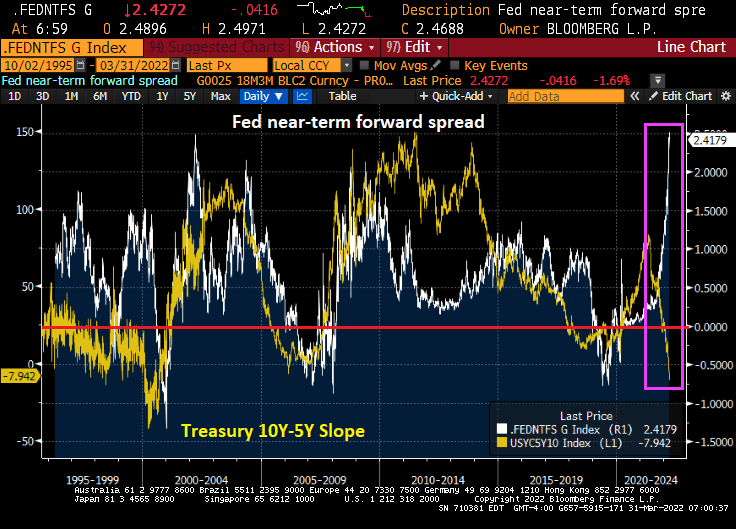

There is a massive divergence between the collapsing US Treasury 10Y-2Y yield curve and the near-term forward spread. The near-term forward spread is the difference between the implied interest rate expected on a three-month Treasury bill six quarters ahead and the current yield on a three-month Treasury bill.

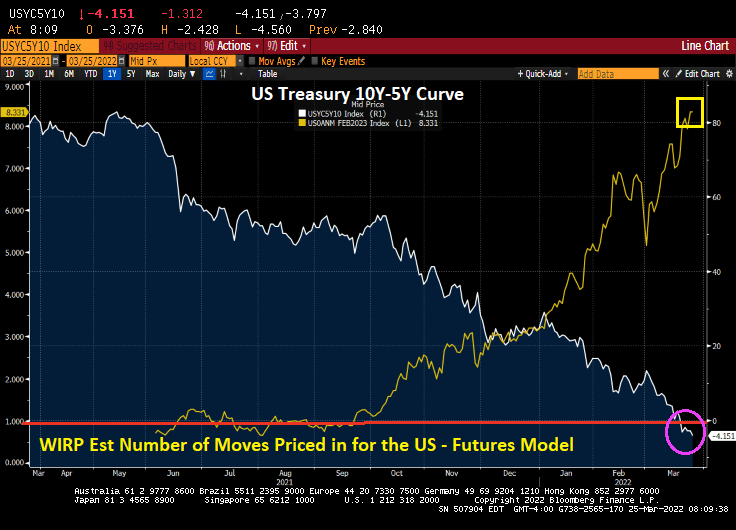

As we already know, the 10Y-5Y yield curve has inverted signaling a coming recession.

This divergence between the Treasury yield curves and the near-term forward spread is occurring as US inflation hits the highest rate in 40 years.

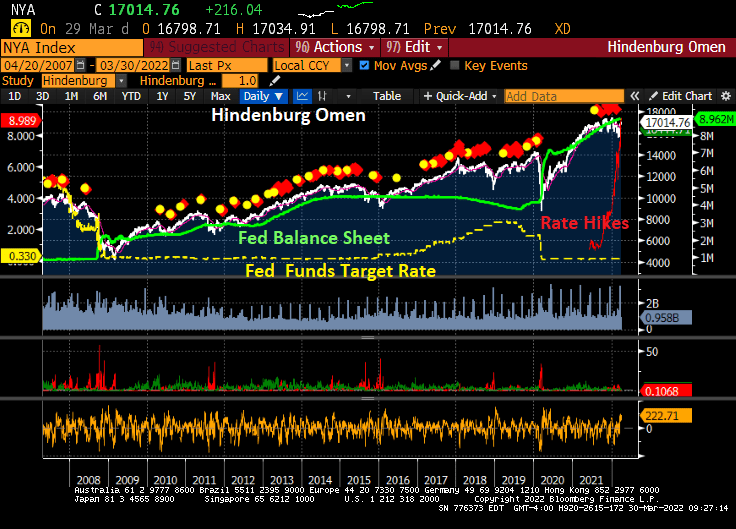

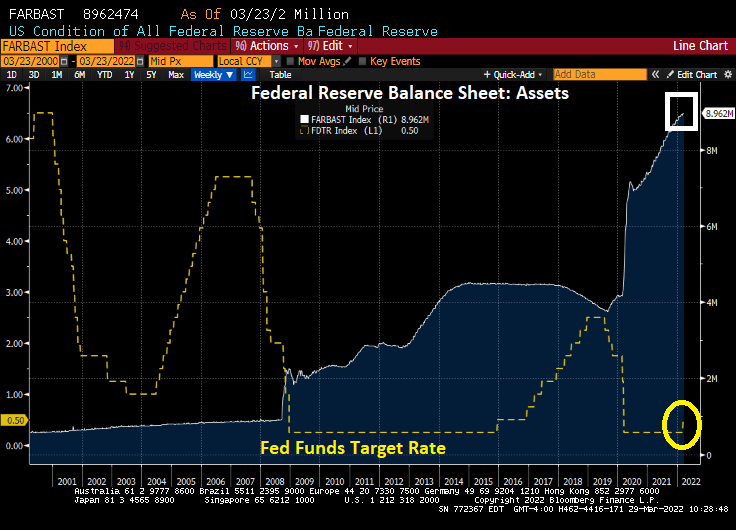

As of today, Jerome “Nero” Powell and The Gang at The Federal Reserve have not trimmed the Fed’s balance sheet and have only raised their target rate once under President Biden.

Here is the Hindenburg Omen, named for the catastrophic explosion on May 6, 1937 at Lakehurst Naval Air Station in New Jersey. The Hindenburg Omen was flashing red before the stock market correction of late 2007-2009. But, the Hindenburg Omen has flashed red repeatedly since the financial crisis, yet the S&P 500 index has kept rising. The reason? Repeated policy errors by The Fed leaving monetary stimulus in place for too long leading to a bubble forming in the stock market.

The Shiller CAPE (Cyclically-adjust price-earnings) ratio is at the second highest level since the 1800s. The highest point was the infamous Dot.com bubble and bust in 2000/2001.

Since The Fed continues to say “We have a plan!” to slow/shrink The Fed’s balance sheet and raise their target rate … it has not done anything yet (other than a 25 basis point bump at the March meeting).

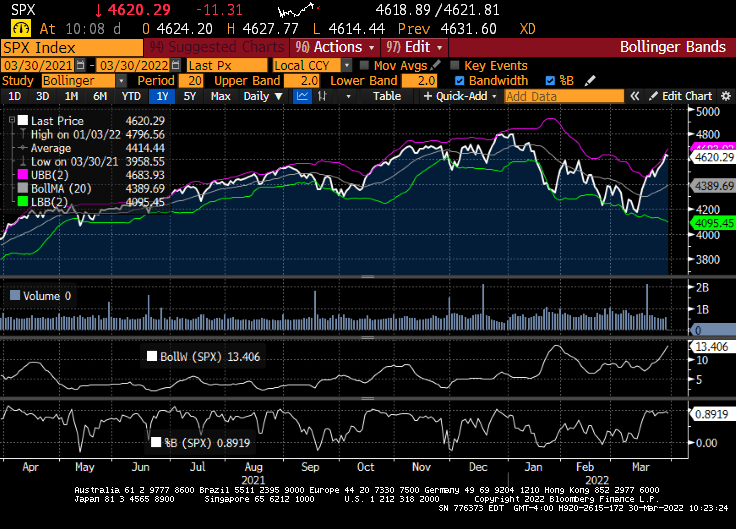

I am not advocating technical analysis for stocks, but the Bollinger Band analysis for the S&P500 index is showing the S&P 500 index near the top band indicating that a decline in likely.

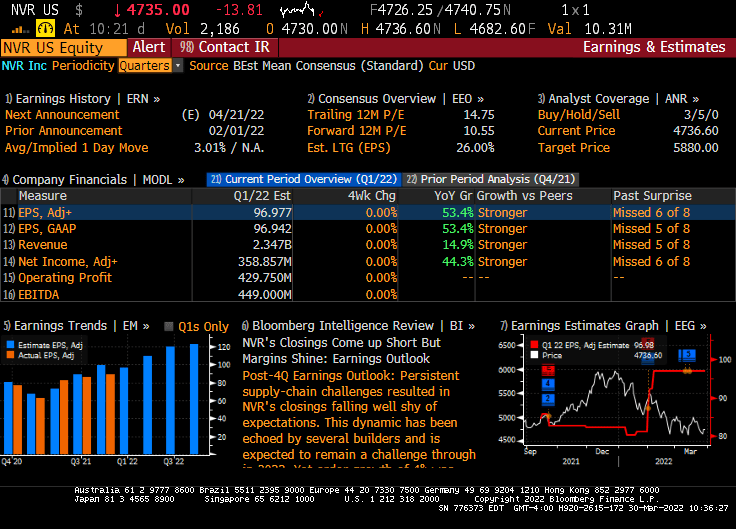

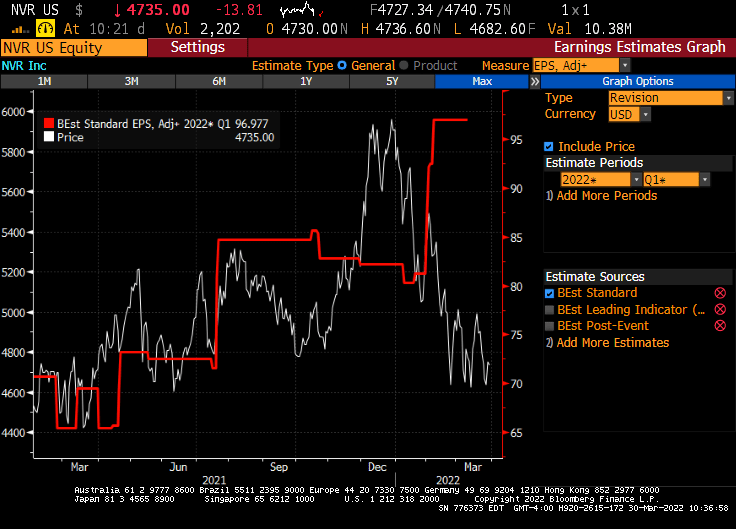

Today, the US equity market in essentially flat given the massive uncertainty about the Russia/Ukraine situation and whether the US economy is slipping into darkness. But this morning, Federal government blessed companies (healthcare, solar energy and Blackrock) are doing quite well, while homebuider NVR is taking it on the chin thanks to hints that The Fed will raising rates.

Now, NVR (Northern Virginia Homes, Ryan Homes) had explosive earnings growth in their February 1, 2022 report.

But the market is pricing in the crushing Fed rate hikes that are expected.

So, will Foul Powell pull a Volcker and raise rates and crush the economy (and stocks)? Or will Foul Powell And The Fed gang let inflation burn out of control, but preserve the massive asset bubbles?

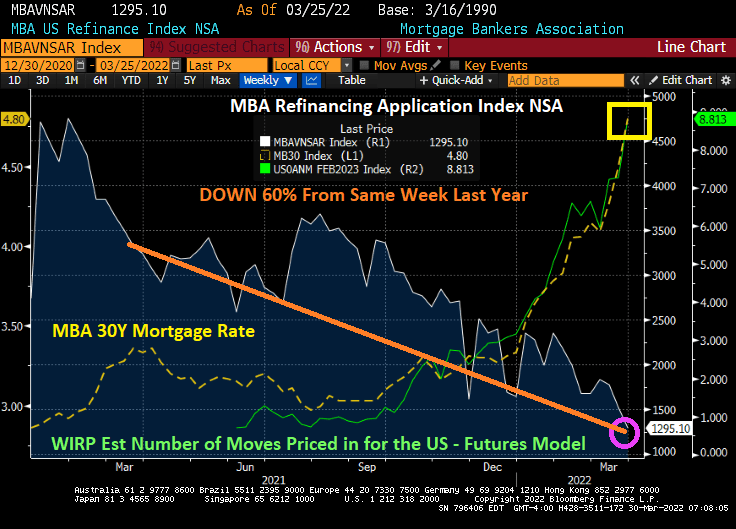

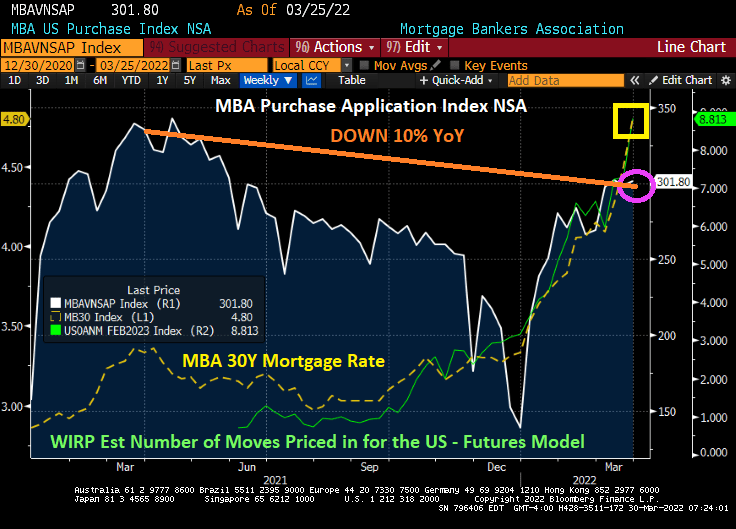

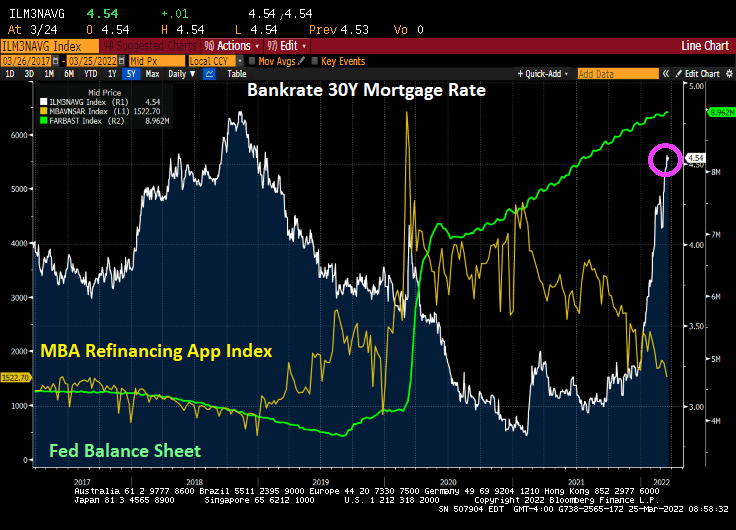

Anticipation about Federal Reserve rate hikes over the next 12 months are seeding mortgage rates soaring and mortgage refinancing applications plummeting.

Mortgage applications decreased 6.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 25, 2022.

The Refinance Index decreased 15 percent from the previous week and was 60 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 10 percent lower than the same week one year ago.

Yes, I am surprised at the rise in mortgage purchase applications with rising mortgage rates, unless, of course, people are trying to buy ahead of Fed rate increases.

Inflation is roaring along caused by government spending and energy policies, hurting the American middle class and lower-income groups.

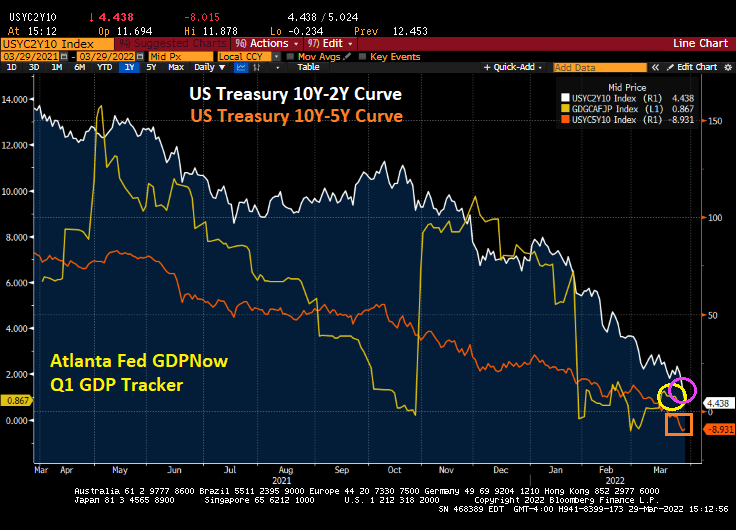

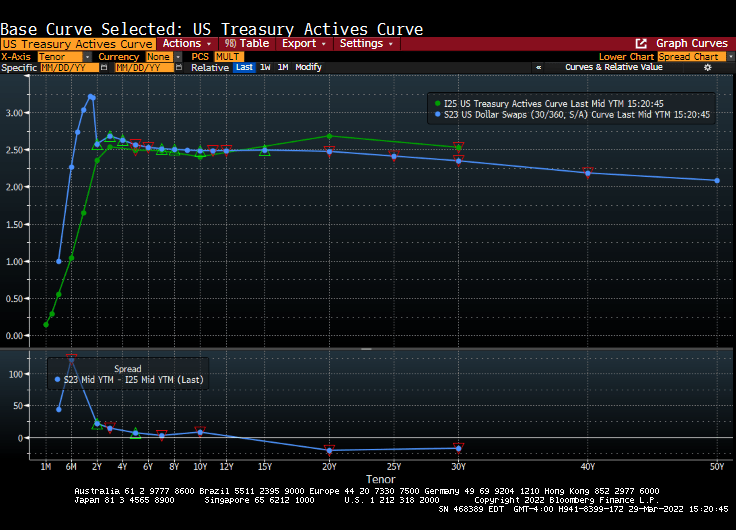

Now we see the US Treasury 10Y-2Y flattening towards zero and the10Y-5Y curve slipping deeper into inversion as Q1 GDP growth slows to 0.867.

The US yield and dollar swap curves remain steeply upward sloping, but with the dollar swap curve around 120 basis points high than the Treasury yield at the 6-month tenor.

“With inflation at a four-decade high, Fed Chair Jerome Powell has set the central bank on course for a series of interest-rate increases this year. He has stressed the toll that price increases are taking on lower-income Americans.” (No duh, Jay!)

“We understand that high inflation imposes significant hardship, especially on those least able to meet the higher costs of essentials like food, housing, and transportation,” Powell said after the Fed’s interest-rate decision this month (of only a 25 basis point increase).

Philadelphia Fed’s Patrick Harker, in a speech Tuesday, said “One of our contacts, for instance, mentioned whopping membership fee increases at his golf club, suggesting this summer may be a good time to play at your local muni instead,” said Harker, a former University of Delaware president and dean of the Wharton School of the University of Pennsylvania.

Perhaps Harker wins the Derek Zoolander award for his remarks on how the rich are impacted by inflation too.

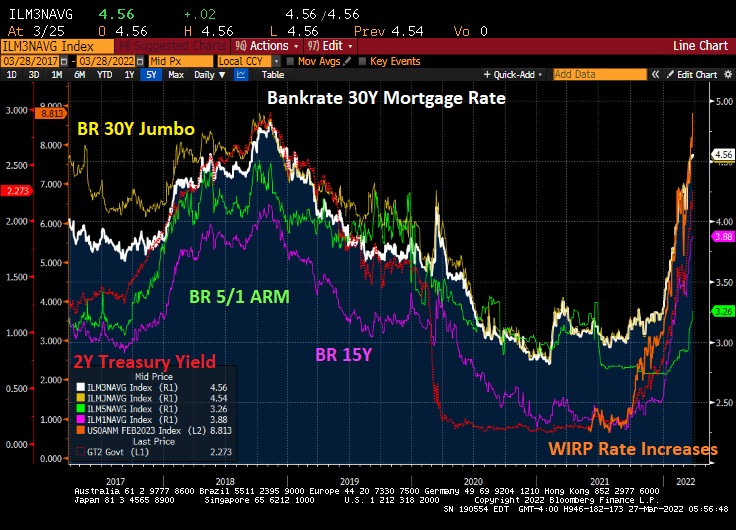

The reason why the fear of ARMs is unwarranted is that ARMs generally have CAPS on rate increases, either in a given period or over the life of the loan. Of course, READ the loan terms to ensure that the ARMs has restrictive caps on rate increases.

Currently, the 5/1 ARM is at 3.26% while the 30-year FRM is at 4.56%, a spread of 130 basis points.

Mortgage rates of all flavors are rising rapidly with the expectation of Federal Reserve Quantitative Tightening (QT). There are several headwinds that could counter The Fed’s QT efforts such as low GDP growth (Atlanta Fed’s GDPNow real-time GDP tracker is at 0.9% for Q1), the Russia-Ukraine invasion, approaching midterm elections, etc. But as of today, The Fed seems on a collision course with rising mortgage rates.

With the increasing likelihood of Fed rate hikes over the next year, we are seeing an increase in US ARM loan share from 4% to 7.9%, almost a doubling of ARM share. But FRMs are still over 90% of all mortgage originations.

Lending institutions would prefer consumers to use ARMs rather than FRMs since ARMs allow for the transfer on long-term interest rate risk to the borrower, while the FRM sticks the lender with long-term interest rate risk. Hence, we have Fannie Mae and Freddie Mac, the Government Sponsored Enterprises (GSEs) that allow lenders to originate FRMs and sell them to F&F. We are the only country with twin GSEs.

So, while most consumers would be better-off with an adjustable-rate mortgage, the structure of the mortgage market (particularly after the financial crisis) encourages lenders to originate FRMs and sell them to Fannie Mae and Freddie Mac.

But FEAR drives many US mortgage borrowers into the FRM space rather than getting an ARM with a lower interest rate, even if ARM caps would prevent the mortgage rate from rising more than 100 basis points over the life of the loan.

Unfortunately, the US Breakeven 10Y inflation rate hit another all-time high as West Texas Intermediate Crude Oil (Cushing Spot) soars.

But note that the WTI Crude spot rate is still lower than it previous peak in June 2008. What is notable in the above chart is that M2 Money growth YoY has slowed after Covid “Stimulypto”. But M2 is still growing at an 11% YoY clip, much faster growth than pre-Covid rates. So, Federal stimulypto is still in place, helping to drive inflation to the moon.

As The Biden Administration and Congress pushes Green Energy and demonizes fossil fuels, we are seeing Green Energy commodities such as Lithium (for batteries) soar even faster than oil prices.

And just an update on The US Dollar, Crypto Currencies and Gold. This is just a sample of alternatives to the US Dollar for transactions. Freedom of choice is a great thing!

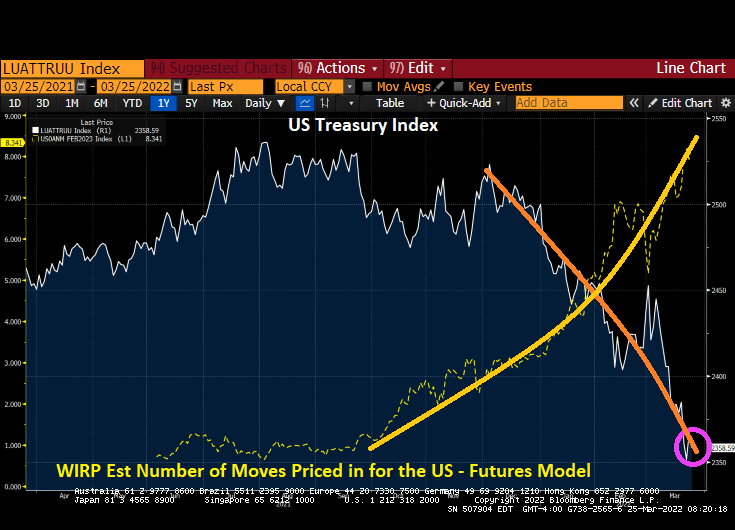

According to Fed Funds Futures data, The Federal Reserve is now forecasting 9 rate increases over the next year.

Fed Funds Futures are pointing to 8.924 rate hikes by the Fed FOMC meeting on February 1, 2023.

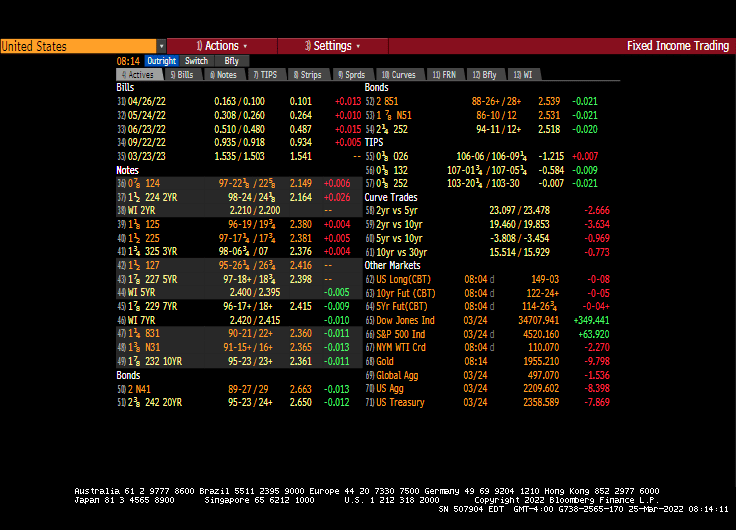

The US Treasury 10Y-2Y curve flattened by 5.5 bps today with the entire curve downshifting.

The Federal Reserve reminds me of The Office episode “Malone’s Cones.” They can’t really explain why they kept rates so low for so long (policy error) and seem to risk collapsing the market with rapid rate hikes without much sensible explanation.

You must be logged in to post a comment.