“Some participants also noted that it could be appropriate to begin to reduce the size of the Federal Reserve’s balance sheet relatively soon after beginning to raise the federal funds rate,” the minutes said.

The S&P 500 stock index extended declines following the release and was on track for its biggest loss in more than a month. Treasuries also extended losses and the dollar pared its decline.

At the conclusion of the December meeting, the FOMC announced it would wind down the Fed’s bond-buying program at a faster pace than first outlined at the previous meeting in early November, citing rising risks from inflation. The new schedule puts the central bank on track to conclude purchases in March.

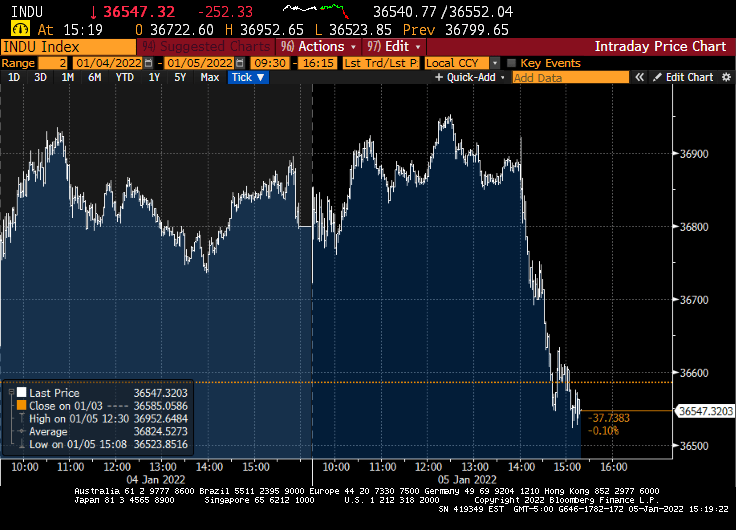

And with the minutes released, the Down dumped.

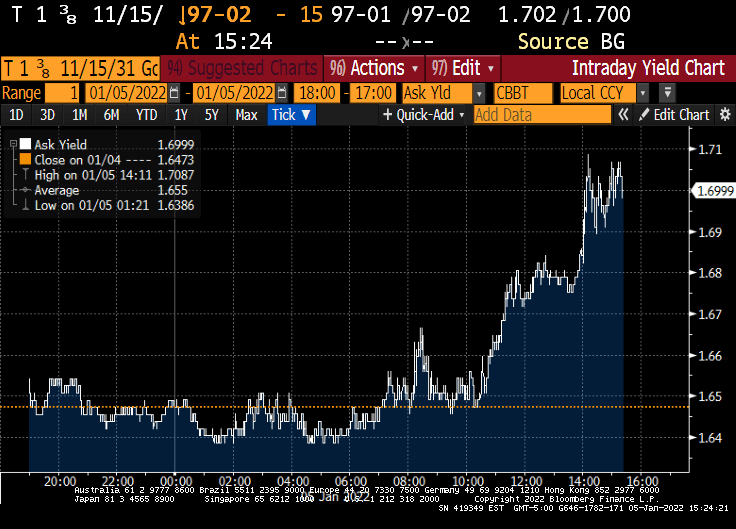

And the 10-year Treasury yield jumped 5.3 bps on the release.

When we look at the Buffett Indicator, we can see how The Federal Reserve’s loose monetary policies (or follycies) are driving up stocks to unsustainable levels that may not survive without The Fed’s “Do Ho Big Bubble Policies.”

How about the Shiller CAPE (Cyclically-adjusted Price/Earnings) ratio? While not up to dot.com levels yet, the Shiller CAPE ratio is climbing with the assistance of The Fed and their insane money printing.

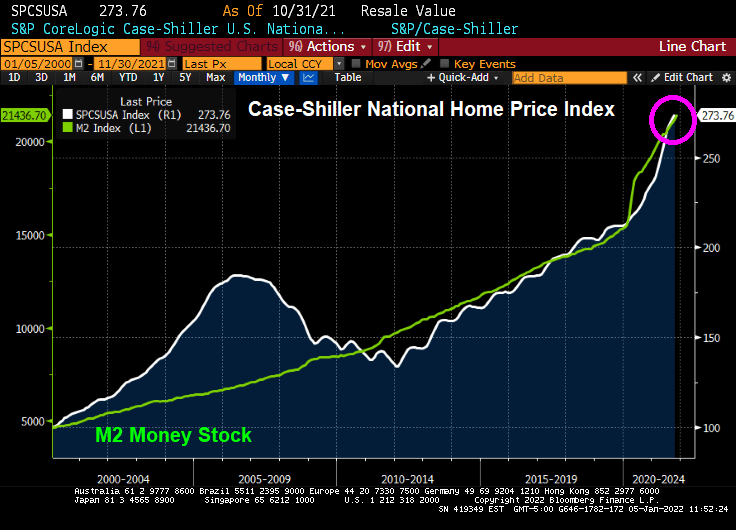

How about house prices? The Case-Shiller National home price index is far above the level last scene during the housing bubble of 2005-2007. Again, with a little help from The Federal Reserve.

I can’t wait to see how the equity market and housing market reacts IF The Fed actually follows through with reducing monetary stimulus. Probably not just adding more stimulus, just reinvesting the Treasury and MBS proceeds (aka, not shrinking the balance sheet).

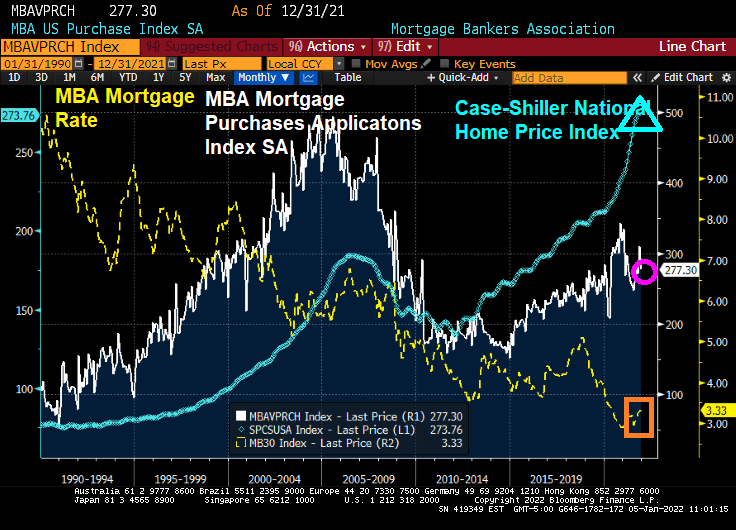

The last mortgage purchase applications index from the Mortgage Bankers Association was released this morning. The headline is “Mortgage Purchase Applications Plunge 10% WoW (since the previous week). But this is called “Seasonality.” And it happens EVERY YEAR.

Here is a chart of mortgage purchase application (NON-seasonally adjusted). What will happen when the new year starts and purchase applications began rising?

Whether seasonally-adjusted or not, all number are down for the final week of 2021, except for the 30-year mortgage rate that rose 60 basis points.

On a seasonally-adjusted basis (aka, smoothed-out), we can see the impact of super-low mortgage rates on home prices.

Here is the data summary for the last week of December 2021. All indices are down … except for the 30 year mortgage rate which was up 60 basis points.

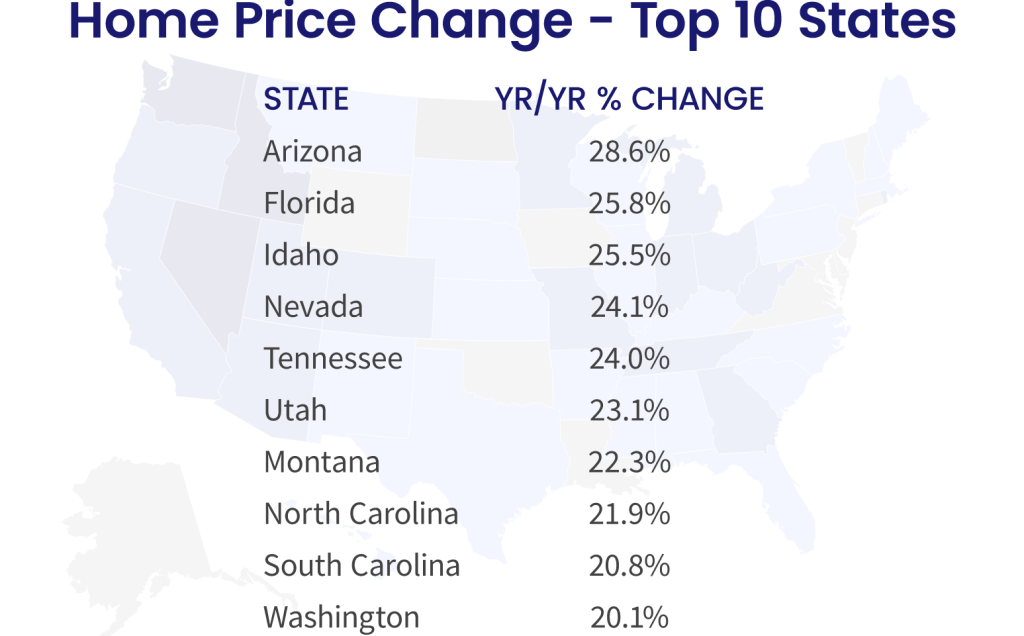

The inventory of existing homes for sale in the US is extremely low. The lack of available inventory to buy is helping drive home prices through the roof.

Available inventory for purchase peaked back in the 2007-2008 period during the dreaded housing bubble in the US. But inventory for sale has declined ever since. Why?

I think it has something to do with the aging of the US population. Look at this chart of Existing Home Sales Inventory against the growth 65+ years old.

Perhaps households 65+ are resisting moving to states like Florida and Arizona as they had in the past, leaving them stationary in their dwelling.

Another reason for the bewildering lack of inventory is the growth of the HECM (Home Equity Conversion Mortgage) that allows elderly households to drain the equity in their home rather than have to sell to utilize it. But HECMs have not taken-off sufficiently to explain the mystery of the missing inventory.

So we know that housing inventory is very low and we know that the number of Americans 65 and over is increasing. But we do not know the reason for the decline in inventory.

Treasury yields rose a second day, with five-year rates hitting the highest since before the pandemic took hold in the U.S., amid increasing conviction that the Federal Reserve will raise rates at least three times beginning in May.

The five-year Treasury note’s yield climbed as much as 3.8 basis points to 1.392%, the highest since Feb. 20, 2020, while 30-year yields bumped up toward their 200-day moving average.

Yields across the curve are rising for a second straight day, after Monday’s selloff lifted the 10-year note’s yield by nearly 12 basis points in its worst start to a year since 2009. The two-year yield topped 0.80% for the first time since March 2020.

At the 10-year mark, we see Canada’s sovereign notes rising 18.7 basis points.

Also at the 10 year mark, we see the US 1-year breakeven inflation rate (red line) surging.

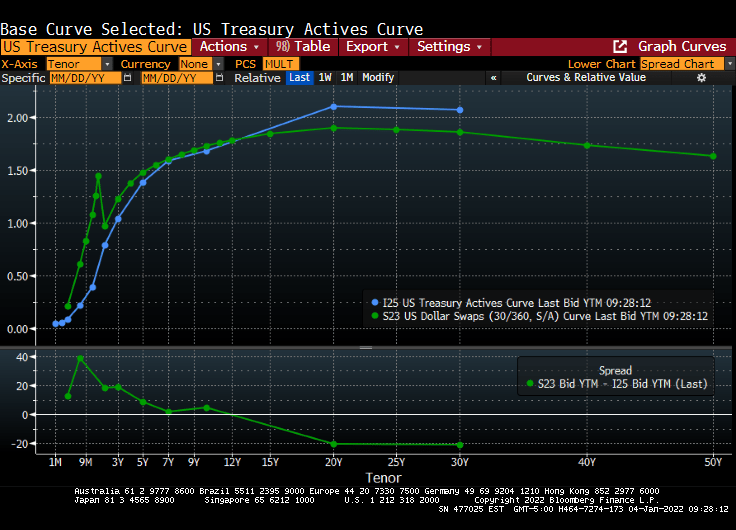

The US Treasury actives curve and Dollar Swaps curve remain steeply upward sloping.

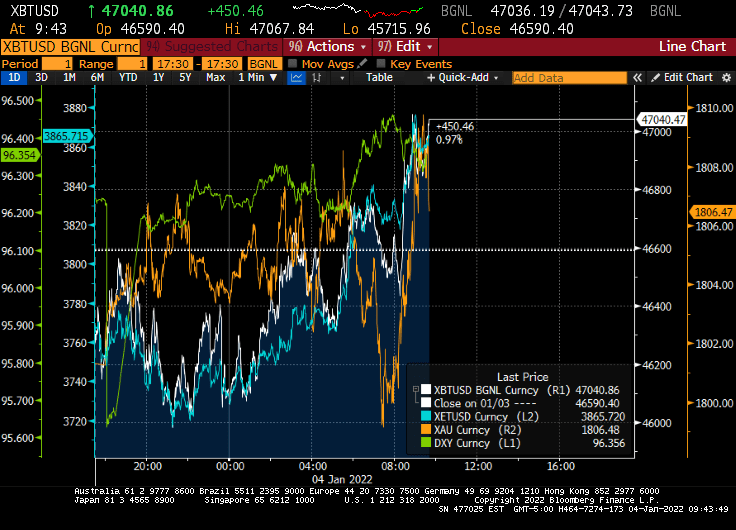

And on the crypto and gold front, gold surged this morning after tanking in the evening, while Ethereum (blue) is doing quite well along with Bitcoin.

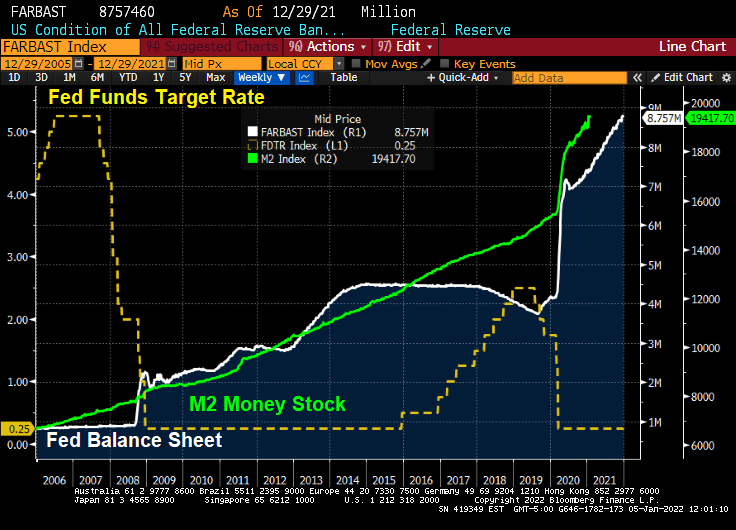

My favorite non-bond, non-alt investment chart. The S&P 500 index charted against The Fed’s M2 Money Stock.

Following my friend Jesse’s habit of posting great French food dishes, here is one from my favorite Parisian eatery, Le Duc de Richelieu. Mmmmmmm.

Happy New Year! And Treasuries are off to fast start with investors bailing on Treasuries and buying stocks. AND the expectation that The Fed will raise rates 3 times this year.

The 10-year Treasury Note yield rose above 1.60% this morning.

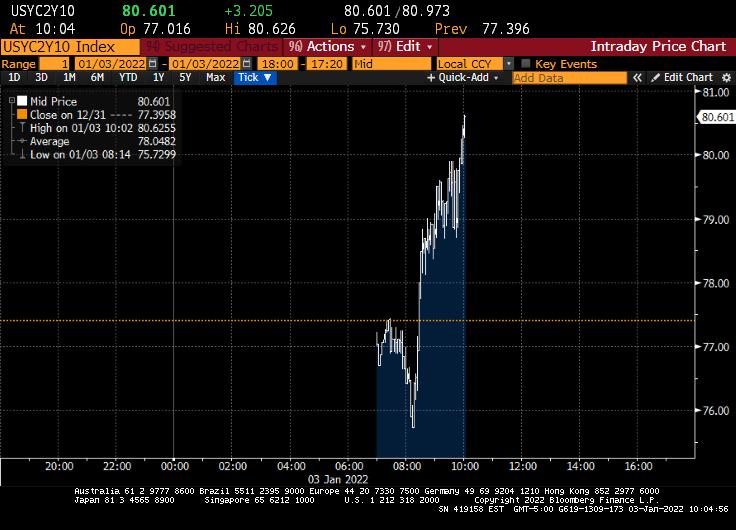

And the US Treasury 10Y-2Y curve rose to 80.601 basis points.

Fed Funds Futures data is showing 3 rates hikes in 2022. May, September and December.

The Fed Dots project is definitely showing an upward trend in the Fed Funds Target rate with FOMC member forecasting the median target rate to be above 2% by 2024.

Of course, Fed reverse repo activity grew to an all-time high (but it is expected to pare-back).

How about mortgage rates? I expect mortgages rates to rise over 2022 as the 10-year Treasury Note rises.

Cautionary note: The Fed is likely to protect economic growth and ignore inflation. So I expect FOMC will continue to reinvest prepayments into Treasury and MBS, pro-rata to the current portfolio.

A good quote from The Hill story: “Under Biden, the American economy has recovered from its Trump-era lows with remarkable speed.” As Leslie Knope said “That seems like an unfair phrasing.”

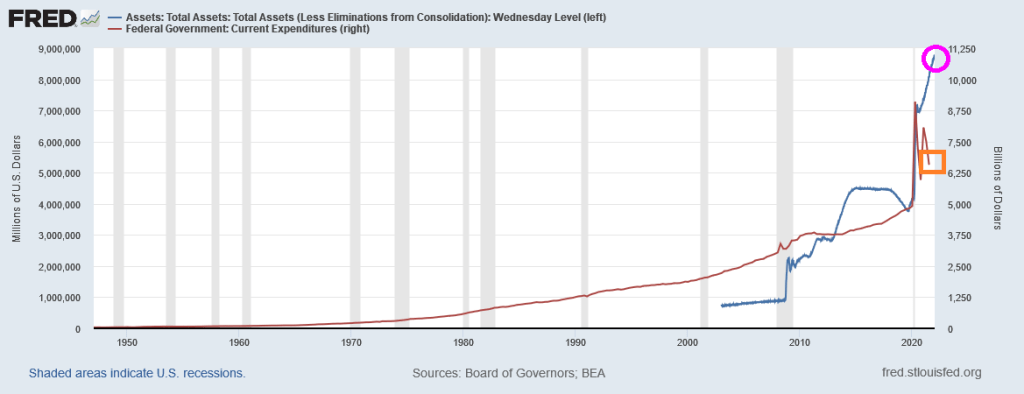

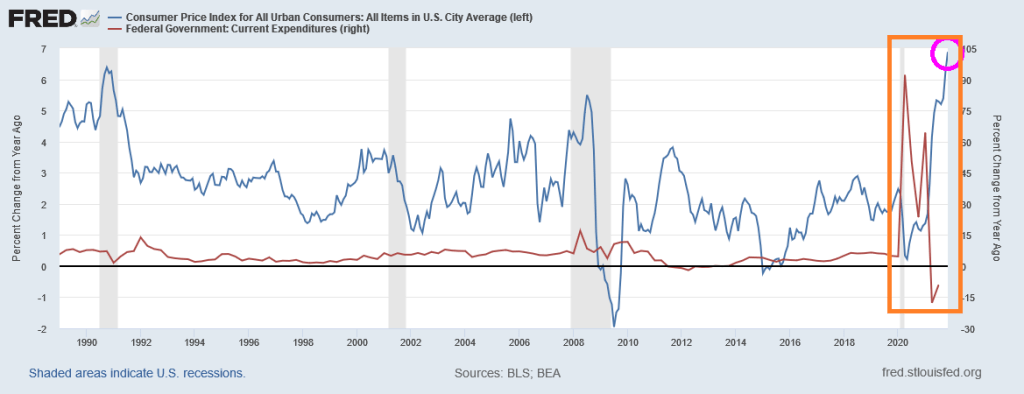

Hmm. Well, here is a chart that best explains the “Biden Miracle.” It shows the growth in Federal expenditures from the previous year during the banking crisis and then the COVID crisis. During the banking crisis, the increase in Federal expenditures (red) was normal. It was the increase in The Fed’s balance sheet (blue) that was staggering. But for the mini-recession related to COVID (only two months so you can barely see it on the chart below), it was the growth in Federal expenditures (red) combined with another round of staggering Federal Reserve stimulus (blue).

A different view of Federal “Stimulypto” is show below. Since COVID and the election of Joe Biden as President, Fed monetary stimulus is at an all-time high and Federal expenditures, while they have slowed, are still above the pre-COVID spending levels.

Please note that the massive surge in Federal expenditures and Fed monetary stimulus began under Trump, but were only continued under Biden. That is why no one notices … it was Trump.

And if we look at the 10Y-2Y Treasury curve slope, the US is slippin’ into darkness since the slope typically rises after a recession, then falls. And we are in the falling (or slippin’) stage.

So, President Biden is benefiting from Trump’s and The Fed’s Stimulypto. I don’t expect partisan outlets like The Hill or crooner Barbra Streisand to look at the data.

With Build Back (Inflation) Better not passing in the US Senate, I fully expect The Federal Reserve to continue “low riding” interest rates. Inflation will probably cool as well as Federal expenditure growth slows.

So, Streisand’s statement should have said “Joe Biden’s economic record in his first year is the best in 40 years. The media largely ignores this … because the unsustainable Federal stimulus began under Trump, not Biden.”

Another thing The Hill and Barbra Streisand left out was declining REAL average hourly earnings growth (that is, average hourly earnings YoY – inflation).

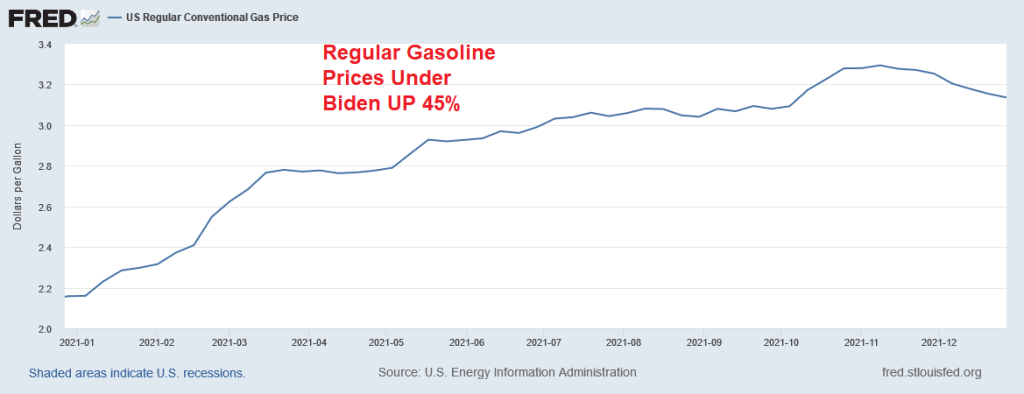

Biden’s real contribution? Anti-fossil fuels actions have driven up energy prices. Regular gasoline prices, for example, are up 45% under Biden.

If The Fed actually follows through and removes COVID stimulus and Congress doesn’t keep the incredible rate Federal spending growing, I sincerely doubt that GDP will continue at this hot pace.

Inflation is the highest in 40 years. There used to be a lot of discussion about hedging against inflation in the 1970s and 1980s, but discussion subsided as inflation cooled in the US. But now it is roaring back as Fed monetary stimulus continues unabated and The Federal government continues to spends like crazy.

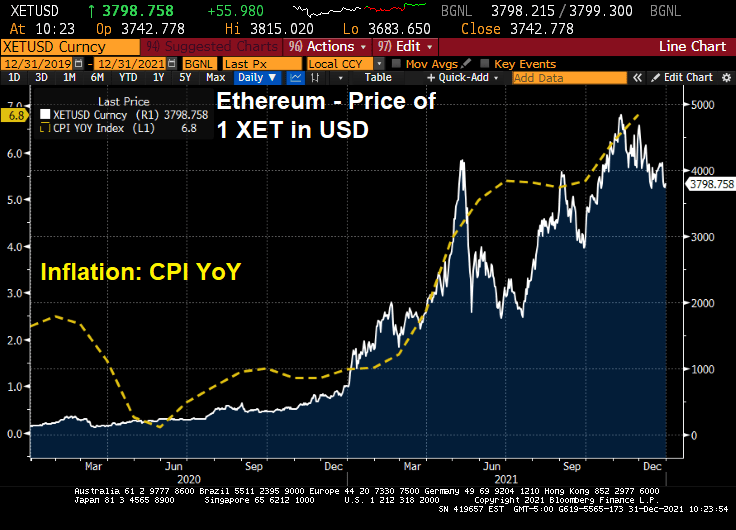

So, how do we protect ourselves against inflation caused by Federal government policies (or follicies)? How about cryptocurrencies like Ethereum?

Ethereum really started to take off as US inflation took off. Not a perfect fit (or hedge), but on average Ethereum has kept up with inflation.

If you believe in technical analysis, Ethereum is in the 3rd wave on the downside.

But if you believe the Ichimoku Cloud, Ethereum lies BELOW the cloud indicating that Ethereum is likely to rise.

Bear in mind that Biden’s energy policies have created large increases in energy prices which lead to large increases in other products such as food prices. Again, not all inflation is due to Federal policies. Arabica coffee prices are driven by droughts and excessive rainfall, etc. But inflation causes a rise in agriculture prices due to transportation cost increases, increases in fertilizer prices (thank to natural gas price increases), and panic buying by consumers.

Despite what Federal officials jawbone about, inflation has momentum and is unlikely to swiftly subside, particularly if the Build Back (Inflation) Better Act passes in 2022.

Remember, consumer purchasing power of the US Dollar has declined dramatically since the creation of The Federal Reserve System in 1913. The Fed isn’t going away and neither is wasteful Federal spending, like BBB.

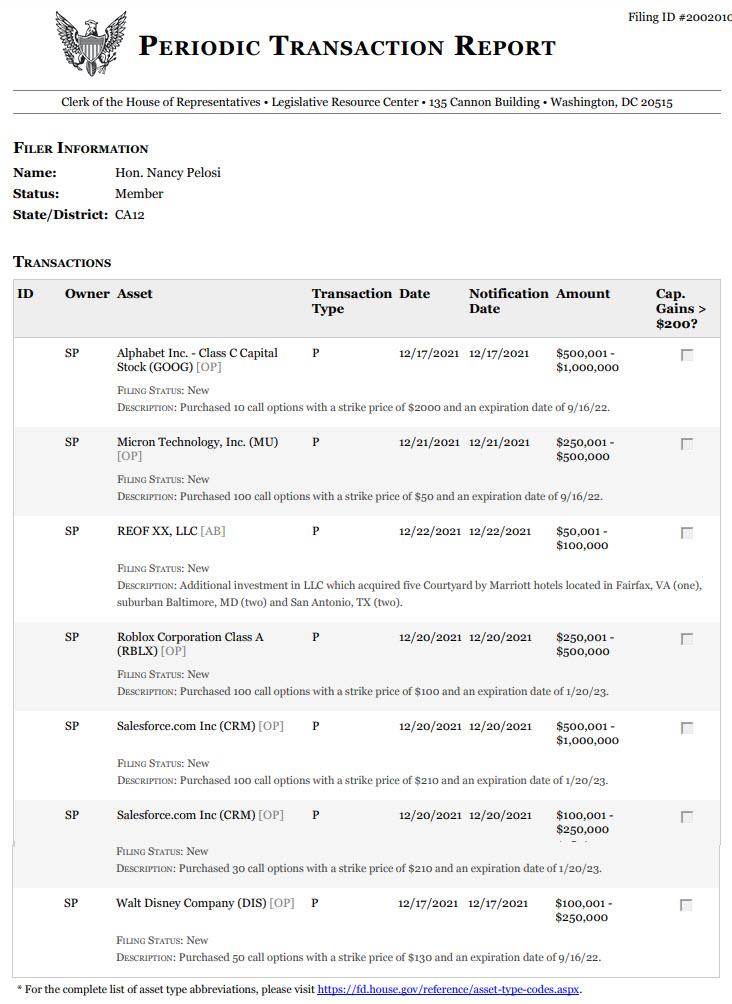

I thought US House Speaker Nancy Pelosi was going to retire, but now it looks like she wants to keep inside trading with information about regulation and government spending that investors don’t have.

Largely, her investments were in call options for Disney, Saleforce, Roblox, Micron and Google (Alphabet).

I would prefer that she retire and replace Cramer on CNBC’s Mad Money. So she could bang the gong instead of her gavel. Or call it CNBC Investing Club with Nancy Pelosi.

Her defense that she should be allowed to invest in stocks and options since the US is a free-market economy was comical at best, and extremely hypocritical at worst.

You must be logged in to post a comment.