The culprits? Declining auto sales, manufacturing, etc.

I have discussed soaring prices since Biden’s election (food, energy, housing, rent, etc). But another soaring price component is shipping costs. Up 315% since mid-February.

While Trump’s slogan was “Make American Great Again”, Biden and The Fed’s slogan should be “Make America Far More Expensive For The Middle Class.” But that won’t fit on a bumper sticker.

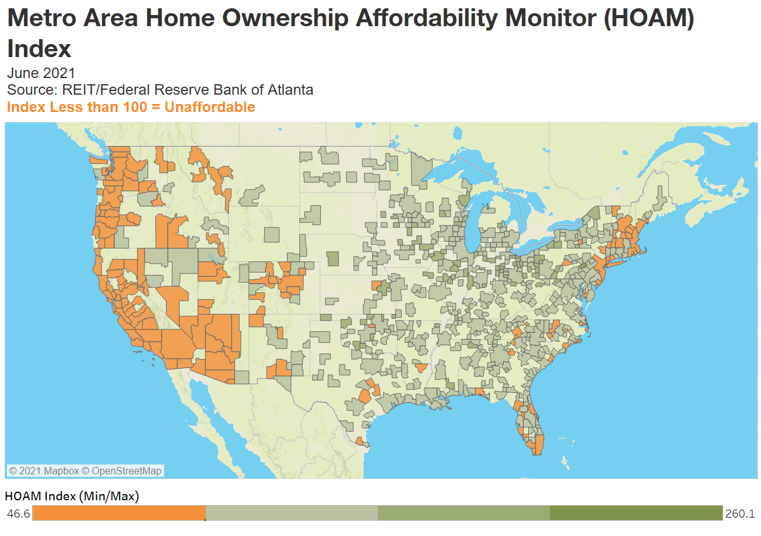

The national HOAM index stood at 92.2 in June, its lowest level since 2008.

National housing affordability fell 11.9 percent in June, the sharpest drop since 2014.

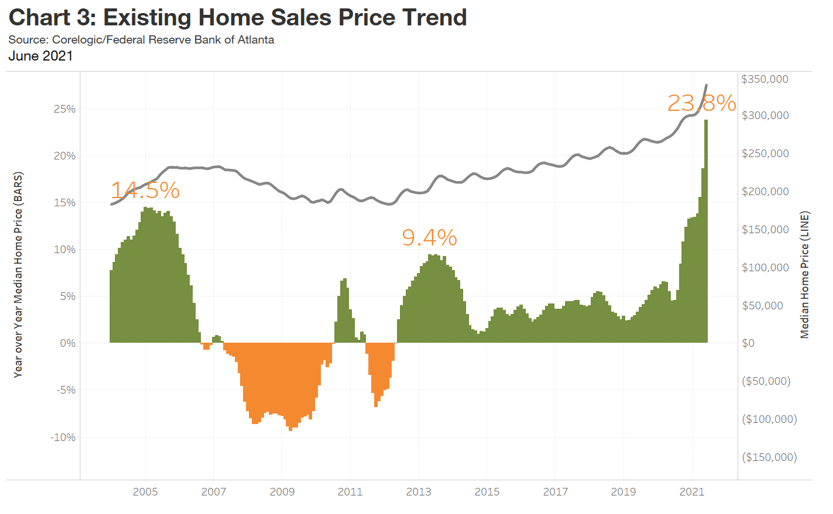

Home sale prices were up 23.8 percent over the past year.

On average, a median-income household would need to spend 32.6 percent of its annual earnings to own a median-priced home.

Although demand for housing remains strong, steadily declining affordability is beginning to affect buying decisions.

The latest reading of an Atlanta Fed measure and US housing trends show home ownership is becoming out of reach for many buyers and resistance to higher prices is building. More than 80 percent of US metro areas had a drop in affordability.

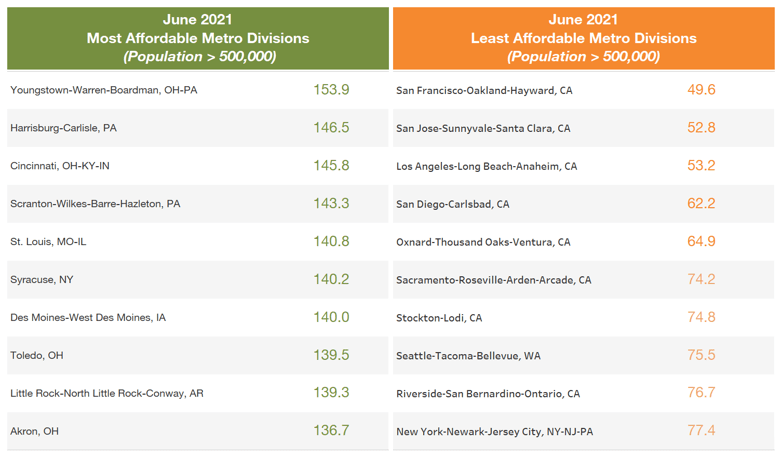

Where is housing most and least affordable?

ddd

Of course, the one chart that The Fed never includes is home price growth and Fed monetary policy.

So, if The Fed is so concerned with median-income households being priced out of housing markets, why are the still sticking with their unorthodox monetary policies?

Can you say “All the king’s horses and all the king’s men ..” Or “All The Fed’s stimulus and all of Biden’s jobs bills ..”

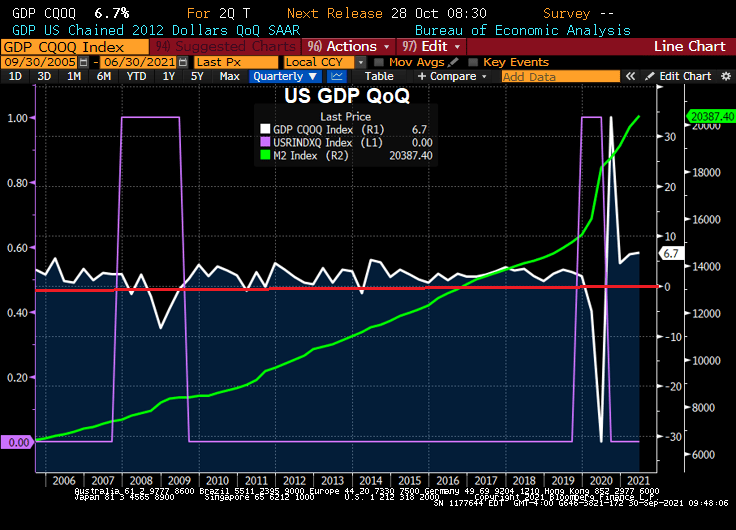

Yes, the Atlanta Fed’s GDPNow Q3 tracker slumped to 2.3% despite the massive stimulus coming from The Federal Reserve and the Biden Administration. Down from 13.7% GDP growth as of 5/5/2021.

I have a new term for consumers that get beaten-up by The Fed’s massive distortion of markets. I call this being “Powell’d”.

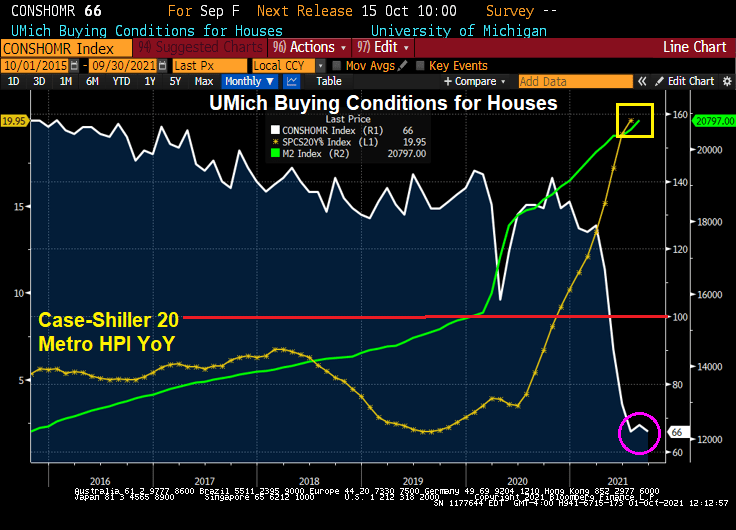

The latest example of consumers getting Powell’d is in the University of Michigan consumer survey. Buying conditions for housing just fell to the lowest level since 1982.

“I am in the camp that believes it will soon be time to begin slowly and methodically — frankly, boringly — tapering our $120 billion in monthly purchases of Treasury bills and mortgage-backed securities.”

Only a multi-millionaire like Powell would call it frustrating. Most US consumers would call it “devastating.”

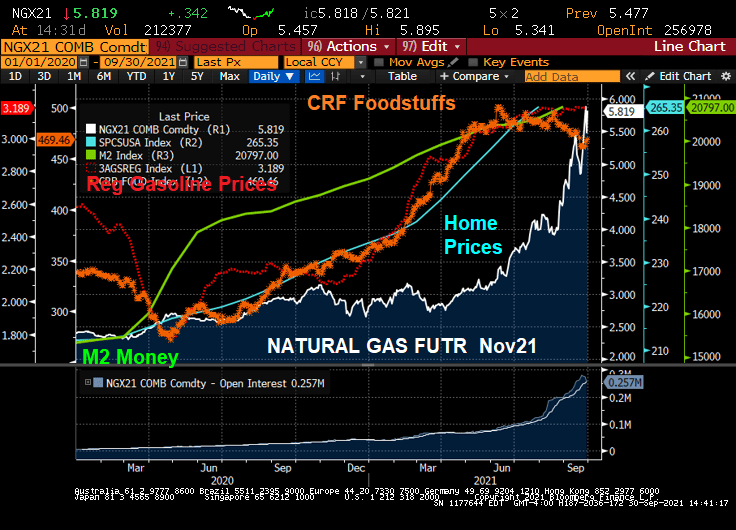

Look at home prices, natural gas, gasoline and food prices since The Fed turned on the money pump to combat the Covid shutdown by government. Well, at least food price growth has slowed, but that is more that offset by natural gas (heating) costs skyrocketing.

Rent? That too has zoomed upwards, although Powell likely isn’t worried about his rent rising by 11.5%.

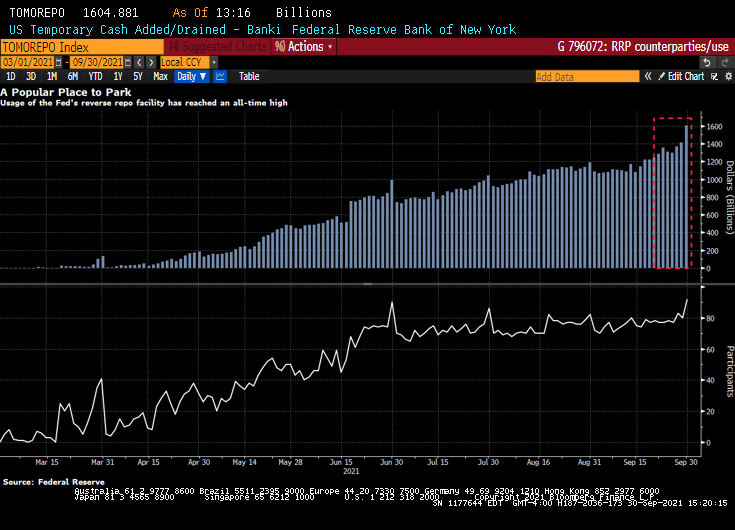

I wonder if Powell is frustrated by banks parking their money at the Fed’s reverse repo facility? Ninety-two participants on Thursday placed a total of $1.605 trillion at the Federal Reserve’s overnight reverse repurchase agreement facility, in which counterparties like money-market funds can place cash with the central bank. The previous record, set the day before, was $1.416 trillion. Thursday’s leap was the biggest one-day increase in usage since mid-June.

Biden blames “greed” for rising prices, Powell is “frustrated” by bottlenecks. But why pump trillions into the economy when you know there are bottlenecks? Or meatpacking firms are “greedy”?

So much for the transitory inflation that The Federal Reserve keeps spouting on about.

(Bloomberg) — The pace of rent increases is heating up in the U.S.

Rent data for the past two months show no sign yet of the usual seasonal dip at this time of year, following peaks early in the summer, when many lease renewals come due.

A Zillow Group Inc. index based on the mean of listed rents rose 11.5% in August from a year earlier, with some cities in Florida, Georgia and Washington state seeing increases of more than 25%.

Since the start of the pandemic, the median rent for a two-bedroom apartment has soared 13.1% to $1,663, Zumper data show.

But rent on newly-signed leases rose 17% from the previous tenant’s lease.

For the New York market, landlords are raising rent prices as much as 70% now that people are flooding back into the city as offices and entertainment venues open up. In July, the median asking rent in New York City surged to $3,000, compared with the pandemic low of $2,750 in January 2021, data from StreetEasy showed.

Of course, rent surge is not surprising given that home prices have surged since Covid given limited inventory and massive Fed stimulus.

Perhaps if The Fed and Federales (Federal government) start reducing their apocalyptic-level stimulus, THEN we will see inflation as transitory.

A national mortgage lender has just introduced a 105 Loan-to-value (LTV) ratio loan and a lowering of FICO scores from 660 to 620.

Now, the loan still requires 97% LTV with downpayment assistance and gift funds permitted to boost CLTV to 105%.

With The Fed helping to raise home prices at a whopping 20% YoY, …

lenders are trying to find loan products for lower-income households so they can get in on the bubble! Hence, a 105% CLTV mortgage product with reduced credit requirements and increased Debt-to-income requirement rising from 43% to 45%. Also, borrowers can avoid the 3% downpayment requirement and put down only $500.

This is lending into the storm: softening of underwriting requirements as the house price bubble surges. Sound like 2005. This was not supposed to happen. After the housing bubble burst and the financial crisis, The Fed was supposed to encourage counter-cyclical lending (tighten credit standards as a housing bubble worsens). Instead, lenders are lowering credit standards, feeding the house price bubble.

If this was just one lender, I would have barely noticed. But this mortgage is being offered by most banks. And then sold to our GSEs: Fannie Mae and Freddie Mac.

Speaking of lending into a storm, as part of the raft of new legislation designed to spur first-time homeownership in America, a remarkable bill has joined the fray: its sponsors propose creating a new subsdizied 20-year-fixed-rate mortgage program through Ginnie Mae, HousingWire reports.

According to the bill, Ginnie Mae in tandem with the Department of the Treasury would subsidize the interest rate and origination fees associated with these 20-year mortgages, so that the monthly payment would be in line with a new 30-year FHA-insured mortgage. The move – which is an explicit subsidy of one share of the population by another – could, in theory, “allow qualified homebuyers to build equity-and wealth- at twice the rate of a conventional 30-year mortgage.” Instead, what it will do is lead to is an even bigger housing bubble.

The Federal Reserve is dominating the news today as two Fed regional Presidents have resigned (Rosengren [Boston] and Kaplan [Dallas]) for trading irregularities.

Now, it is September 28, so this is a report of happenings two months ago. Well, now you know why The Fed ignores housing despite being the largest asset is most household’s portfolio.

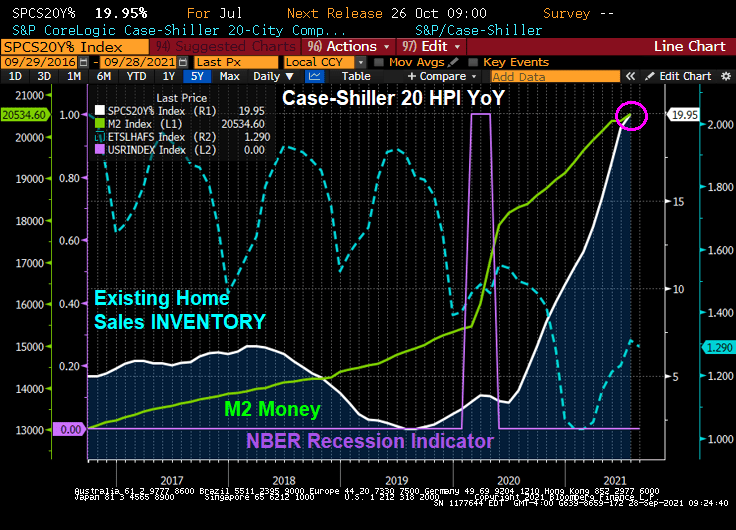

A measure of prices in 20 U.S. cities gained 19.9% in July. Phoenix led the way with a 32.4% surge. New York (17.8%), Boston (18.7%), Dallas (23.7%), Seattle (25.5%) and Denver (21.3%) were among the cities that posted record year-over-year increases.

The housing market is over, under, sideways, down thanks to The Fed pumping trillions into a market with limited available inventory.

Phil Hall of Benzinga wrote a series of excellent articles in four parts for MortgageOrb (although “The Orb” has removed his name). Here are the links to his stories.

After re-reading these excellent articles on the housing bubble and crash, I thought I would take the opportunity to present a few charts to highlight the housing bubble, pre-crash and post-crash.

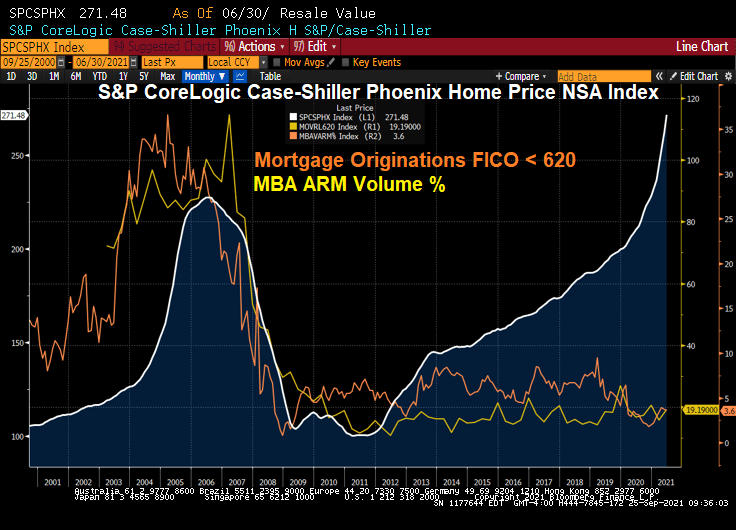

Here is a graph of Phoenix AZ home prices. Note the bubble that peaked in mid 2006. The Phoenix bubble correlates with the large volume of sub-620 FICO lending and Adjustable-rate mortgage (ARM) lending. Bear in mind, many of the ARMs prior to 2010 were NINJA (no income, no job) ARM loans.

What happened? Serious delinquenices at the national levels spiked as The Great Recession set in and unemployment spiked.

Since the housing bubble burst and surge in serious mortgage delinquencies, The Federal Reserve entered the economy with a vengeance. And have never left, and increased their drowning of markets with liquidity.

The Fed whip-sawing of interest rates in response to the 2001 recession was certainly a problem. They dropped The Fed Funds Target rate like a rock, then homebuilding went wild nationally and home prices soared thanks to Alt-A (NINJA) and ARM lending. But now The Fed is dominating markets like a gigantic T-Rex.

Oddly, then Fed Chair Ben Bernanke never saw the bubble coming. Or the burst.

Speaking of pizza, Donato’s from Columbus Ohio is my favorite. Founder’s Favorite is my favorite, but they do offer the dreaded Hawaiian pizza (ham, pineapple, almonds and … cinnamon?)

You must be logged in to post a comment.