The US Q1 GDP report is due out tomorrow morning. The forecast is for -1.3% decline in GDP.

The Atlanta Fed GDPNow real-time GDP tracker is for 1.806% for Q2. If this holds, then recession fears will diminish.

Even though the US may avoid consecutive negative GDP quarters, M2 Money Velocity (GDP/M2 Money) got crushed by The Fed’s reaction to Covid back in 2020.

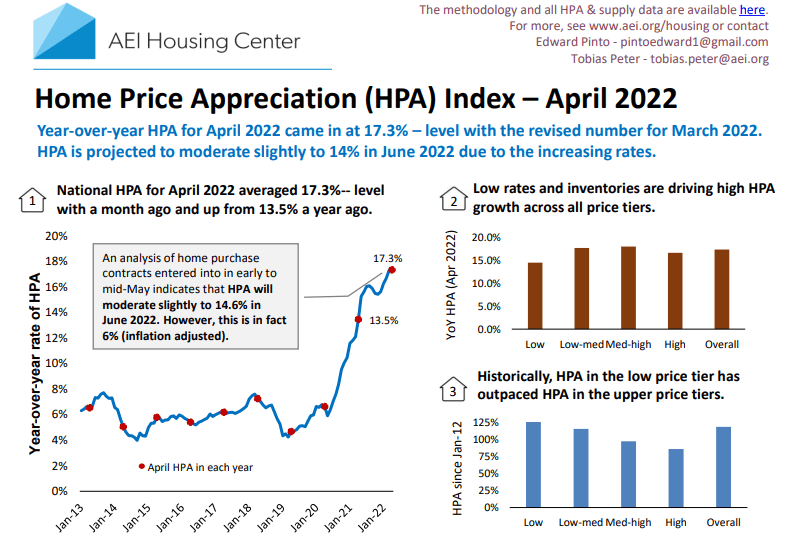

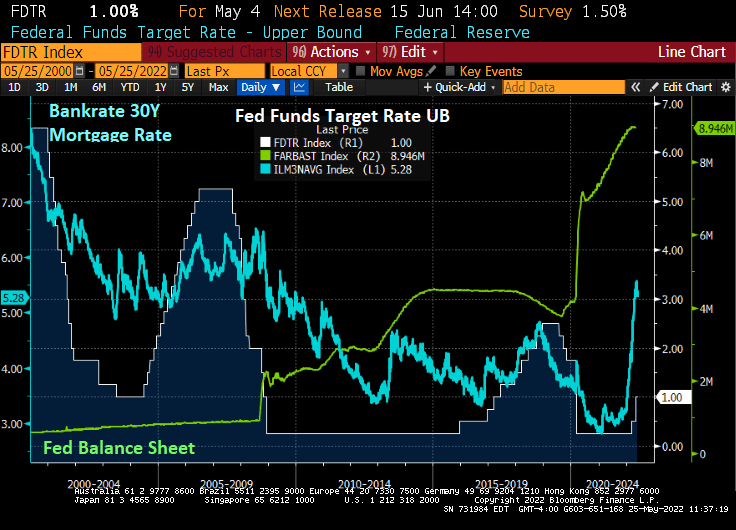

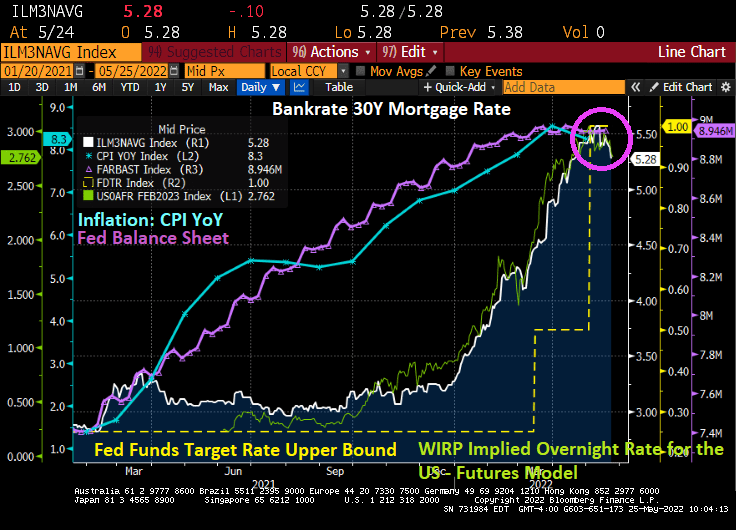

The reason why home prices are still raging at 17.3% YoY? The Fed’s monetary stimulypto is STILL in place! The Fed’s balance sheet (green line) is still staggering, and The Fed Funds target rate (white line) is a measly 1%.

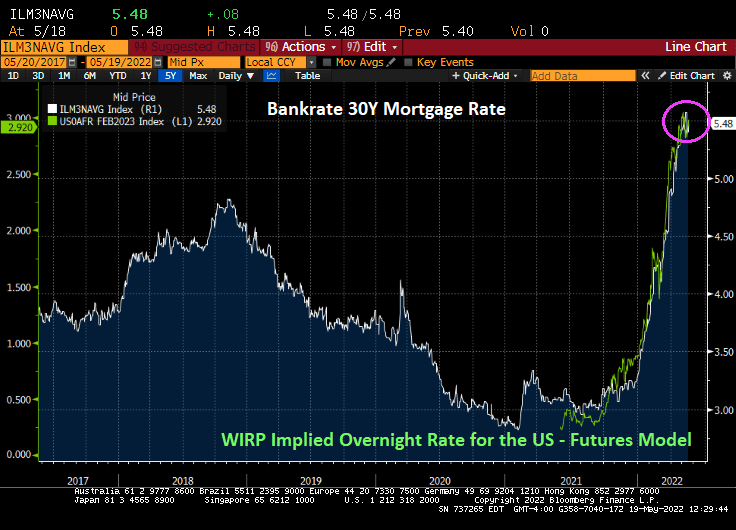

Atlanta Fed President Raphael Bostic is talking about a pause in Fed tightening. Which they haven’t paused yet.

Fed Chair Jerome Powell is really “slowhand,” not Eric Clapton. Bostic is now a member of The Fed’s “Slowhand” strategy.

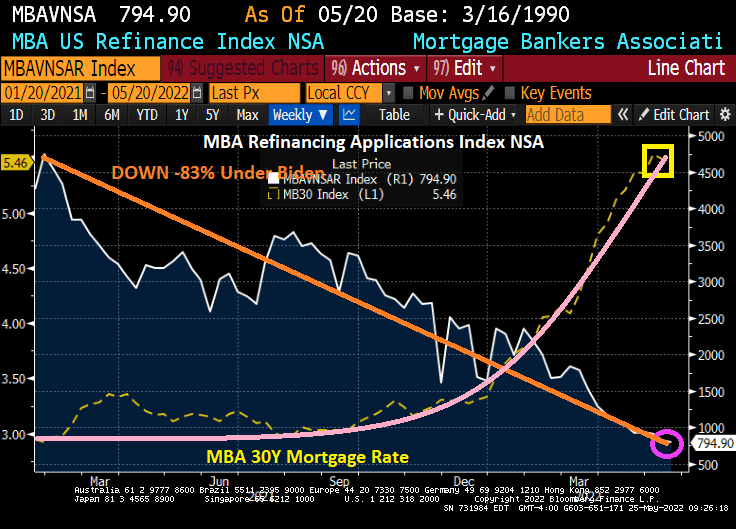

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 20, 2022.

The Refinance Index decreased 4 percent from the previous week and was 75 percent lower than the same week one year ago. And under Biden, the refinance index is down -83.2%.

The good news? The seasonally adjusted Purchase Index increased 0.2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 16 percent lower than the same week one year ago. And the mortgage purchase applications index is down -12% under Biden.

While mortgage interest rates are up 71.7% than one year ago and mortgage rates are up 87% under Biden. As The Federal Reserve signals (but not yet accomplished) monetary tightening.

Once again, The Fed is dead set on cooling inflation caused by 1) Biden’s anti-drilling policies and 2) the remnants of the Federal government spending splurge to combat Covid. The Fed has been increasing their asset purchases (purple line) as inflation increase (blue line). Now they are signaling a decline in the balance sheet (green line) in the hope that it will cool inflation. Fat chance.

Let’s see how DEAD SET The Fed is about tightening monetary policy in the face of rising energy and food prices while a war rages in Ukraine and China in a Covid lockdown.

I have never seen two Federal entities make such a mess in my life. The Federal Reserve and The Federal government.

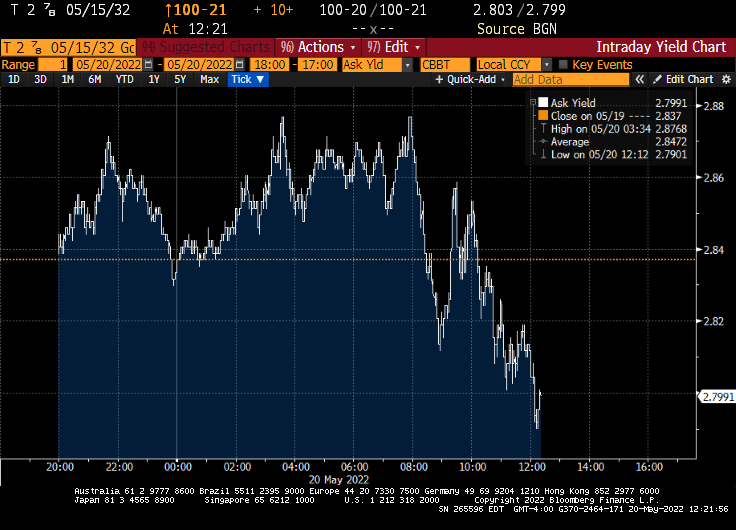

The good news? The 10-year Treasury yield is down -12.9 BPS this morning generally resulting in lower 30-year mortgage rates. Of course, the reason why the 10-yield is falling is generally bad news.

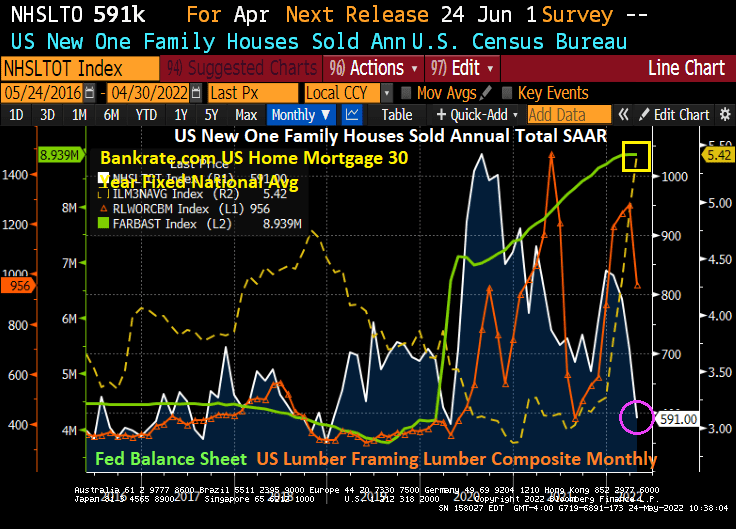

The bad news? US New Home Sales fell -16.6% MoM in April as mortgage rates skyrocketed.

Since the installation of Joe Biden as President, new home sales have plunged -31.2%, mortgage rates are up 88.9%, and framing lumber prices are up 29.2%.

Biden is out there bragging about rising energy prices which he views as a necessity to force the conversion of America to electric cars and trucks. Biden is the first President in history to gloat over the suffering of American households.

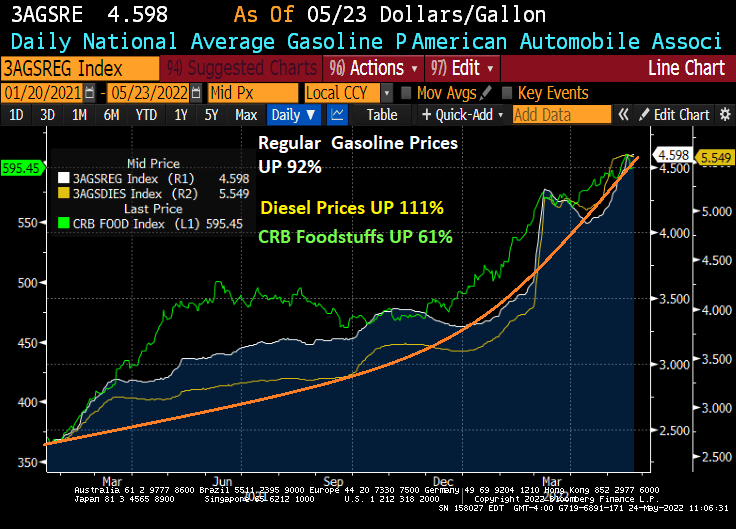

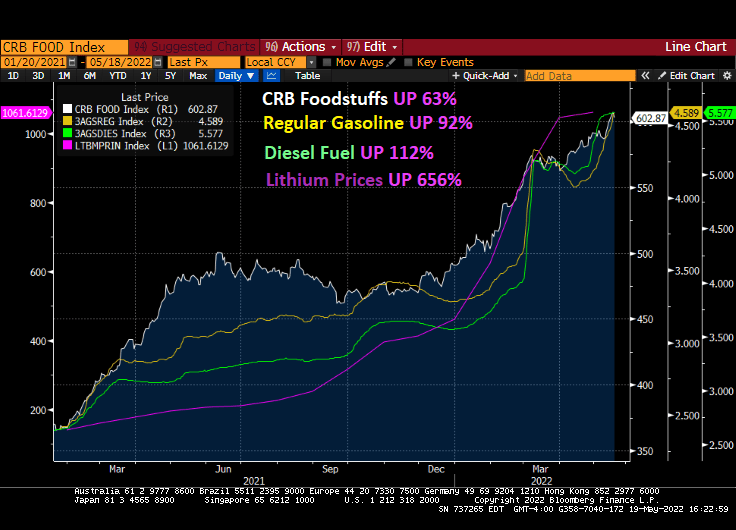

Under Biden, regular gasoline prices are up 92%, diesel prices are up 111%, and CRB Foodstuffs are up 61%.

Say, framing lumber for housing is cheaper than food. Maybe Biden will suggest Americans transform to being beavers and gnaw on wood.

As The Federal Reserve tries to fight inflation (it can’t thanks to Federal energy policies and bottlenecks), it is causing a disconnect between mortgage current coupon rate and the MBS index coupon. The disconnect is so bad that it is back to 1985 levels.

The Fed can certainly try to cool inflation, but Biden is intent on raising energy prices (leading to food price increases, and everything else) to shift us to electric cars. So, Biden is unlikely to back off.

So, The Fed is left trying to fight a war against inflation that only Biden can fight.

Meanwhile, the US mortgage market is getting pulverized

US home prices were growing at a near 20% YoY rate for the latest Case-Shiller National home price index report. But mortgage rates have soaring like a SpaceX missile shot.

Of course, I am moving to one of the metro areas in the USA where closed sales fell only -1.10% YoY in April: Columbus Ohio. I should move to San Diego CA where closed sales fell -21.4% YoY.

Of course, the US still suffers from lack of available inventory for sale.

April new listings are down -5.7% YoY. Columbus Ohio didn’t change from April ’21. San Diego is down -18.4% YoY for new listings.

Rising mortgage rates? Inflation? What a total fiasco.

Mortgage rates have increased dramatically under “Middle Class Joe” as The Federal Reserve attempts to choke-off inflation caused by … The Fed coupled with Biden’s energy policies (hope you are enjoying those high gasoline and diesel prices!) and the Federal government’s staggering spending spree under Pelosi, Schumer and McConnell.

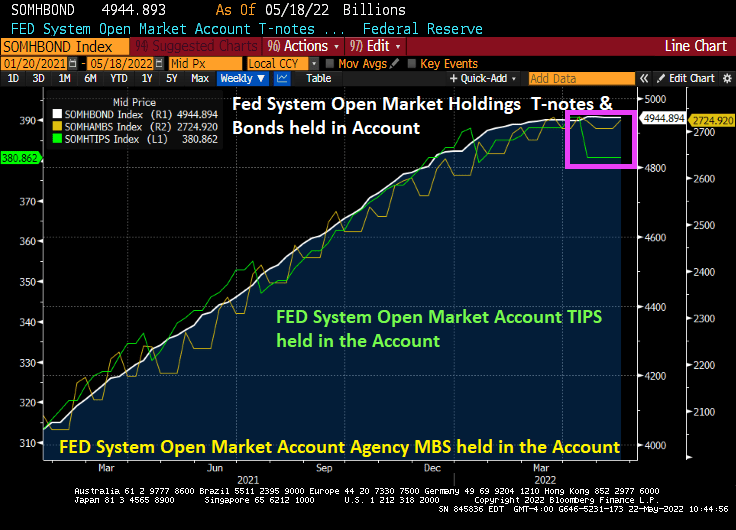

Thus far, The Federal Reserve has leveled-out out their Treasury Note and Bond purchases, increased their Agency Mortgage-backed Securities (AgMBS) holdings, but strangely have reduced their holding of Treasury Inflation-Protected Securities (TIPS) in the face of rising inflation.

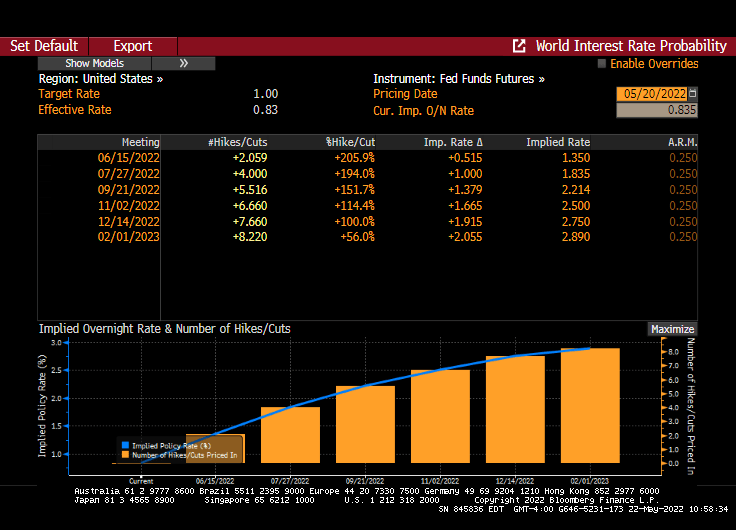

And while The Fed Funds Target rate is a lowly 1%, it is projected to rise to 2.890% by the February 1, 2023 FOMC meeting. That should send mortgage rates up.

As if mortgage rates haven’t skyrocketed already, thanks to The Fed’s jawboning about having to raise rates and extinguish inflation.

With sizzling mortgage rates (cooling a bit as the global economy slows), home mortgage payments have risen +43.4% YoY.

Now we have President Biden trying to scare us about the Monkey Pox, yet leaves the southern border wide open. One would think that Biden would shut the borders (as if the surge in Fentanyl, sex trafficking and other diseases aren’t reason enough. But I do predict another massive spending bill from Biden/Congress to combat Monkey Pox and the resurgence of Covid variants.

Meanwhile The Fed jawbones fighting inflation with monetary tightening in the future, even if they jawboning causes mortgage rates to soar and mortgage payments to spiral.

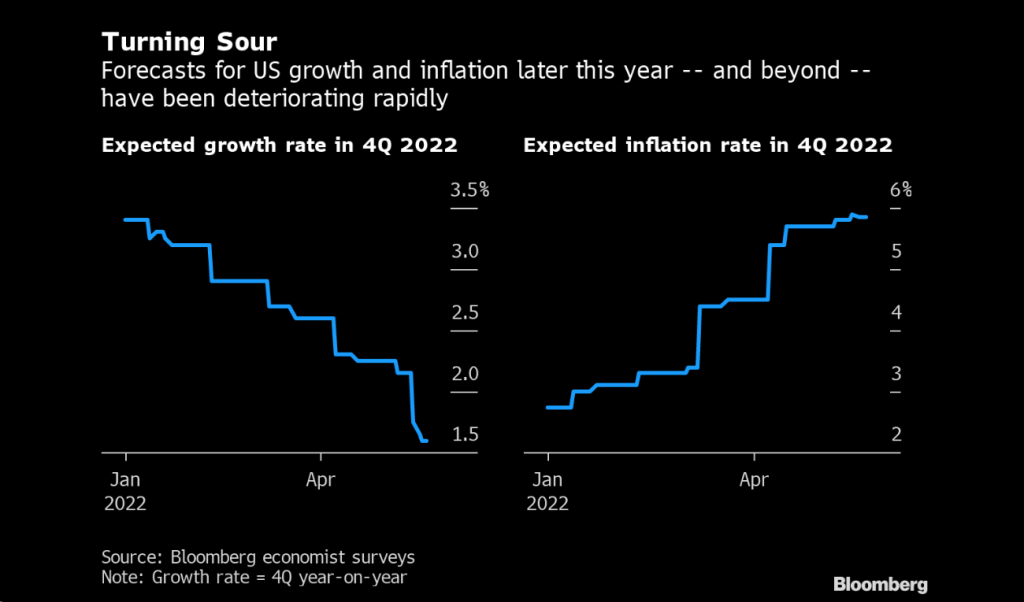

The US economy us approaching recession as inflation soars and expected growth declines.

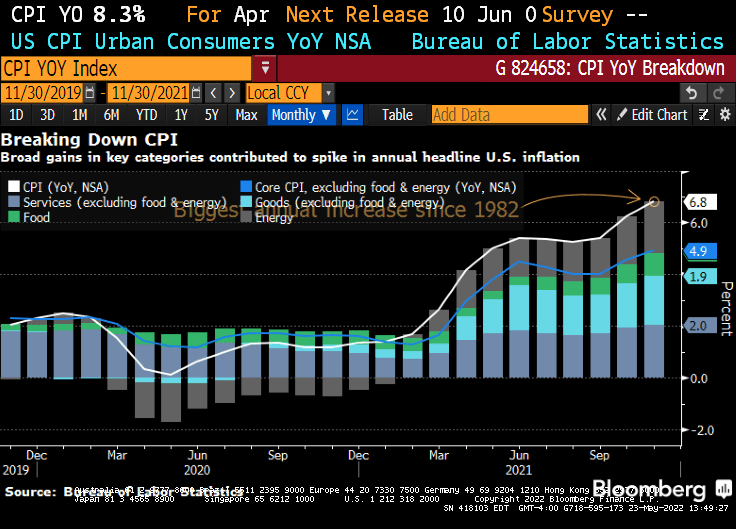

Food and energy prices are soaring, hitting middle class and low-wage households like a hammer. While the headline inflation rate is 8.3% YoY, food is up 63% under Biden and gasoline is up 92%.

The 10-year Treasury note yield is down today, which bodes well for 30-year mortgage rates.

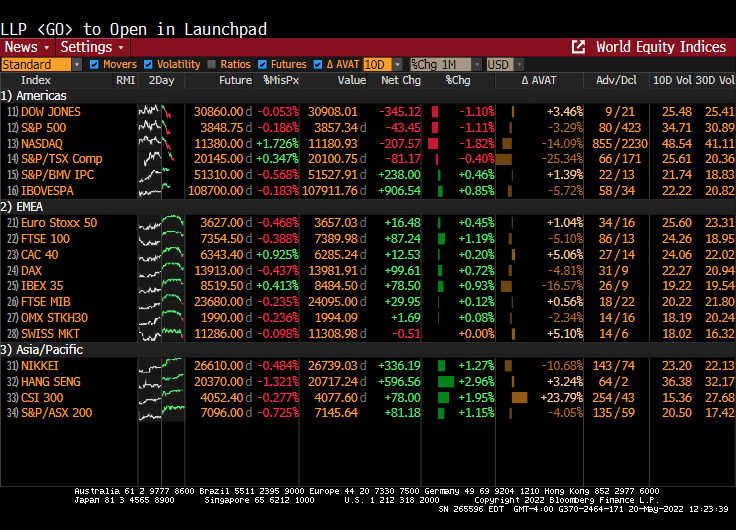

The Dow, S&P 500 and NASDAQ are all down over -1% today.

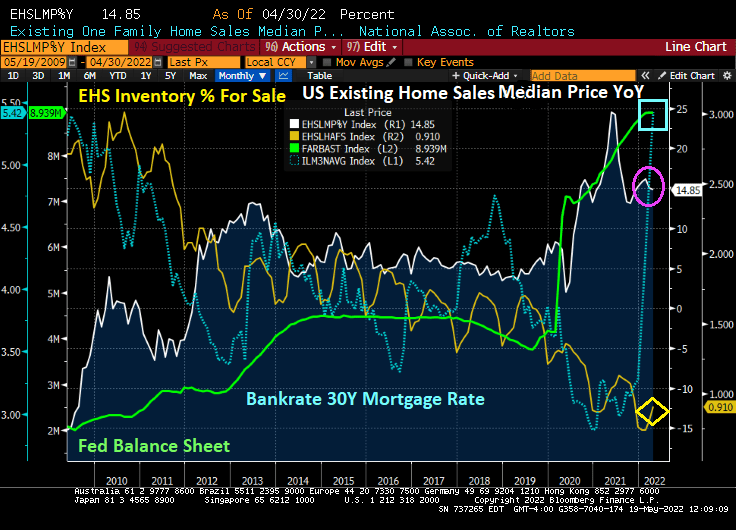

US Existing Home Sales were 5.61M SAAR in April, down -2.4% from March’s -3.0% MoM reading. But median prices YoY for existing home sales printed at 14.85%, still hot, hot, hot.

With 3 consecutive declines in MoM existing home sales, how can prices still be raging at 14.85%? First, inventory for sale in April remains low compared to 2010 (yellow line). Second, The Federal Reserve’s Stimulypto (excessive monetary easing) is still out there in force despite Jerome “Slowhand” Powell signaling rate increases (green line). 30Y mortgage rates are still rising.

Where do we go from here? 30 year mortgage rates have been climbing as The Fed signals its intents to tighten monetary policy. But with global economic slowing, Treasury yields have been coming down (like today’s -5.2 BPS drop (Germany’s 10Y Bund Yield dropped -8 BPS on slowing global economic growth).

But remember, the Existing Home Sales numbers are for April.

Mortgage applications decreased 11.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 13, 2022.

The Refinance Index decreased 10 percent from the previous week and was 76 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 12 percent from one week earlier. The unadjusted Purchase Index decreased 12 percent compared with the previous week and was 15 percent lower than the same week one year ago.

Of course, The Fed has about as much chance of slowing down energy and food prices as I do of becoming King of the United States. But Jay the Revelator may be able to cool housing demand with rising mortgage rates.

You must be logged in to post a comment.