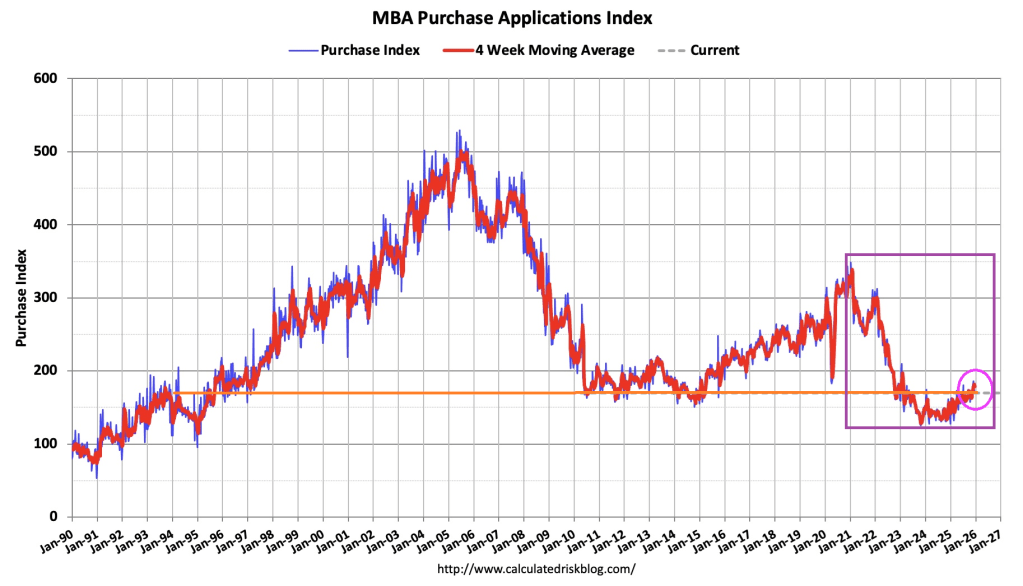

The Market Composite Index, a measure of mortgage loan application volume, decreased 5.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 6 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was 16 percent higher than the same week one year ago.

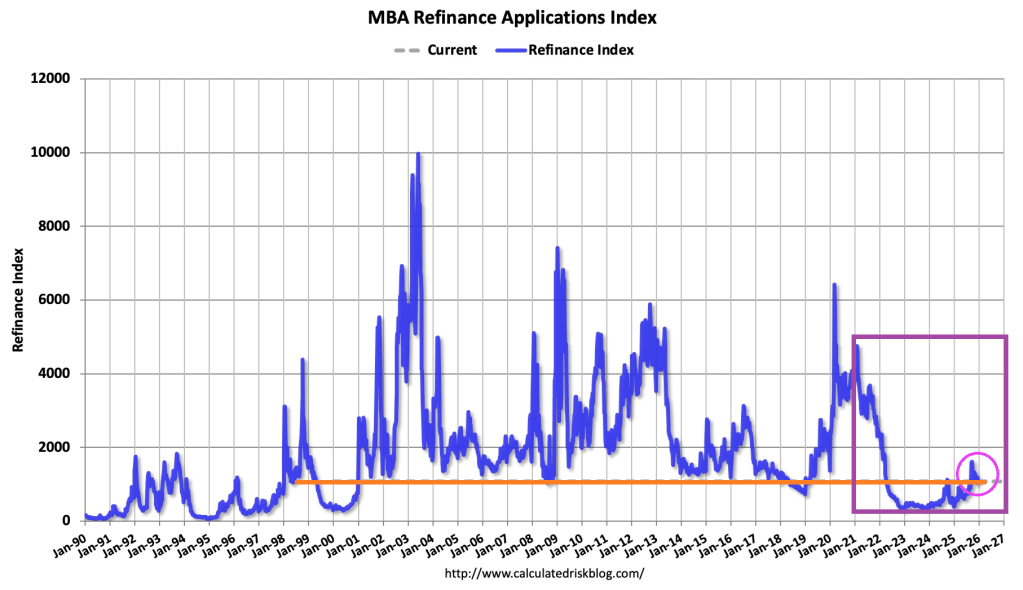

The Refinance Index decreased 6 percent from the previous week and was 110 percent higher than the same week one year ago.

Overall mortgage application volume fell last week, despite the slight decline in mortgage rates. I expect the trends of a softening job market, sticky inflation, elevated home inventories, and steady mortgage rates will persist into the new year.

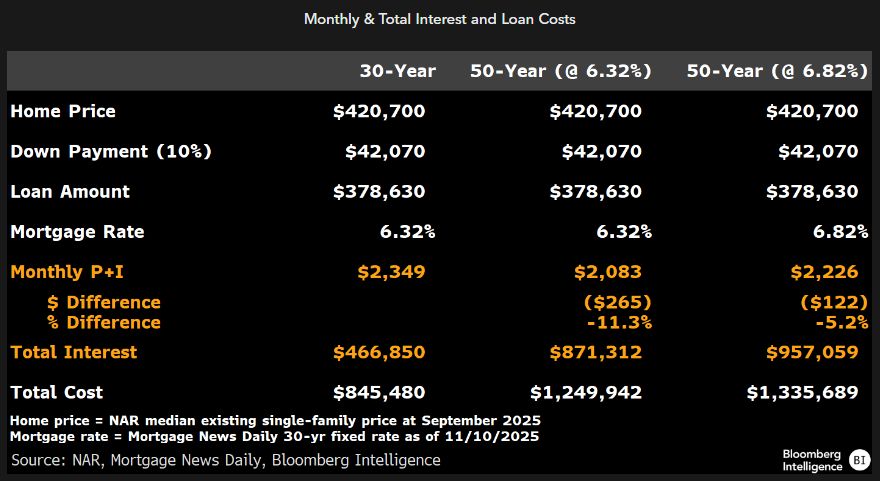

Every time the government tries to make housing more affordable, they make the problem worse. Some people should rent and not fall for the government’s latest folly, the 50-year mortgage.

True, the 50-year mortgage would lower the monthly payment by several hundred dollars (see the following example where the monthly payment falls from $2,349 to $2,083. Or from $2,349 to $2,226 if the most rate increases with the longer mortgage life. BUT total interest paid increases 87% if the 50-year rate remains the same and 105% if the rate rises.

Principal paydown slows to a crawl with a 50-year mortgage, leaving the lender (or mortgage holder) exposed to higher risk if home prices fall.

August data for the US housing market has been ‘mixed’ to say the least with a surge in new home sales (thanks to a massive rise in incentives from homebuilders) and a small decline (near multi-year lows), leaving this morning’s pending home sales data as the tie-breaker (with expectations of an ‘unch’ shift MoM).

It appears the drop in mortgage rates is driving some purchase activity as pending home sales soared 4.0% MoM in August – the most since March – dragging sales up 0.5% YoY.

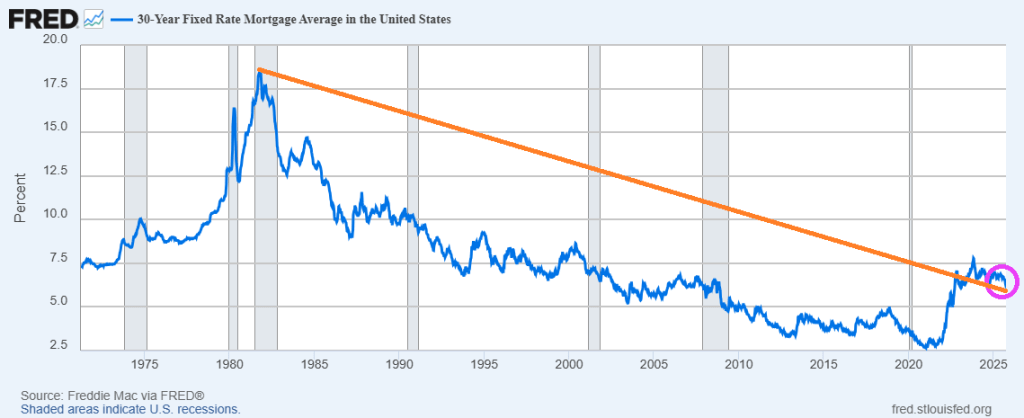

Mortgage rates are falling, helping existing home sales. Note that the 30-year mortgage rate peaked at 18.63% in 1981.

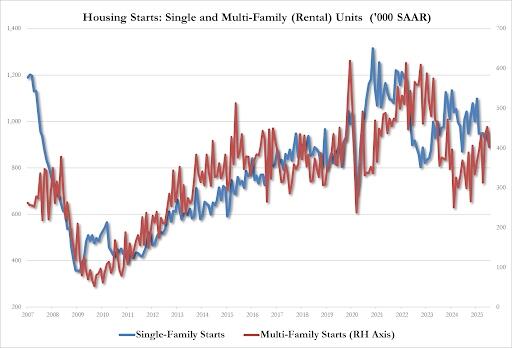

It will take a while to recover from Biden’s “Reign of Error.” According the US Census Bureau, housing starts are 6.0 percent below the August 2024 rate.

Housing starts:

Single-family 890K SAAR, down 7.0% from 957K in July and the lowest since July 2024

Multi-family 403K SAAR, down 11% from 453K in July and the lowest since May.

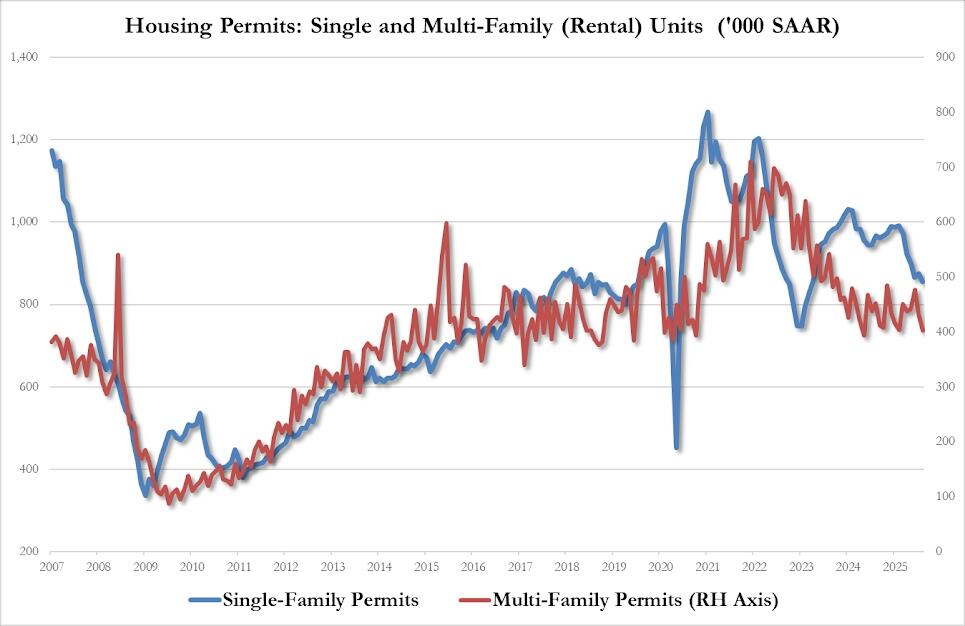

Housing permits?

Single-family 856K SAAR, down 2.2% from 875K in July and the lowest since March 2023

Multi-family 403K SAAR, down 6.7% from 432K in July and the lowest since May 2024

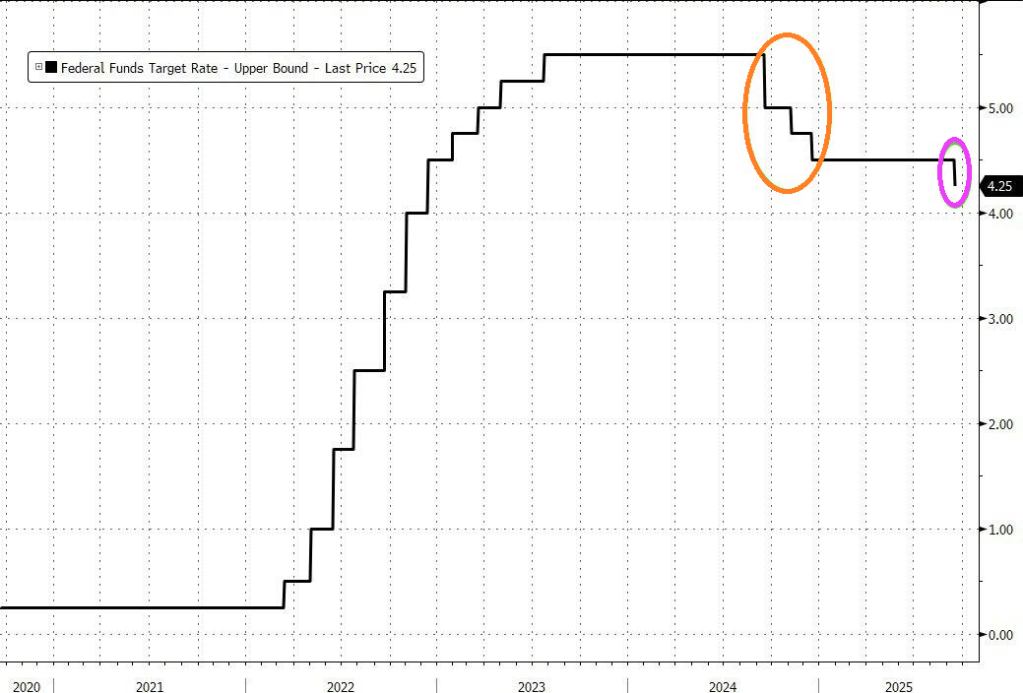

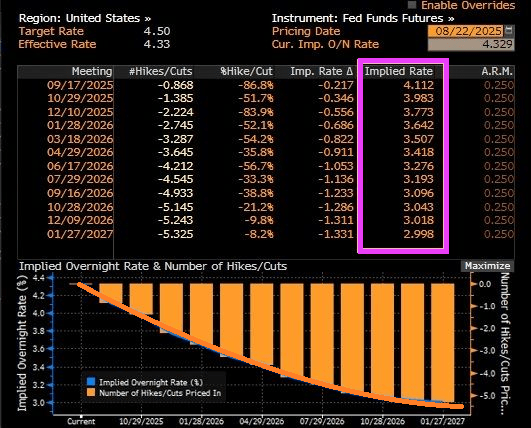

Let’s see if Powell and The Gang drop rates 25 or 50 basis points at today’s FOMC meeting.

Between The Fed’s persistent policy errors and Biden’s centralized mismanagement of the economy, Biden’s Maladministration is the epitome of a “Reign of Error.”

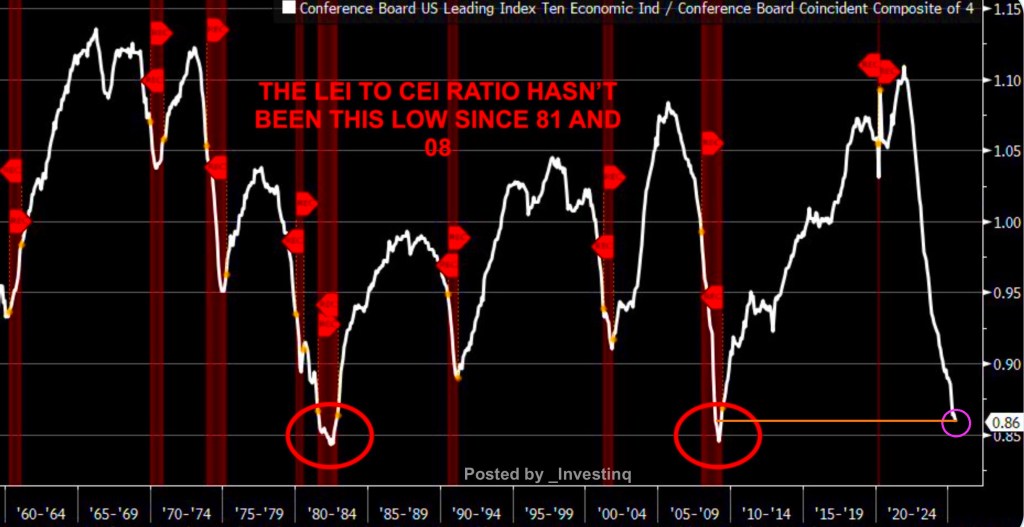

The Fed will have to whip it good with rate cuts if the recession warnings are an indicator of what lies ahead for the US economy.

The ratio of The Conference Board’s Leading Economic Indicators (LEI) vs. The Conference Board’s Coincident Economic Index (CEI) ratio hasn’t been this low since 2008.

Fed Funds Futures are signalling rate cuts at the September 17th FOMC meeting and December 10th meetings.

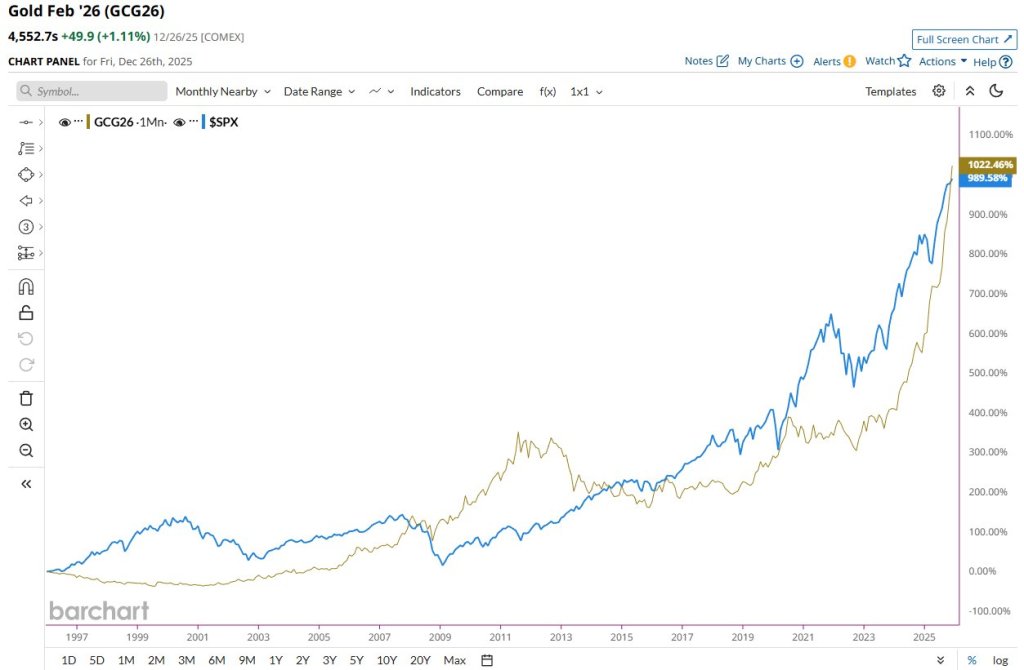

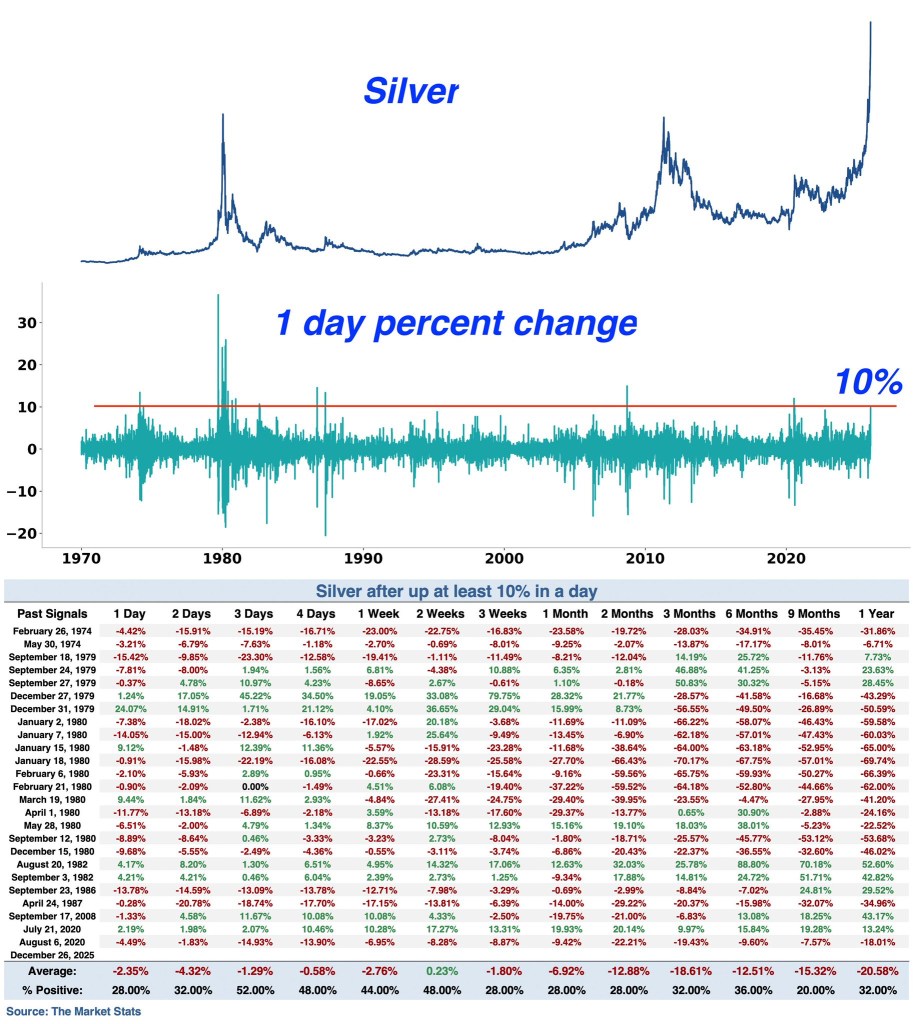

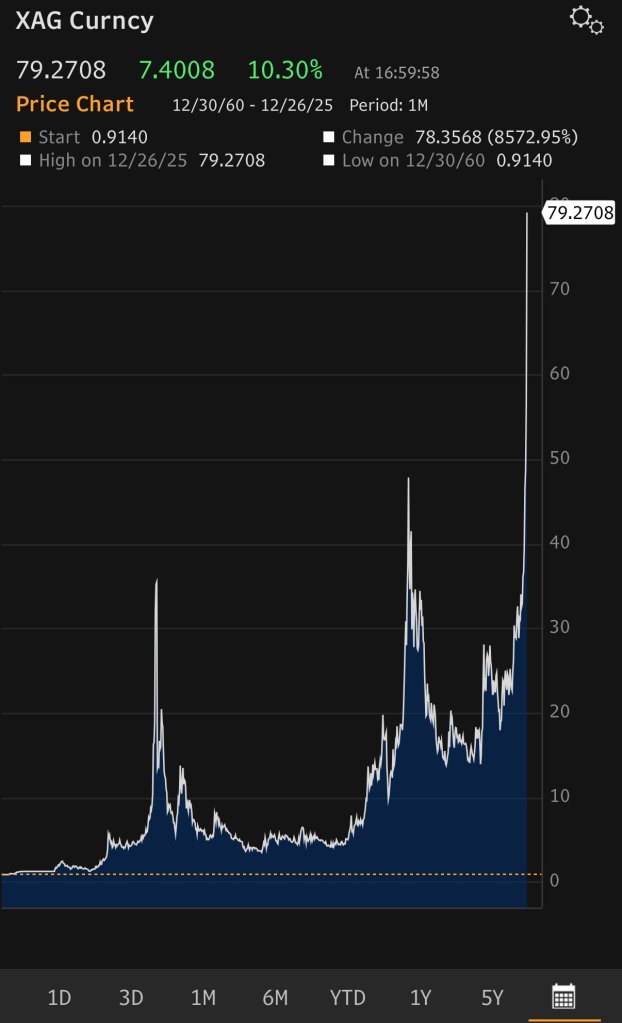

Tavi Costa at Crescat Capital (founded by my former MBA student at University of Chicago Kevin Smith) produced this excellent chart of silver prices showing the cup and handle of silver prices.

The rise in silver prices corresponds with a deterioration of the US bond market. Look at Treasury futures courtesy of Bravos Research.

Of course, Washington DC’s insane spending has led to insane money printing by The Feral Reserve.

Everyone in Washington DC deserves a “Silver Cup of Failure” for uncontrolled government waste and spending and mismanagement by The Feral Reserve.

{kind=link}

{kind=link}

You must be logged in to post a comment.