I have a new term for consumers that get beaten-up by The Fed’s massive distortion of markets. I call this being “Powell’d”.

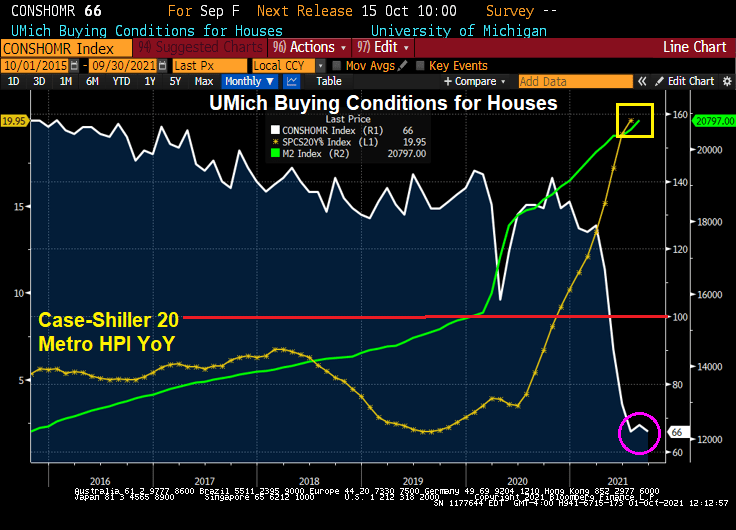

The latest example of consumers getting Powell’d is in the University of Michigan consumer survey. Buying conditions for housing just fell to the lowest level since 1982.

“I am in the camp that believes it will soon be time to begin slowly and methodically — frankly, boringly — tapering our $120 billion in monthly purchases of Treasury bills and mortgage-backed securities.”

Only a multi-millionaire like Powell would call it frustrating. Most US consumers would call it “devastating.”

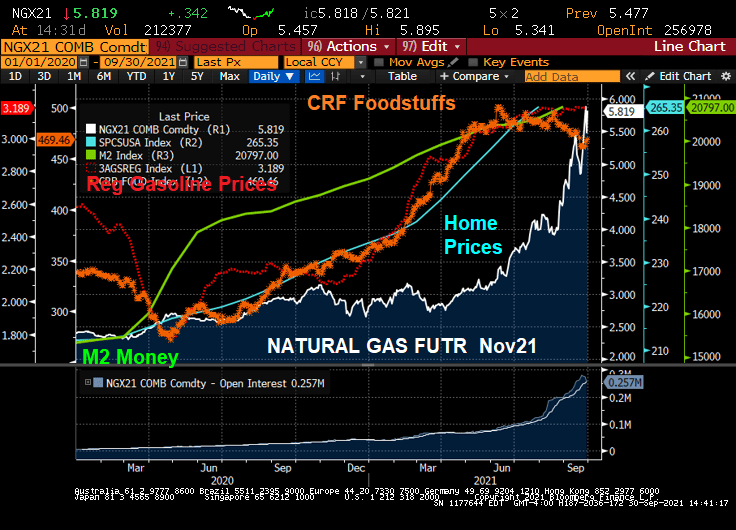

Look at home prices, natural gas, gasoline and food prices since The Fed turned on the money pump to combat the Covid shutdown by government. Well, at least food price growth has slowed, but that is more that offset by natural gas (heating) costs skyrocketing.

Rent? That too has zoomed upwards, although Powell likely isn’t worried about his rent rising by 11.5%.

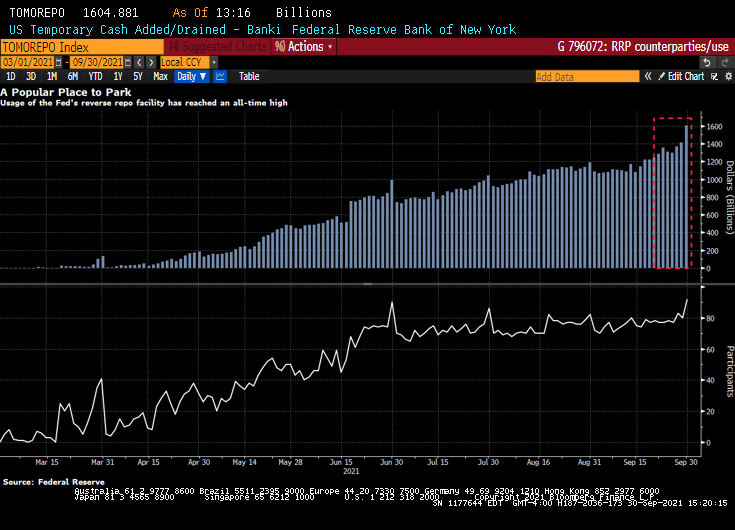

I wonder if Powell is frustrated by banks parking their money at the Fed’s reverse repo facility? Ninety-two participants on Thursday placed a total of $1.605 trillion at the Federal Reserve’s overnight reverse repurchase agreement facility, in which counterparties like money-market funds can place cash with the central bank. The previous record, set the day before, was $1.416 trillion. Thursday’s leap was the biggest one-day increase in usage since mid-June.

Biden blames “greed” for rising prices, Powell is “frustrated” by bottlenecks. But why pump trillions into the economy when you know there are bottlenecks? Or meatpacking firms are “greedy”?

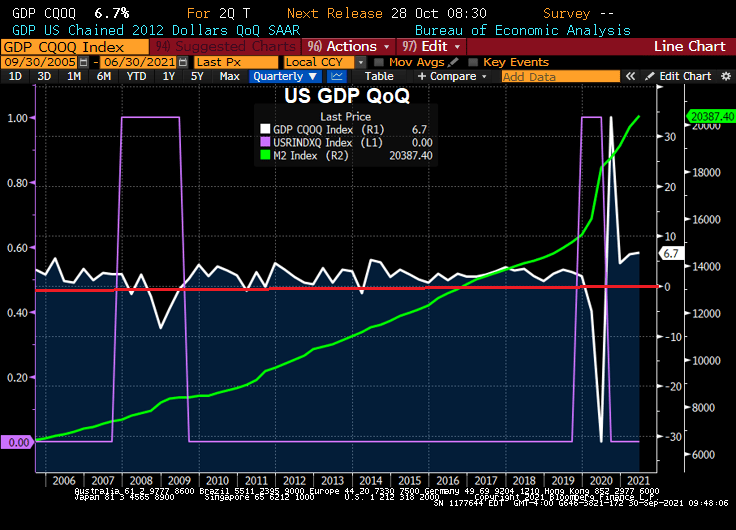

So much for the transitory inflation that The Federal Reserve keeps spouting on about.

(Bloomberg) — The pace of rent increases is heating up in the U.S.

Rent data for the past two months show no sign yet of the usual seasonal dip at this time of year, following peaks early in the summer, when many lease renewals come due.

A Zillow Group Inc. index based on the mean of listed rents rose 11.5% in August from a year earlier, with some cities in Florida, Georgia and Washington state seeing increases of more than 25%.

Since the start of the pandemic, the median rent for a two-bedroom apartment has soared 13.1% to $1,663, Zumper data show.

But rent on newly-signed leases rose 17% from the previous tenant’s lease.

For the New York market, landlords are raising rent prices as much as 70% now that people are flooding back into the city as offices and entertainment venues open up. In July, the median asking rent in New York City surged to $3,000, compared with the pandemic low of $2,750 in January 2021, data from StreetEasy showed.

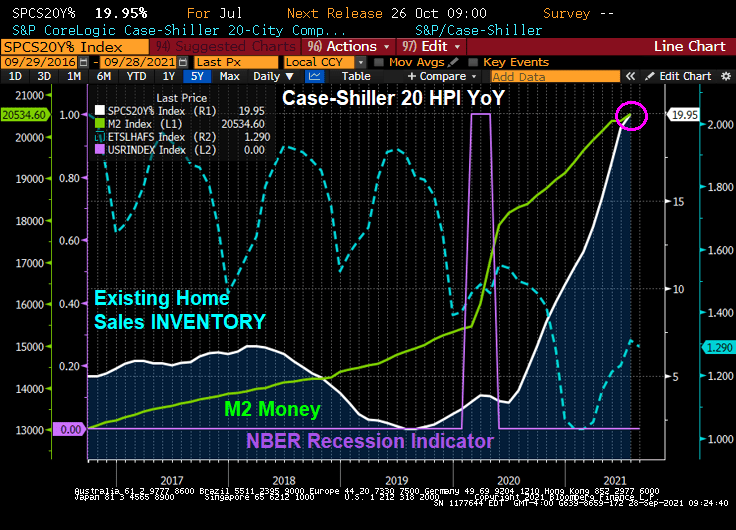

Of course, rent surge is not surprising given that home prices have surged since Covid given limited inventory and massive Fed stimulus.

Perhaps if The Fed and Federales (Federal government) start reducing their apocalyptic-level stimulus, THEN we will see inflation as transitory.

A national mortgage lender has just introduced a 105 Loan-to-value (LTV) ratio loan and a lowering of FICO scores from 660 to 620.

Now, the loan still requires 97% LTV with downpayment assistance and gift funds permitted to boost CLTV to 105%.

With The Fed helping to raise home prices at a whopping 20% YoY, …

lenders are trying to find loan products for lower-income households so they can get in on the bubble! Hence, a 105% CLTV mortgage product with reduced credit requirements and increased Debt-to-income requirement rising from 43% to 45%. Also, borrowers can avoid the 3% downpayment requirement and put down only $500.

This is lending into the storm: softening of underwriting requirements as the house price bubble surges. Sound like 2005. This was not supposed to happen. After the housing bubble burst and the financial crisis, The Fed was supposed to encourage counter-cyclical lending (tighten credit standards as a housing bubble worsens). Instead, lenders are lowering credit standards, feeding the house price bubble.

If this was just one lender, I would have barely noticed. But this mortgage is being offered by most banks. And then sold to our GSEs: Fannie Mae and Freddie Mac.

Speaking of lending into a storm, as part of the raft of new legislation designed to spur first-time homeownership in America, a remarkable bill has joined the fray: its sponsors propose creating a new subsdizied 20-year-fixed-rate mortgage program through Ginnie Mae, HousingWire reports.

According to the bill, Ginnie Mae in tandem with the Department of the Treasury would subsidize the interest rate and origination fees associated with these 20-year mortgages, so that the monthly payment would be in line with a new 30-year FHA-insured mortgage. The move – which is an explicit subsidy of one share of the population by another – could, in theory, “allow qualified homebuyers to build equity-and wealth- at twice the rate of a conventional 30-year mortgage.” Instead, what it will do is lead to is an even bigger housing bubble.

I certainly hope The Federal Reserve starts normalizing interest rates. Hold that Fed tiger!

(Bloomberg) — Sales of previously owned U.S. homes fell in August, suggesting that demand is moderating as lean inventory and high prices squeezed out some buyers.

Contract closings decreased 2% from the prior month to an annualized 5.88 million, in line with economists’ estimates, figures from the National Association of Realtors showed Wednesday. “Clearly the home sales are settling down but above pre-pandemic conditions,” Lawrence Yun, NAR’s chief economist, said on a call with reporters.

Lawrence Yun is correct. There was a huge spike in existing home sales (EHS) following the Covid outbreak and the overreaction by The Federal Reserve (aka, when the ain’ts went marching in). Despite continuing stimulus, but EHS has simmered down.

At least the median price of EHS YoY slowed to 12.1% YoY as The Fed slows M2 Money growth.

Inventory remains relatively low compared to historic levels while price zooms with Fed stimulus.

Want home price growth to slow its insane growth? Hold that tiger! That is, The Fed has to start normalizing interest rates.

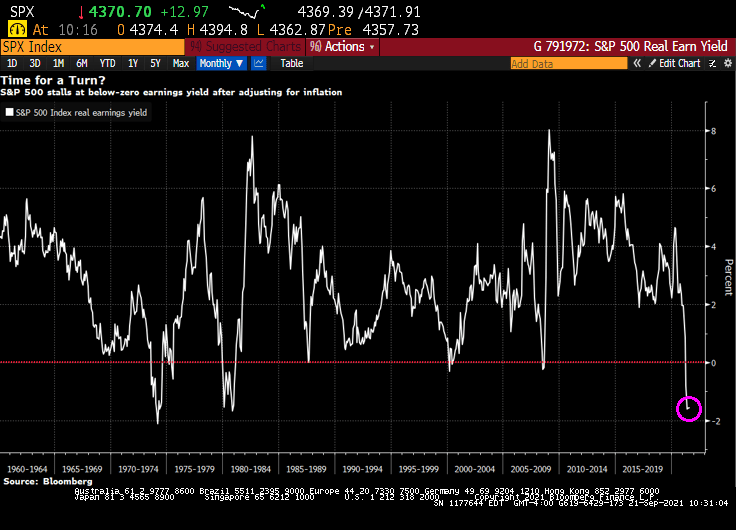

The stock market mildly rebounded from yesterday’s mild correction, but a glaring problem remains: S&P 500 real earning yields are negative.

With all the Federal government fiscal stimulus and Federal Reserve monetary stimulus, we are seeing inflation and that inflation is eating away at S&P 500 earnings yield.

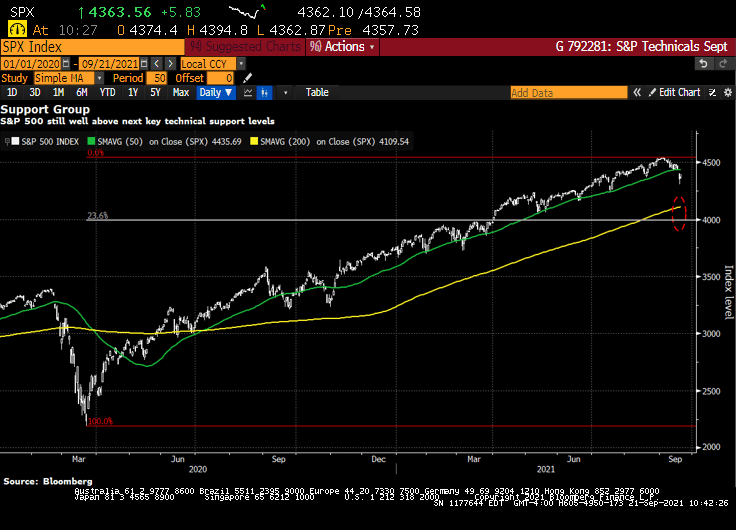

The S&P 500 is still well above key technical support levels.

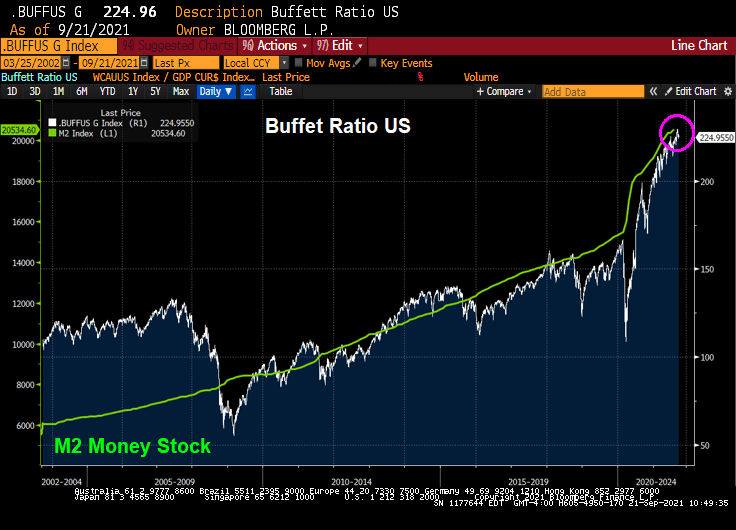

However, the Buffet ratio is raging along with Fed stimulus.

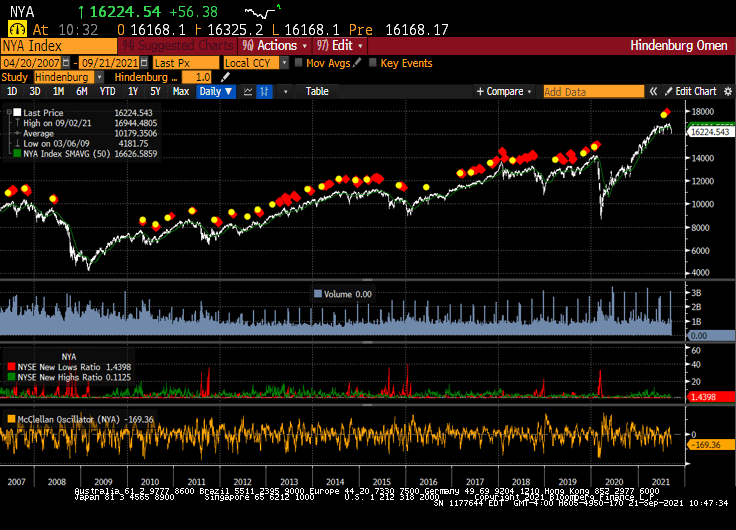

And the Hindenburg Omen is flashing RED!

The mystery of the Flying Fed is whether they will withdraw their massive monetary stimulus or not.

The unorthodox monetary stimulus from The Federal Reserve and stimulypto-level spending by the Federal government has resulted in a surge in US housing starts. But that thrill may be gone if the stimulypto is removed.

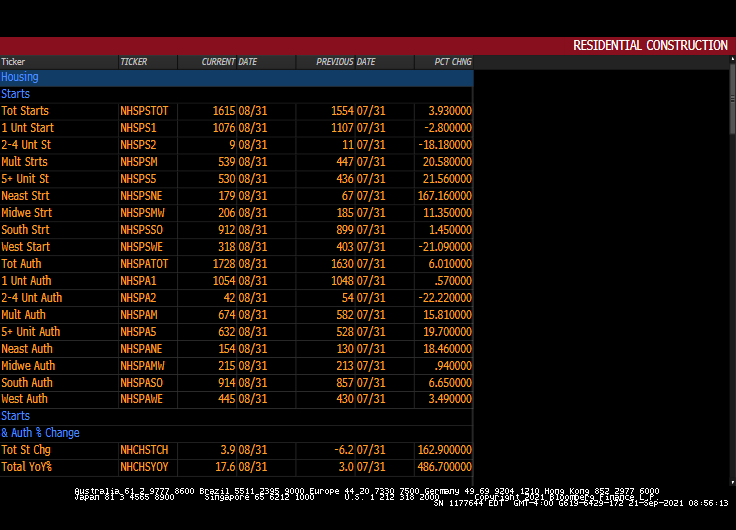

(Bloomberg) -By Olivia Rockeman- U.S. housing starts rose by more than expected in August, suggesting that the supply and labor constraints that have been holding back construction eased in the month.

Residential starts rose 3.9% last month to a 1.62 million annualized rate after an upwardly revised July print, according to government data released Tuesday. The median estimate in a Bloomberg survey called for a 1.55 million pace.

Building permits, meanwhile, increased 6% in August, the biggest gain since January, reflecting a sizable jump in multi-family units. Permit applications for single-family homes also edged higher.

The data suggest that builders are making some construction headway despite limited availability of land, labor and materials, which has slowed residential starts from a 15-year high in March. Despite the bottlenecks, housing starts remain mostly above pre-pandemic levels, which is expected keep construction activity elevated for some time.

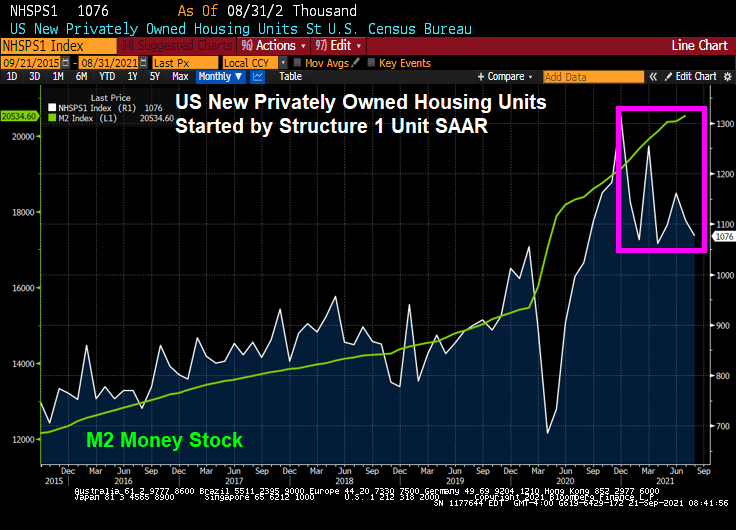

1-unit (single family detached) starts got a tremendous jolt from The Fed’s monetary stimulus and Federal governments fiscal stimulus. But government stimulus wears out.

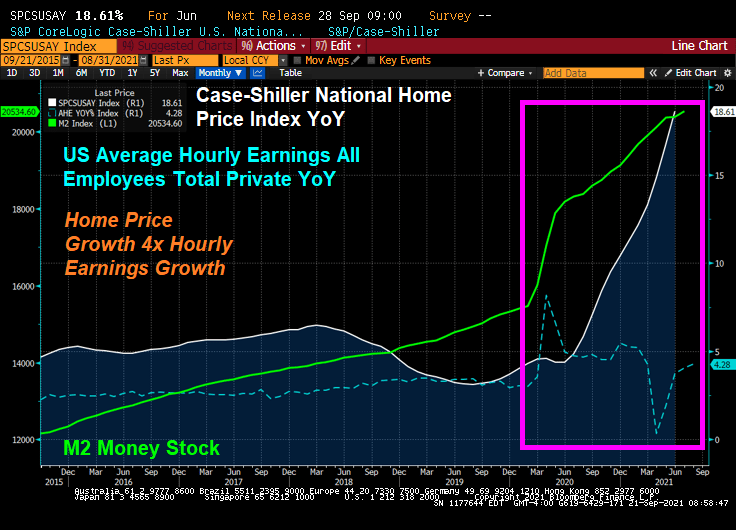

Given the high cost of housing in the USA, particularly in coastal metro areas, we see home price growth raging at over 4 times hourly earnings growth.

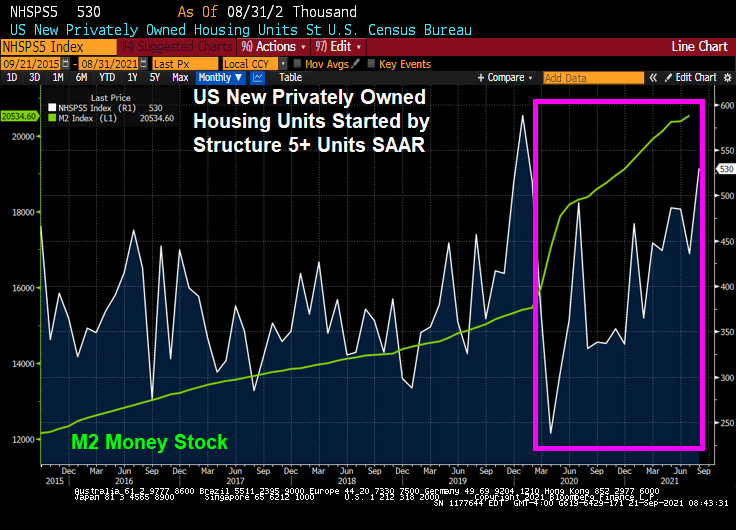

As a result, we are seeing a burst of 5+ unit (multifamily) housing starts. Note the burst of 5+ housing starts prior to Covid striking in early 2020.

Permits for 1-unit housing are up only slightly but 5+ unit permits are up 19.7%.

Remember, the withdrawal of fiscal stimulus will lead to a big fiscal cliff.

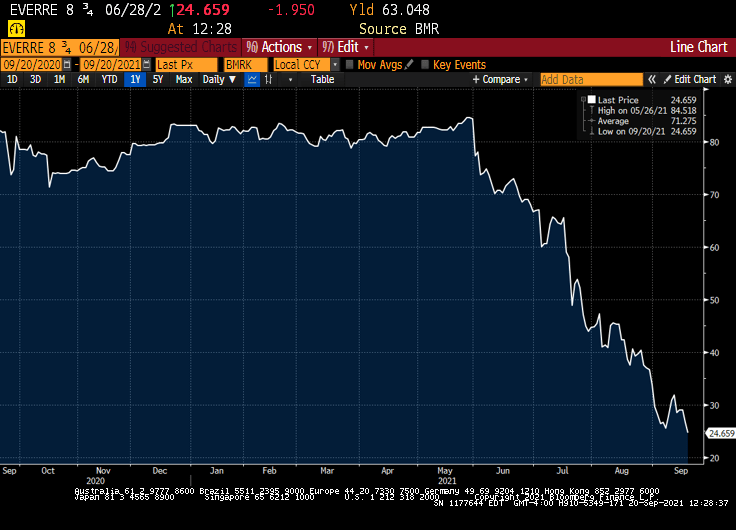

(Bloomberg) — The S&P 500 Index extended its decline past 2% Monday afternoon amid growing investor jitters about China’s real estate crackdown potentially sparking a financial contagion. And the Hang Seng fell 3.30% overnight.

The benchmark gauge was down 2.1% as of 12:08 p.m. in New York. All of the 11 major industry groups declined, with the energy, financials and materials sectors leading the losses. The tech-heavy Nasdaq 100 index slumped 2.4%, while the blue-chip Dow Jones Industrial Average retreated 1.9%.

By 2:33pm, the Dow is down 2.55%, NASDAQ down 3.15%.

Volatility also soared, with the Cboe Volatility Index — often called Wall Street’s “fear index” — jumping as much as 29% to 26.75, the highest level in over four months.

“While the Evergrande situation is front and center, the reality is, stock market valuations are overstretched and the market has enjoyed too long of a break from volatility and Monday’s stock market declines are not surprising,” said David Bahnsen, chief investment officer at the Bahnsen Group, a wealth management firm.

As Evergrande bonds continue to tank.

Meanwhile, most commodity prices are falling … except for UK Natural Gas Futures which are up 16.5%!

This is the Steve Urkel economy where The Federal Reserve and Federal government screw everything up with their policies (or follicies) and say “Whoops! Did I do that?”

(Bloomberg) — U.S. consumer sentiment rose slightly in early September but remained close to a near-decade low, while buying conditions deteriorated to their worst since 1980 because of high prices.

The University of Michigan’s preliminary sentiment index edged up to 71 from 70.3 in August, data released Friday showed. The figure trailed the median estimate of 72 in a Bloomberg survey of economists.

Buying conditions for household durables, homes and motor vehicles all fell to the lowest in decades. The report said the declines were due to complaints about high prices. Consumers expect inflation to rise 4.7% over the coming year, matching the highest since 2008.

September’s UMich Buying Conditions for Houses fell to 60 … thanks to superheated house prices.

I can just picture Fed Chair Jerome Powell channeling Steve Urkel and saying “Whoops!! Did I do that?”

You must be logged in to post a comment.