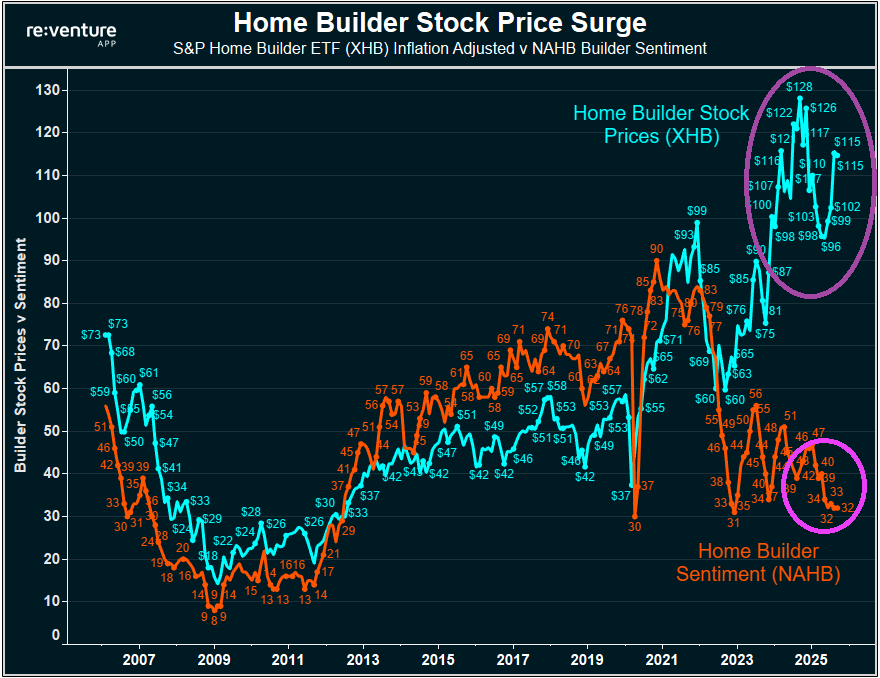

Home builder stock prices have surged, while home builder sentiment has plunged.

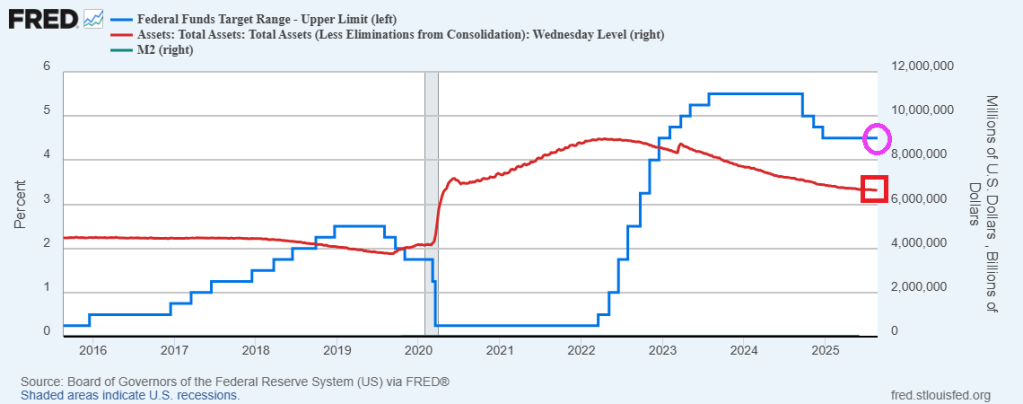

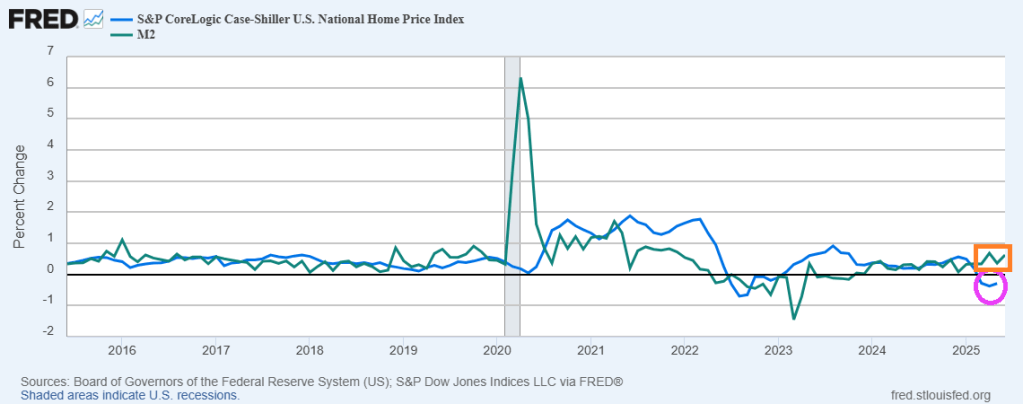

Of course, The Fed’s endless money printing isn’t helping the supply side of home building.

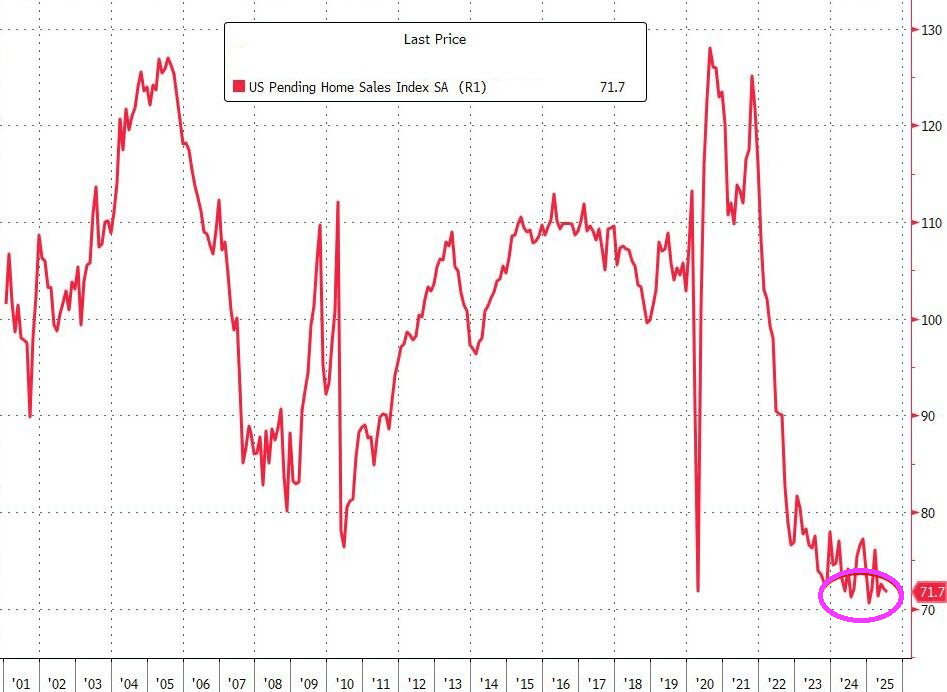

To make matters worse, pending home sales remain in the doldrums.

Federal Reserve Board member Lisa Cook is an embarrasment for committing mortgage fraud, then refusing to step down. And now she has filed a lawsuit against the Trump Administration for wrongful termination. Typical of an Obama appointee!

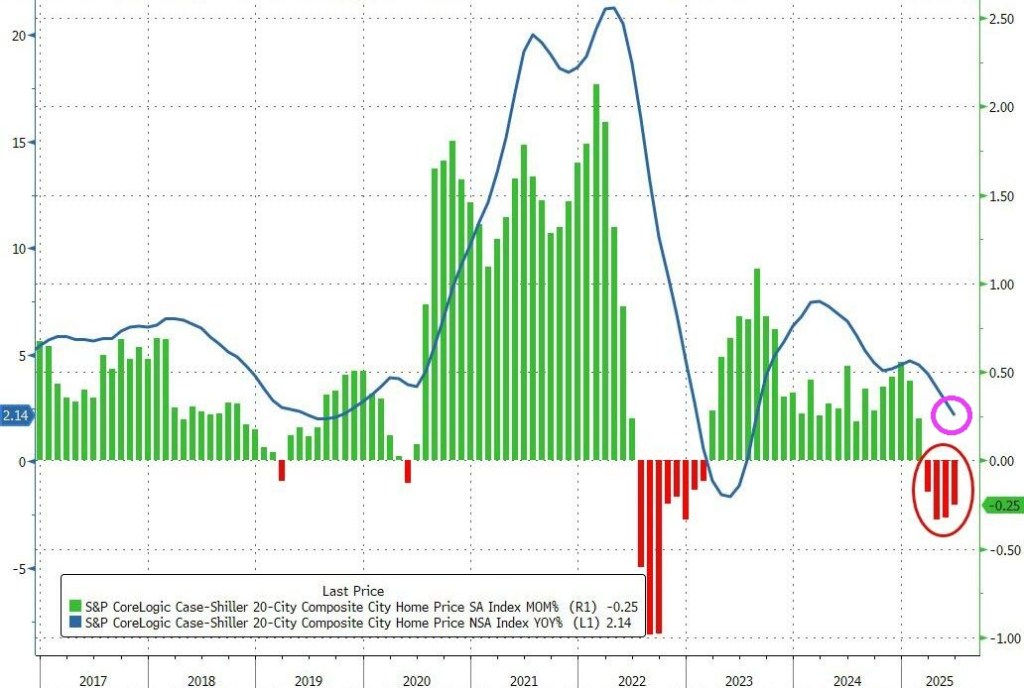

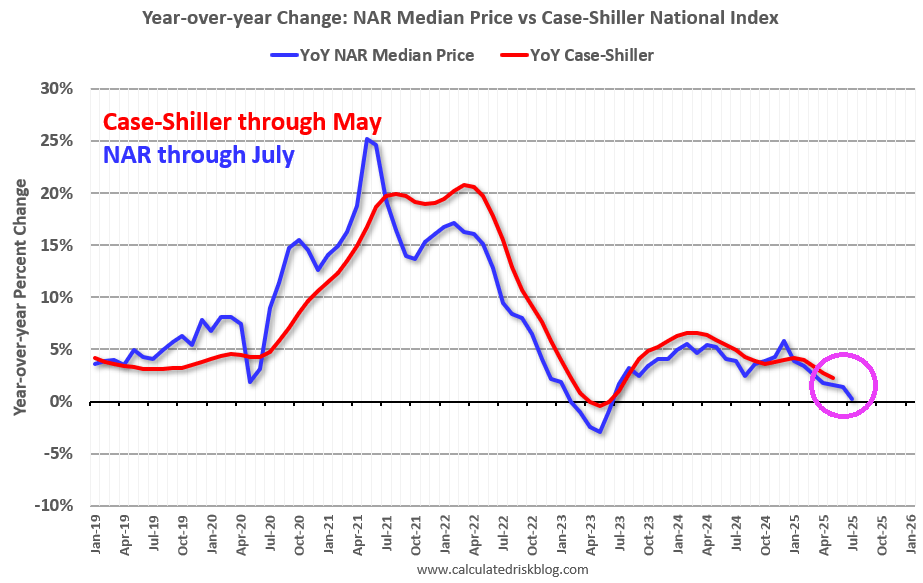

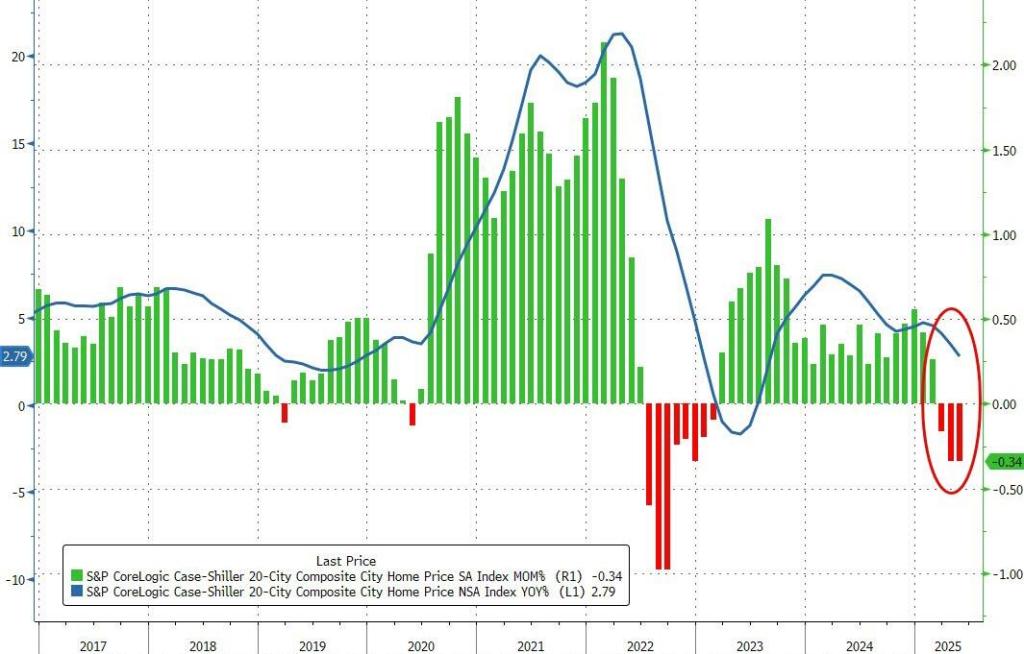

Home prices in America’s 20 largest cities fell for the 4th straight month in June (the latest data available from S&P CoreLogic’s Case-Shiller data released this morning).

The -0.25% MoM drop was larger than expected and dragged the YoY price growth down to +2.15% – the weakest since July 2023.

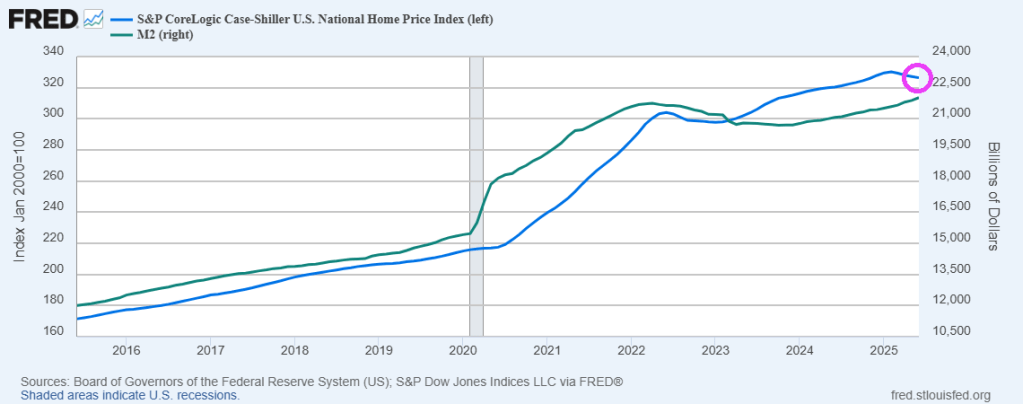

Meanwhile The Federal Reserve keeps on printing money, helping to drive up home prices.

,Metro level? New York and Chicago lead, with Phoenix, Miami, Denver, San Diego, Dallas, San Francisco and Tampa all experiencing price declines.

On a side note, Chicago is even more unaffordable than last year. So much for Mayor Brandon Johnson saying there would be no crime if everyone could afford housing (one of the stupidest comments I have ever heard).

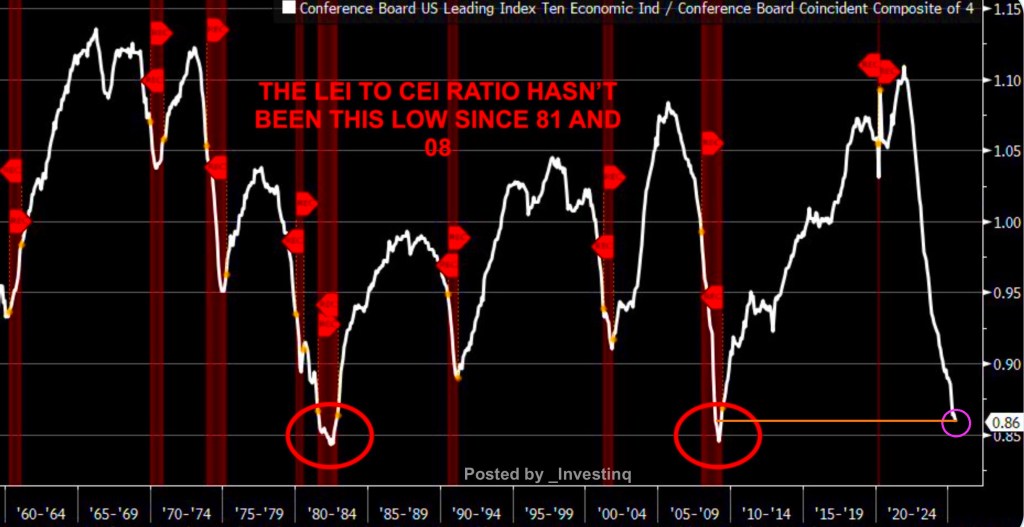

The Fed will have to whip it good with rate cuts if the recession warnings are an indicator of what lies ahead for the US economy.

The ratio of The Conference Board’s Leading Economic Indicators (LEI) vs. The Conference Board’s Coincident Economic Index (CEI) ratio hasn’t been this low since 2008.

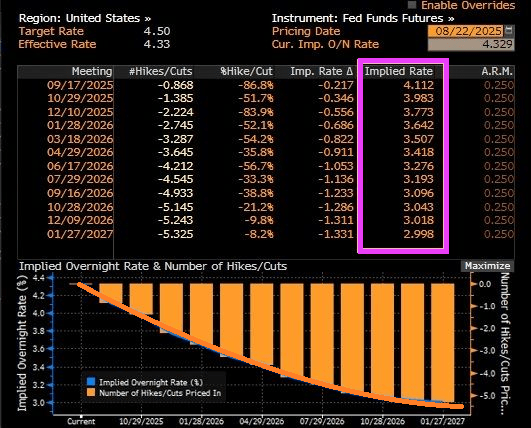

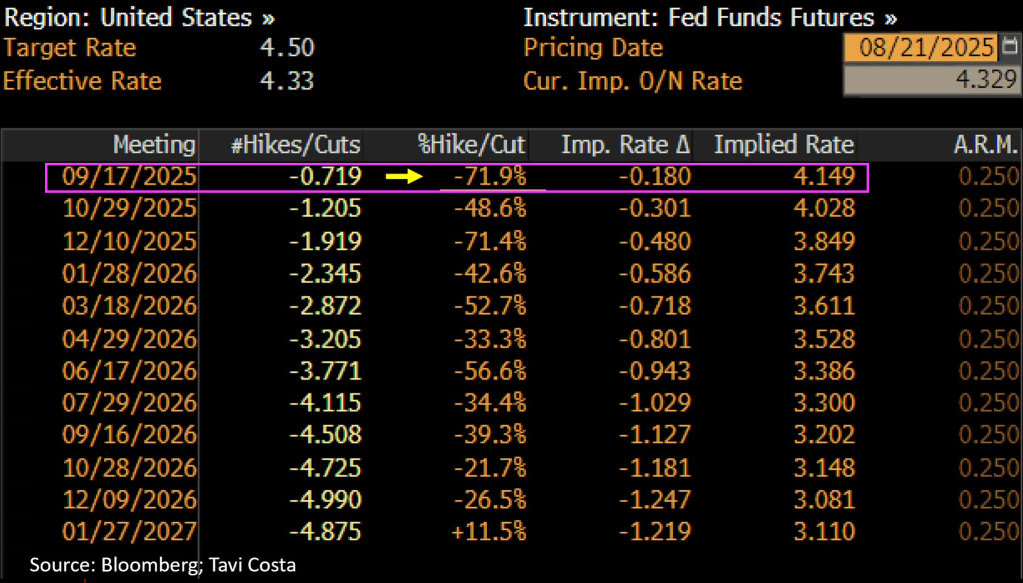

Fed Funds Futures are signalling rate cuts at the September 17th FOMC meeting and December 10th meetings.

Month-over-month sales increased in the Northeast, South, and West, and fell in the Midwest. Year-over-year, sales rose in the South, Northeast, and Midwest, and fell in the West.

• 2.0% increase in existing-home sales – seasonally adjusted annual rate of 4.01 million in July.

• Year-over-year: 0.8% increase in existing-home sales

Median existing-home price for all housing types, up 0.2% from one year ago ($421,400) – the 25th consecutive month of year-over-year price increases.

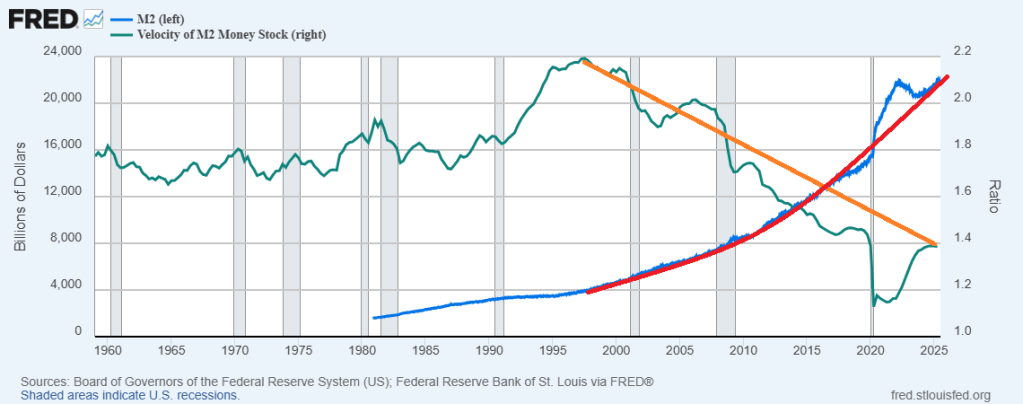

It will be hard to make housing more affordable as long as The Fed keeps printing money.

Powell et al cutting rates 25 basis points won’t really matter as long as they continue to print money. Unfortunately, M2 VELOCITY peaked under the Clinton Administration and has declined since despite frantic money printing.

What happended in 1995? Clinton’s National Homeownership Strategy that mandated HUD partners (GNMA, FHA, Fannie Mae, Freddie Mac, banks, etc.) to lower credit standards to encourage homeownership.

We need FHFA Director Bill Pulte to avoid doing what Democrats love (everything free or cheap).

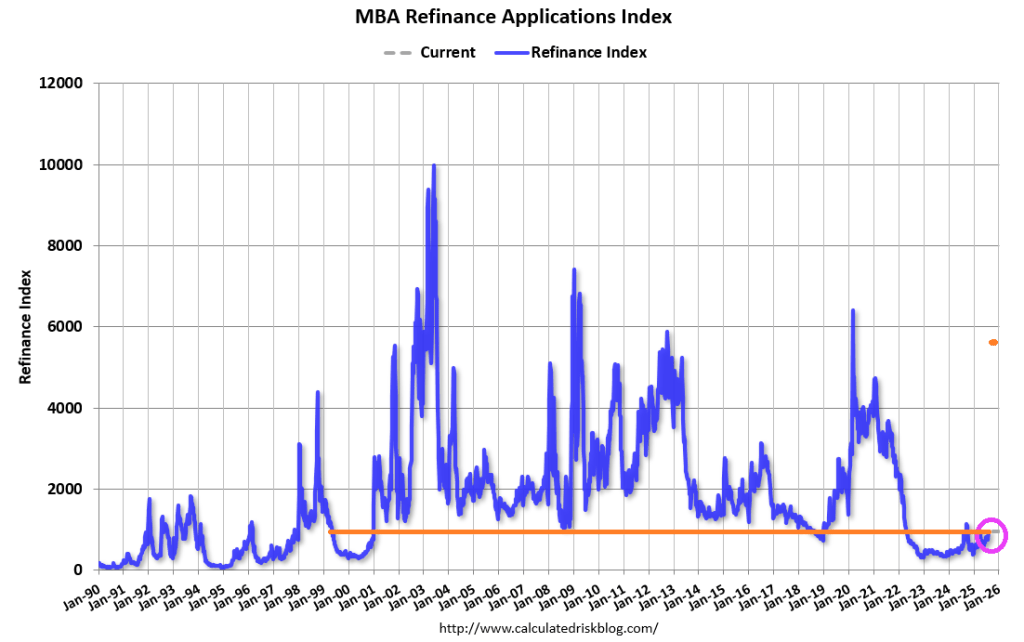

The Fed didn’t try, but mortgage rates fell and mortgage applications rose 10.9% week-over-week.

Mortgage applications increased 10.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 8, 2025.

The Market Composite Index, a measure of mortgage loan application volume, increased 10.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 10 percent compared with the previous week. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 17 percent higher than the same week one year ago.

The Refinance Index increased 23 percent from the previous week and was 8 percent higher than the same week one year ago.

The 30-year fixed mortgage rate declined to 6.67 percent last week,which spurred the strongest week for refinance activity since April. Borrowers responded favorably, as refinance applications increased 23 percent, driven mostly by conventional and VA applications. Refinances accounted for 46.5 percent of applications and as seen in other recent refinance bursts, the average loan size grew significantly to $366,400. Borrowers with larger loan sizes continue to be more sensitive to rate movements.

The latest inflation report continues to show no negative impact from tariffs. Core goods prices were up 0.2% in July. They are up just 1.1% over the past 12 months and are actually up a lesser 0.8% since President Trump began phasing in tariffs.

Business applications are booming under Trump’s economy.

While consumer prices are calm (2.7% YoY).

Shelter inflation is higher than the average price increase (3.7% YoY).

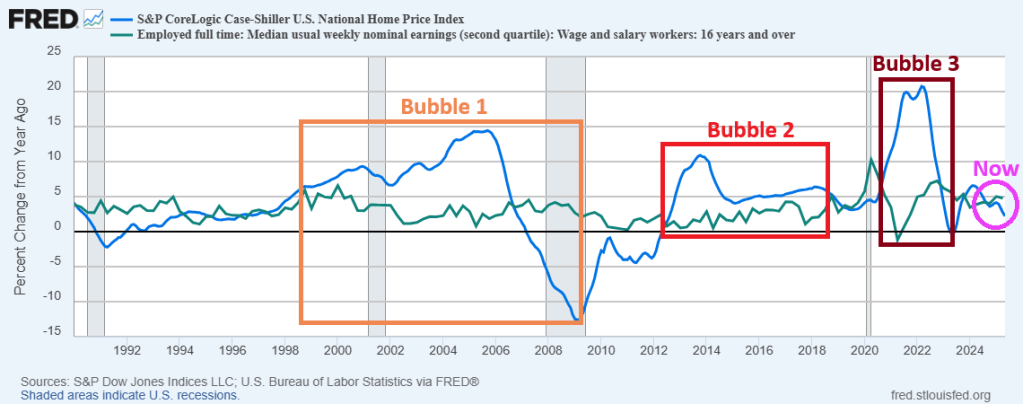

The US housing market is finally slowing down in terms of price growth. But this is after 3 Federal government-fueled house price bubbles.

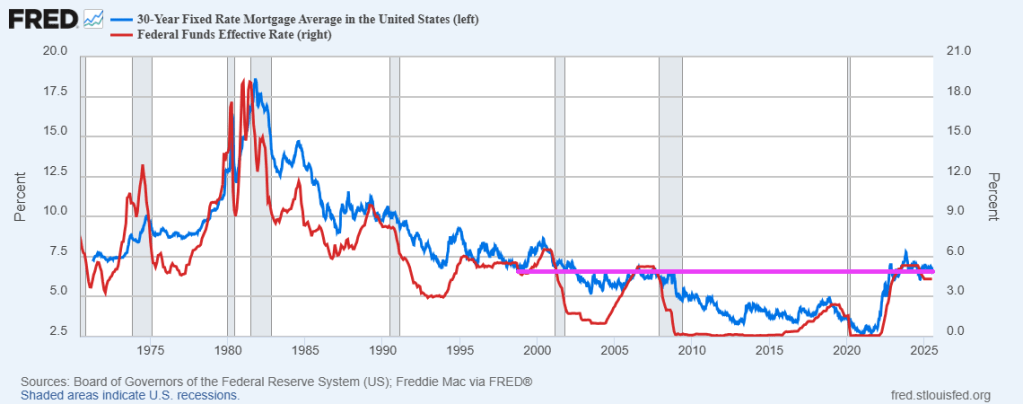

In addition to record-high housing prices, mortgage rates are higher than levels going back to 2006.

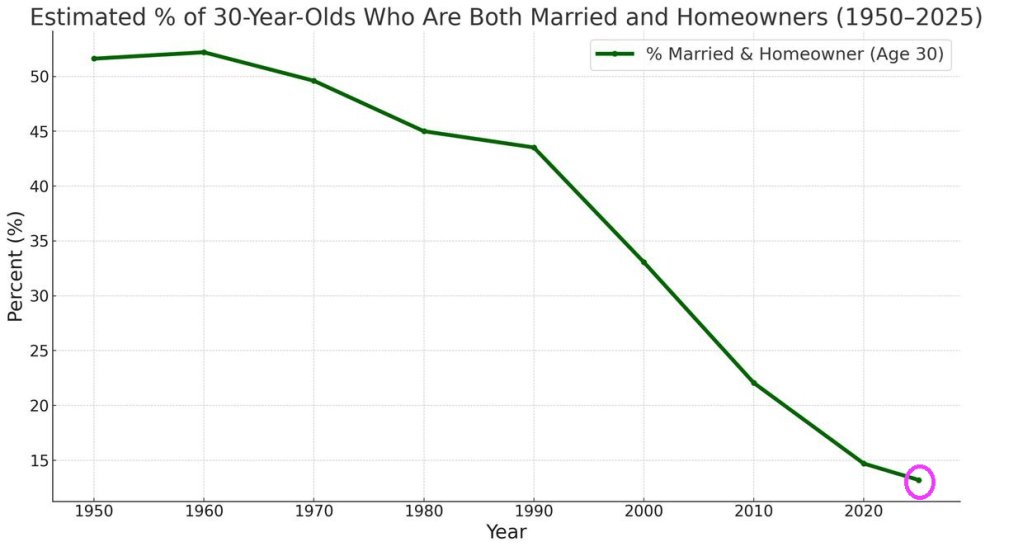

Throw in the “woke” movement, and we have a problem. The percentage of 30-year-olds who are both married and homeowners has plummeted to the lowest level since 1950.

Simply lowering interest rates won’t fix this problem. Much of the housing “crisis” is due to local and state level politicians and their restrictive housing policies. Like LA Mayor Karen “Venceremos Brigade” Bass allocating the burnt-down Pacific Palisades area on the Pacific Ocean to “affordable housing.”

US home prices fell for the 3rd straight month In May. The MoM decrease in the seasonally adjusted (SA) Case-Shiller National Index was at -0.29% (-3.5% annual rate).

You must be logged in to post a comment.