care had added an average of 36,000 jobs per month.

Employment in information continued to trend down in February (-11,000). The industry had lost an average of 5,000 jobs per month over the prior 12 months.

In February, federal government employment continued to decline (-10,000). Since reaching a peak in October 2024, federal government employment is down by 330,000, or 11.0 percent.

Employment in social assistance continued its upward trend in February (+9,000), driven by individual and family services (+12,000).

Transportation and warehousing employment changed little in February (-11,000). A job loss in couriers and messengers (-17,000) was partially offset by a gain in air transportation (+5,000). Employment in transportation and warehousing has declined by 157,000, or 2.4 percent, since reaching a peak in February 2025.

Employment showed little change over the month in other major industries, including mining, quarrying, and oil and gas extraction; construction; manufacturing; wholesale trade; retail trade; financial activities; professional and business services; leisure and hospitality; and other services.

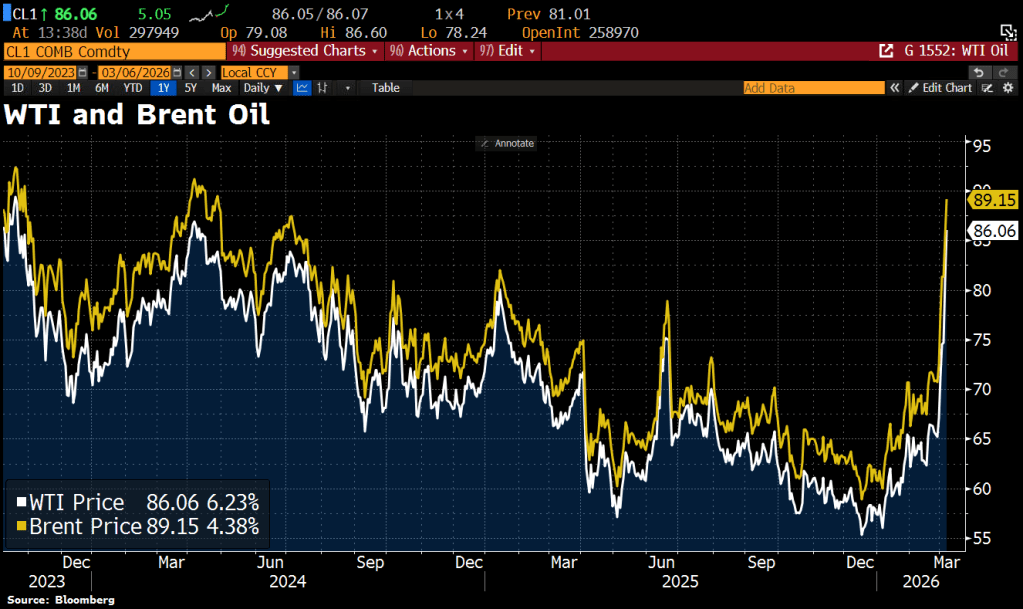

Switching to oil, we see the West Texas Intermediate and Brent Oil prices soaring on the attacks on Iran.

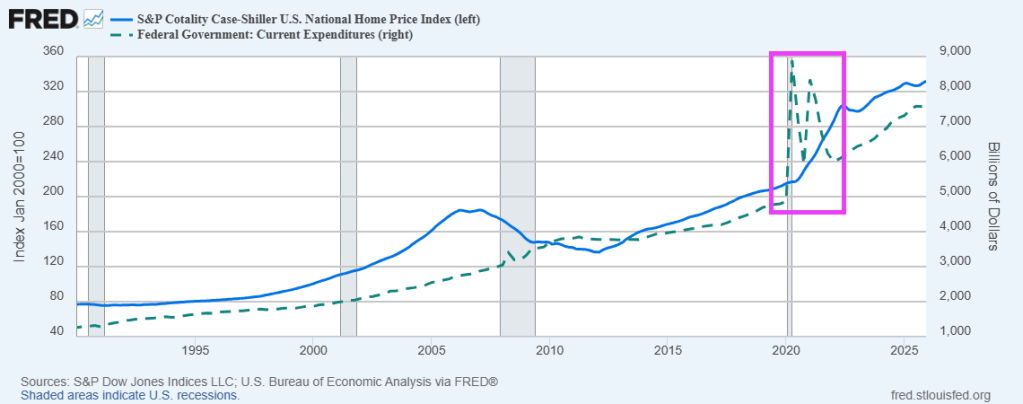

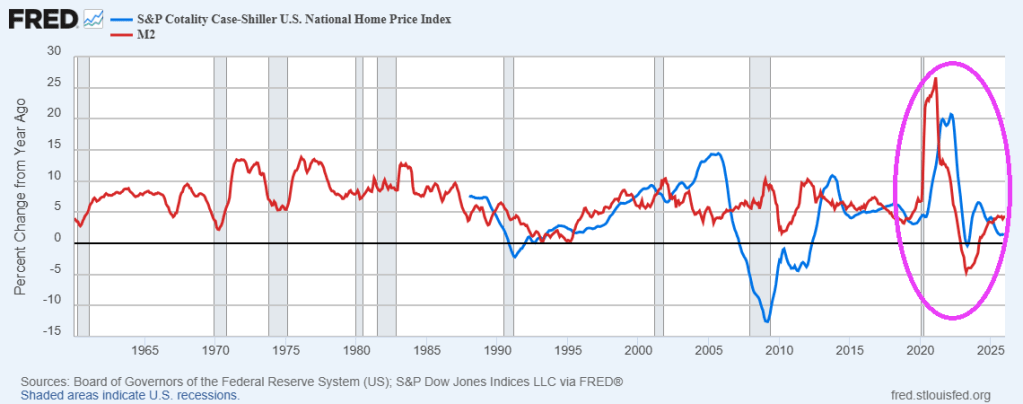

We are seeing the aftermath of the Federal government’s fiscal response to the Covid outbreak of 2020. Home prices exploded following The Federal government’s spending spree. The end result? US housing is simply unaffordable for millions of households.

Not really surprising given the soaring home prices following the Covid Federal spending spree.

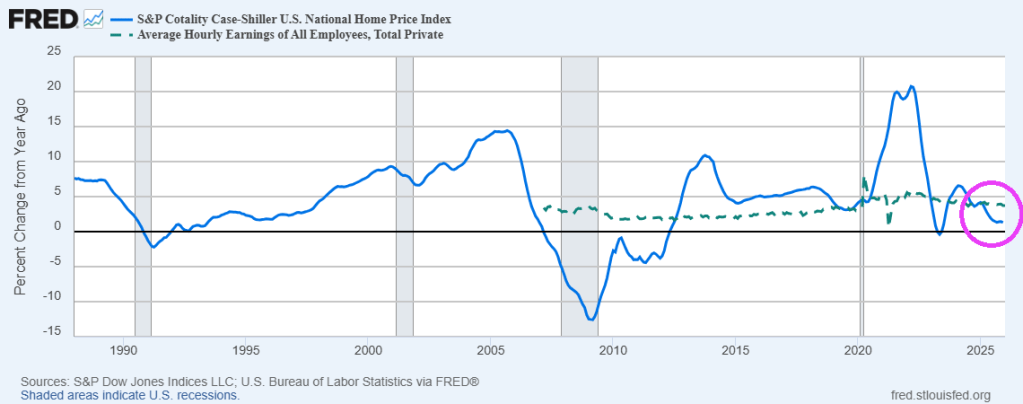

The S&P Cotality Case-Shiller U.S. National Home Price NSA Index posted a 1.3% annual gain (YoY) for December 2025, down from a 1.4% rise in the previous month. Average hourly earnings now at 3.73% YoY, higher than home price growth.

Home price growth exploded following The Federal governments’ Covid-related spending splurge.

Geographic divergence widened sharply: Chicago and New York led all markets with gains above 5%, while Tampa, Phoenix, Dallas, and Miami posted the steepest declines among markets that finished the year in negative territory.

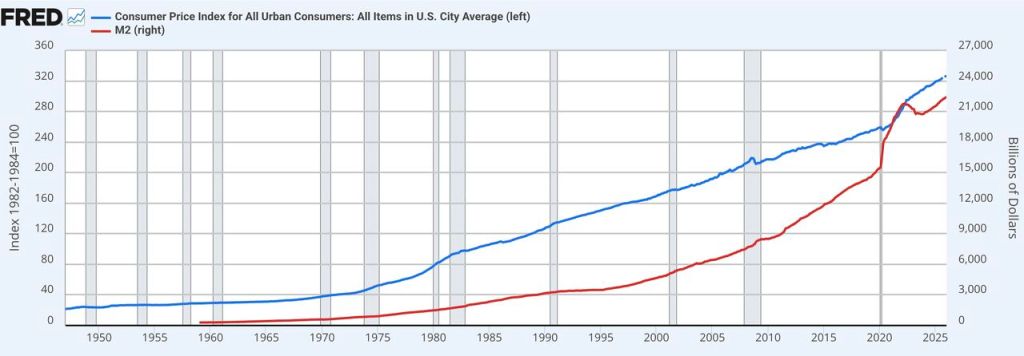

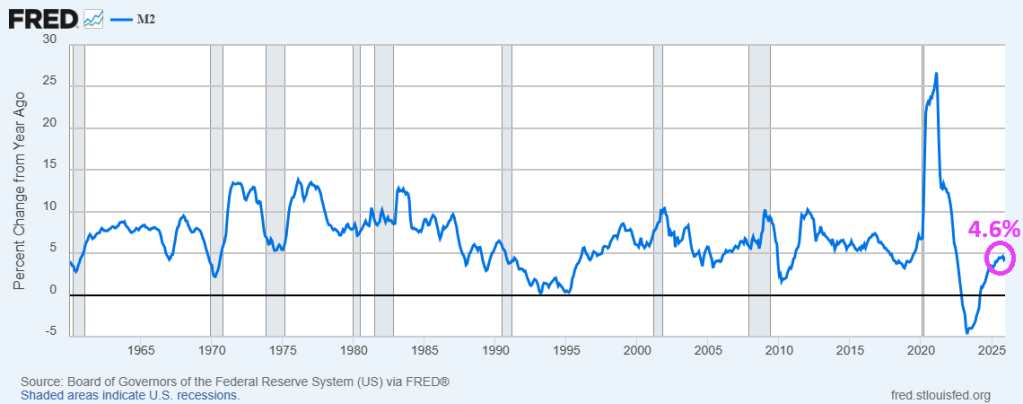

Inflation cooled significantly under Trump, but The Fed keeps printing M2!

Underlying U.S. inflation increased more than expected in December, and signs are pointing to a further acceleration in January, which would strengthen expectations that the Federal Reserve would not cut interest rates before June.

The personal consumption expenditures price index, excluding the volatile food and energy components, rose 0.4% after an unrevised 0.2% gain in November, the Commerce Department’s Bureau of Economic Analysis said on Friday. In the 12 months through December, core PCE inflation advanced 3.0% after increasing 2.8% in November.

The PCE price index increased 0.4% in December after rising 0.2% in November. PCE inflation increased 2.9% year-on-year after gaining 2.8% in November.

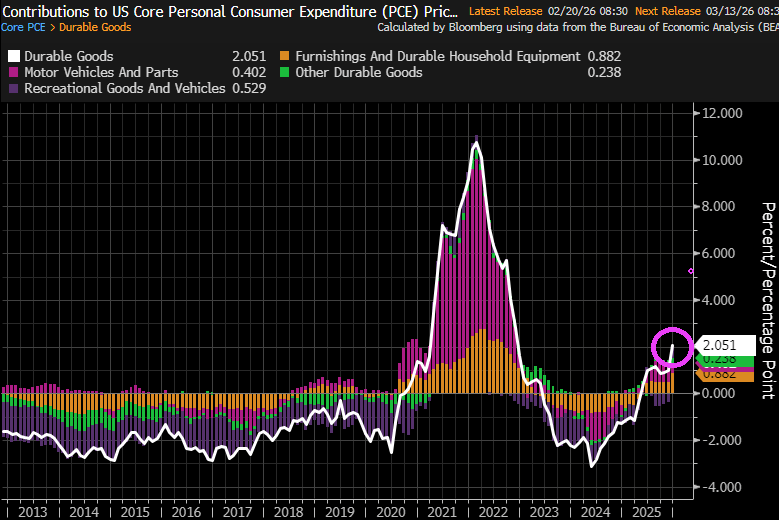

But in terms of contributions to the 0.4% figure is that durable goods rose 2.051%.

The Fed has been printing money (M2) like there is no tomorrow. With M2 growing at 4.6% YoY in December.

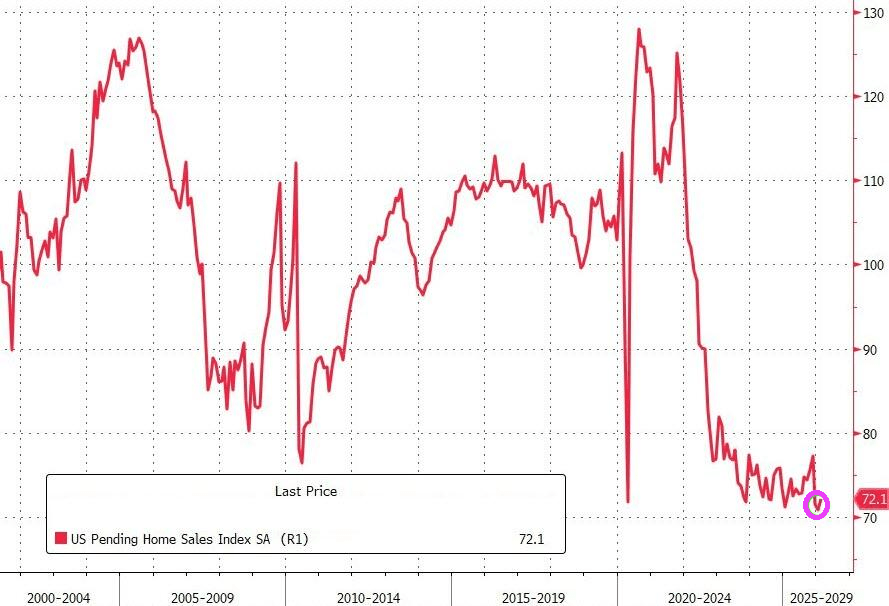

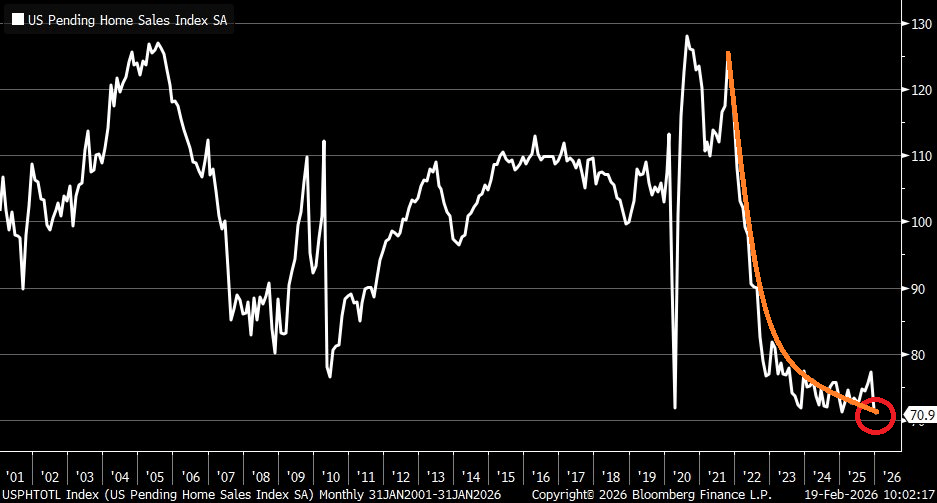

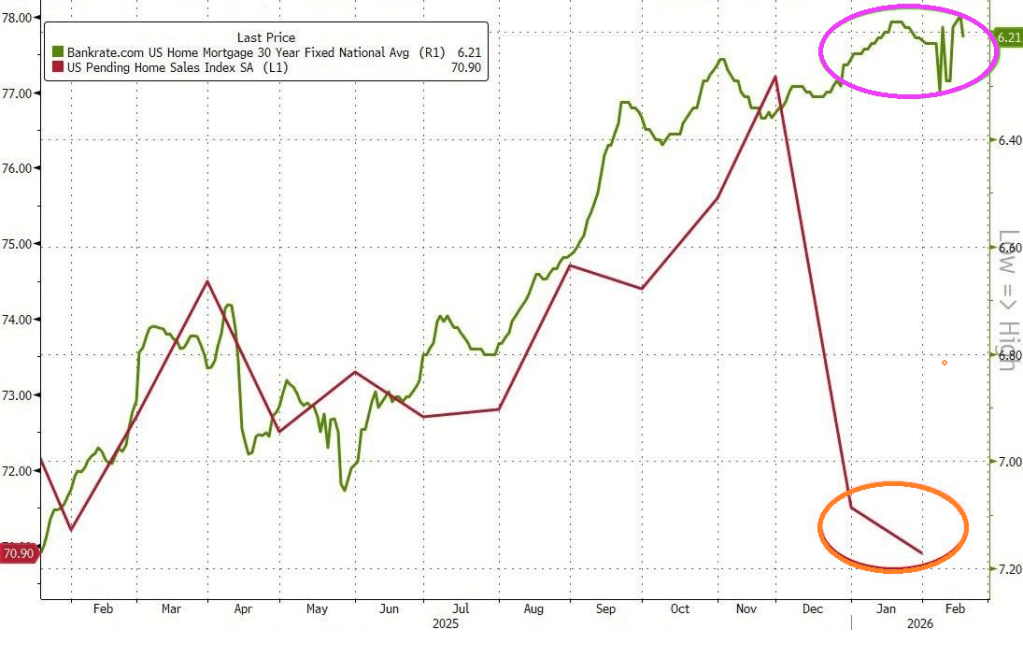

Unfortunately, US pending home sales have collapsed to the lowest level since at least 2001. Nothing has been the same since Biden/Harris administration.

Mortgage rates are still too high by historic standards.

Speaking of Democrats running the economy, New York’s mayor Zoran Mandami (the Ugandan Communist) is seeking to raise property taxes to 9.5% which will hit EVERY New Yorker, not just the billionaires he allegedly wants to tax.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.