The US mortgage market is livin’ la vida Biden! And for the US mortgage market, la vida Biden in ugly.

Mortgage applications decreased 3.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 4, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The Refinance Index decreased 4 percent from the previous week and was 37 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was27 percent lower than the same week one year ago.

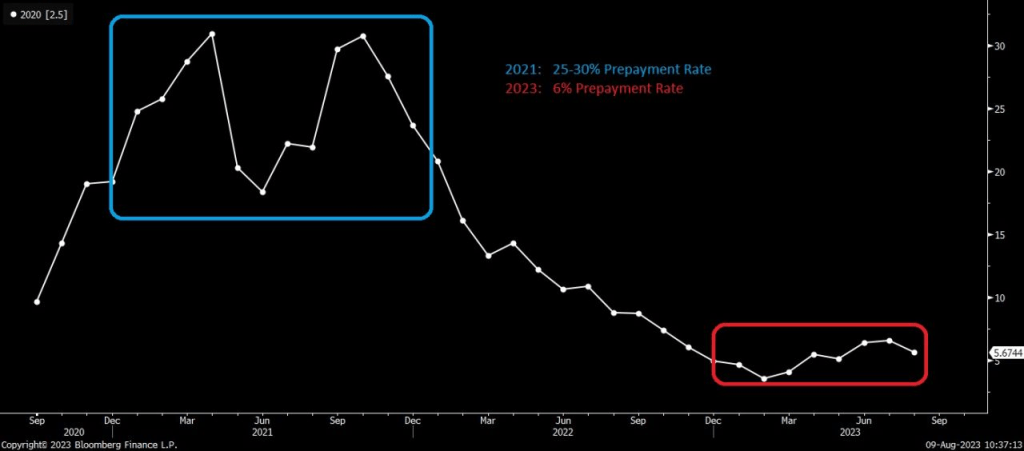

Here is a chart of mortgage purchase applications with Biden’s record in the orange box.

Prepayment rates with rising mortgage rates (to try to cool Bidenflation) are now low by historic standards.

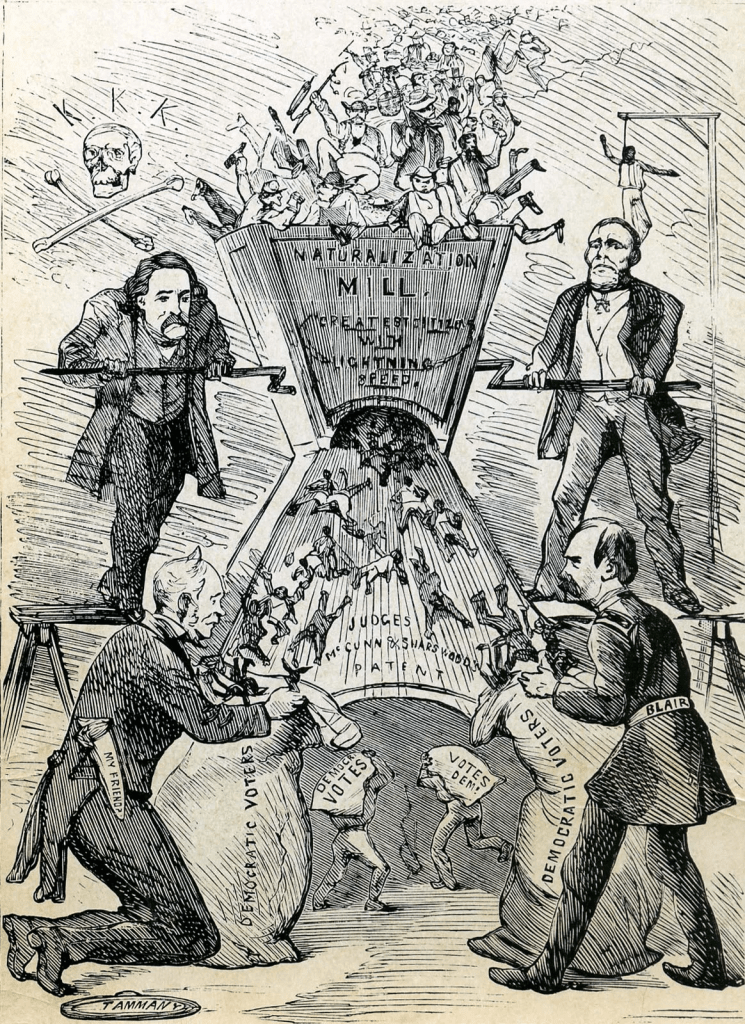

Here is a photo of Joe Biden (or is that Boss Tweed of NYC’s Tammany Hall)? Doesn’t matter because they are both the same corrupt person.

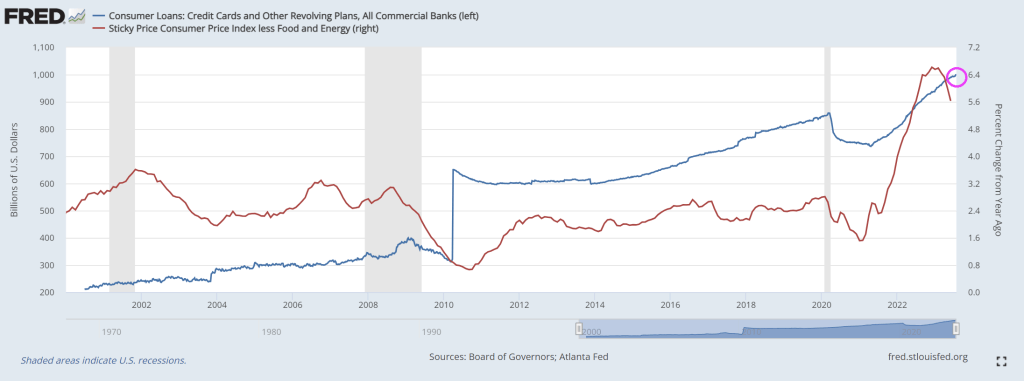

One of the themesongs of Biden’s Bidenomics should be Credit Card (CC) Rider, since consumers are turning to credit cards to cope with high inflation (Bidenomics).

US credit card debt oustanding just passed the $1 trillion mark as consumers continue to struggle with effects of inflation. Caused by The Federal Reserve and insame Federal spending. Note that sticky core inflation is still at 5.63%.

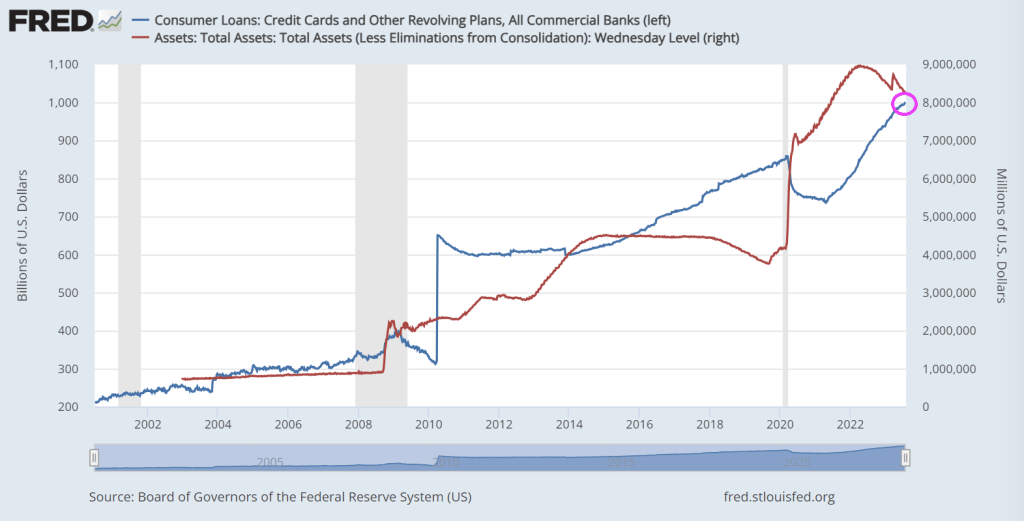

If we look at credit card debt compare to The Fed’s balance sheet, we see the relationship.

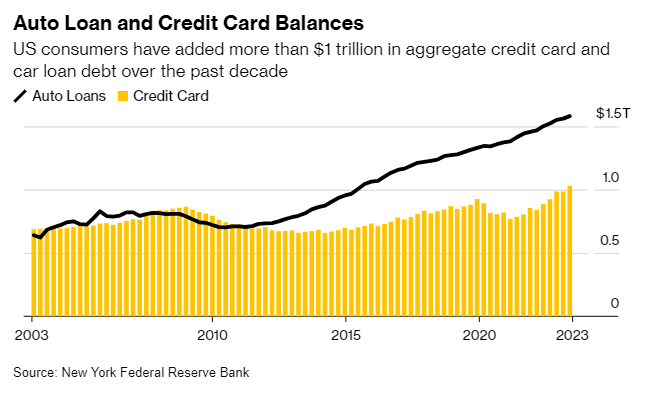

Credit cards + auto loan balances are now over $1.6 trillion.

Biden is currently out west trying to sell Bidenomics while announcing prohibitions on uranium m

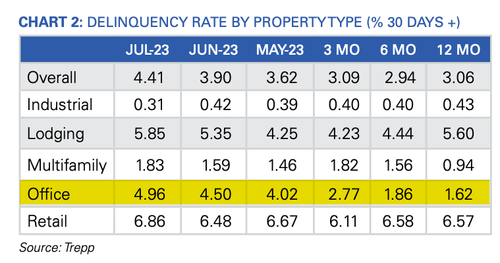

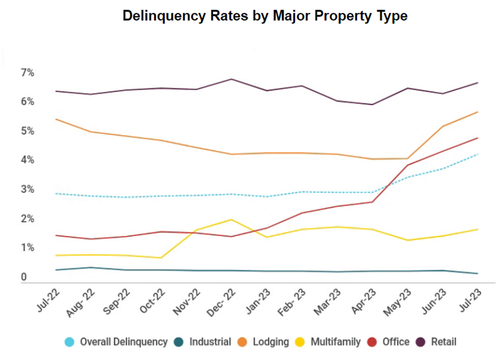

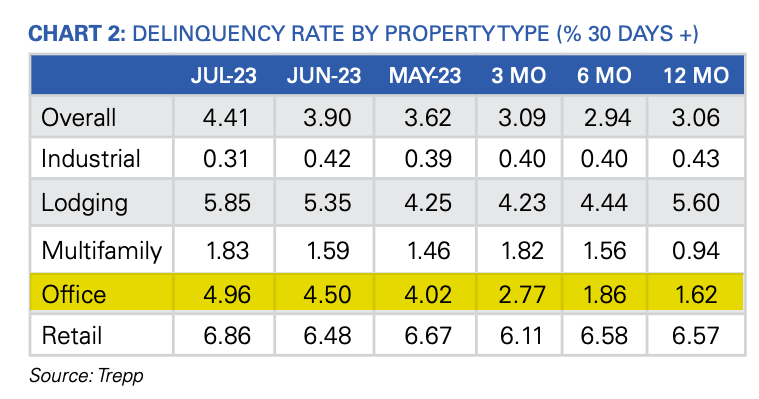

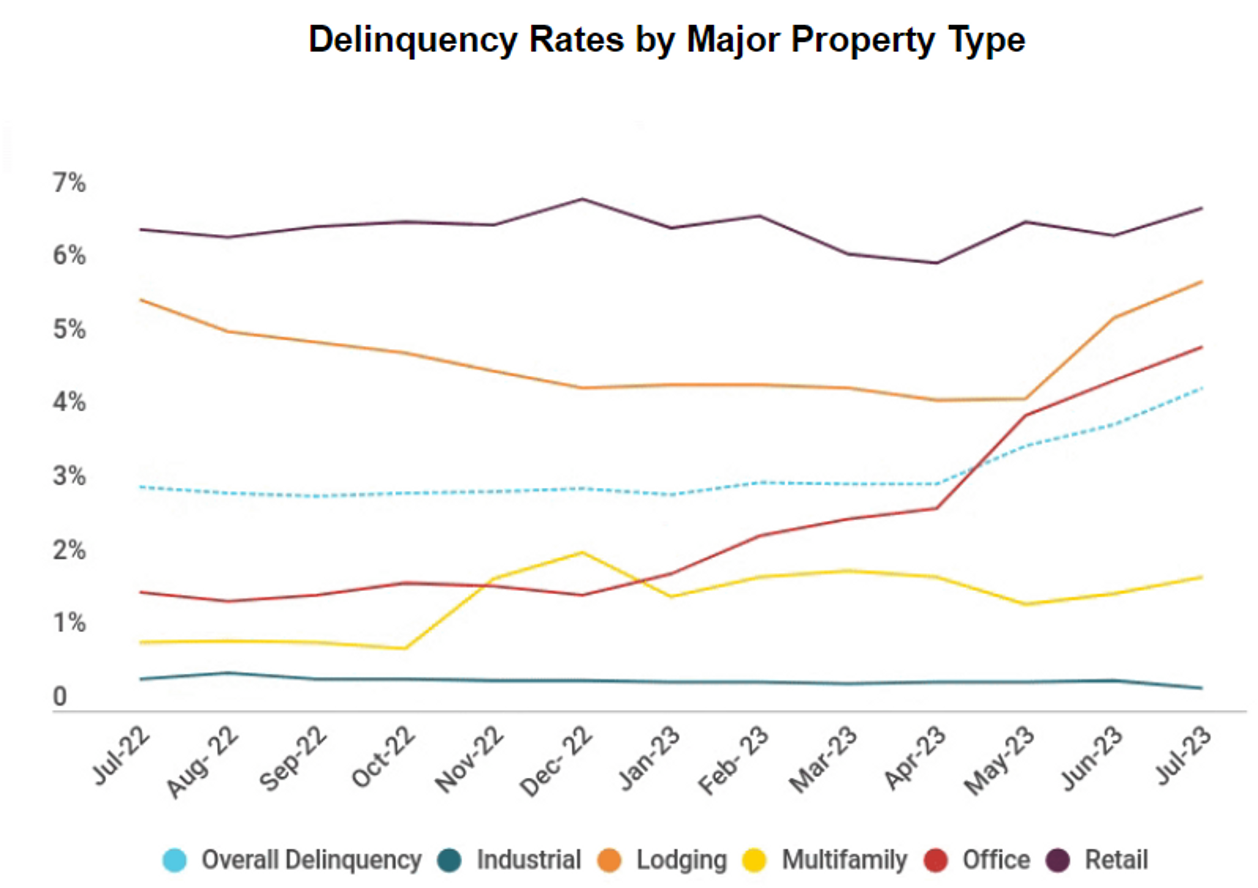

The latest data from Trepp, which tracks commercial mortgage-backed securities (CMBS) securities market data, shows the delinquency rate of commercial property loans packaged up by Wall Street jumped again in July, with four of the five major property segments posting increases.

“While the rest of the US economy has seen relief in terms of higher equity prices, better-than-expected corporate earnings, and falling inflation numbers, the commercial real estate (CRE) market continues to be left behind,” Trepp wrote in the report.

Trepp data found the delinquency rate rose 51 basis points to 4.41% last month — the highest level since December 2021. Office delinquencies increased by 46 basis points to 4.96% — up more than 350 basis points since the end of 2022. The deterioration in the office segment is intensifying at an alarmingly rapid pace.

A broad overview of the US CMBS market shows the delinquency rate increased to 4.41%, a 51bps rise compared to the previous month, but still significantly lower than the 10.34% rate recorded in July 2012. The rate peaked at 10.32% in June 2020 during the government-forced Covid lockdowns.

Here are more highlights from the report:

Year over year, the overall US CMBS delinquency rate is up 135 basis points.

Year to date, the rate is up 137 basis points.

The percentage of loans that are seriously delinquent (60+ days delinquent, in foreclosure, REO, or non-performing balloons) is now 3.92%, up 20 basis points for the month.

If defeased loans were taken out of the equation, the overall headline delinquency rate would be 4.64%, up 51 basis points from June.

One year ago, the US CMBS delinquency rate was 3.06%.

Six months ago, the US CMBS delinquency rate was 2.94%.

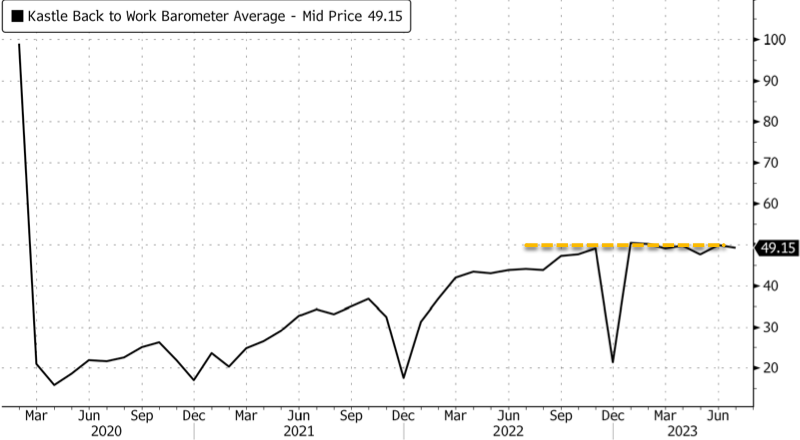

To better understand what might come next for the CRE market, Kiran Raichura, Capital Economics’ deputy chief property economist, recently warned in a note to clients that the office segment might experience a 35% plunge in values by the second half 2025 and “is unlikely to be recovered even by 2040.”

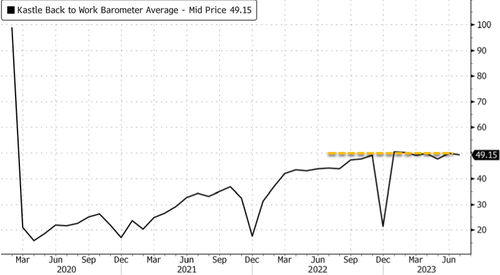

According to swipe data from Kastle Systems, the US office occupancy rate is less than 50%. The figure has plateaued since September, indicating a new reality of remote work.

One major hurdle for CRE space is that “more than 50% of the $2.9 trillion in commercial mortgages will need to be renegotiated in the next 24 months when new lending rates are likely to be up by 350 to 450 basis points,” Lisa Shalett, chief investment officer for Morgan Stanley Wealth Management, wrote in a note to clients.

Shalett expects a “peak-to-trough CRE price decline of as much as 40%, worse than in the Great Financial Crisis.”

Bank of America analysts expect challenges in the CRE space but noted, “They are manageable and do not represent a systemic risk to the US economy.”

Meanwhile, analysts at UBS warned:

“About $1.3 billion of office mortgage loans are currently slated to mature over the next three years.

“It’s possible that some of these loans will need to be restructured, but the scope of the issue pales in comparison to the more than $2 trillion of bank equity capital. Office exposure for banks represents less than 5% of total loans and just 1.9% on average for large banks.”

We’ve already seen major building owners returning their office towers and malls to lenders in California (here & here) and elsewhere (here). This will result in an uptick in CMBS delinquencies moving forward.

Higher funding costs, potential regulatory capital weaknesses and rising risks tied to commercial real estate are among strains prompting the review, Moody’s said late Monday.

“Collectively, these three developments have lowered the credit profile of a number of US banks, though not all banks equally,” the rating company said.

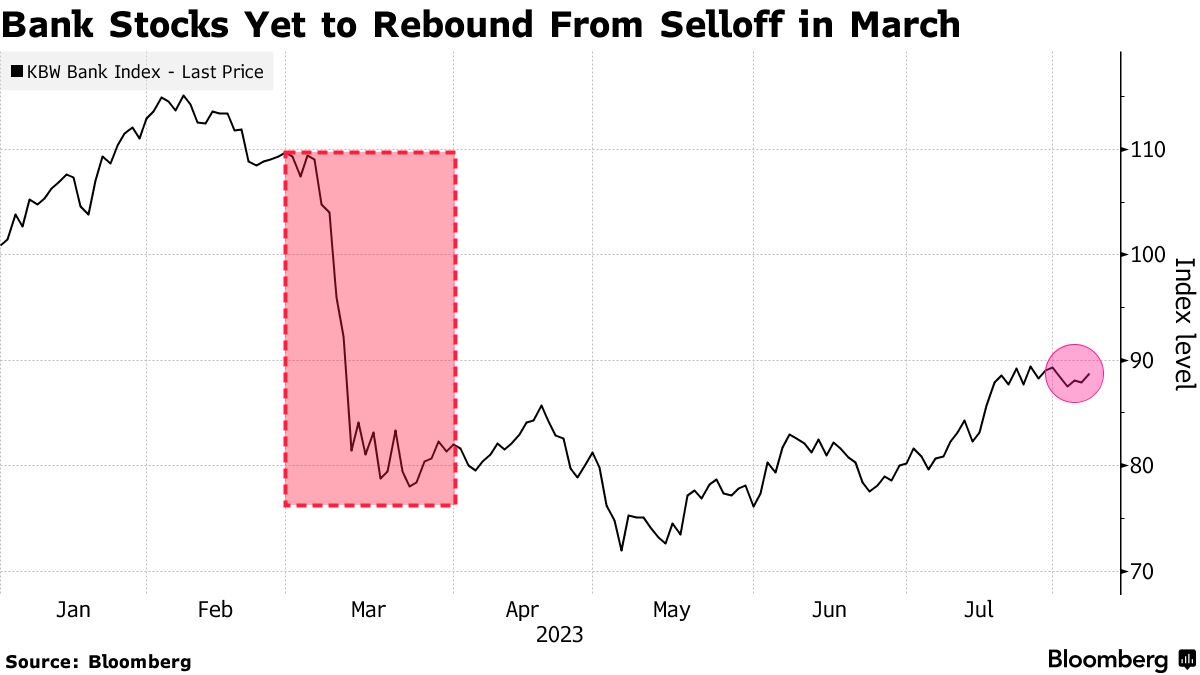

Moody’s Sees Problems Ahead for US Banks

Rating company issues raft of downgrades, outlook

Source: Moody’s

Shares declined for firms that had their ratings cut, including M&T Bank Corp., down 3.2%, and Webster Financial Corp., which lost 1.3%. Moody’s also adopted a “negative” outlook for 11 lenders, including PNC Financial Services Group, Capital One Financial Corp. and Citizens Financial Group Inc. Among those, PNC was down 2.2% and Capital One lost 2.4%.

Investors, rattled by the collapse of regional banks in California and New York this year, have been watching closely for signs of stress in the industry as rising interest rates force firms to pay more for deposits and bump up the cost of funding from alternative sources. At the same time, those higher rates are eroding the value of banks’ assets and making it harder for commercial real estate borrowers to refinance their debts, potentially weakening lenders’ balance sheets.

“Rising funding costs and declining income metrics will erode profitability, the first buffer against losses,” Moody’s wrote in a separate note explaining the moves. “Asset risk is rising, in particular for small and midsize banks with large CRE exposures.”

Some banks have curbed loan growth, which preserves capital but also slows the shift in their loan mix toward higher-yielding assets, Moody’s said.

Banks that depend on more concentrated or higher levels of uninsured deposits are more exposed to these pressures, especially banks with high levels of fixed-rate securities and loans.

Deposits are declining as The Fed hikes rates.

So, Bidenomics reminds me of the film “Rollerball” where big corporations run the government and run a game akin to Rome’s gladiator fights.

“It is with profound disappointment that Yellow announces that it is closing after nearly 100 years in business,” said Yellow CEO Darren Hawkins in a statement Sunday.

Hawkins continued, “Today, it is not common for someone to work at one company for 20, 30, or even 40 years, yet many at Yellow did. For generations, Yellow provided hundreds of thousands of Americans with solid, good-paying jobs and fulfilling careers.”

Yellow’s bankruptcy marks the largest filing in US trucking history. The firm was responsible for roughly 15% of major corporations’ less than truckload. It has struggled with a sizeable debt load and changing consumer habits in a post-Covid environment. Yellow has $1 billion in debt due in 2024 alone and has struggled to find common ground with the Teamsters Union.

Hawkins blamed the union for the company’s failure:

“We faced nine months of union intransigence, bullying and deliberately destructive tactics.”

Yellow asked the Delaware court for permission to make payments, including employee wages and benefits, taxes, and certain vendors essential to its businesses.

Much of Yellow’s business halted weeks ago when it stopped making pickups. It axed most non-union employees and closed its yards at the end of July.

Stifel research director Bruce Chan said the demise of Yellow has been “two decades in the making,” blaming poor management and strategic decisions from the early 2000s.

For the overall trucking industry, Amit Mehrotra with Deutsche Bank said the collapse of Yellow is “clearly very positive for the companies that remain open for business.” He listed Old Dominion, Saia, CSX, and FedEx among other top picks in the industry.

Yellow shares trading in New York plunged more than 26% on the news. This followed a 781% surge from about 50 cents on July 27 to a high of $4.34 last Thursday.

Bidenomics = missing free markets replaced by the massive Federal foot of idiotic policies.

Yes, Bidenomics is an FDR-type massive expansion of government into the private sectors requiring massive Federal spending … and inflation. Except that it beenfits anything BIG and powerful to the detriment of the small and weak.

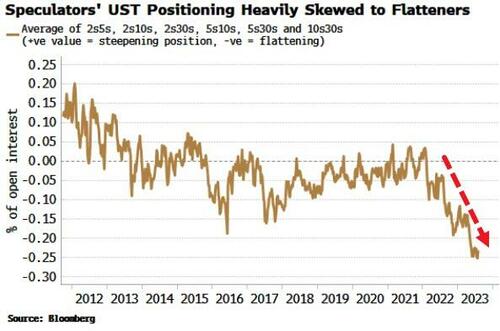

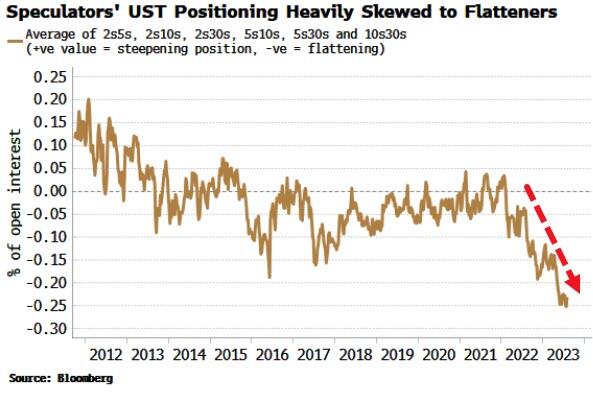

(Bloomberg) Friday’s jobs data sparked a relief rally in bonds and a flatter yield curve, but the pain trade is still for higher yields and a steeper curve – the lesser-spotted bear steepener – with this week’s CPI a potential catalyst.

Last week was a turbulent one for bonds, but the continued softening in payrolls data served to remind the market that supply and fiscal-profligacy fears have to be counter-balanced with an economy that’s in its late-cycle stages.

After the data, 10-year yields took the elevator back down to sub-4.05% after briefly going above 4.20%. They have since clambered back to 4.12%, but their next cue is likely to come from Thursday’s CPI report. Headline is expected to nudge back up to 3.3% (from 3% last month), mainly due to base effects, and core is expected to hold steady at 4.8%.

Still, stronger-than-expected data probably means higher yields in a market more acutely alert to inflation (and therefore supply) risks. As with last week, term premium would likely drive the move, meaning a curve steepening. After relentlessly flattening for the last two years, the pain trade is for a steeper curve. Implicit positioning of speculators from the COT report shows there is a heavy skew to a flatter curve.

The negative carry for most flatteners remains punitive (for 2s10s USTs it’s ~83bps over a year), but the large upside potential from supply/inflation worries and the covering of positions begins to make that look less insurmountable.

Finally, the Bundesbank’s decision to stop paying interest on domestic government deposits – which initially pushed short-term German bonds higher this morning – highlights the broader issue of central banks paying interest on reserves when they are superabundant.

In the days of QE and 0% interest rates, the ECB and Fed at al. remitted money to their treasuries from the income on their bond portfolios.

But now that is reversed as bond income is dwarfed by the cost of paying interest on trillions of bank reserves. Take the Fed, whose debt to the Treasury is now accruing at over $2 billion each week.

This is something that will become more politically contentious, especially as economies continue to slow and cost-of-living pressures bite further.

Bidenomics. The takeover of the US economy by BIG corporations, BIG labor unions, BIG tech, BIG pharma, BIG defense, BIG healthcare, BIG media, BIG banks, BIG tech, BIG … Well, anyting that is BIG and powerful that can buy influence in Congress and the Administration. Except BIG energy which lost out to BIG Progressive DC thinktanks.

Leading to BIG inflation!

But I feel good! Even though inflation expectations are soaring again as gasoline soars again.

If you believe the recovery talk (from the reckless Covid economic and school shutdowns of 2020), all is well in the (economic) garden. For example, M2 Money Velocity (GDP/M2), is almost back to where it was just prior to the 2020 Covid outbreak and resulting government-caused recession. M2 Velocity was 1.425 in Q4 2019 and was 1.289 for Q2 2023. But ever since The Federal Reserve became hyper intervention in the economy (let’s just start with Bernanke’s massive intervention in late 2008 (red line) and the Fed balance sheet expansion), and it was increased dramatically during the Covid shutdown. And is STILL above $8 trillion!

Before Bernanke and the financial crisis of 2008-2009, M2 Money Velocity was above 2.0. But it has been below 2.0 ever since The Fed’s intervention in 2008.

Granholm called China National Energy Administration Chairman Zhang Jianhua, a longstanding senior member of the Chinese Communist Party, for a half-hour one-on-one conversation on Nov. 21, 2021. Granholm’s calendar also shows an earlier phone call had been scheduled with Jianhua for Nov. 19 but a rep for the former Michigan governor said the first call never took place. Then, on Nov. 23, 2021, the White House announced a release of 50 million barrels of oil from the SPR, the largest release of its kind in U.S. history at the time.

According to Fox News, Granholm’s previously-undisclosed talks with China National Energy Administration Chairman Zhang Jianhua — revealed in internal Energy Department calendars obtained by Americans for Public Trust (APT) and shared with Fox News Digital — reveal that the Biden administration likely discussed its plans to release oil from the SPR with China before its public announcement in the US: yes, China’s Communist Party learned what Biden would be doing before the US did.

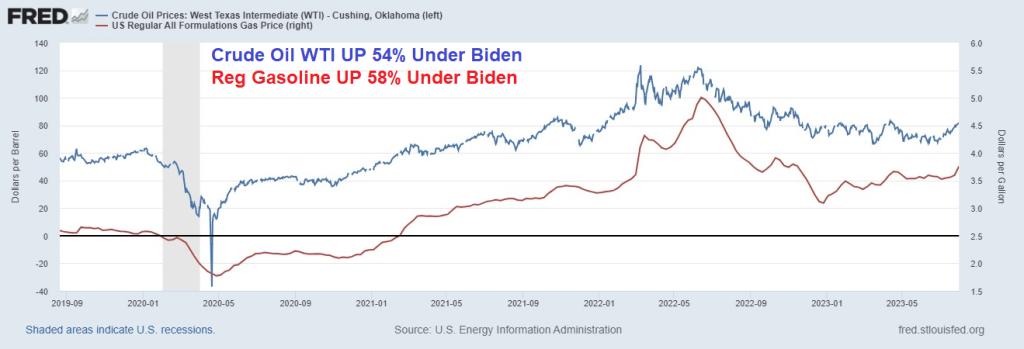

While Biden/Granholm are merrily draining the Strategic Petroleum Reserve, we see that West Texas Intermediate Crude Oil (Cushing) prices are up 54% under Biden and regular gasoline prices are up 58%.

All is sort of well in the garden because The Federal Reserve still has its massive interventionist foot on the gas pedal. Yet, America is on an economic suicide course with its green energy hype.

Frankly, Biden talks like Chance The Gardener from the film “Being There.” Except that Chance the Gardener is a nice person and Biden is reputed to have been the nastiest member of the US Senate. Not to mention the stupidest member of the US Senate. Although I don’t think Chance the Gardener would have taken millions in bribes from foreign countries like China and Ukraine.

Biden The Gardener should be Biden’s re-election slogan! Of course, Chance the Gardener could walk much better than Biden with his dementia shuffle. And Chance was a great gardener, all Biden knows how to do is sell the “Biden Brand” of political influece peddling to foreign countries.

“One of the most cowardly things ordinarily people do, Is to shut their eyes to facts.” – C.S. Lewis

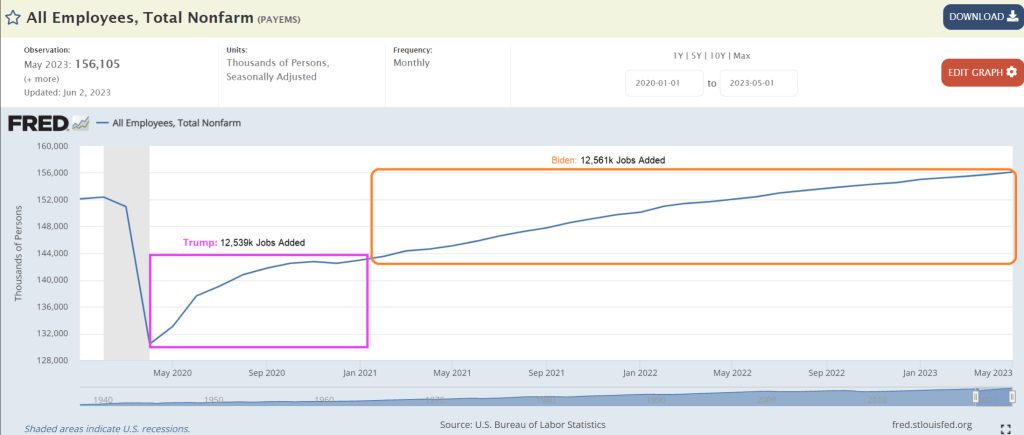

Okay, we know Biden lies constantly and misrepresents facts (hey, he is a politician like Adam Schiff (D-CA). But this graphic praising Bidenomics with Biden having created the most jobs (average per month) since Carter (notice they left out Democrat darling Jimmy Carter!!!). In this absurd graphic, Biden wins by “creating” over 400k jobs per month while Trump lost jobs per month. Riveting … except that it is completely misleading.

Actually, the US economy added 12.53 million jobs after April 2020 (Trump) while Bidenomics created took 2 1/2 years to add 12.56 million jobs. So, Biden took over twice as long to create jobs after Covid than it did under Trump. Simply opening the economy and schools produced that magical claim by Biden. And the National Teacher’s Union and Randi Weingarten worked with Fauci to orchestrate shutting down schools. Blaming Trump for local governments shutting down the economy is pure bunk.

12.53 millions jobs added / 8 months = 1.56 million jobs average per month. Biden? 12.56 million jobs added / 30 months = .43 million jobs average per month. So, Trump averaged more than 3x the job growth post-Covid than Biden.

Here is the “glories of Bidenomics” from the White House. As Biden likes to say, pure malarkey!

I wonder if the Democrat Party is a rebirth of New York City’s Tammany Hall corrupt political movement of the 1800s? Is Biden Boss Tweed? Or is Obama Boss Tweed with Biden as his nasty, dimwitted henchman?

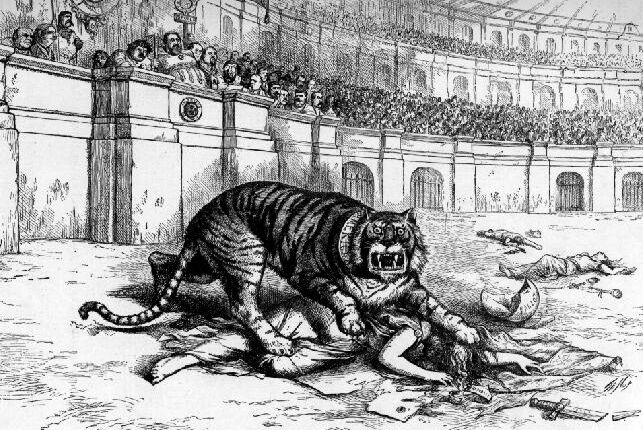

In 1871, Thomas Nast denounces Tammany as a ferocious tiger killing democracy. The image of a tiger was often used to represent the Tammany Hall political movement. Sounds an awful lot like today’s Democrat Party.

Josef Stalin of the old Soviet Union used to be called County Joe. But Biden has so many possible nicknames: Corrupt Joe, Pay-for-play Joe, Sleazy Joe, Bully Joe, etc. How about Green Joe?

Green Joe (or the Nasty Green Giant?) along with his energy goon Jennifer Granholm, have drained the strategic petroleum reserve by 46% while gasoline prices have soared 60% under Bidenomics.

Gasoline prices have rise over 6.5% just since 7/23/2023.

Trump wants to drain the swamp, Biden/Granholm want to drain the strategic petroleum reserve so we can’t go back to fossil fuels. Biden and Granholm as Fossil Fools

Energy Secretary Jennifer “The Evil Pixie’ Granholm demostrating how she will refill the strategic petroleum reserve. Which she never will, of course.

US average hourly earnings continued at 4.4% year-over-year (YoY). However, the last core inflation reading was 4.8% YoY, so real wages continue to decline.

Rent CPI for June was 7.8% YoY.

Here is the rest of the story.

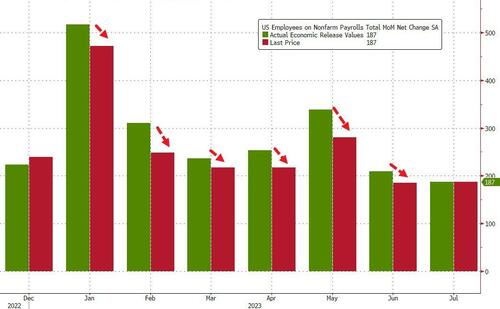

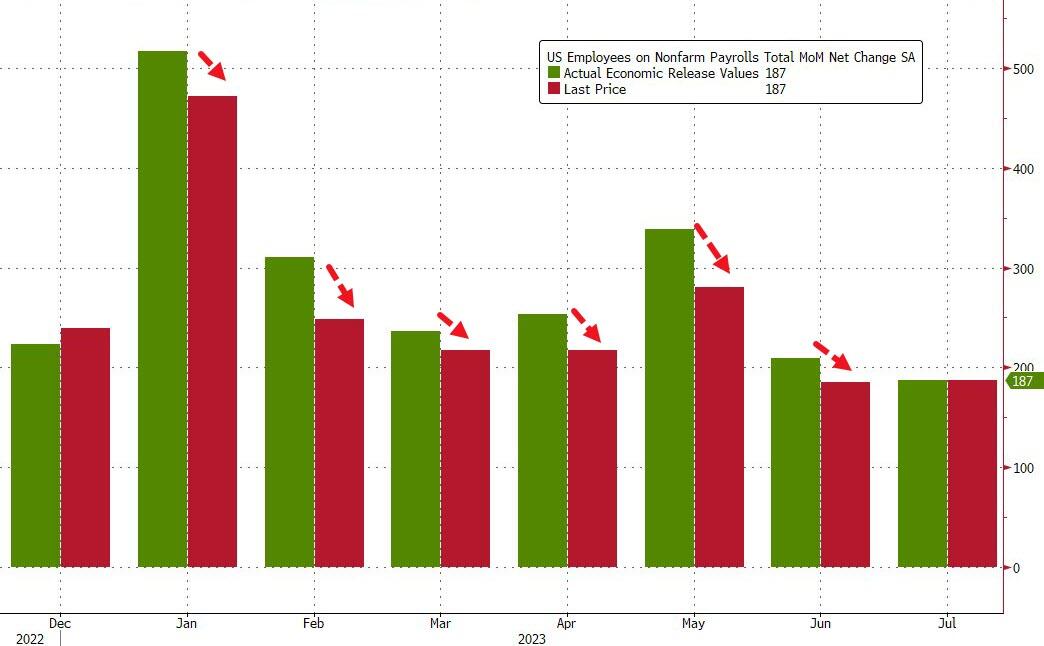

In keeping in with Biden admin’s penchant of constantly fabricating data, both May and June numbers were revised sharply lower of course:

May revised down by 25,000, from +306,000 to +281,000

June was revised down by 24,000, from +209,000 to +185,000.

To show just how ridiculous the data manipulation is, consider this chart – every monthly payrolls report in 2023 has been revised lower.

And on the disappointing jobs report and massive revisions of past data (the REAL inflation plaguing the nation is The Federal goverment lying about data), the US Treasury 2 year yield dropped like Biden on a flight of stairs.

Here are the faces of Washington DC. Lies, corruption, government for sale to highest bidder, cynacism, oppression, fear mongering, etc. This is Biden’s legacy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.