High housing prices, high commodity prices, high interest rates. All thanks to Biden’s horrible top-down economic policies. Its as is Biden was humming “I’m going to take prices higher” while he was President.

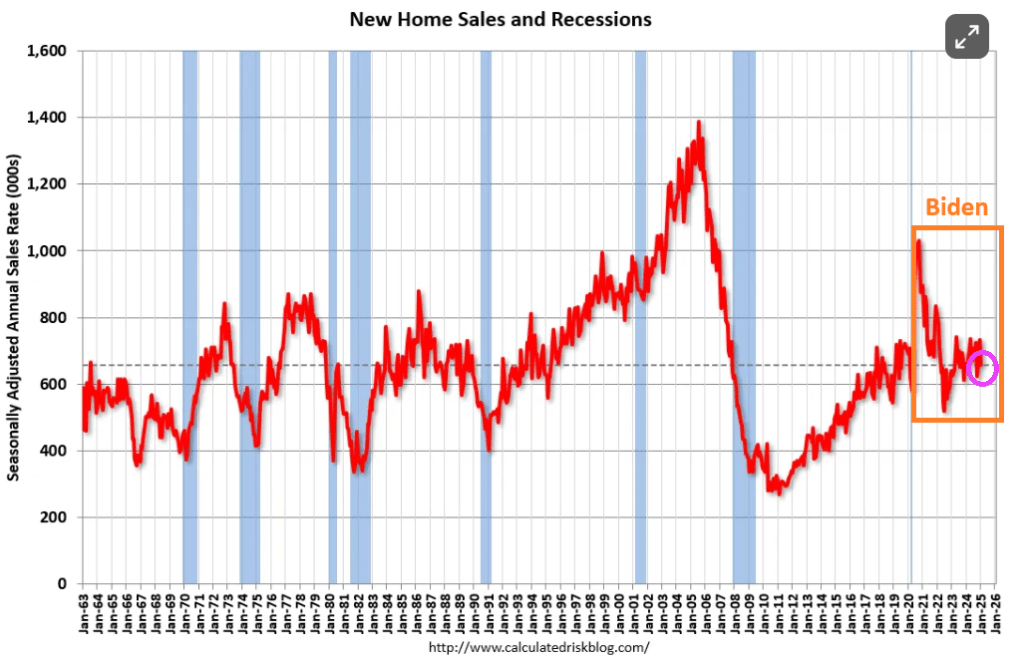

Sales of new single-family houses in January 2025 were at a seasonally adjusted annual rate of 657,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 10.5 percent below the revised December rate of 734,000 and is 1.1 percent below the January 2024 estimate of 664,000.

The most unaffordble countries are Portugal, Canada, the USA, Switzerland, and the Czech Republic. The most affordable? Romania, Finland, Italy, and Bulgaria.

For the USA, Hawaii and California are the least affordable while West Virginia and Iowa are the most affordable.

Sales of existing single-family houses, townhouses, condos, and co-ops that closed in January dropped by 4.9% from December, seasonally adjusted, to an annual rate of 4.08 million sales, according to the National Association of Realtors today.

This rate of sales was up just 2.0% from the abysmally low levels a year ago – 2024 as a whole had been the worst sales year since 1995 – and flat with the abysmally low levels two years ago.

Compared to January 2021, the sales rate was down by 36%, compared to January 2019, the sales rate was down by 25%

On a NON seasonally adjusted basis, things look even more grim.

Active inventory is up 27.6% YoY. As mortgage rates are projected to rise, things can get worse.

Mortgage rates continue to hover around 7%. Mortgage rates rose 164% under Biden!

Maybe if Fed Chair Jerome Powell is forced to wear Sky Saxon of The Seed’s wizard outfit, he will improve his policies.

I call this the house latitudes. Horse latitudes is a belt of calm air and sea occurring in both the northern and southern hemispheres between the trade winds and the westerlies. And when the ships motion stalled, the crews would jetison their cargo of horses to the delight of sharks! So, we are in state of HOUSE latitudes where the wind pushing mortgage refis and purchase apps. So we are all riders on the storm.

Mortgage applications decreased 6.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 14, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 6.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 6 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 7 percent higher than the same week one year ago.

The Refinance Index decreased 7 percent from the previous week and was 39 percent higher than the same week one year ago.

Privately-owned housing starts in January were at a seasonally adjusted annual rate of 1,366,000. This is 9.8 percent below the revised December estimate of 1,515,000 and is 0.7 percent below the January 2024 rate of 1,376,000. Single-family housing starts in January were at a rate of 993,000; this is 8.4 percent below the revised December figure of 1,084,000. The January rate for units in buildings with five units or more was 355,000.

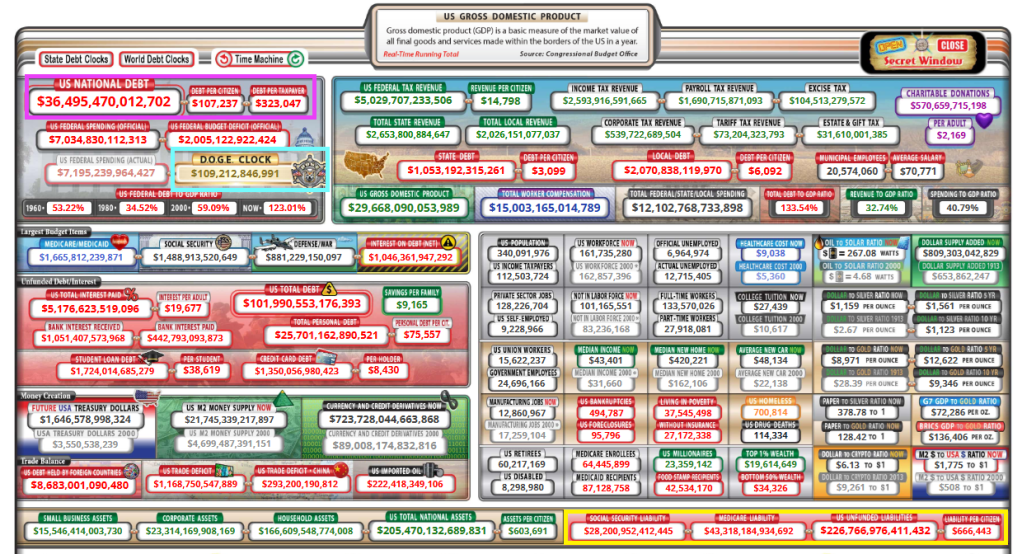

Janet Yelllen, the former Federal Reserve Chair and Treasury Secretary under clueless Joe Biden was a disaster in every respect. As Fed Chair, she was noteworthy for her clinging to low rates for too long. And as Treasury Secretary, she is noteworthy for her gross fiscal mismanagement (look at the deficit and debt crisis!). Now Zero Hedge has this disastrous report of $4.7 TRILLION in virtuallly untraceable Treasury payments.

The Elon Musk-led Department of Government Efficiency (DOGE) on Monday revealed its finding that $4.7 trillion in disbursements by the US Treasury are “almost impossible” to trace, thanks to a rampant disregard for the basic accounting practice of using of tracking codes when dishing out money.

With a debt load of $36.5 trillion and D.O.G.E. clock at $109 million and growing. Not to mention the $227 trillion in unfunded liabilities.

Mind you, it’s not as if such a federal tracking system wasn’t already in place— it simply went casually unused for all sorts of payouts adding up to an almost unfathomable $4.7 trillion. Without Treasury Access Symbol (TAS) identification codes associated with those payouts, there’s little hope in figuring out where all that money went.

“In the Federal Government, the TAS field was optional for ~$4.7 Trillion in payments and was often left blank, making traceability almost impossible,” DOGE announced via its X account. Thanks to DOGE, those “optional” days are over. “As of Saturday, this is now a required field, increasing insight into where money is actually going,” DOGE added.

DOGE’s scrutiny of various government agencies is eliciting high-pitched shrieks from nearly every leftist in America, from establishment politicians who don’t want the curtain that hides their hijinks and grifting torn down, to your liberal sister-in-law who thinks the government has an endless supply of money and that it spends it all virtuously.

Earlier this month, Treasury Secretary Scott Bessent pushed back on portrayals of DOGE employees as reckless rogues. “These are highly trained professionals,” he told Bloomberg. “This is not some roving band going around doing things. This is methodical and it is going to yield big savings.”

In the wake of the latest revelation that makes normal people glad that DOGE teams are scouring the federal government, Democrats desperately tried to find a way to make it sound bad that DOGE exposed trillions in untraceable payouts and promptly instituted tighter accounting discipline.

Meanwhile, leftists have also been foaming at the mouth over news that DOGE staffers are looking into the Social Security Administration’s (SSA) books, as if they were going to start rerouting funds to Tesla. Considering Social Security is careening toward mandatory benefit cuts as soon as 2033, everyone should welcome a team of financial professionals making sure the system isn’t being drained by improper payments.

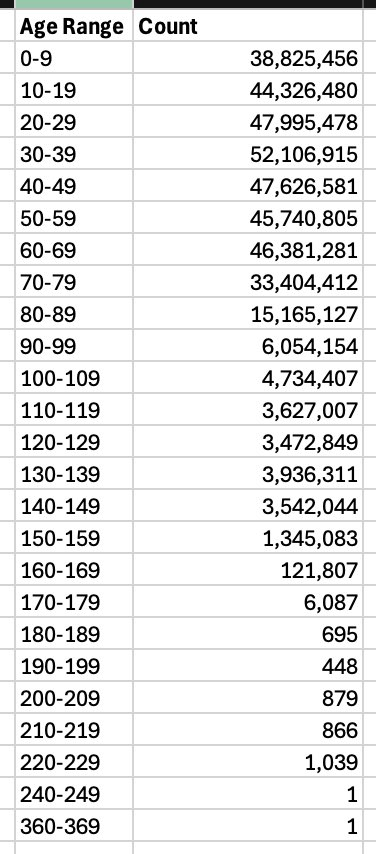

Of course, that appears to be exactly what’s been happening. On Sunday night, Musk said DOGE might be on the trail of “the biggest fraud in history,” as SSA data appears to show that 20.789 million Americans over the age of 100 are collecting Social Security retirement benefits. That includes 12 million who are purportedly over 120 years old.

Bent on derailing DOGE, Democrats have sued to prevent the organization from accessing federal data associated with the Office of Personnel Management, and the Health and Human Services, Education, Energy, Transportation, Labor and Commerce departments. On Monday, the federal judge handling the request for a restraining order expressed skepticism over Democrats’ challenge, noting that their “evidence” was largely media speculation about potential harms springing from DOGE’s activities: “The courts can’t act based on media reports. We can’t do that.“

A ruling is expected Tuesday. Here’s looking forward to DOGE proceeding to uncover a relentless string of scandals for months and months to come.

The left has come out in force to attack D.O.G.E. and Elon Musk. Why? First, The Left doesn’t want to upset the candy apple cart (government waste and corruption). Second, the Left wants to pretend that they hate the rich (although George/Alexander Soros are huge donors, not to mention Bill Gates and most of Hollywood elites are billionaires/millionaires). But the saddest act of all are Joe Biden and Kamala Harris. These two clowns had the Social Security data and never looked at it … allegedly.

What would they have found if they had looked at the Social Security books? According to Elon Musk, they would have discovered 20,788,904 people at the age of 100 and above. That is significantly higher that the entire population of Naples Florida at 19,704.

Here is what Elon Musk discovered about people receiving Social Security (and disability payments). Joe and Kamala didnt notice someone that was between 360 and 369 years of age??

The point is that this is a collosal embarrasment. And epic fraud. And even more vexxing is that 394,943,364 are collecting Social Security while the total population of the USA is 334 Million?? That leaves 60 million more people receiving Social Security payments than there are people in the USA!

Don’t tell Elon about candied apples that have replaced government cheese in the Federal government giveaway program for votes!And Cloward/Piven!

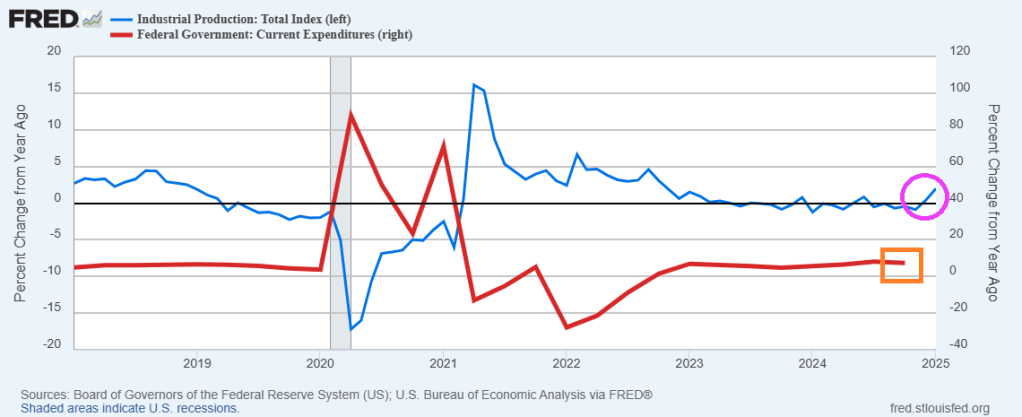

In January, US Industrial Production rose 2.00% YoY, the strongest growth rate since Oct 2022.

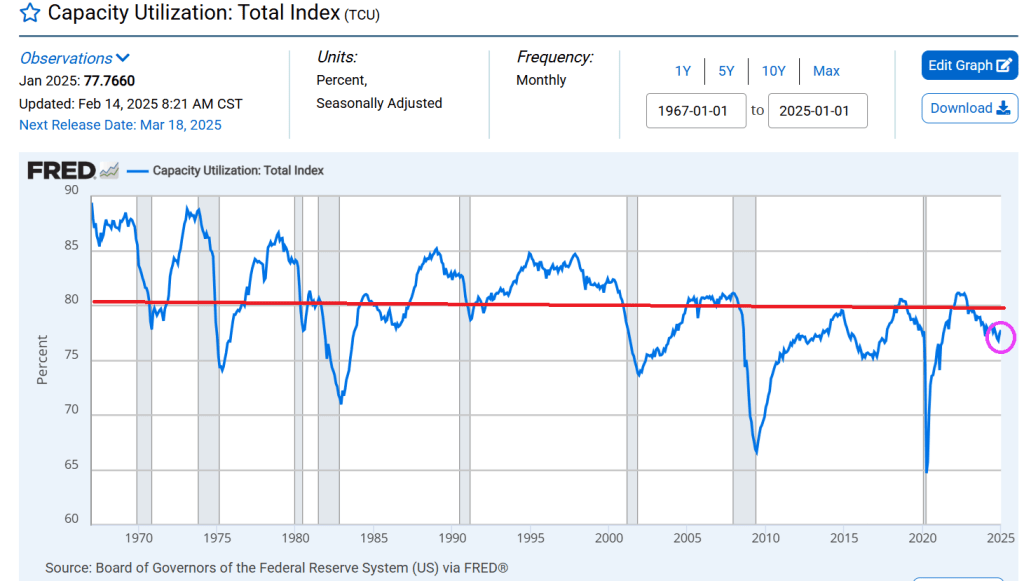

Capacity Utilization accelerated again in January (2nd straight month), rejecting the recessionary red flags. But CAPUTE remains below the critcal measure of 80.

Biden is out and so are the crazy job preferences of his administration (e.g., green energy). There is a new sheriff in town (Donald Trump).

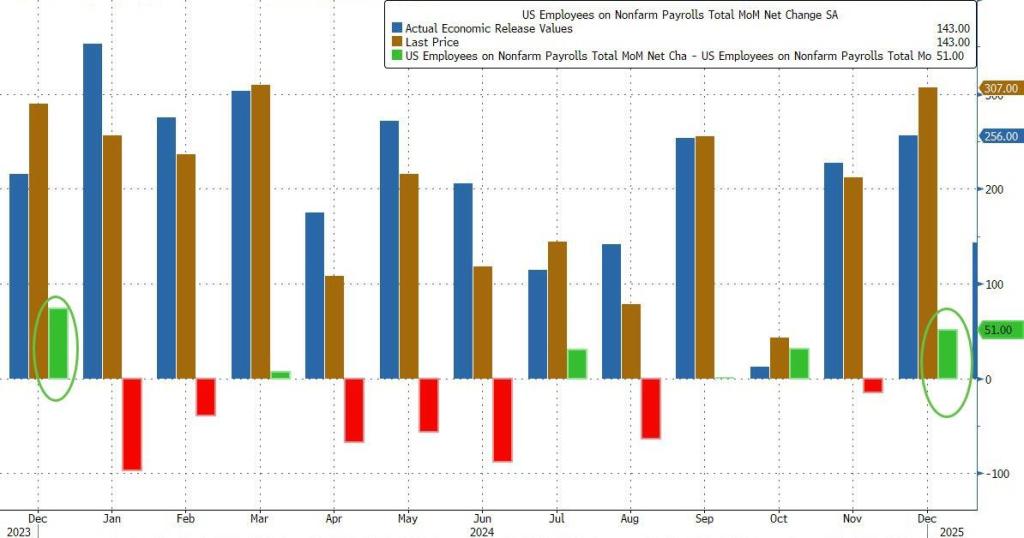

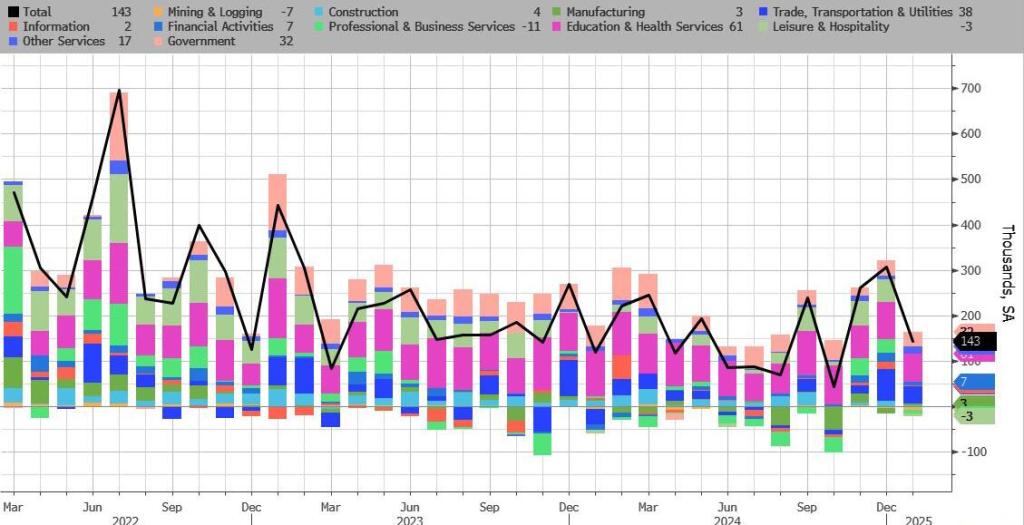

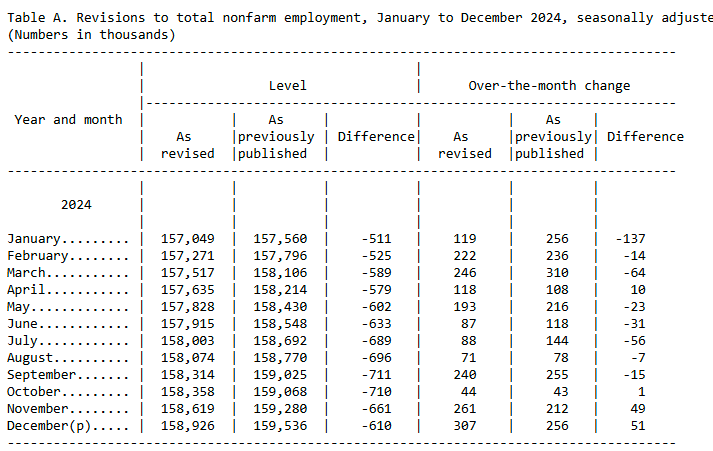

Here’s what the BLS reported in Trump’s first official jobs report since he returned to the White House: total payrolls printed at 143K.

down sharply from an upward revised 307K (256K originally) and missing estimates of 175K.

Looking further back, the change in total nonfarm payroll employment for November was revised up by 49,000, from +212,000 to +261,000, and when adding the +51,000 revision to December employment in November and December combined is 100,000 higher than previously reported

But while the sequential change in the Establishment survey was notable, what was far more remarkable was the Household survey where we saw massive population related revisions (discussed last night), which pushed the civilian labor force higher by 2.2 million to 170.744 million, while the number of employed workers also increased by over 2.2 million to 163.895 million. As a result, the Household survey has finally caught up to Establishment survey.

No, its not 1903. Its 2025 and Dayton Ohio is the third most affordable city in the USA.

Ohio, the cradle of American Presidents (McKinley, Grant, Taft, Benjamin Harrison, Hayes, Garfield, Harding), is also home to 4 of the most affordable cities in the USA, according to The Virtual Capitalist.

As expected, the Trump Administration levied tariffs against Canada, Mexico, China, etc. The short-term result? Gold is stable, Bitcoin fell. Or as Gene Autry sang, “South of the Border (Down Mexico Way)”.

The stock market? Down -1.53%.

And then we have the doom porn about Mexico’s “impending” collapse. The Peso is declining, and Senator Chuck Schumer is getting hysterical about Mexican exports to the USA for Super Bowl Sunday. He incorrectly claimed that most beer is imported from Mexico and avacados for guacamole. Avacados are also grown in the USA, Peru, etc.

Bear in mind that Mexico is like California where the Left holds a supermajority. Hence, Mexico employs destructive economic policies (it could only be worse if California Governor Gavin Newsom was President of Mexico. But Mexico’s impending collapse is years in the making and Trump’s tariffs were only the last nudge over the cliff. Mexico COULD try to get control over the drug and human trafficking cartels, stop illegal immigration and stop the flow of fentanyl.

You must be logged in to post a comment.