Every time the government tries to make housing more affordable, they make the problem worse. Some people should rent and not fall for the government’s latest folly, the 50-year mortgage.

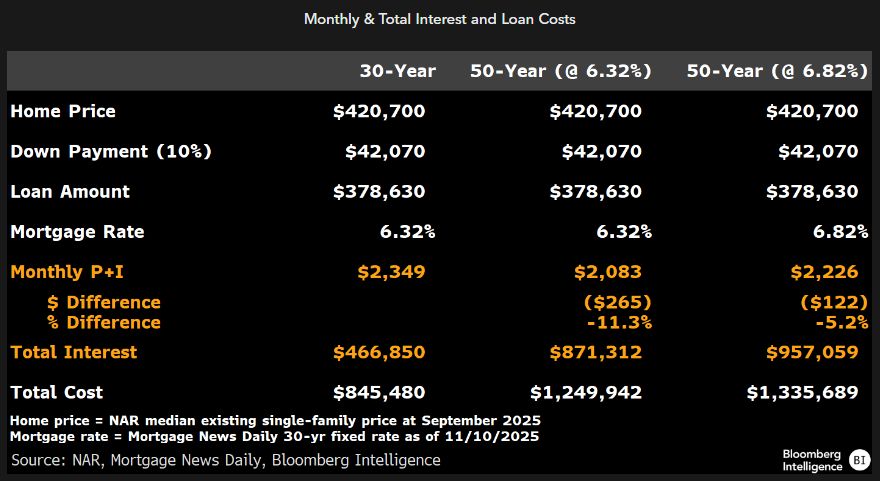

True, the 50-year mortgage would lower the monthly payment by several hundred dollars (see the following example where the monthly payment falls from $2,349 to $2,083. Or from $2,349 to $2,226 if the most rate increases with the longer mortgage life. BUT total interest paid increases 87% if the 50-year rate remains the same and 105% if the rate rises.

Principal paydown slows to a crawl with a 50-year mortgage, leaving the lender (or mortgage holder) exposed to higher risk if home prices fall.

Government housing policies remind me of the Curly versus the oyster stew skit. where Curly can’t catch the oyster. Yet keeps trying.

The 50-year mortgage reminds me of the ill-fated National Homeownership Strategy under Bill Clinton. By prdering all Federal housing finance entities to work with HUD, the National Homeownership Strategy helped crash the housing market (watch The Big Short!)

{kind=link}

{kind=link}

You must be logged in to post a comment.