It will take a while to recover from Biden’s “Reign of Error.” According the US Census Bureau, housing starts are 6.0 percent below the August 2024 rate.

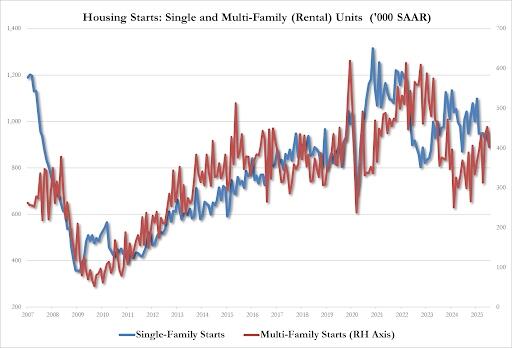

Housing starts:

- Single-family 890K SAAR, down 7.0% from 957K in July and the lowest since July 2024

- Multi-family 403K SAAR, down 11% from 453K in July and the lowest since May.

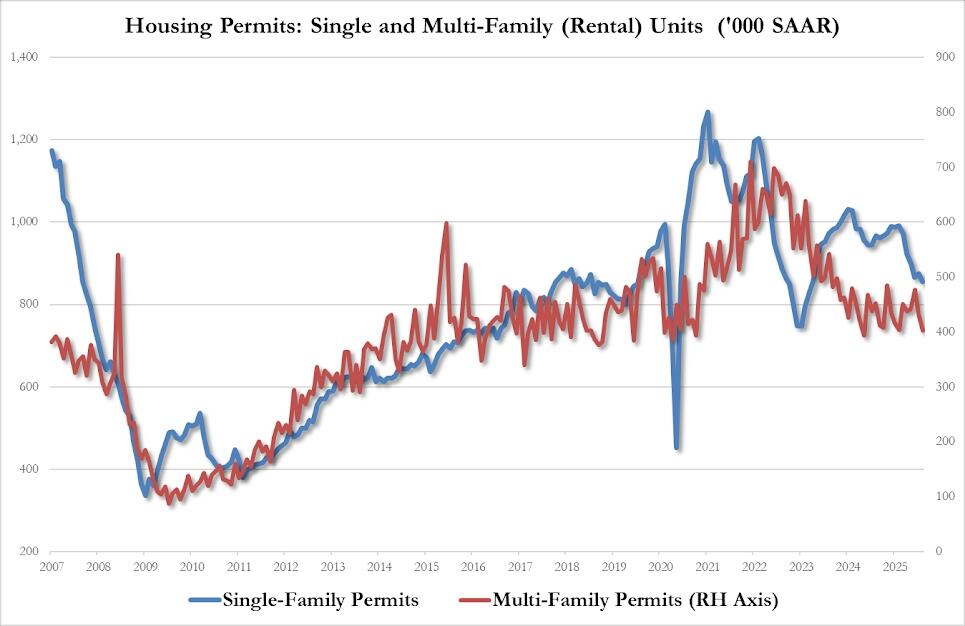

Housing permits?

- Single-family 856K SAAR, down 2.2% from 875K in July and the lowest since March 2023

- Multi-family 403K SAAR, down 6.7% from 432K in July and the lowest since May 2024

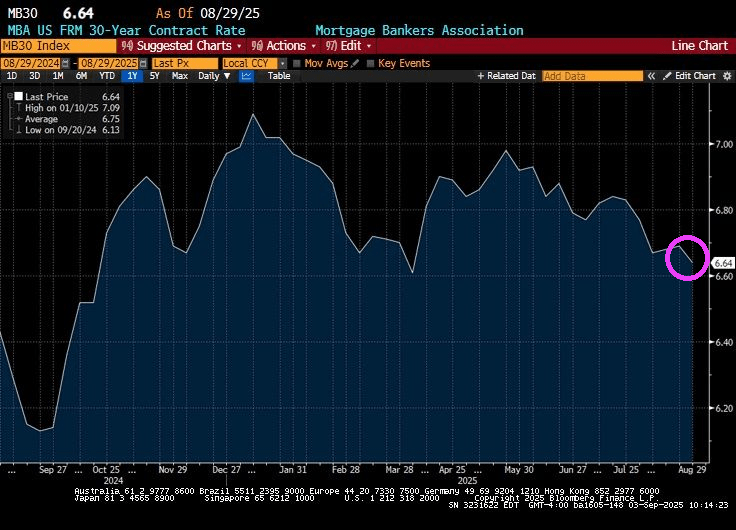

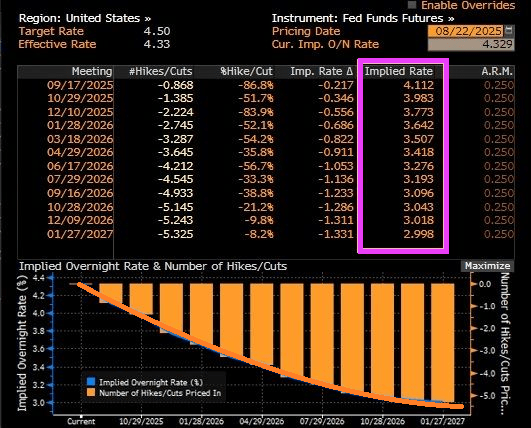

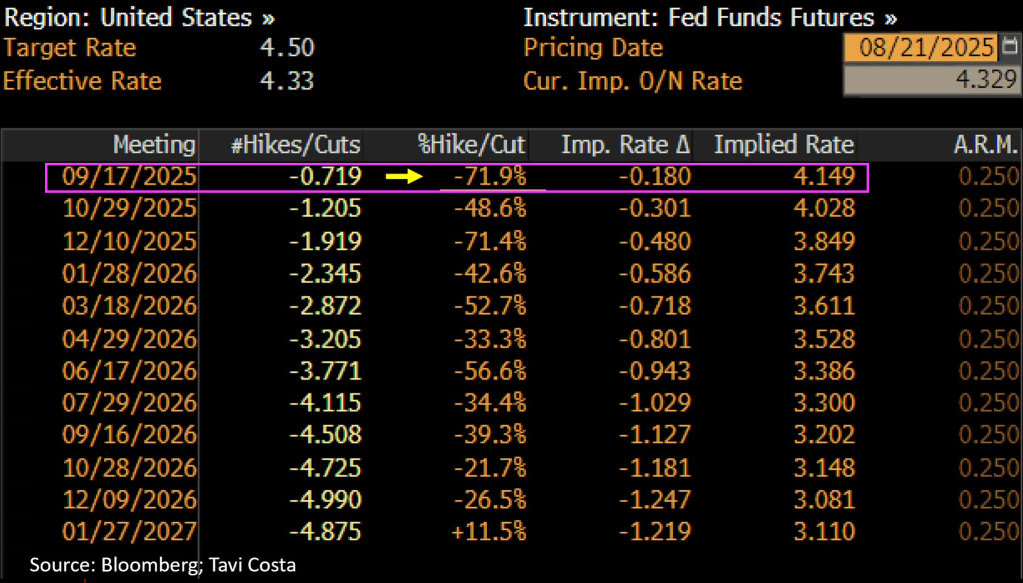

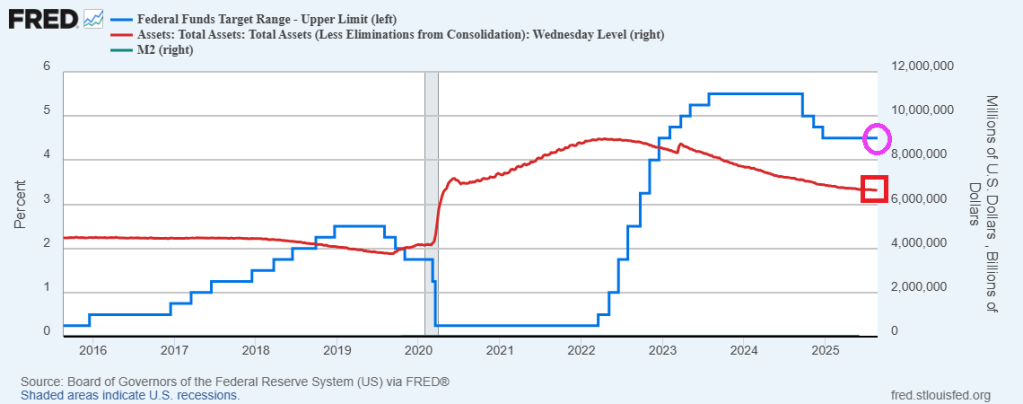

Let’s see if Powell and The Gang drop rates 25 or 50 basis points at today’s FOMC meeting.

Between The Fed’s persistent policy errors and Biden’s centralized mismanagement of the economy, Biden’s Maladministration is the epitome of a “Reign of Error.”

{kind=link}

{kind=link}

You must be logged in to post a comment.