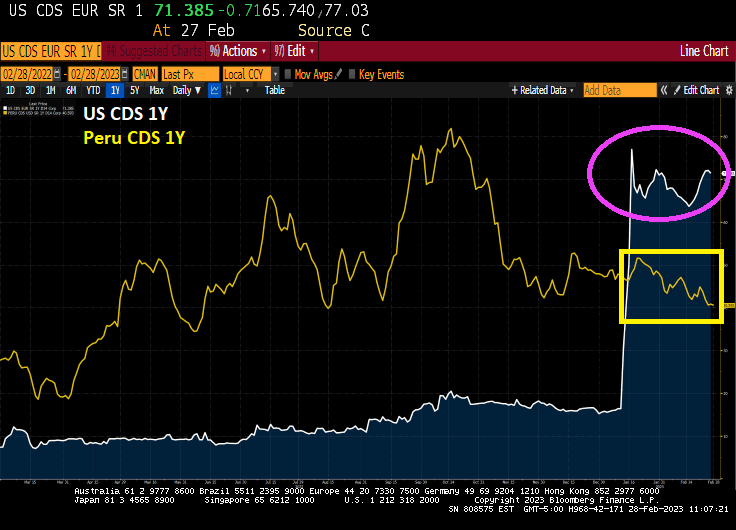

I used to write that the US is fast becoming Venezuela or Argentina. But its now official — the US has greater default risk than Peru!

Credit default swaps (CDS) represent the price of insuring against default. So it is now more expensive to insure against a US debt default than perpetually mismanaged Peru.

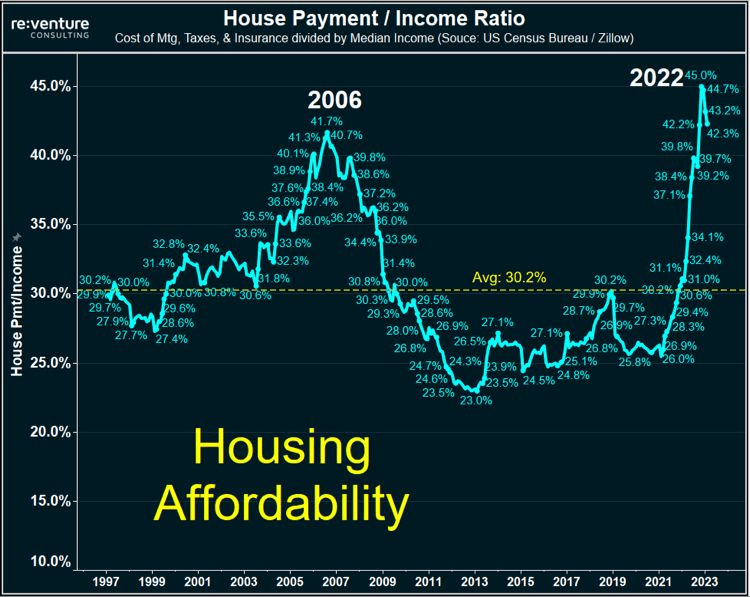

Janet Yellen and The Federal Reserve held rates too low for too long and now we are paying for it. Now, after a massive run-up in home prices, The Fed is raising rates helping make US housing the most unaffordable in history (or at least since the early 1980s).

And negative real wage rate growth for 22 straight months isn’t helping!

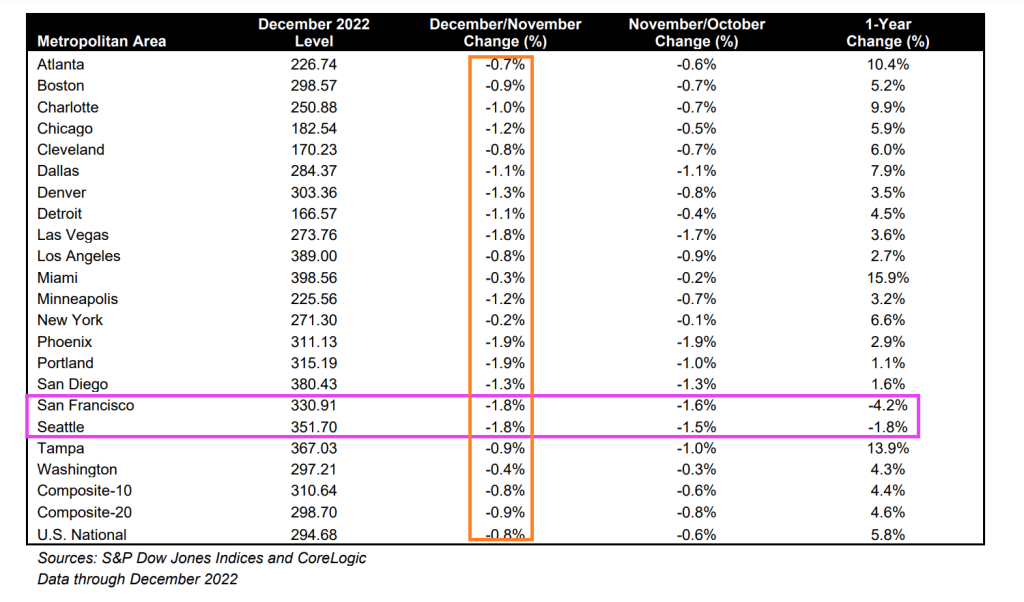

Only Seattle and San Francisco experienced negative growth in home prices on a year-over-year basis. All of the top twenty metro areas experience negative month-over-month price declines from November to December.

The Federal Reserve is retreating from its Covid-era monetary expansion. And with the retreat, US durable goods NEW ORDERS fell -4.5%% in January. The worst reading since … Covid in 2020.

A breakdown of new orders shows that while NONDEFENSE capital goods orders dropped -5.4% YoY in January, DEFENSE capital goods orders increased by 25.4% YoY.

The gap between the VIX Put-call volume and CBOE Put-call ratio is the widest since 2006, the precursor of a major volatility spike.

Meanwhile, for those of you interest in railroad regulatory issues, as a general matter, regulations are rarely ever “reversed,:” but rather modified or replaced with changes. No administration would be able to outright “repeal” a major safety regulation because it almost certainly be immediately enjoined by a court and found to be counter to Congressional delegation.

I assume most of the attention will be on this final rule (https://www.federalregister.gov/documents/2020/10/07/2020-18339/rail-integrity-and-track-safety-standards) published and effective on Oct 7, 2020. It is considered”deregulatory” in the sense that it results in an economic or compliance cost savings, mostly owing to a change in the permissible type of track integrity monitoring, and decrease in the resulting number of “slow orders.”

Unlike Pete Buttigieg who apparently did not read the regulations when he blamed Trump, read the actual published “deregulation.” A faulty railcar axel which was the cause of the East Palestine Ohio trail derailment was NOT impacted by the “deregulation.” Instead of Mayor Pete, he should be called “Cheap Shot Pete.”

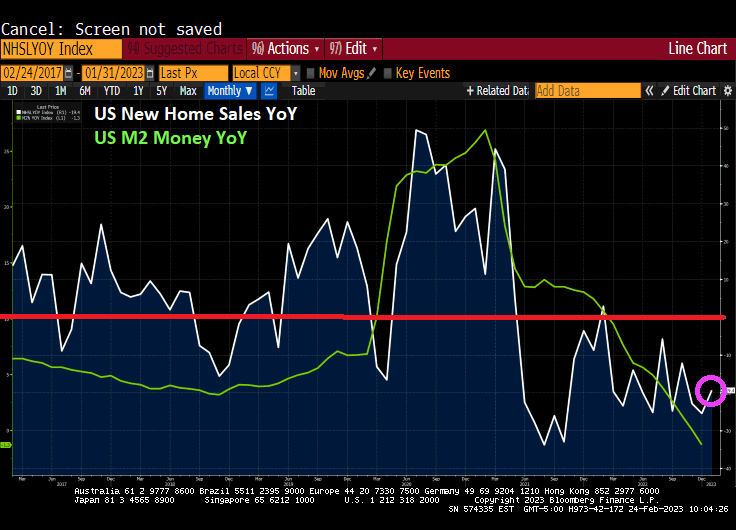

Another sign of a not healthy economy is housing. New Home Sales collapsed -19.4% from January 2022 (aka, year-over-year or YoY).

If I were Joe Biden, I would be touting the month-over-month numbers, up 7.20% from December to January. But the reality is that year-over-year new home sales are down -19.4%.

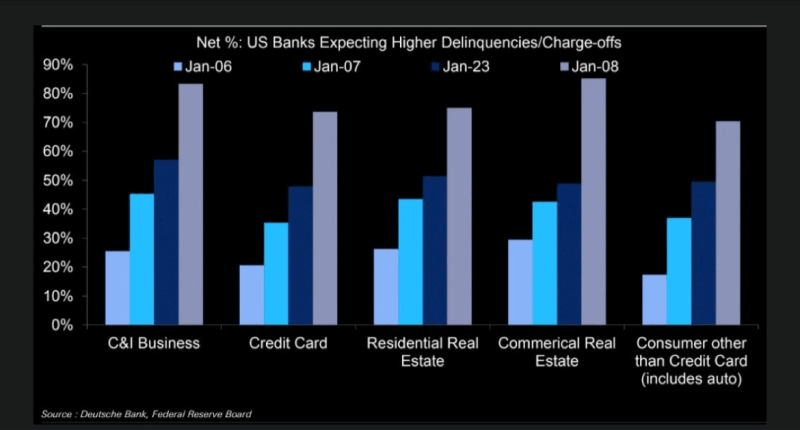

Also, on the “Alarm!” front, US banks are expecting higher delinquencies, including on residential mortgages.

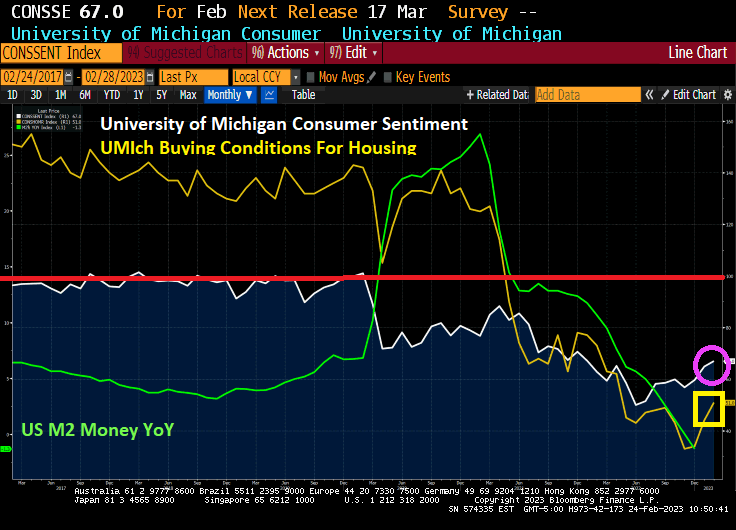

University of Michgan consumer sentiment for housing is rising, but still woefully below the 100 benchmark.

Not really a surprise, but January’s personal spending numbers came in hot at 1.8% MoM. Also, Personal Consumption Expenditures PRICE index (aka, inflation) rose to 5.4% YoY.

Here comes The Fed! The 2-year Treasury yield rose 10 basis points this morning.

The US Federal government reminds me of the Peggy Lee song “Is That All There Is?” Since the outbreak of Covid in 2020 and the absurb spending spree by Pelosi and Schumer, the Federal government has increased their debt by 36% to help pay for the Federal spending spree. That amounts to $54.8 TRILLION in additional Federal debt since January 2020.

What did the US economy get for all that Federal spending? In Q4 2022, Real GDP rose by … 0.91% YoY. Seriously? Is that all there is from $54.8 TRILLION in additional Federal debt?

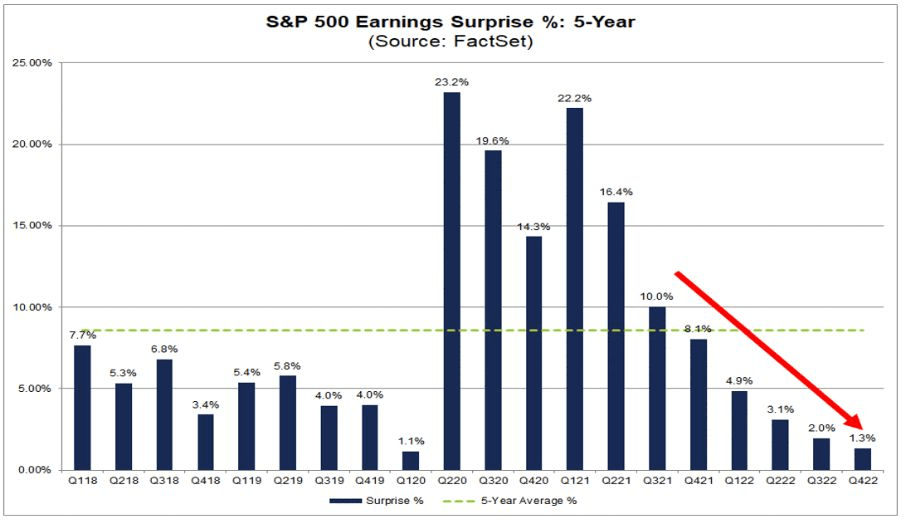

Another bit of lousy news. Look at the trend in S&P 500 Earnings Surprise (5 year).

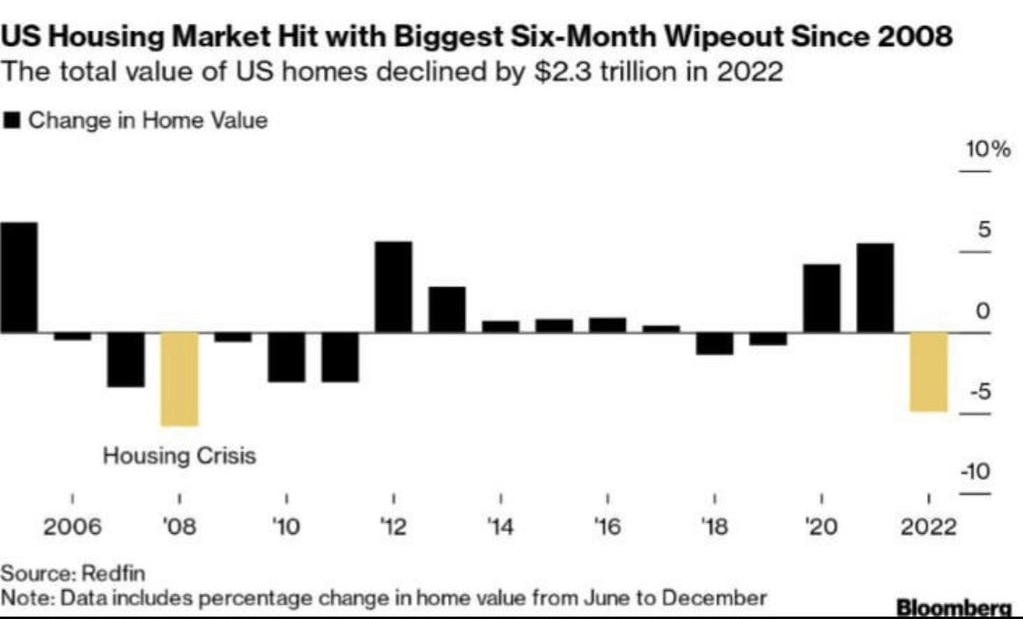

On the housing front, the US housing market was hit with the biggest six-month wipeout since 2008.

At least US Transportation Secretary “Pothole Pete” Buttigieg FINALLY showed up (three weeks after that East Palestine Ohio train disaster). Here is Buttigieg practising for his press conference.

Bull steepenings in the yield curve are generally seen as a precursor to a recession, but they are often preceded by bear steepenings. The 3m30y curve is currently bear steepening, indicating a recession could begin as early as the summer. In fact, the 3m30y curve is now inverted at -94.628 basis points pointing to a recession in summer 2023.

This is happening as the US house payment to income ratio near all-time highs.

You must be logged in to post a comment.