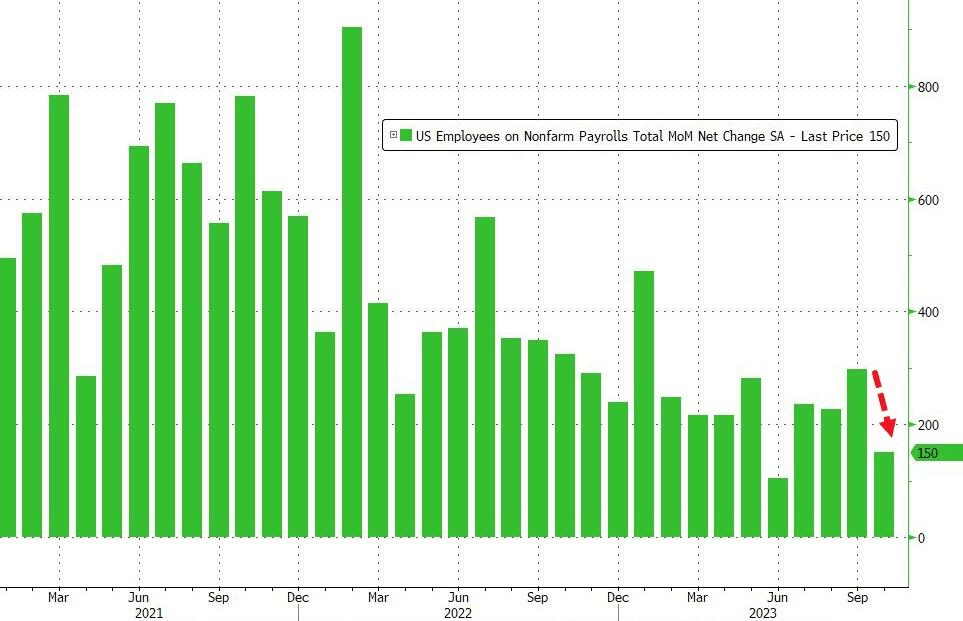

Yes, the jobs come crumbling down!

Total nonfarm payroll employment increased by 150,000 in October, below the average monthly gain of 258,000 over the prior 12 months. This represents a drop of more than 50% from the original Sept print, and the second lowest since 2022!

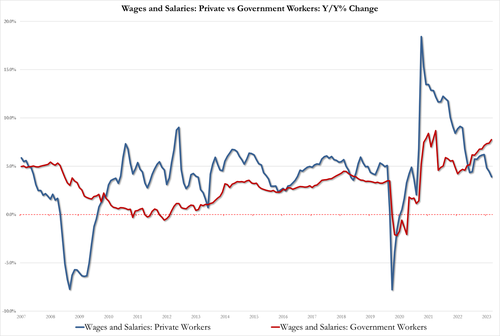

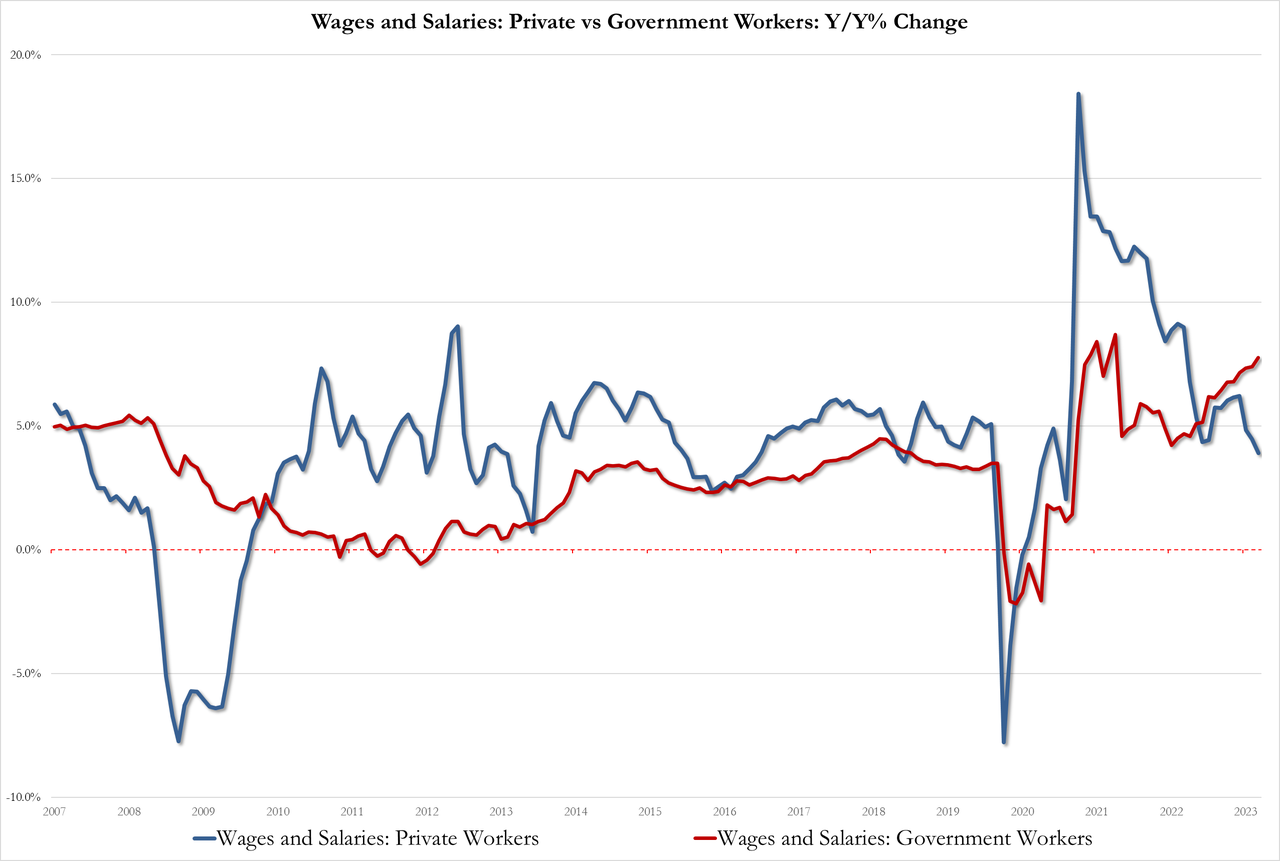

In October, job gains occurred in health care, government, and social assistance. Employment in manufacturing declined due to strike activity. (See table B-1.) Health care added 58,000 jobs in October, in line with the average monthly gain of 53,000 over the prior 12 months. Over the month, employment continued to trend up in ambulatory health care services (+32,000), hospitals (+18,000), and nursing and residential care facilities (+8,000). Employment in government increased by 51,000 in October and has returned to its pre-pandemic February 2020 level. Monthly job growth in government had averaged 50,000 in the prior 12 months. In October, employment continued to trend up in local government (+38,000).

In October, construction employment continued to trend up (+23,000).

So, unproductive government jobs increased by 51k while productive construction employment grew by only 23k.

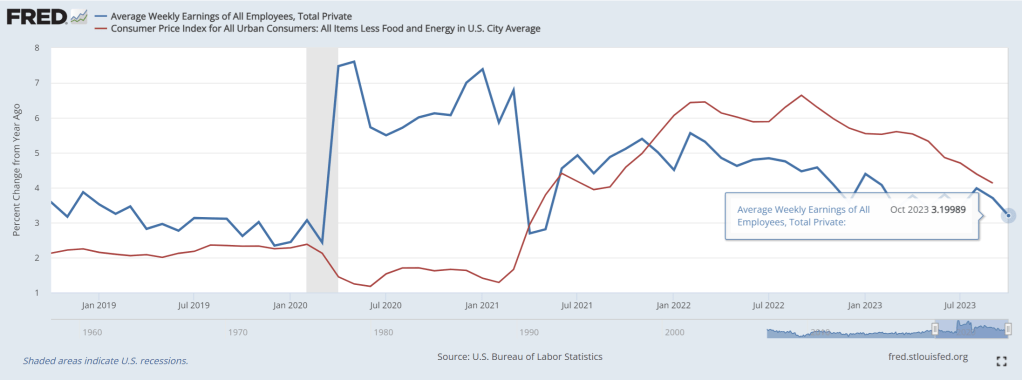

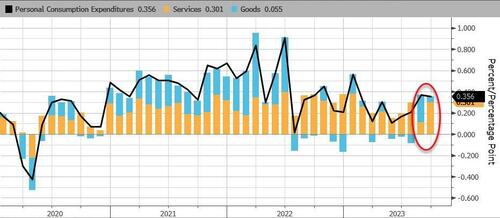

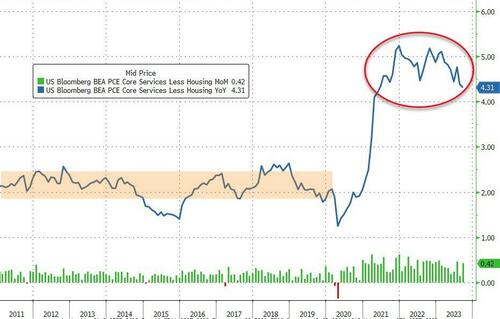

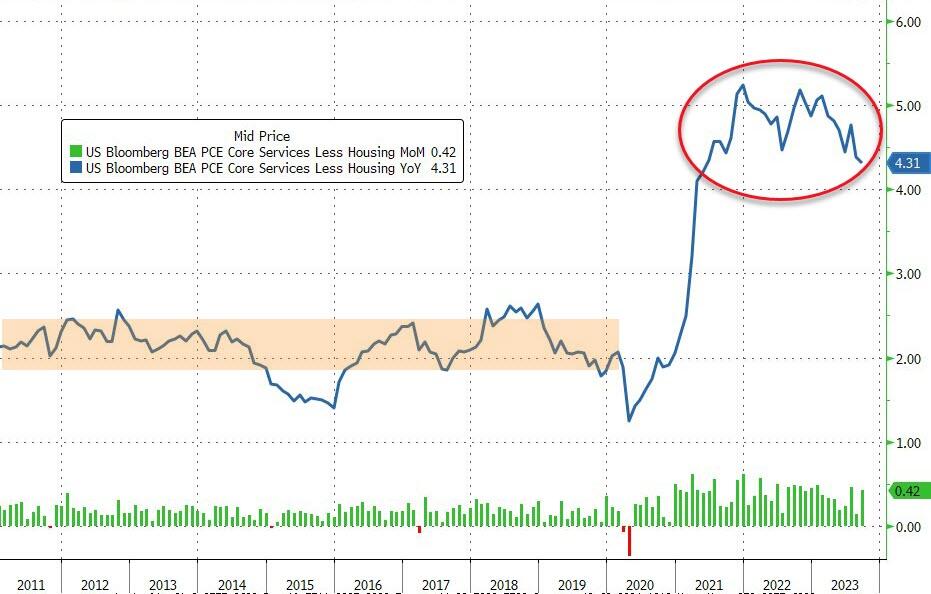

Average weeky; earnings growth YoY slowed to 3.2%. Too bad core inflation last printed at 4.13% YoY in September.

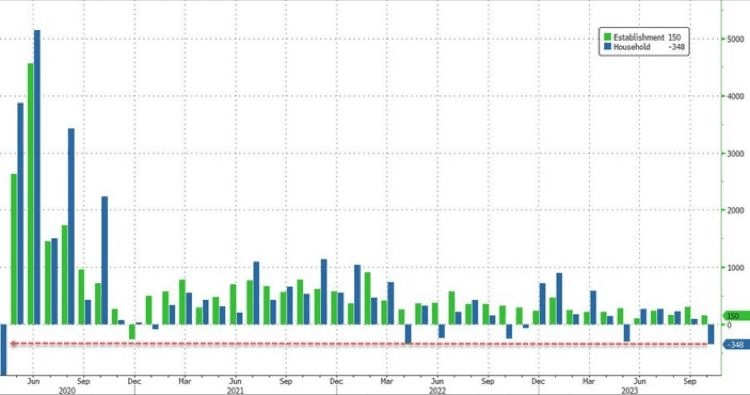

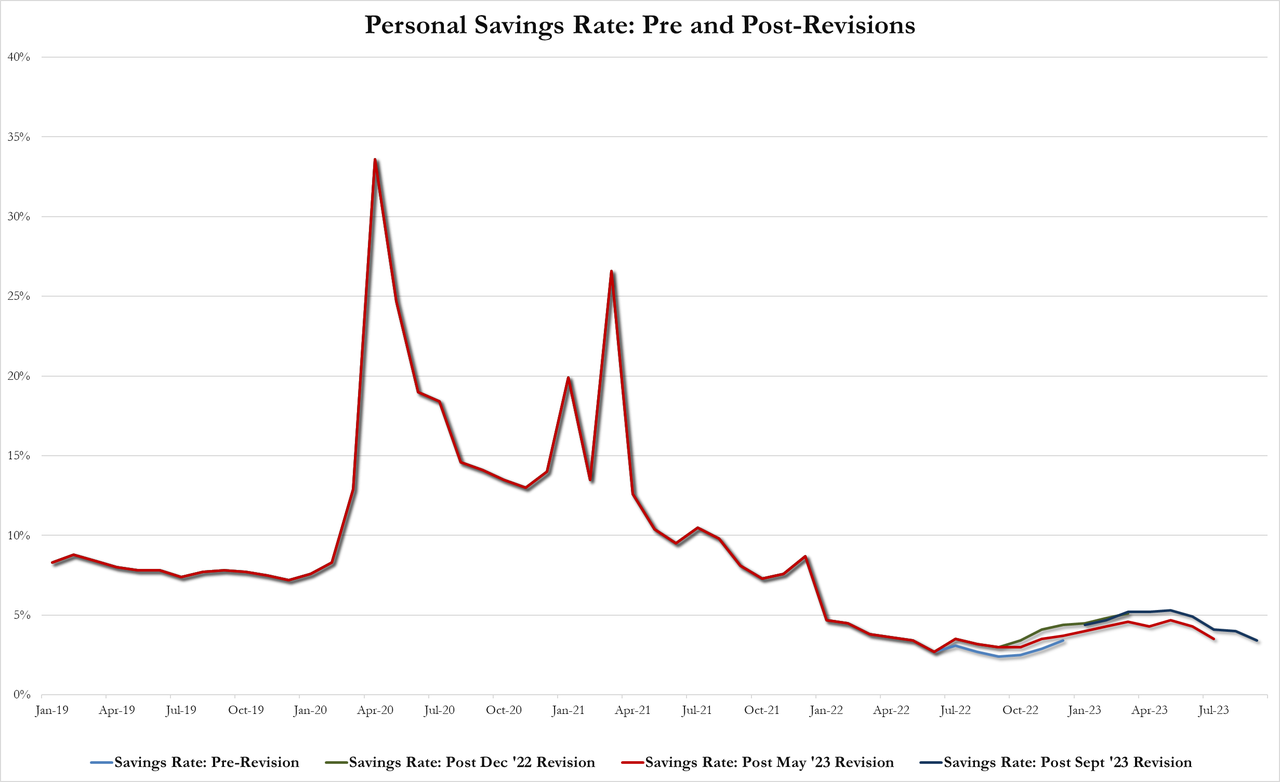

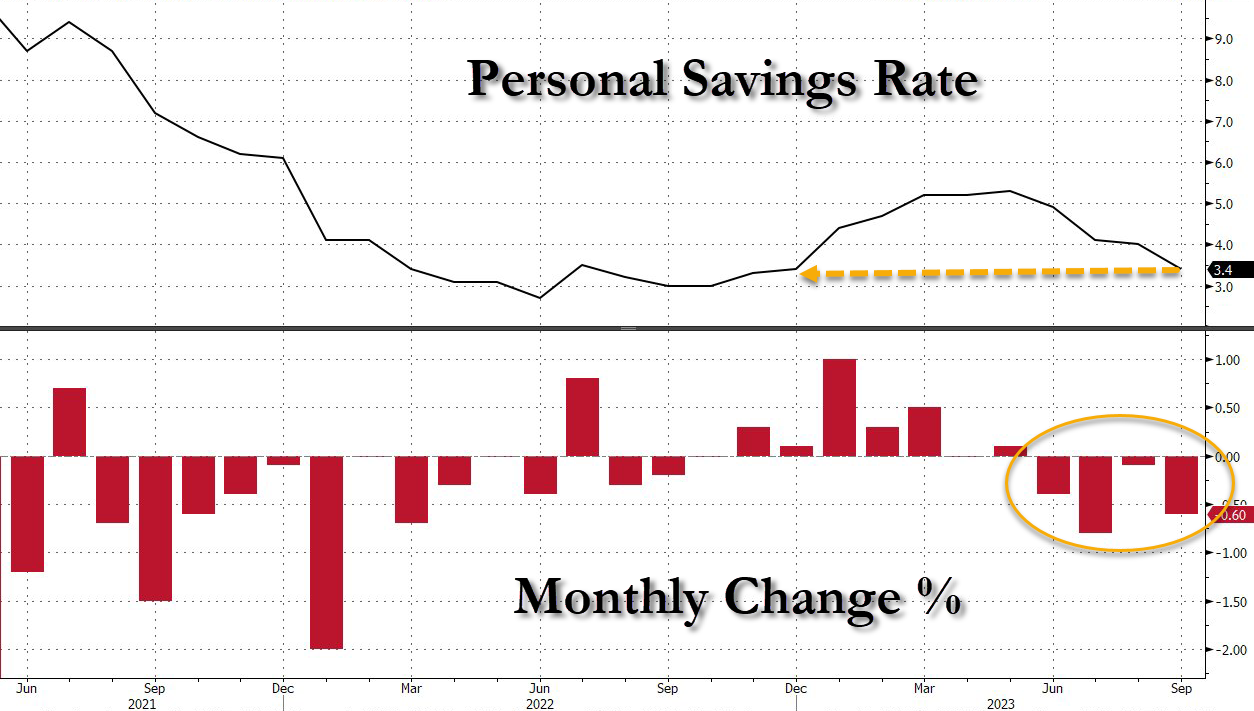

But the household survey shows employment collapsed by 348K, the biggest drop since the Covid shutdown.

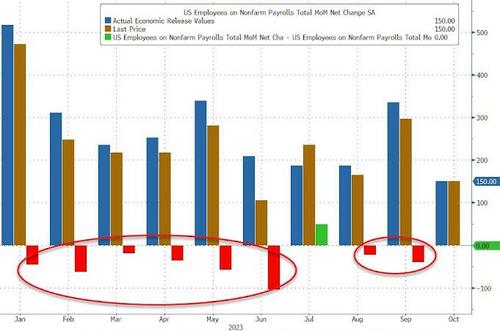

As usual, historical data was revised massively lower, with the jobs change for August revised down by 62,000, from +227,000 to +165,000, and the change for September was revised down by 39,000, from +336,000 to +297,000. With these revisions, employment in August and September combined is 101,000 lower than previously reported. In total, 8 of the past 8 months have been revised sharply lower in what only idiots can not see is clearly mandated political propaganda designed to make the economy look stronger at first glance then quietly revise the growth away.

Bidenomics hurts so good? At least that is what Biden and KJP will say.

Soft Jobs Report Weakens Impetus for Fed Rate Hike in December. Translation? Weak jobs report = no more Fed rate hikes = falling interest and mortgage rates.

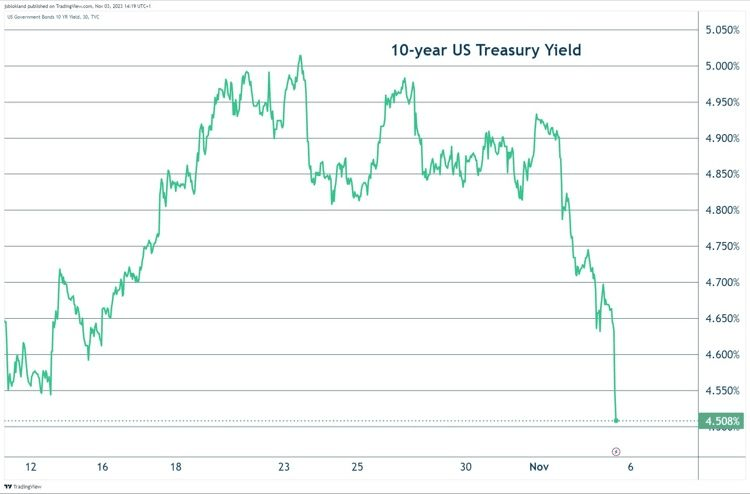

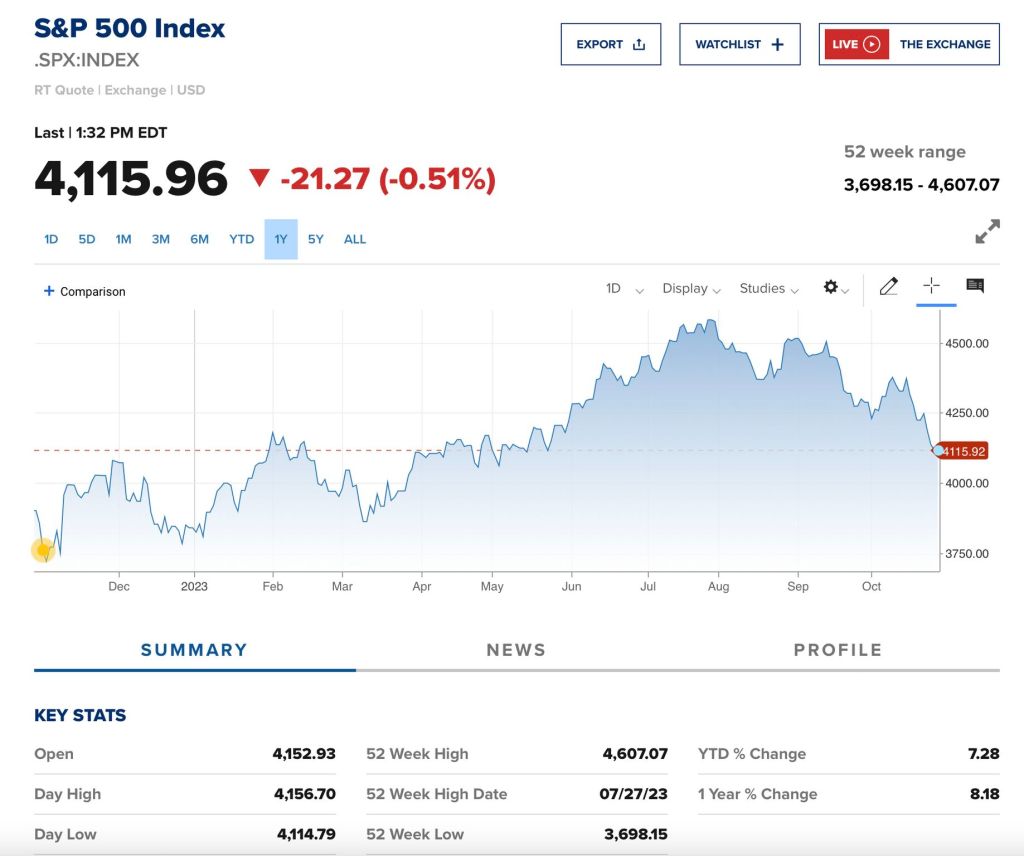

10-year US Treasury yield now down a whopping 40 basis points in the last three trading sessions.

And its beginnig to look a lot like a BAD Christmas!

How do you recession? B-I-D-E-N-O-M-I-C-S.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.