Big bubbles! US home pricest hit an all-time high as The Fed keeps its foot on the monetary gas pedal following the Covid economic shutdown in 2020.

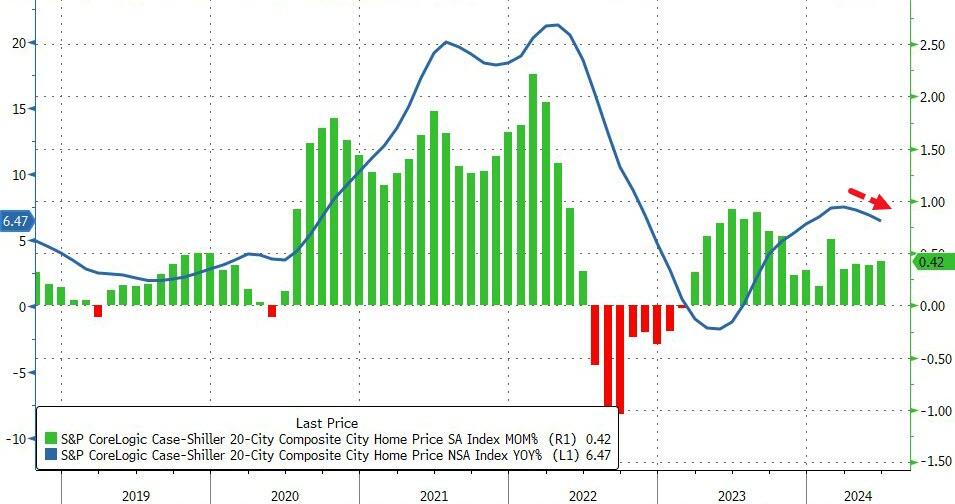

Home prices in America’s 20 largest cities rose for the 16th straight month in June (according to the latest data from S&P CoreLogic – Case Shiller – data today), up 0.42% MoM (hotter than expected and accelerating from May). On a YoY basis, prices rose 6.47%, but notably that is the third straight monthly slowdown in the pace of price appreciation…

Source: Bloomberg

Overall, US home prices reached a new record high in June (as median new home prices continued to tread water)…

Source: Bloomberg

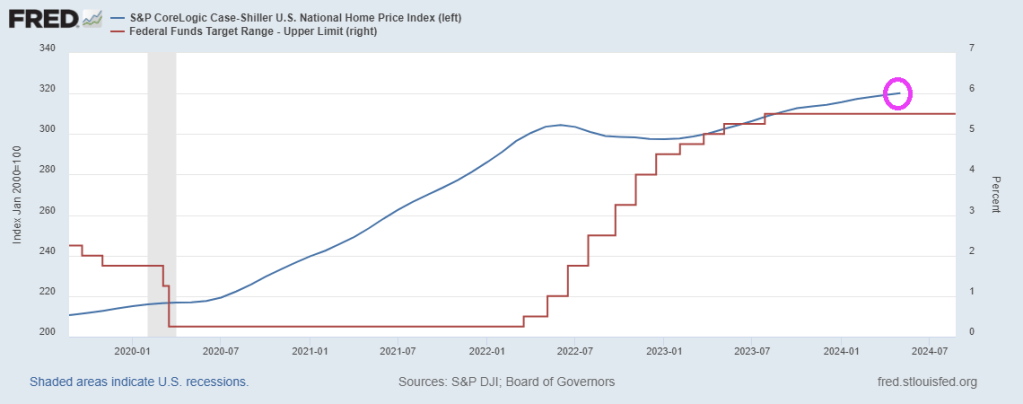

Home prices continue to track Fed Reserves closely, but a turning point may come soon…

Source: Bloomberg

Given the smoothing and heavy lag in the Case-Shiller data, it’s hard to find a causal relationship between prices and mortgage rates…

Source: Bloomberg

But, with prices reaccelerating and mortgage rates already back below 7.00% – in anticipation of The Fed – WTF does Powell think is going to happen when he actually starts cutting with prices at these record highs.

The Freddie Mac HP index shows the variation in home price growth. New Jersey coastal towns of Atlantic City and Ocean City grew at 10% YoY while Lake Charles LA declined by -2% YoY.

Combined Biden/Harris’ spending spree with The Fed’s monetary goonery and we got inflation (gasoline, food, shelter). With spiraling inflation in mortgage rates and shelter prices we saw a correponding decline in existing home sales under Biden/Harris.

Harris claims to lower prices on her first day in office (she has been in office as VP since 2021 and actually voted in the US Senate as tie breaker to enact policies that INCREASED Inflation). But her suggestion of $25,000 for ALL first time homebuyers is of course INFLATIONARY. And her anti-price gouging policies willl of course reduce supply of groceries avaiable, driving up INFLATION.

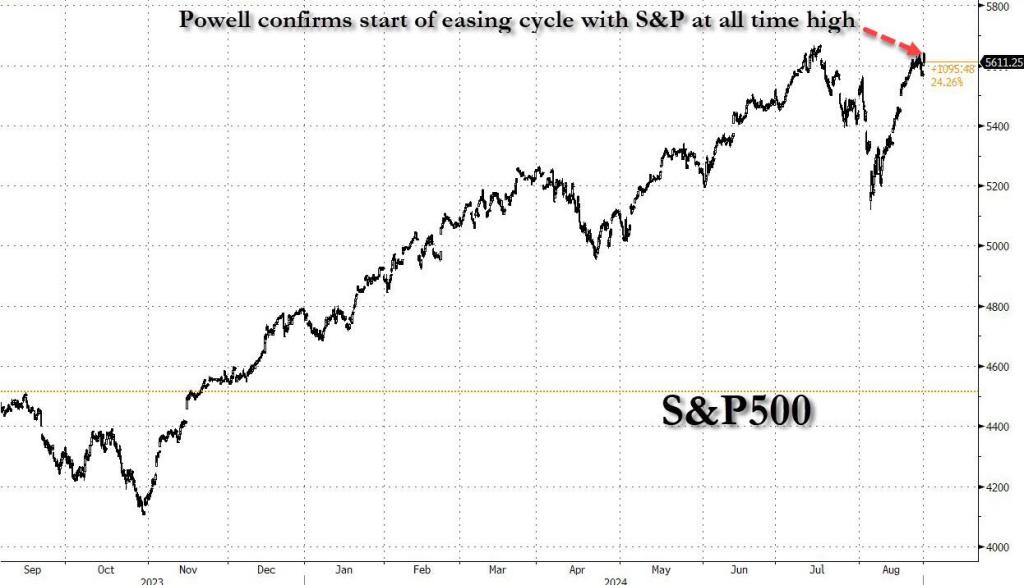

Having put inflation fully in the rearview mirror, the “Powell payrolls pivot” is now complete because as the Fed chair said, “the cooling in labor market conditions is unmistakable” even if it was quite mistakable to the Biden admin’s presstitutes as recently as one month ago.

Which is also why it was imperative for the Biden labor department to admit the truth about the deteriorating labor market: without that -818K revision earlier this week, the Fed would have some pushback to turning fully dovish. But now that we know that a third of the job gains in the last year of Bidenomics were bogus…well, please come save us Chairman Fed.

Or, as TradeStation head of strategy David Russell said, “here comes the punchbowl. Jerome Powell came out swinging today with a litany of dovish signals. He said inflation is on a sustainable path lower and talked about how the job market has cooled to pre-pandemic levels. He drove the point home with a clear call for adjusting policy.”

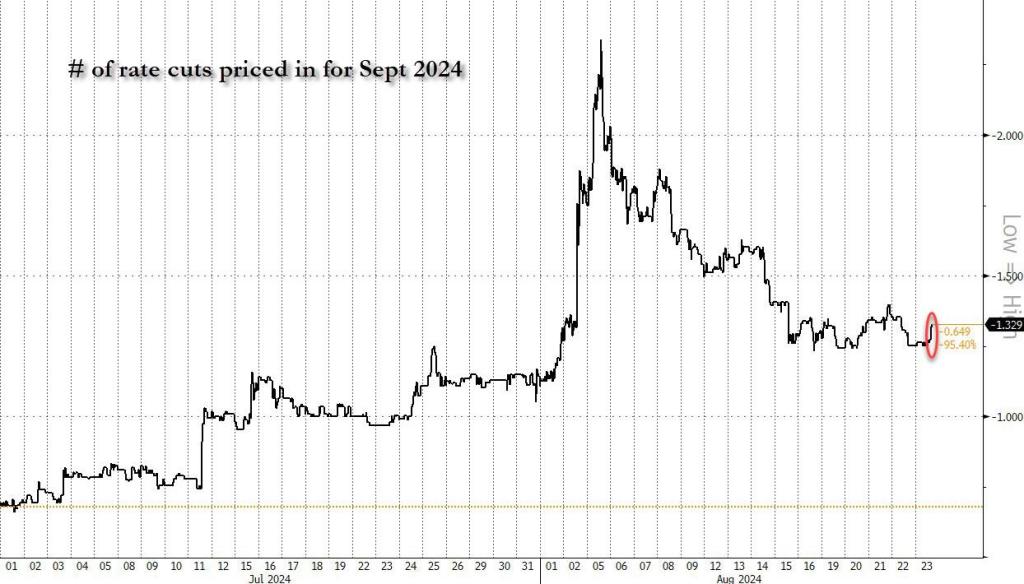

The market agreed, and quickly cemented at least one rate cut while also pricing in as much as 33% odds of a 50bps rate cut.

Which is all great: after all as we have long said, with the November elections looming, the Fed will do everything to make sure the establishment candidate isn’t distracted by such trivial things as a market crash.

There are just four small problems with this.

First: the Fed will end its tightening cycle and starts the next easing cycle with stocks at all time highs, something that has never before happened in the history of capital markets!

It means that, unless the current expansion ends in a gruesome recession which crushes the economy, the S&P is about to enter a full-blown bubble, which in turn will burst in even more spectacular fashion and force the Fed to not only cut back to ZIRP, but activate NIRP (just like Japan did years ago) and also go right back to QE and buying bonds ETFs. For now, however, as in the next three months ahead of the elections, all shall be well and should serve the all time high in the market to Kamala Harris on a silver platter…. which is precisely why the Fed is doing what it is doing.

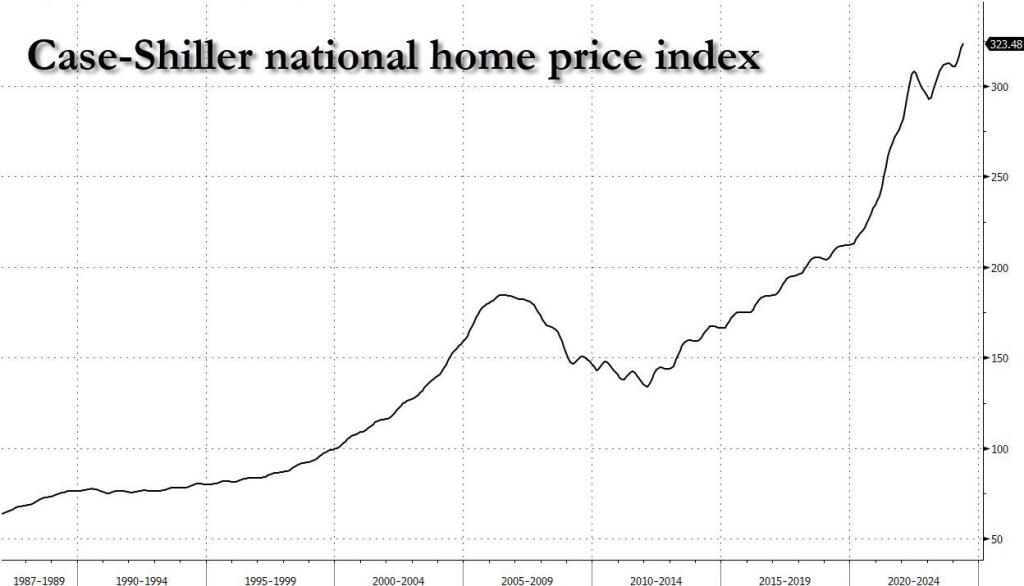

Second, this is also the first time in history when the Fed has aborted a tightening cycle having achieved zero home price easing. Indeed, one look at the case-shiller index shows that home prices are the highest they have ever been…

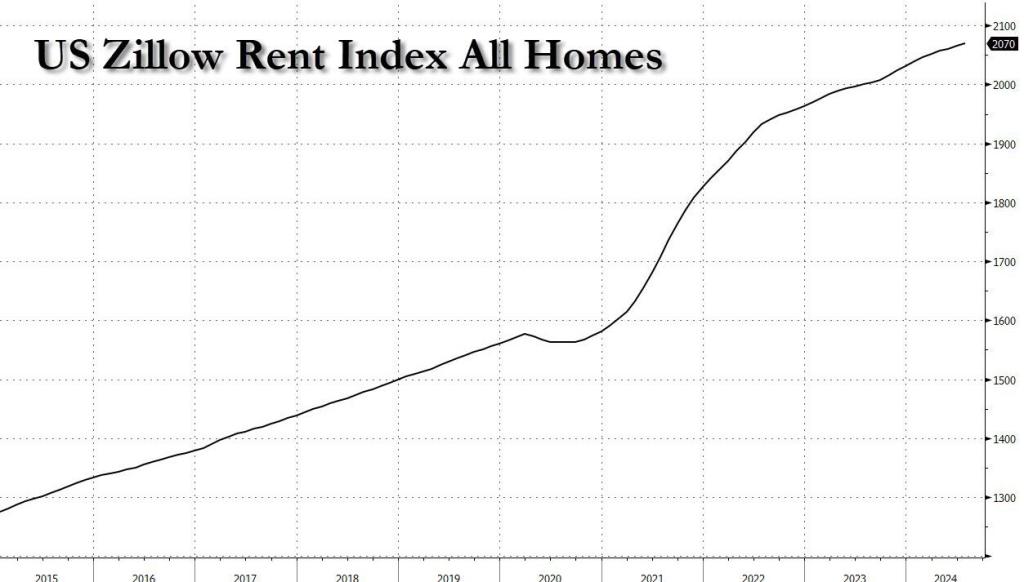

… as are actual asking rents according to Zillow (not that delayed aberration known as Owner-Equivalent Rent).

And then you have Kamala’s promise to provides $25,000 in new home purchase subsidies, which will go straight to the asking price, sending prices even higher.

In short, both home prices and rents, already at record high, are about to go record-er…

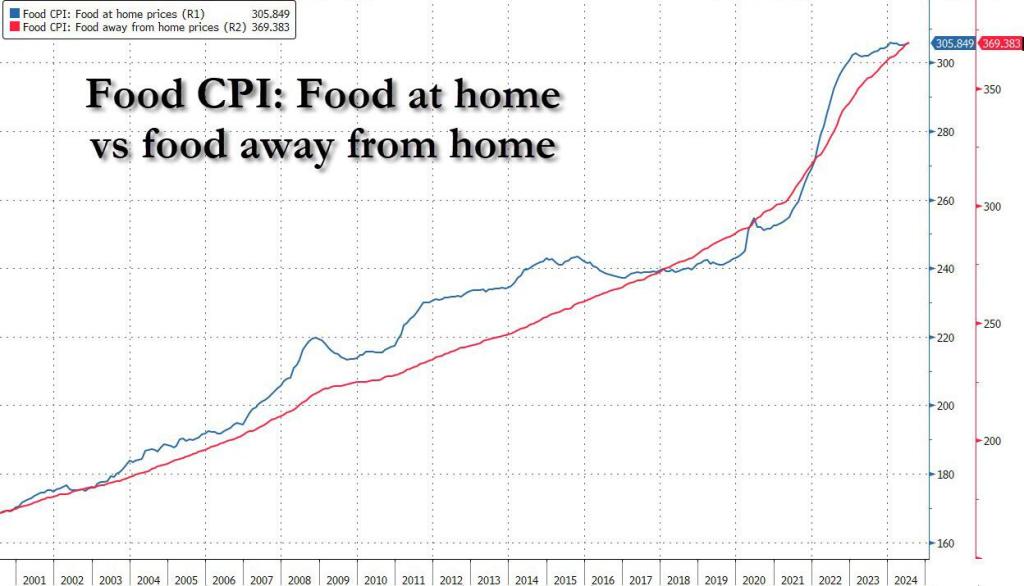

Third, while one can technically live without housing or rent, one still needs to eat. And here we find another problem, because not only did the Fed’s rate hikes not contain stock, home or rent prices, but food prices – both at home and away from home – are also at all time high! And guess what cutting rates and stimulating the economy will do to food prices from this point on…

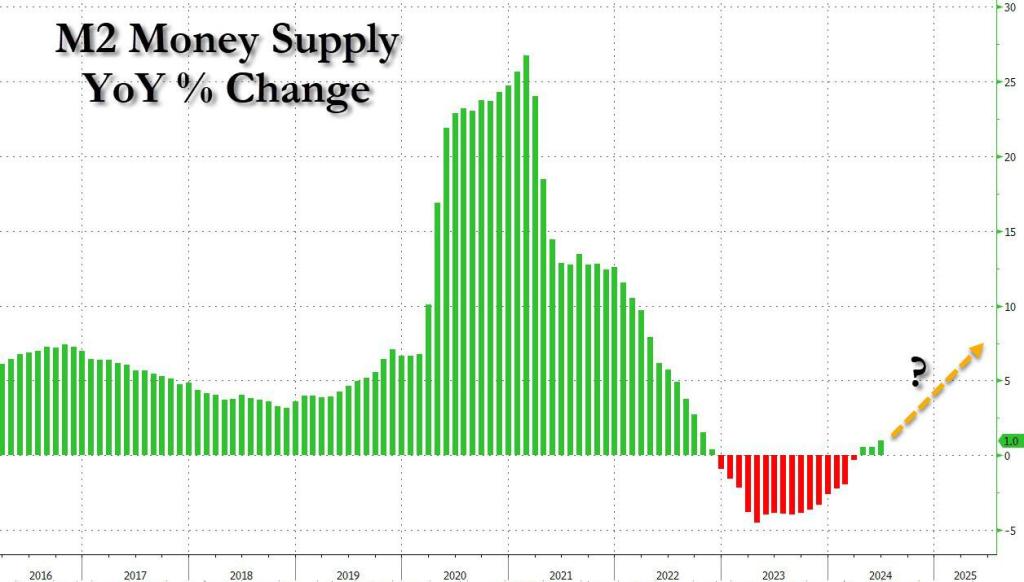

Fourth, and final, the seeds of the next inflationary bubble are already set, because even as the Fed kept conditions tight (or even exceptionally tight), M2 – the broadest money aggregate tracked by the Fed – is once again rising after declining for the past three years.

Of course, there are countless other examples, because besides the above case studies, prices are at all time highs pretty much everywhere else too. But you get the message. The only question is what can possibly go wrong with the Fed launching an easing (i.e., monetary stimulus) cycle with prices for pretty much everything, stocks and homes included, at all time highs and rising.

After watching the Democrat hate fest last night (Aka, the Democrat National Convention), I was not shocked that the DNC platform looked like a playbook to destroy the US economy. High taxes, endless spending, more regulations, etc. Not a word about the staggering side of the US debt load … with Harris’ economic plan projected to add a whopping $25 trillon in debt to the already massive $35+ trillion debt load.

And not a mention that US interest payments on the national debt already exceeds defense spending. And is booming!

Of course, Harris’s economic vision is a continutation of Biden’s disastrous visions (which are Obama’s vision of US obliteration). Most politicians in Congress are millionaires (including Bernie Sanders) and won’t suffer from their insane “progressive” policies. Watching last night’s DNC hatefest was like watching nasty 2nd graders having a party.

Of course, the drove of anti-American, anti-properity speakers spewing venom (I hate Hillary’s flat-tone speaking style) like Hillary, Jaime Raskin (aka, Rasputin), AOC, etc. all failed to acknowledge to acknowledge the already monstrous size of the US debt ($35+ trillion) or the massive size of the unfunded promises ($218+ TRILLION). Of course not.

The handle the staggering interest payments that will crowd out other spending, The Federal Reserve will be forced to lower rates.

Of course, Democrats will wheel out “economists” like Robert Reich who say that the debt doesn’t matter.

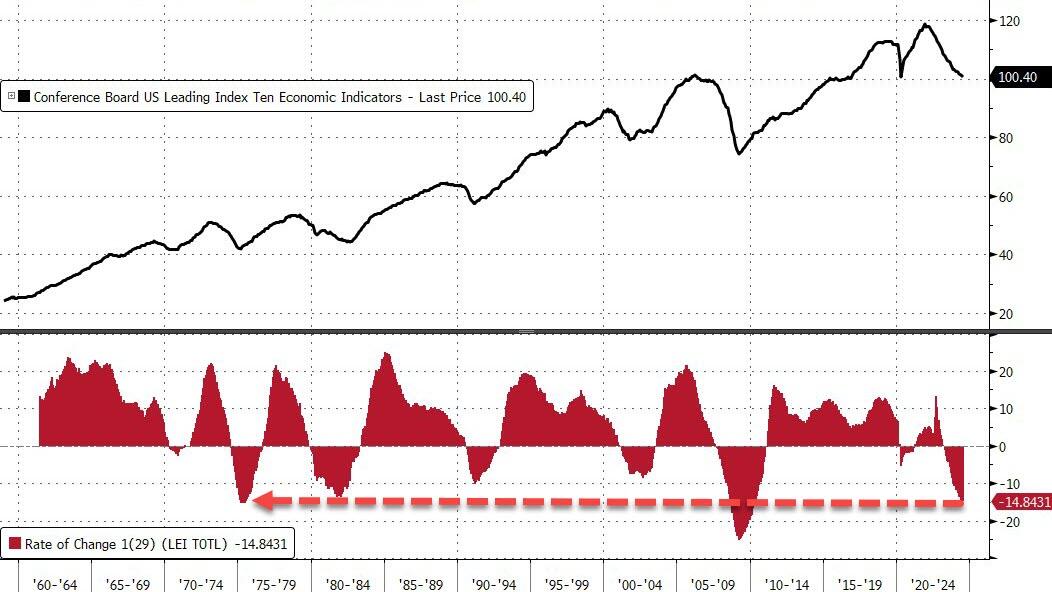

…and the head of The Conference Board says ‘nothing to see here’…

“The LEI continues to fall on a month-over-month basis, but the six-month annual growth rate no longer signals recession ahead,” said Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators, at The Conference Board.

For context, outside of the great financial crisis, this is the worst decline in LEI since the mid ’70s!!!

And what is behind the ‘no recession’ call… US equity strength!!

Thank The Feral Reserve for the equity spike!

So, to summarize – almost all the macro data signals weakening growth for years… but because stocks are up (and credit spreads down), there’s no recession anywhere on the horizon!!??

Harris has released her “vision” for the US economy, but it is what you would expect. $25k subsidy for first-time homebuyers which will make housing even MORE expensive. According the University of Michigan consumer survey, buying conditions for housing has already plummeted to 21, the lowest in history.

Cause? Already high housing prices and relatively high mortgage rates.

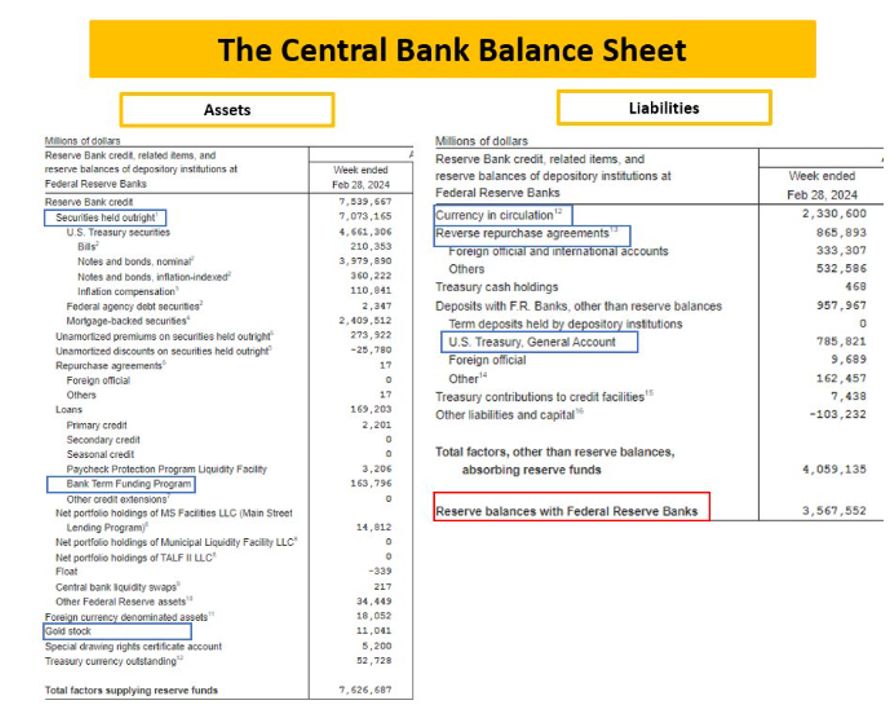

Kamala Harris, despite being VP for almost 4 years, is going to annouce her plans for taming inflation. Why doesn’t she do it now?? What Harris can’t control is The Federal Reserve that is losing money at breakneck speed.

Here is The Fed’s balance sheet.

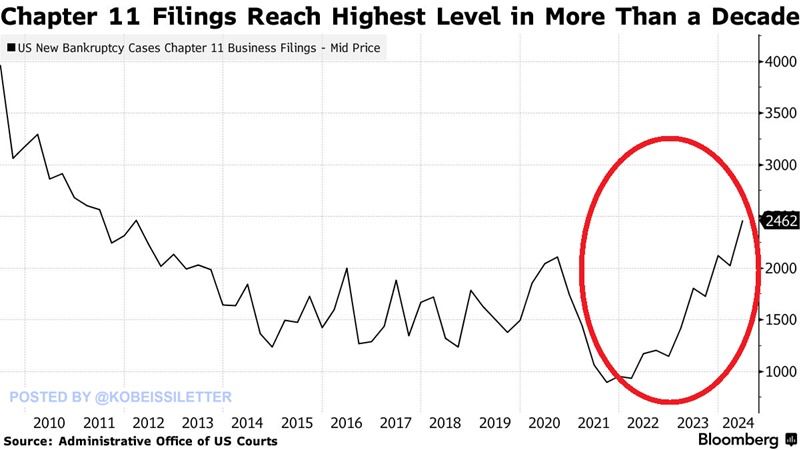

I shudder to think what Harris will propose to solve the highest bankrupty (Chap 11) rate in 13 years. Probably more Bidenomics (big wealth transfers to large corporations/donors).

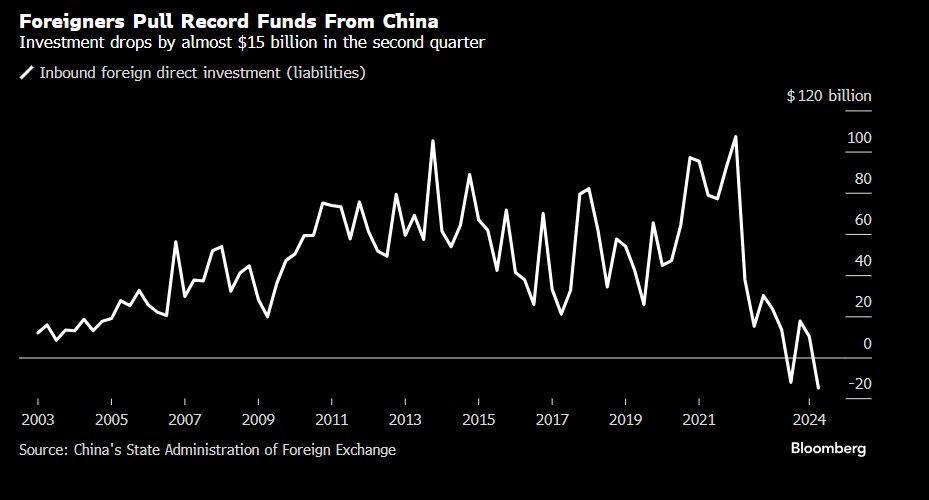

Meanwhile, foreigns pulled a record amount of funds from ailing China.

Kamala Harris will say anything to get elected, then fall back on her Communist agenda.

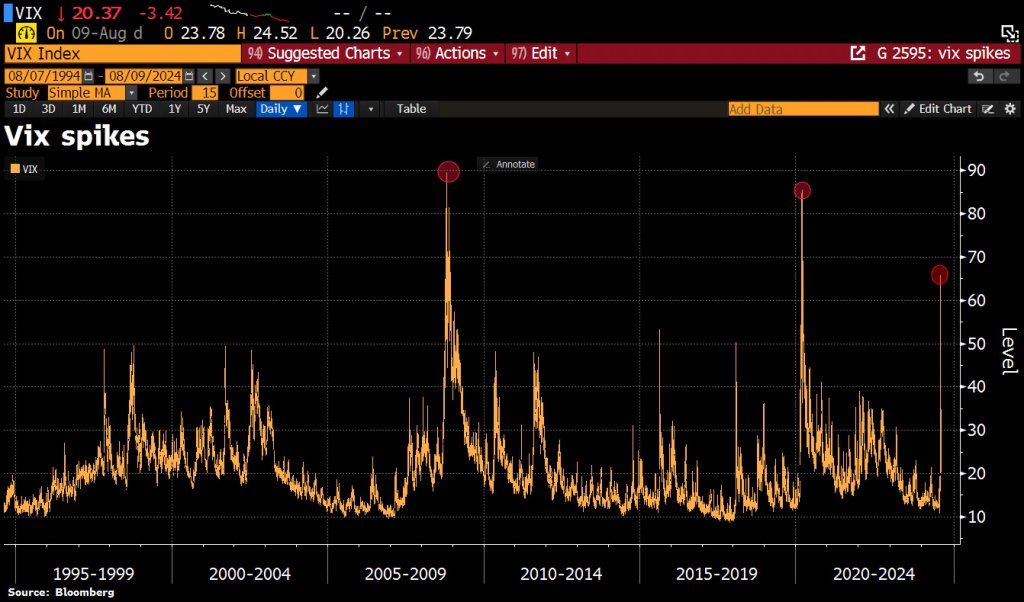

I have another use for VIX … to wipe out stock market gains. VIX is the S&P 500 volatility index, also known as “The Fear Index.”

Over the last 35yrs, the whole life of VIX history, there have only been 2 prior episodes of VIX trading >60: The 1st was during GFC, the collapse of Lehman, the 2nd episode occurred during Covid and we had a 3rd occurrence: that was last Monday.

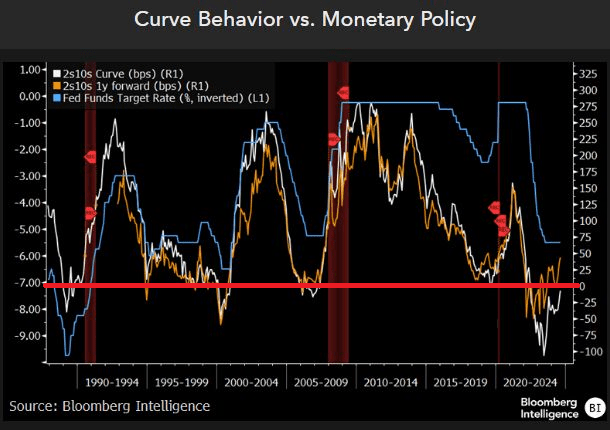

We know several things about the yield curve. First, it goes negative before recessions. Second, it is related to the inverse of The Fed’s target rate (blue line).

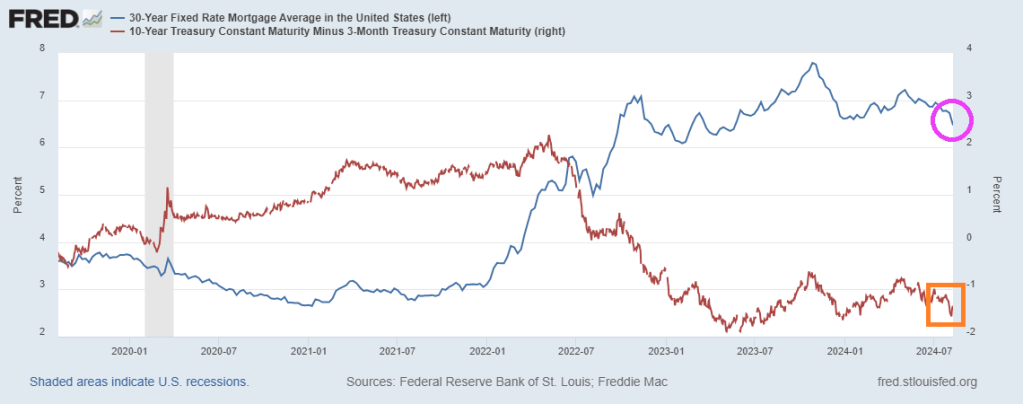

How about the US mortgage rate? Generally, US Mortgage rates are inverse to the 10Y-3M yield curve, but lately the US mortgage rate (pink circle) have declined with the 10Y-3M yield curve.

The yield curve does forecast recessions, but is unreliable in forecasting mortgage rate movements.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.