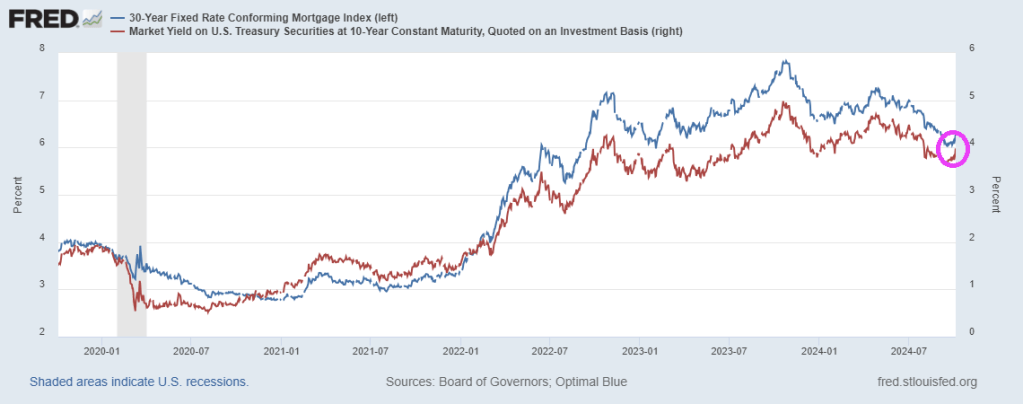

Mortgage rates are rising again with Friday’s surprising jobs report. But as it just a false election report. If Rasmussen is correct, mortgage rates should FALL again.

The Presidential and Vice Presidential debates thus far feature weak moderators asking lame questions. For example, there are still 97 hostages stll held by Hamas and what would the candidates do to get them released? (Hint: Trump/Vance would have sensible responses. Harris would just laugh and say she was raised in a middle class family and Walz would look like a deer in the headlights. Then we have national debt of $36 trillion, $271K per taxpayer.

But the hidden bomb that will never be discussed is unfunded liabilities (entitlements) such as Social Security and Medicare. Currently, unfunded liabilities are $219 TRILLION or $650K per citizen.

Of course, Biden/Harris have let the southern border wide open to criminals and uneducated Democrat voters who will voter for MORE entitlements.

So, when will the lame debate moderators ask HARD questions? And can Harris attempt to answer one hard question without laughing or falling back on lame “I was raised in a middle-class household.” etc.

It turns out that Powell’s “emergency” 50bps rate cut was – drumroll – another major policy mistake by the Fed. Or it is Presidential election interference by The Biden/Harris Administration giving Cacklin’ Kamala as talking point?

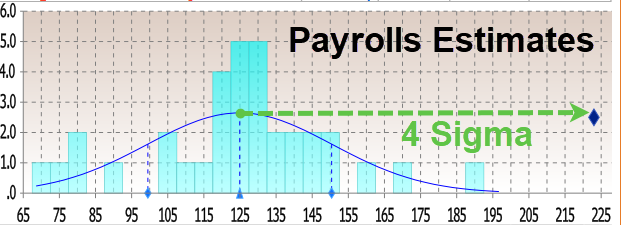

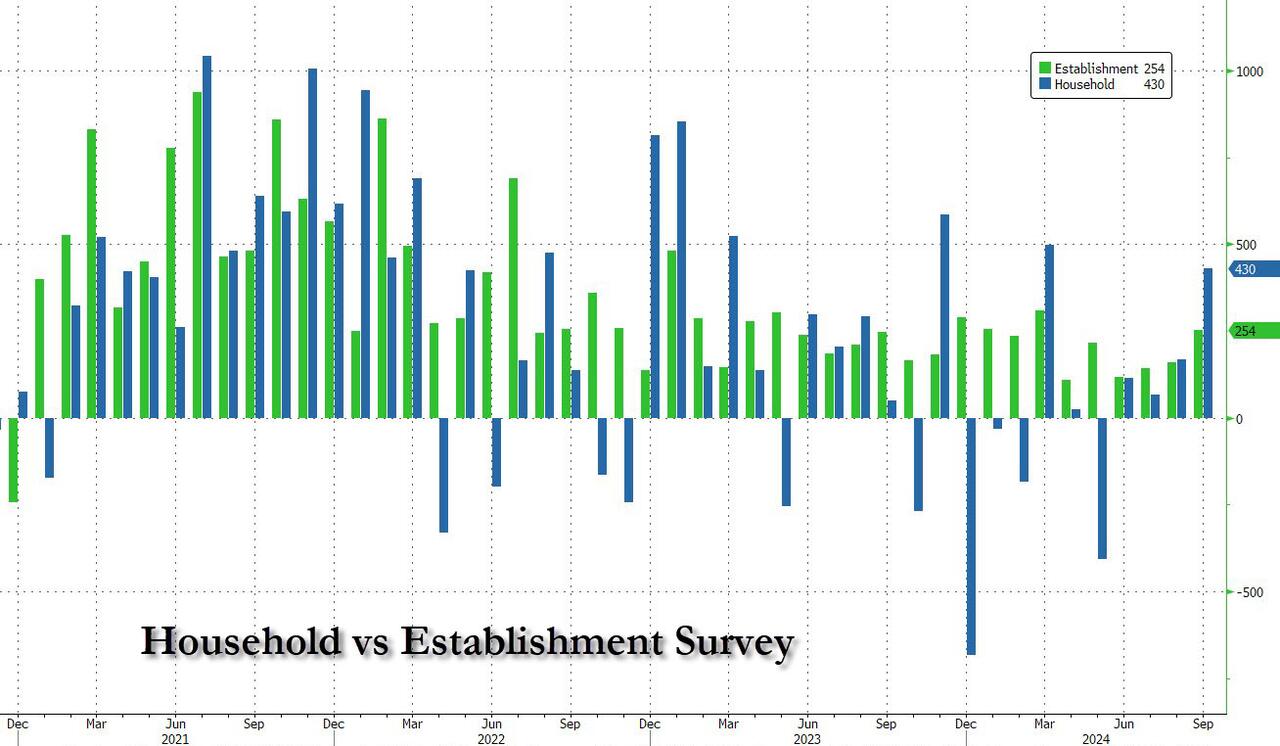

Moments ago, the BLS reported that at a time when prevailing consensus was for jobs to continue their recent downward slide sparked by the near-record annual jobs revision and several months of downbeat jobs reports, in September the US unexpectedly added a whopping 254K jobs, the biggest monthly increase since March…

There’s more: unlike previous months where we saw repeat downward job revisions, the BLS said that both prior months were revised up, to wit: the change in total nonfarm payroll employment for July was revised up by 55,000, from +89,000 to +144,000, and the change for August was revised up by 17,000, from +142,000 to +159,000. With these revisions, employment in July and August combined is 72,000 higher than previously reported.

Some context: as UBS notes, the moving six-month average on nonfarm payrolls is 167k. The estimate is that 150k is about consistent with a return of the economy to trend growth. Which means that inflation is about to come back with a vengeance, just as the Fed launches its easing cycle.

Remarkably, while payrolls jumped by the most in half a year, the number of employed people also surged, rising by a whopping 430K, also the biggest one-month jump since March.

It wasn’t just the payrolls, however, which came in far stronger than estimates: the unemployment rate also came in stronger than expected, and thanks to the jump in employed workers coupled with the decline in unemployed workers (from 7.115MM to 6.834MM), it dropped from 4.2% to 4.1% (and down from 4.3% two months ago which spared the entire recession panic).

Among the major worker groups, the unemployment rate for adult men (3.7 percent) decreased in September. The jobless rates for adult women (3.6 percent), teenagers (14.3 percent), Whites (3.6 percent), Blacks (5.7 percent), Asians (4.1 percent), and Hispanics (5.1 percent) showed little or no change over the month.

And here is the rub, because in a vacuum the super strong jobs numbers would have been fantastic, the only issue is that the September blowout comes as the Fed launches an easing cycle and as wages are once again rising as we have warned for the past 3 months. Indeed, in September, the average hourly earnings rose 0.4% sequentially, beating the estimate of 0.3%, while on an annual basis, wage growth was 4.0%, up from an upward revised 3.9% and beating the 3.8% estimate.

One note here: the average workweek for all employees edged down by 0.1 hour to 34.2 hours in September, which means the hourly earnings increase is not “pure” but rather a function of denominator adjustments. In manufacturing, the average workweek was unchanged at 40.0 hours, and overtime edged down by 0.1 hour to 2.9 hours. The average workweek for production and nonsupervisory employees on private nonfarm payrolls remained at 33.7 hours.

What sector had the biggest growth? UNPRODUCTIVE government workers! A record 785,000 government workers were added in September, pushing total govt workers also to a new record high.

The Biden/Harris Administration has given away billions of dollars to foreign nations (like Ukraine) and illegal immigrants so far this year,

– $24,400,000,000 to Ukraine.

– $11,300,000,000 to Israel.

– $1,950,000,000 to Ethiopia.

– $1,600,000,000 to Jordan.

– $1,400,000,000 to Egypt.

– $1,100,000,000 to Afghanistan.

– $1,100,000,000 to Somalia.

– $1,000,000,000 to Yemen.

– $987,000,000 to Congo.

– $896,000,000 to Syria.

– $9,000 per illegal immigrant that has entered the U.S.

And claim that FEMA has no money left for Hurricane Helene victims who have received only $750 per person. So I have plenty of reasons to have no trust or confidence in the Biden/Harris Mal-administration.

Maybe if Kamala Harris actually visited the Mexican border before yesterday, she wouldn’t have greenlighted an invasion of criminals into the US.

BREAKING: According to a new report from the Deputy Director of ICE, Joe Biden and Border Czar Kamala Harris allowed a SHOCKING number of criminals into America, including:

But Biden/Harris had help from their deep state partner, The Federal Reserve.

The purchasung power of the US dollar has fallen by a whopping -20% under Biden/Harris. No wonder Harris is afraid to talk to reporters about her plans.

The children in Congress went on a spending spree as a result of COVID resulting in record inflation.

The deep state’s financing arm, The Federal Reserve, certainly helped create inflation by ramping up M2 Money supply around Covid.

Of course, children in Congress and Harris/Walz will use ANY excuse to tax and spend (and borrow/spend). The most recent inflation report had CPI growng at 2.5% YoY resulting in a further decline of purchasing power of the US dollar of -2.5% YoY.

Harris/Walz fully intend to keep shoveling TRILLIONS into green energy transformation and supporting illegal immigrants.

Whenever the 10Y-2Y Treasury yield curve slope goes negative, it is following by positive slope … then recession. Like clockwork.

Following every recession since the 1970s, the 10Y-2Y Treasury yield curve slope has risen, then declined. This time around, the 10Y-2Y Treasury curve has remained negatively-slope long than usual suggesting a larger than normal snapback. Into a hard landing.

Democrats in particular love hard landings because that green lights them for massive wasteful spending.

More evidence of how destructive Biden/Harris economic policies have been.

The NAR data show existing home sales down 2.5 percent in August to a 3.86 million unit seasonally adjusted annual rate after a small upward revision to 3.96 million units in July.

US existing home sales fell in August to near 14-year lows. Pink box.

Meanwhile, pending home sales (red line) ARE at an all-time low.

Options imply a +/-1.1% move in S&P 500 for the 18-Sept FOMC meeting; this compares to an average of +/-1.2% move priced into SPX ahead of FOMC meetings since the beginning of 2022.

Arguably, this is an unusually important FOMC meeting due to the expected start of a cutting cycle.

On average, the S&P 500 has moved +/-1.3% during FOMC events since the beginning of 2022, coming above options implied moves.

In the July FOMC meeting the index moved +/-1.6% vs. an options implied expectations for a +/-1.1% move.

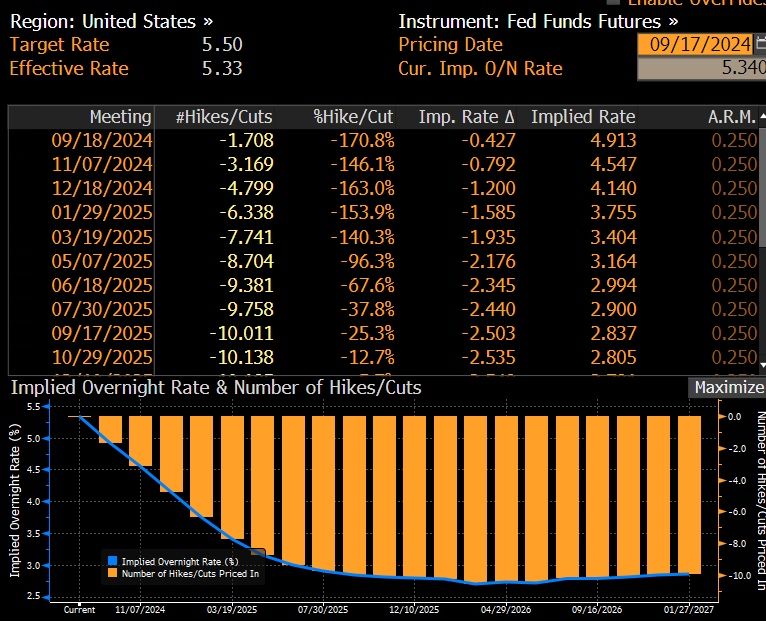

Goldman’s economists expect the September FOMC meeting to be the start of the Fed easing cycle with a 25bp rate cut followed by two consecutive 25bp rate cuts in November and December, and an eventual terminal rate of 3.25-3.5%.

They see differing asset performances around the start of the easing cycle depending on what motivated the Fed cuts.

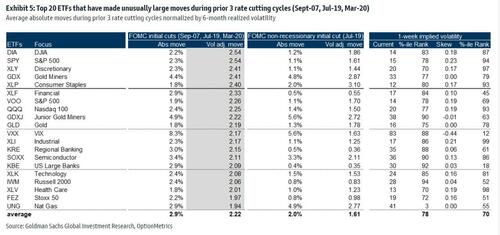

Goldman analyzed moves across stocks and ETFs during the first Fed rate cut in the prior 3 Fed easing cycles (18-Sep-2007, 31-Jul-2019 & 3-Mar-2020).

Rate cuts during the 2007 and 2020 easing cycles were associated with a recession while the 2019 cut was due to a growth scare.

In the tables below are the top 20 names that saw unusual moves during the prior 3 Fed easing cycles and for the 2019 cycle separately.

Financials and Tech were major movers during the beginning of the prior 3 Fed easing cycles while the 2019 cycle also saw unusual moves in Consumer Staples.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.