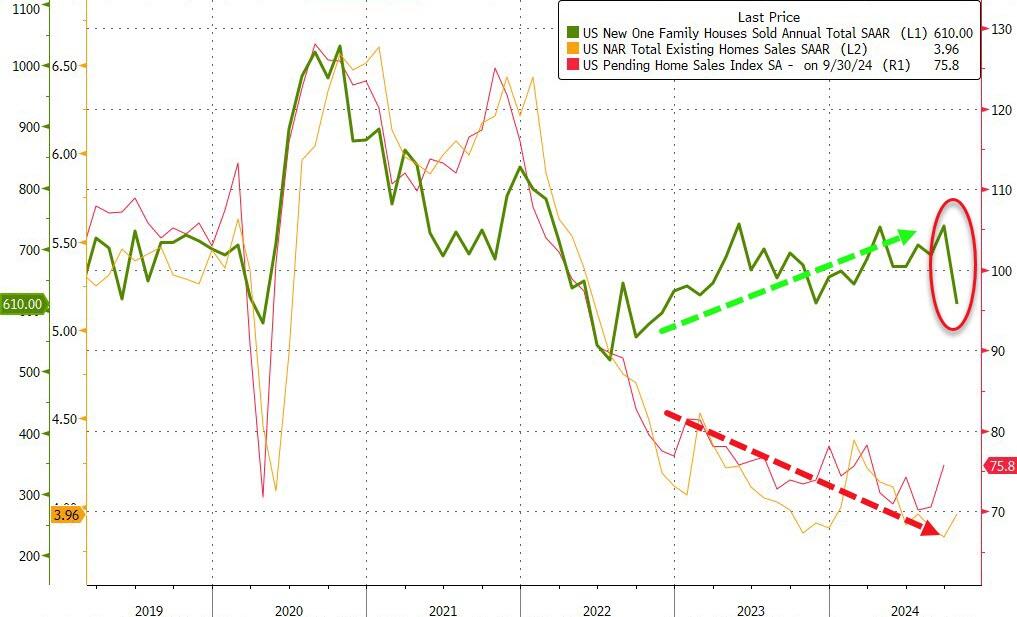

Existing-home sales have finally started to improve on a seasonally adjusted basis after a three-year decline.

Cause? Raging home prices combined with higher than normal mortgage rates. Home prices are up 35.4% under Biden while conforming 30Y mortgage rates are up 148%.

Mortgage applications decreased 21.9 percent from two weeks earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 27, 2024. The results include an adjustment to account for the Christmas holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 21.9 percent on a seasonally adjusted basis from two weeks earlier. On an unadjusted basis, the Index decreased 55 percent compared with two weeks ago. The seasonally adjusted Purchase Index decreased 13 percent compared with two weeks ago. The unadjusted Purchase Index decreased 48 percent compared with two weeks ago and was 17 percent lower than the same week one year ago.

The holiday adjusted Refinance Index decreased 36 percent from two weeks ago and was 10 percent higher than the same week one year ago. The unadjusted Refinance Index decreased 62 percent from two weeks ago and was 6 percent lower than the same week one year ago.

US home prices in the 20 largest cities rose 0.32% MoM in October (the latest data from S&P CoreLogic Case-Shiller), considerably hotter than the 0.22% rise expected. However, despite the MoM beat, the pace of annual acceleration has declined to its slowest since Sept 2023. At 3.62% YoY.

Housing Starts: Privately-owned housing starts in November were at a seasonally adjusted annual rate of 1,289,000. This is 1.8 percent below the revised October estimate of 1,312,000 and is 14.6 percent below the November 2023 rate of 1,510,000. Single-family housing starts in November were at a rate of 1,011,000; this is 6.4 percent above the revised October figure of 950,000. The November rate for units in buildings with five units or more was 264,000.

And down -10.2% year-over-year.

Building Permits: Privately-owned housing units authorized by building permits in November were at a seasonally adjusted annual rate of 1,505,000. This is 6.1 percent above the revised October rate of 1,419,000, but is 0.2 percent below the November 2023 rate of 1,508,000. Single-family authorizations in November were at a rate of 972,000; this is 0.1 percent above the revised October figure of 971,000. Authorizations of units in buildings with five units or more were at a rate of 481,000 in November.

As we watch Biden and Democrats attempt to demolish the country as Biden leaves office. Let’s see how many criminals Biden will pardon on the way out … like the Jan 6th “select” committee of Adam Schiff, Adam Kinzinger, Liz Cheney, Bennie Thompson, etc.

The delinquency rate for commercial mortgage-backed securities (CMBS) tied to office properties reached 10.4 percent in November 2024, approaching the 10.7 percent peak reached during the 2008 financial crisis. The ascent is the fastest two-year increase on record, with rates climbing 8.8 percentage points since late 2022, significantly outrunning the 6.3-point rise seen during the financial crisis nearly 15 years ago.

The office real estate sector has been grappling with a severe downturn for several years now, but are accelerating recently as they are driven by persistently high vacancy rates and declining rents. Property values, particularly for older office buildings, have plummeted, with many losing 50 to 70 percent of their market value and in some cases becoming effectively worthless. Those conditions have left real estate portfolio managers and building owners unable to borrow, refinance or sell properties, contributing to rising delinquencies and foreclosures. (Mortgages become effectively delinquent when payments are missed beyond a standard 30-day grace period.)

On the CMBS front, there have been no upgrades in 2023 and 2024.

Efforts to convert office buildings into residential spaces are increasing but remain limited by structural and economic constraints. Many office towers are unsuitable for conversion due to their large floor plates or prohibitively high retrofitting costs which often exceed the cost of demolition and rebuilding. In 2024, 73 office-to-residential conversions were completed, with an additional 30 underway. Despite plans to increase the pace in 2025, the cumulative impact remains minimal, addressing just 7.9 percent of the 902 million square feet of vacant office space nationwide.

The last gasp of the Biden/Harris reign of (economic) error!

After existing home sales unexpectedly ticked up in October, analysts expected new home sales to slow after their recent resurgence (-1.8% MoM). They were right… BUT… the magnitude is mind-boggling!

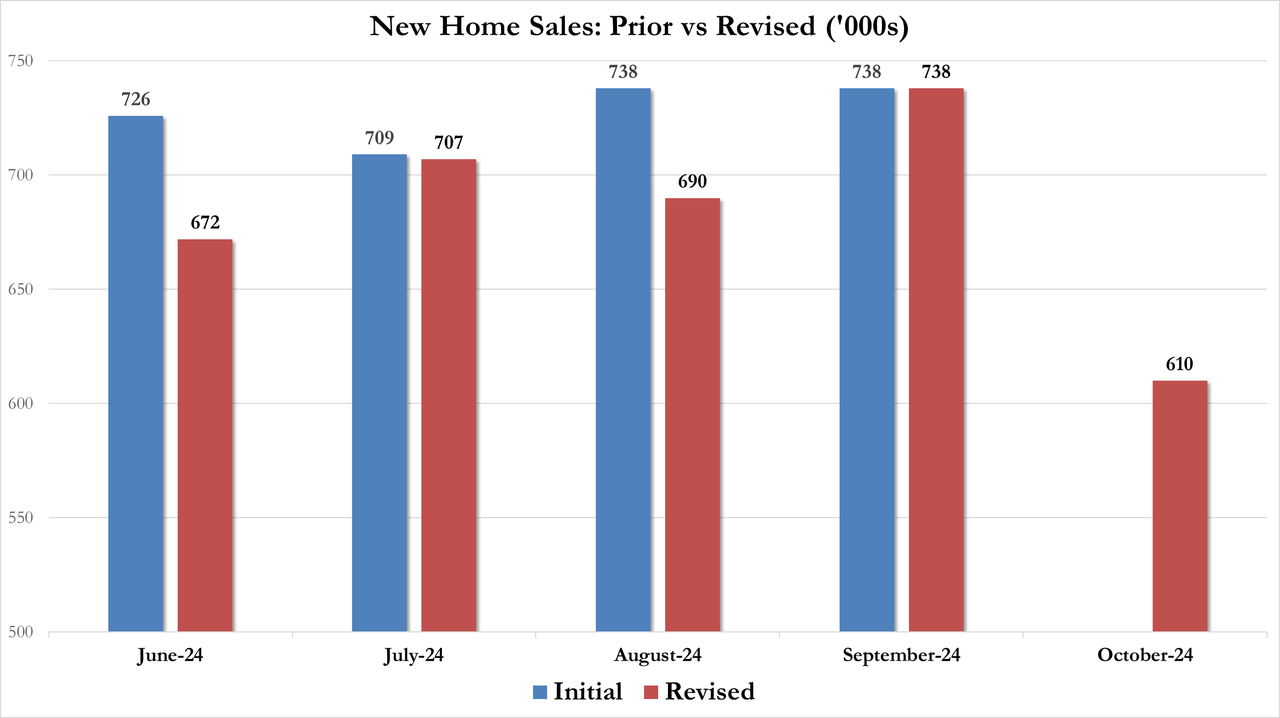

New Home Sales collapsed 17.3% MoM in October. That is the largest MoM drop since July 2013.

Source: Bloomberg

That MoM plunge dragged sales down 9.4% YoY to 610k SAAR – the lowest since Nov 2022

Source: Bloomberg

Of course, all the revisions are lower…

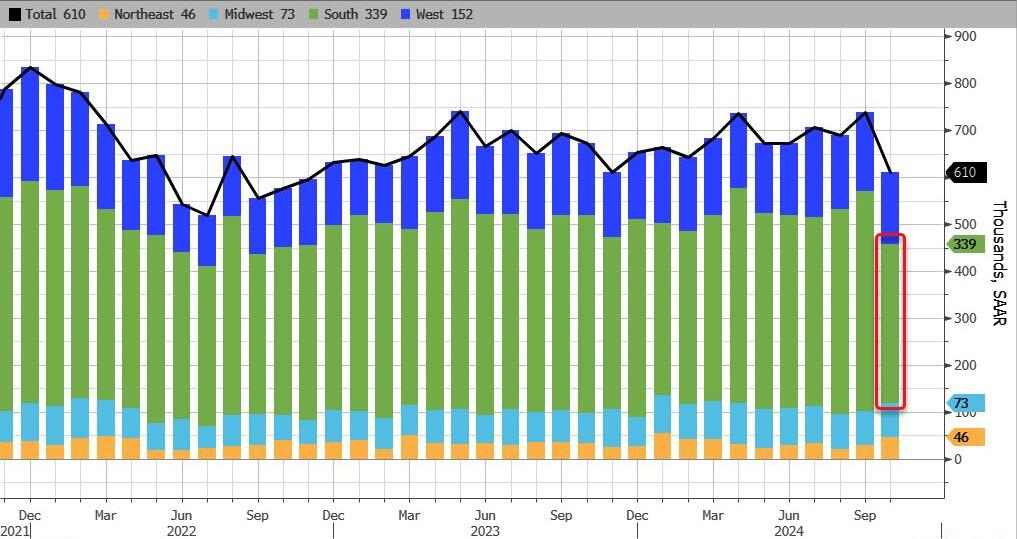

Hurricanes Helene and Milton, which tore through parts of the Southeast, delayed sales in the nation’s biggest housing region and dragged down sales overall.

Sales in the South decreased 28% to 339,000, the slowest pace since April 2020. Sales also fell in the West, but rose in the Northeast and the Midwest.

Source: Bloomberg

Finally, we note that the median sale price of a new home increased to $437,300 in October, the highest in 14 months.

Does this mean November’s data will see a massive surge in new home sales? …even as rates have increased significantly?

NEW YORK, NOVEMBER 26, 2024: S&P Dow Jones Indices (S&P DJI) today released the September 2024 results for the S&P CoreLogic Case-Shiller Indices. The leading measure of U.S. home prices recorded a 3.9% annual gain in September 2024, a slight deceleration from the previous annual gains in 2024.

YEAR-OVER-YEAR The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.9% annual return for September, down from a 4.3% annual gain in the previous month. The 10-City Composite saw an annual increase of 5.2%, down from a 6.0% annual increase in the previous month. The 20-City Composite posted a year-over-year increase of 4.6%, dropping from a 5.2% increase in the previous month. New York again reported the highest annual gain among the 20 cities with a 7.5% increase in September, followed by Cleveland and Chicago with annual increases of 7.1% and 6.9%, respectively. Denver posted the smallest year-over-year growth with 0.2%.

Table 2 below summarizes the results for September 2024. Cleveland and New York top 7% YoY.

Longer-term inflation jumped to their highest since June 2008, according to the latest UMich Sentiment survey, while short-term inflation expectations dropped to four year lows…

Housing sentiment (buying conditions for housing) remains depressed under Biden/Harris “Reign of (economic) error.”

Here is a picture depicting the assassination of the US housing market.

…but in context, that shift up to 3.96mm SAAR homes sold is nothing…

Source: Bloomberg

High borrowing costs have led to a shortage of previously owned homes on the market, discouraging many would-be home sellers from listing their properties for sale and having to part with their current low financing costs.

“Additional job gains and continued economic growth appear assured, resulting in growing housing demand,” NAR Chief Economist Lawrence Yun said in a prepared statement.

“While mortgage rates remain elevated, they are expected to stabilize.”

Last month, the inventory of available homes edged up 0.7% to 1.37 million, continuing to trend higher although well below pre-pandemic levels.

Despite the weakness in sales, tight inventory is keeping prices elevated, yielding one of the least affordable housing markets on record. The median sale price last month increased 4% from a year earlier to $407,200, the highest ever for any October, the NAR figures show.

Contract signings rose in all four US regions, led by a 6.7% jump in the Midwest.

Sales of single-family homes increased 3.5% in October; purchases of condominiums and co-ops were up 2.7%

Finally, while that’s all very exciting – a scintilla of growth off almost record lows – the fecal matter is about to strike the rotating object as rising mortgage rates lagged impact threatens…

Source: Bloomberg

In October, 59% of homes sold were on the market for less than a month, compared with 57% in September, and 19% sold above the list price. Properties remained on the market for 29 days on average, compared with 28 days in the previous month. First-time buyers made up 27% of purchases, still historically low.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.