(Bloomberg) — The Federal Reserve will likely raise interest rates four times this year and will start its balance sheet runoff process in July, if not earlier, according to Goldman Sachs Group Inc.

Rapid progress in the U.S. labor market and hawkish signals in minutes from the Dec. 14-15 Federal Open Market Committee suggest faster normalization, Goldman’s Jan Hatzius said in a research note.

“We are therefore pulling forward our runoff forecast from December to July, with risks tilted to the even earlier side,” Hatzius said. “With inflation probably still far above target at that point, we no longer think that the start to runoff will substitute for a quarterly rate hike. We continue to see hikes in March, June, and September, and have now added a hike in December.”

In its December meeting minutes, Fed officials signaled they are preparing to move quicker than the last time they tightened monetary policy in a bid to keep the U.S. economy from overheating amid high inflation and near-full employment. These conditions — along with a larger balance sheet that’s suppressing longer-term borrowing costs — “could warrant a potentially faster pace of policy rate normalization,” the minutes said.

Officials also saw the timing of reducing the $8.8 trillion balance sheet as likely “closer to that of policy-rate liftoff than in the committee’s previous experience,” according to the minutes.

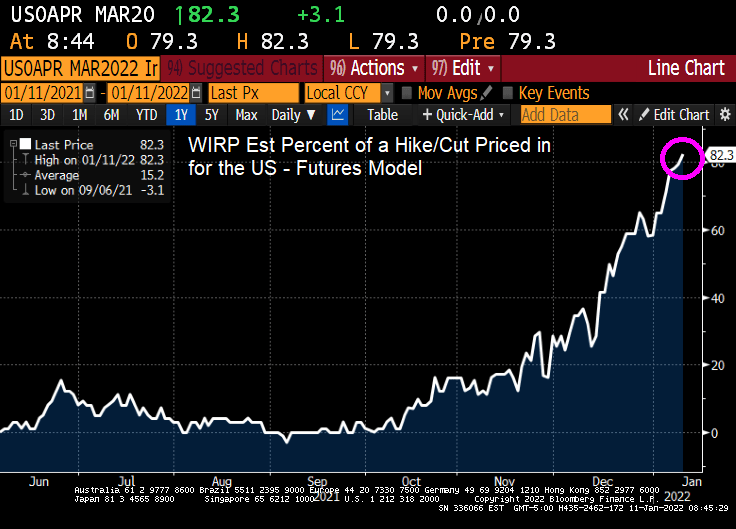

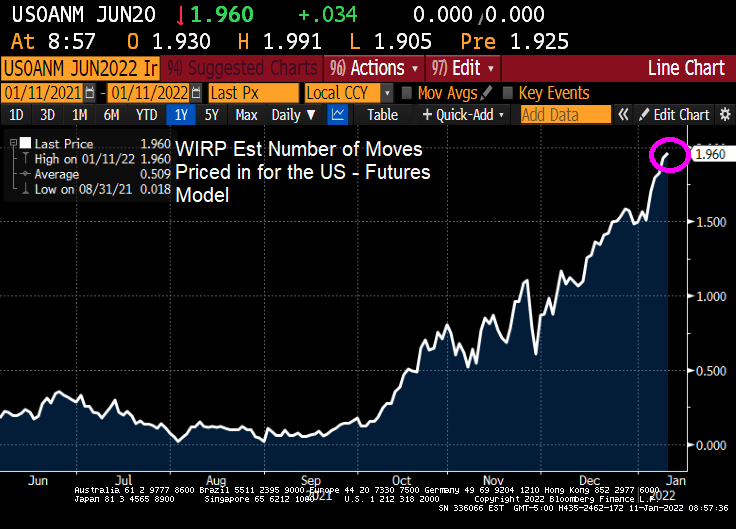

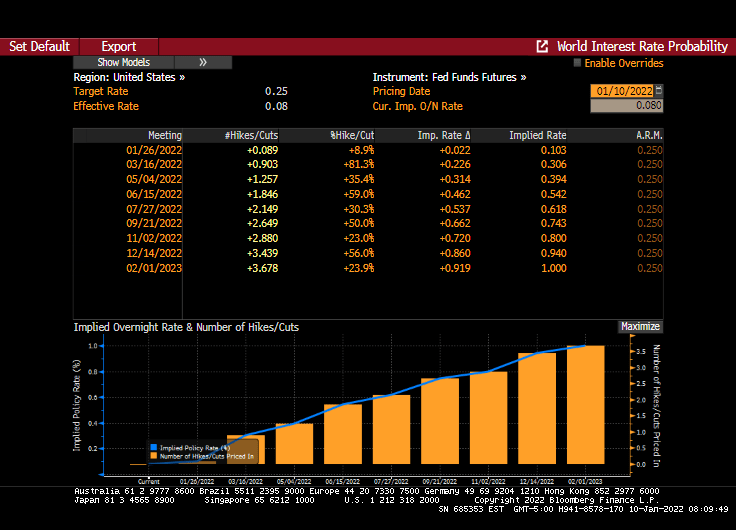

While Goldman sees 4 rate hikes in 2022, The Fed Funds Futures market only sees 3 rate hikes and the Fed Funds target rates hitting 1% by Feb 2023.

An increase to 1%? The Fed Funds target rate hit 5.25% during the housing bubble in 2006/2007 and markets are worried about an increase to 1%??

So, Goldman thinks that there will be faster “run-off” than expected. This simply means that The Fed will allow Treasuries and Agency MBS to mature rather than actually sell securities.

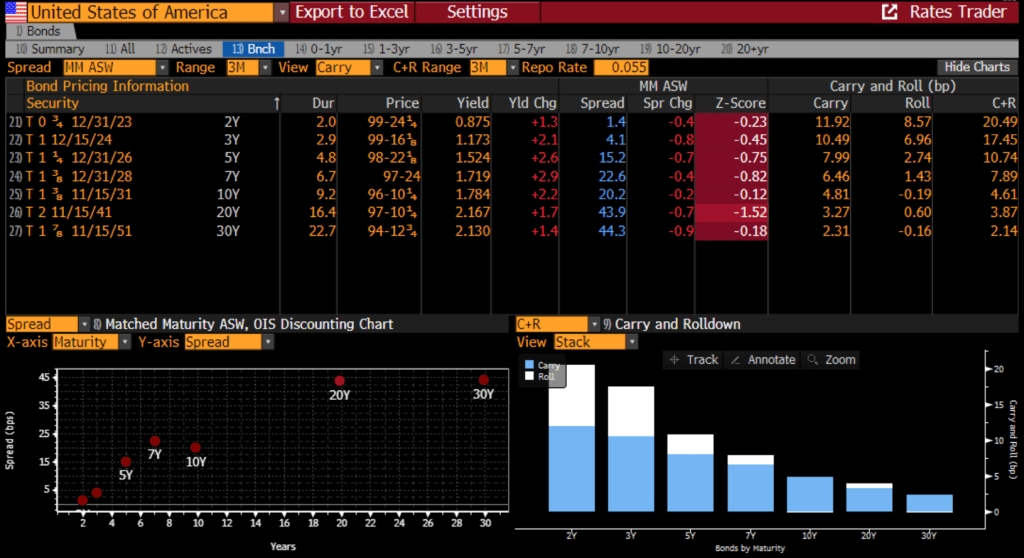

With the expectation of Fed activity, z-scores for Treasuries are negative across the board.

So we shall see if The Fed Open Market Committee are hawks, doves or “birds of war.”

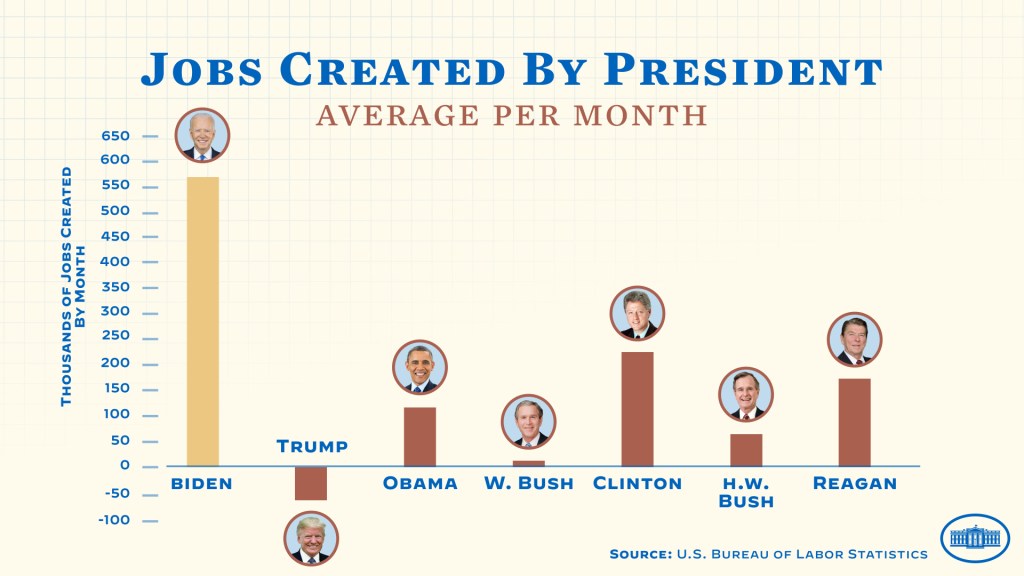

Recently, the White House claimed that the Biden Administration created more jobs (per month) than Trump, Obama, George W Bush, George HW Bush, Clinton and Reagan.

It always helps to be elected President after a recession when the economy naturally snaps back from the economic doldrums (like Obama after the financial crisis, Clinton after the first Gulf War, Reagan after Carter).

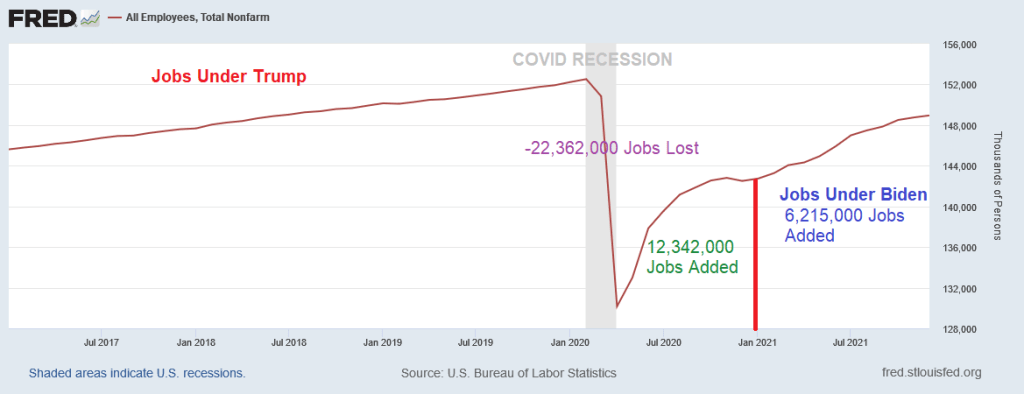

So let’s look at job totals under Trump, the COVID lockdowns, the ensuing economic damage, and the Biden “rebound.” In a brief two months in early 2020 thanks to COVID and lockdowns, the US economy lost 22.362 MILLION jobs. But the snap-back effect under Trump was 12.342 MILLION jobs added back by the time Biden was sworn-in as President.

Under his term as President, Biden has benefited from “Snap-back inertia” and saw 6.215 MILLION jobs added in just a year. Pretty impressive, except that it is about half the snap-back effect experienced under Trump.

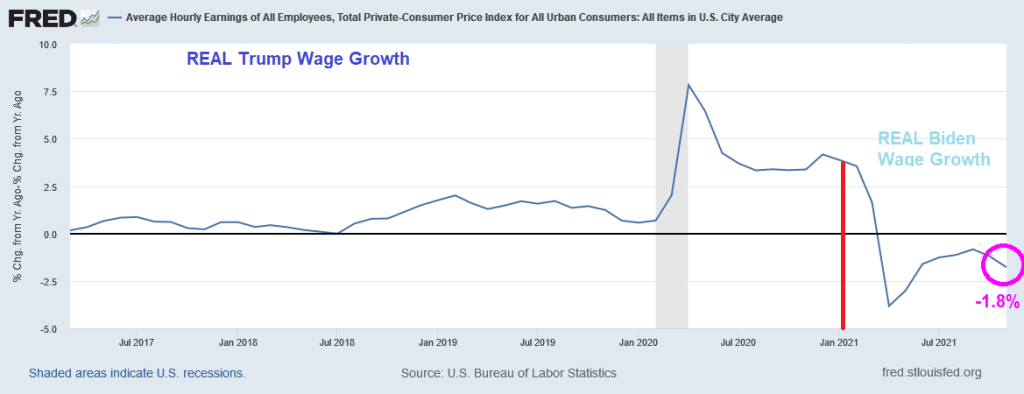

How about REAL wage growth (nominal wage growth less inflation)? Real wage growth was higher under Trump and has been declining under Biden. Strange that the White House isn’t bragging about declining real wage growth under Biden.

Let’s see how Omicron impacts the labor market and whether Biden/Psaki will take credit for the snap-back from Omicron.

Call this the Biden malaise (or Ka-malaise) for wage growth. Where inflation nukes positive wage gains.

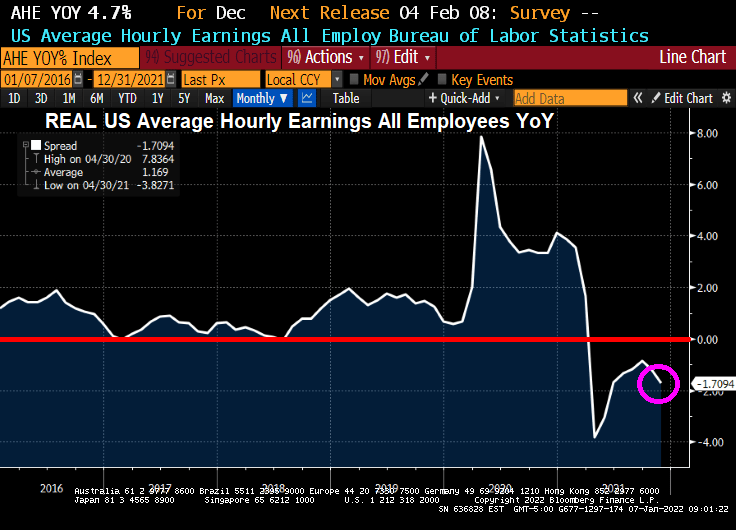

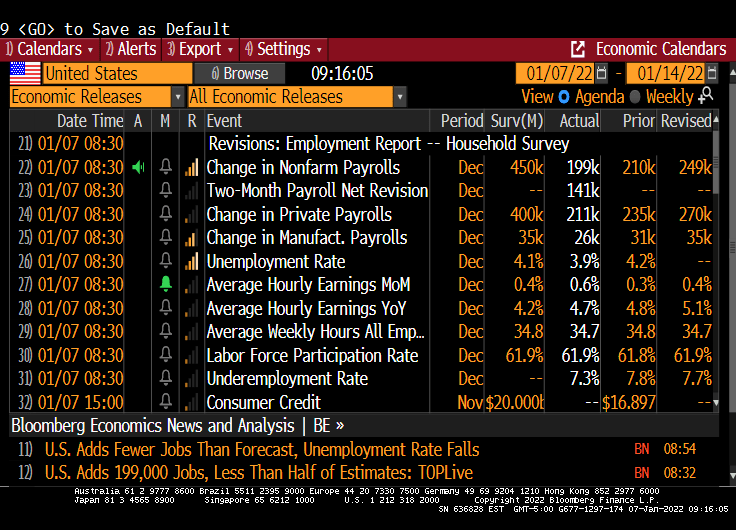

The November jobs report is out and the highlight is that US Average Hourly Earnings GREW at a rate of 4.7% YoY. Unfortunately, inflation is still raging resulting in REAL US Average Hourly Earnings DECLINING at a rate of -1.71% YoY.

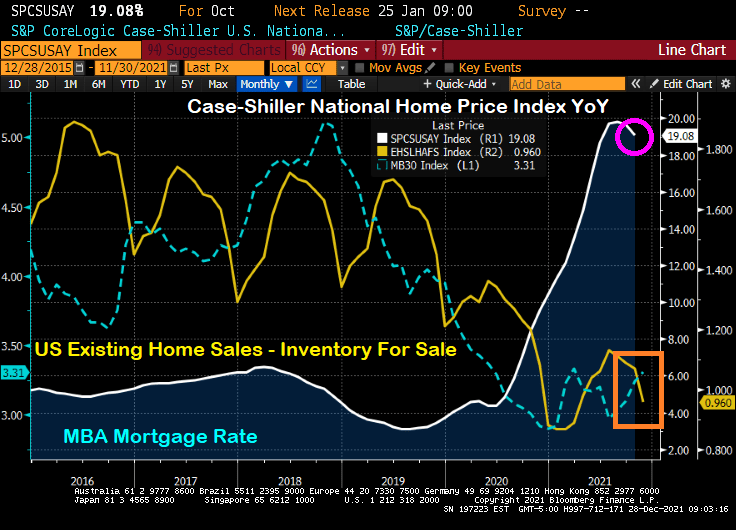

REAL US home price growth is slowing and is at 12.856% YoY as REAL average hourly earnings slowed to -1.7094% YoY.

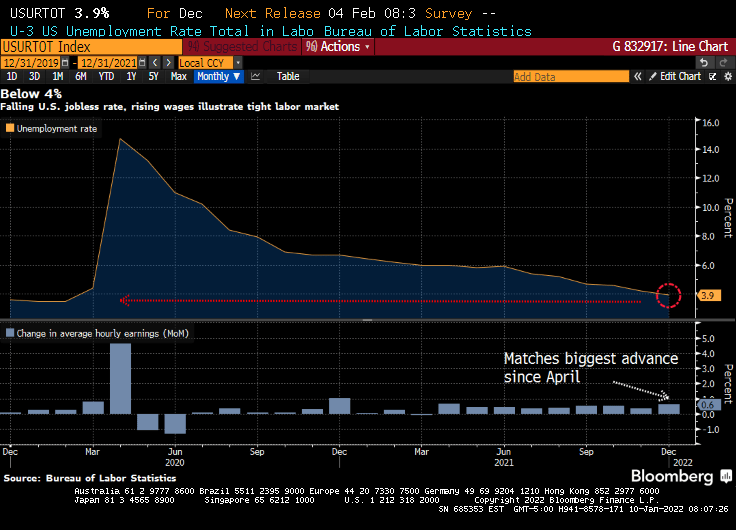

The lowlight of the November jobs report is that only 199K jobs were added versus the 450K jobs expected to be added. At least the unemployment rate fell to 3.9%.

WHERE we the jobs added? Leisure and hospitality led the way! Hey bartender.

Yes, REAL wage growth and REAL home price growth are slowing.

A good quote from The Hill story: “Under Biden, the American economy has recovered from its Trump-era lows with remarkable speed.” As Leslie Knope said “That seems like an unfair phrasing.”

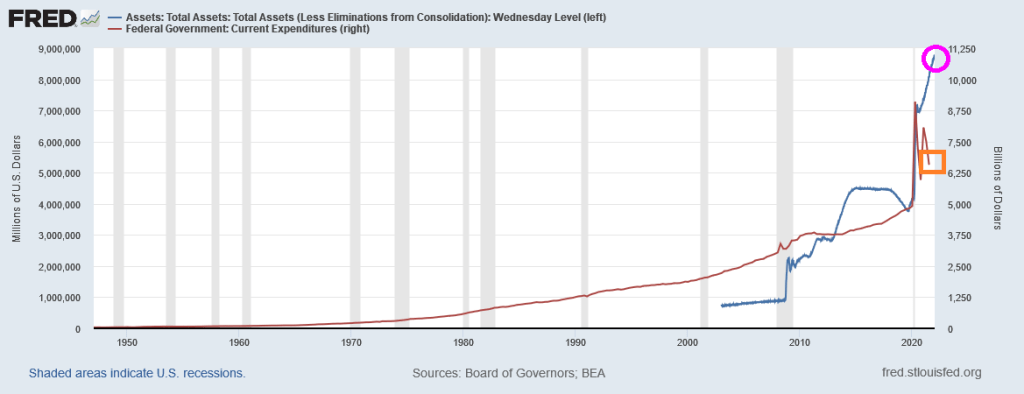

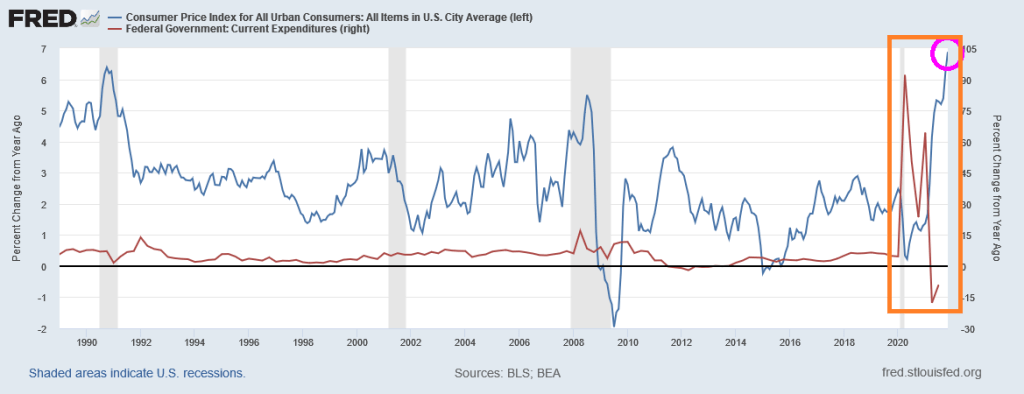

Hmm. Well, here is a chart that best explains the “Biden Miracle.” It shows the growth in Federal expenditures from the previous year during the banking crisis and then the COVID crisis. During the banking crisis, the increase in Federal expenditures (red) was normal. It was the increase in The Fed’s balance sheet (blue) that was staggering. But for the mini-recession related to COVID (only two months so you can barely see it on the chart below), it was the growth in Federal expenditures (red) combined with another round of staggering Federal Reserve stimulus (blue).

A different view of Federal “Stimulypto” is show below. Since COVID and the election of Joe Biden as President, Fed monetary stimulus is at an all-time high and Federal expenditures, while they have slowed, are still above the pre-COVID spending levels.

Please note that the massive surge in Federal expenditures and Fed monetary stimulus began under Trump, but were only continued under Biden. That is why no one notices … it was Trump.

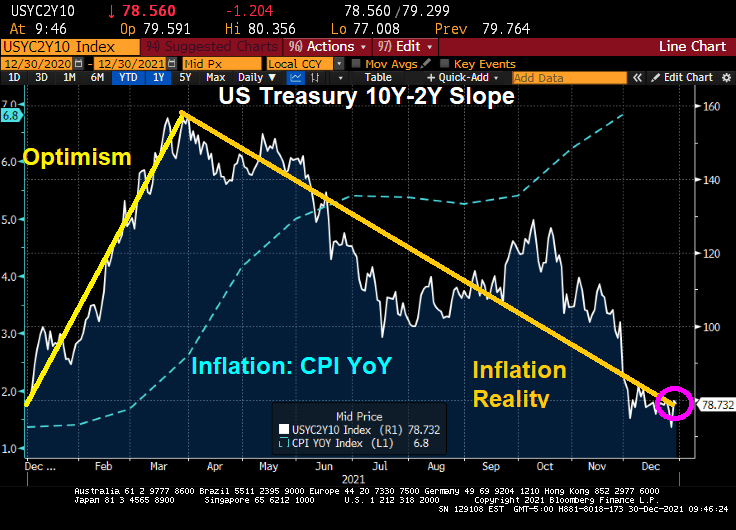

And if we look at the 10Y-2Y Treasury curve slope, the US is slippin’ into darkness since the slope typically rises after a recession, then falls. And we are in the falling (or slippin’) stage.

So, President Biden is benefiting from Trump’s and The Fed’s Stimulypto. I don’t expect partisan outlets like The Hill or crooner Barbra Streisand to look at the data.

With Build Back (Inflation) Better not passing in the US Senate, I fully expect The Federal Reserve to continue “low riding” interest rates. Inflation will probably cool as well as Federal expenditure growth slows.

So, Streisand’s statement should have said “Joe Biden’s economic record in his first year is the best in 40 years. The media largely ignores this … because the unsustainable Federal stimulus began under Trump, not Biden.”

Another thing The Hill and Barbra Streisand left out was declining REAL average hourly earnings growth (that is, average hourly earnings YoY – inflation).

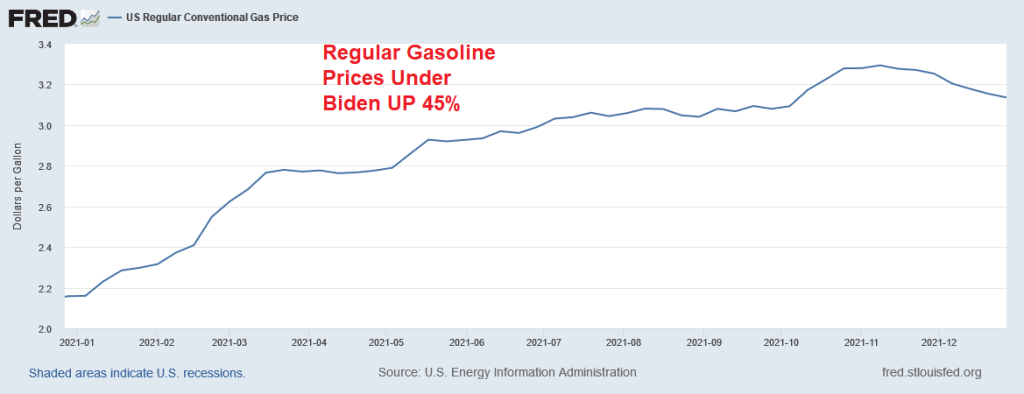

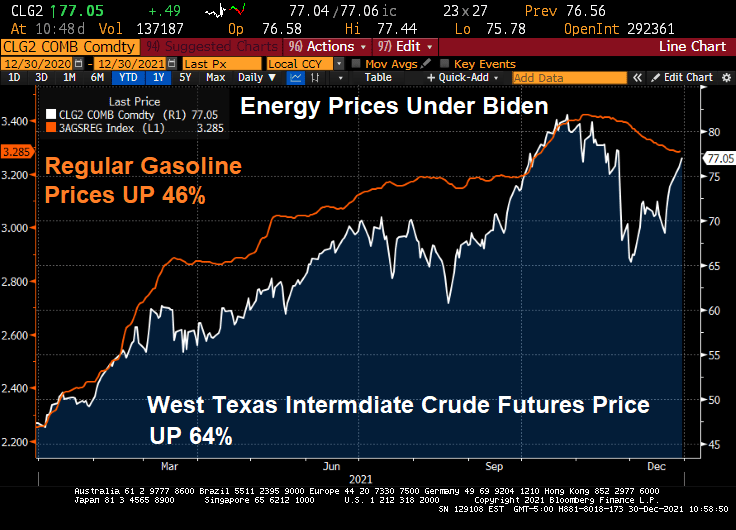

Biden’s real contribution? Anti-fossil fuels actions have driven up energy prices. Regular gasoline prices, for example, are up 45% under Biden.

If The Fed actually follows through and removes COVID stimulus and Congress doesn’t keep the incredible rate Federal spending growing, I sincerely doubt that GDP will continue at this hot pace.

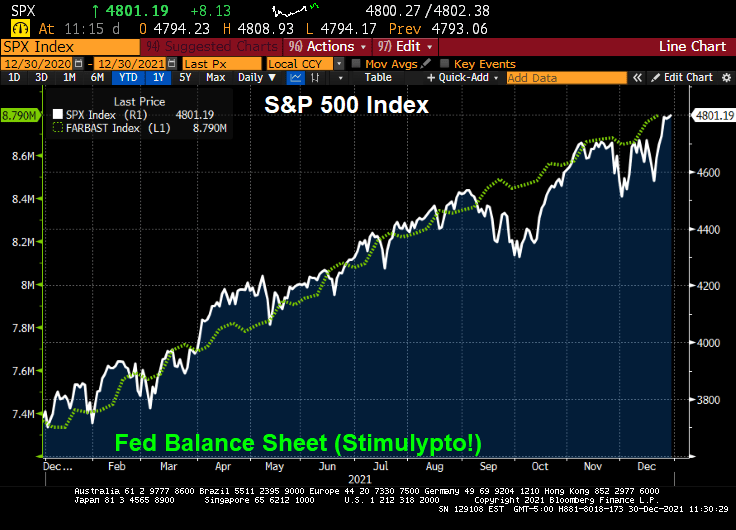

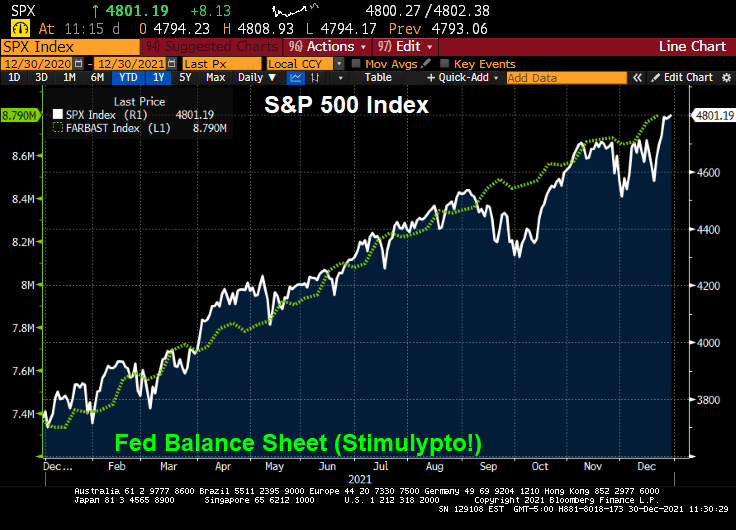

2021 saw the S&P 500 index generate a return of 28.7%. Much of it thanks to The Federal Reserve “stimulypto” or excessive monetary easing.

But only three hedge funds beat the S&P 500 index: Senvest, Impala and SR. Thanks to fees (trading and management), the other hedge funds underperformed the S&P 500 index. And underperformed The Fed!

Melvin Capital was the worst performing hedge fund of the ones examined.

It has been almost a year since Joe Biden has been President of the United States and a Democrat majority took control of The House and Senate. And what has happened to the US Treasury yield curve slope over the past year?

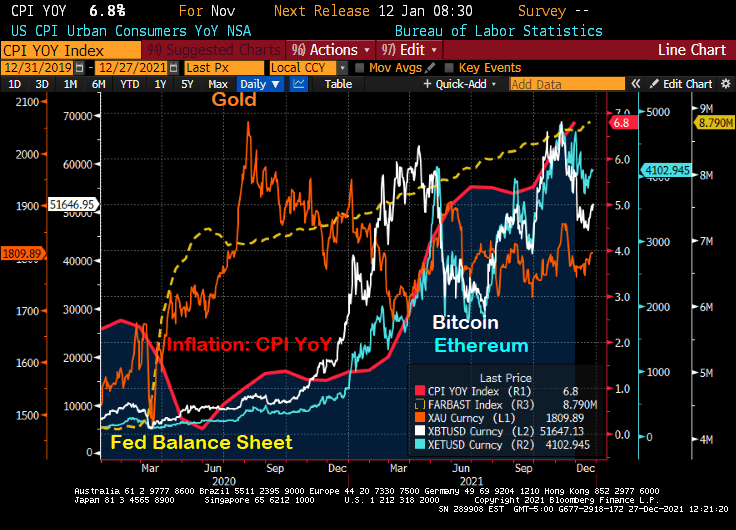

The yield curve is back where it started. There was the “honeymoon effect” where the curve slope rose. After all, Biden was Obama’s Vice President for 8 years and The Democrats has promised so much in the 2020 election. But by early April, the reality of the massive Federal spending (combined with Fed Stimulypto) began showing what was feared: inflation (blue line) started to grow at a rapid rate of speed. With inflation now at 6.8% YoY,

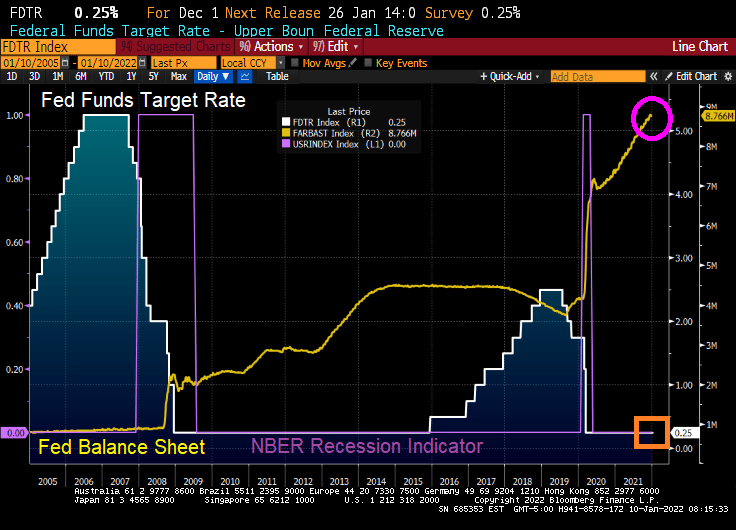

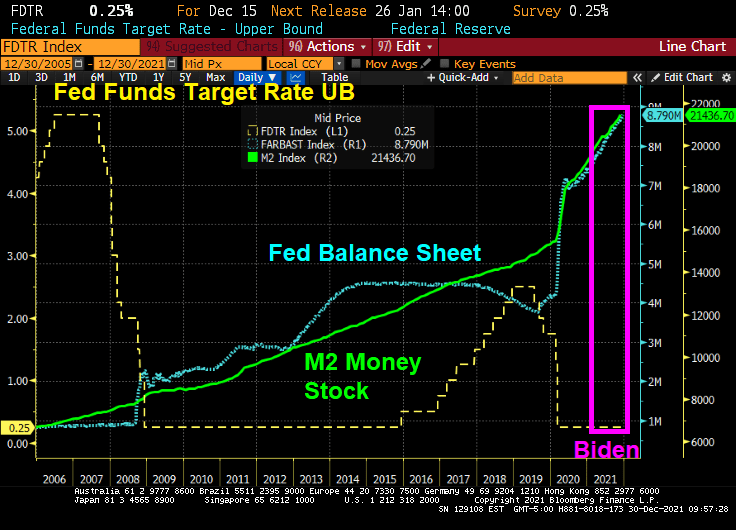

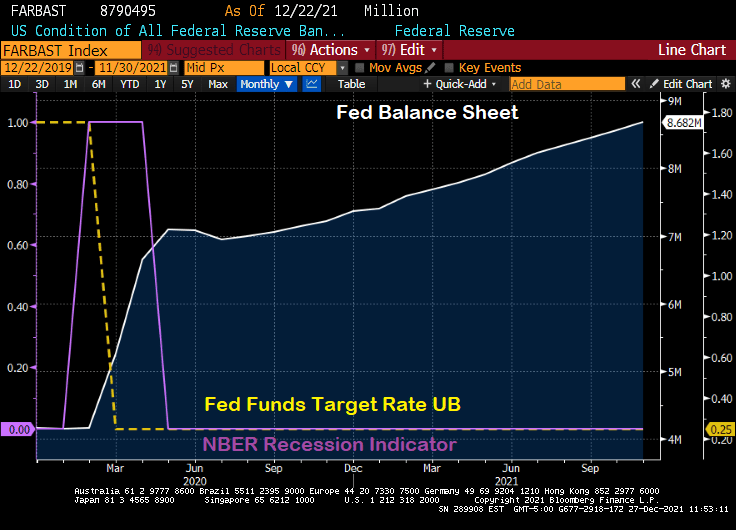

In fairness to Biden, The Federal Reserve has been overstimulating the economy since The Federal Reserve since Ben Bernanke and the Fed Open Market Committee (FOMC) dropped the hammer on The Fed Funds Target Rate once the rate hit 5.25% in September 2007. They kept cutting it reached 25 basis points (or 0.25%) in December 2008. In August 2008, Bernanke and Company began their “Quantitative Easing” or asset purchasing programs. Between The Fed’s Target Rate and QE, The Fed has continued to overstimulate markets ever since. Under Biden, The Fed Funds Target Rate remains at 0.25% and The Fed’s Balance sheet has grown to $8.79 Trillion (bigger than the entire economies of Japan and Germany put together!).

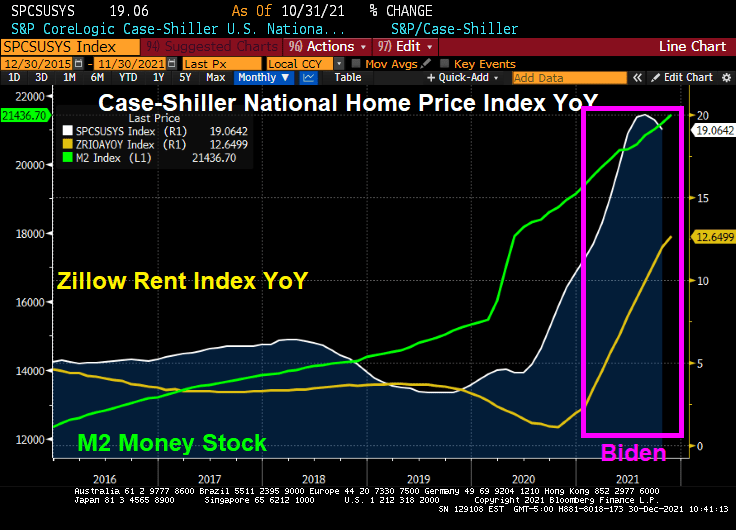

How about housing? Home prices are growing at 19% YoY while rents are growing at 12.65% YoY.

Energy prices have risen dramatically under Biden. Gasoline is up 46% despite a slight reprieve recently. WTI crude prices are up 64%.

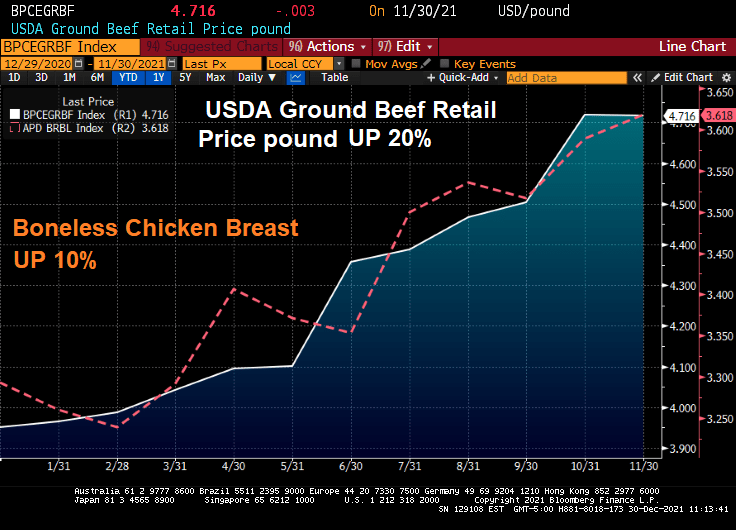

How about food? Beef prices are up 20% and chicken prices are up 10%.

On a positive note, the S&P 500 index has soared … thanks has soared during Biden’s term thanks to Fed stimulus and Federal spending on COVID.

The Build Back Better Act if passed (in its entirety or on a piecemeal basis) will lead to even MORE inflation.

Perhaps Biden’s spokesperson Jen Psaki can recreate the Biden Administration as a lovable, hilarious family like the comic strip Gasoline Alley with old Joe Biden as Skeezix. And insider-trading star, House Speaker Nancy Pelosi as the family matriarch.

There is a lot going on in the US housing market. Excessive monetary stimulus keeping mortgage rates low, historically low inventory available for sale, and FOMO (fear of missing out … on rapidly rising home prices).

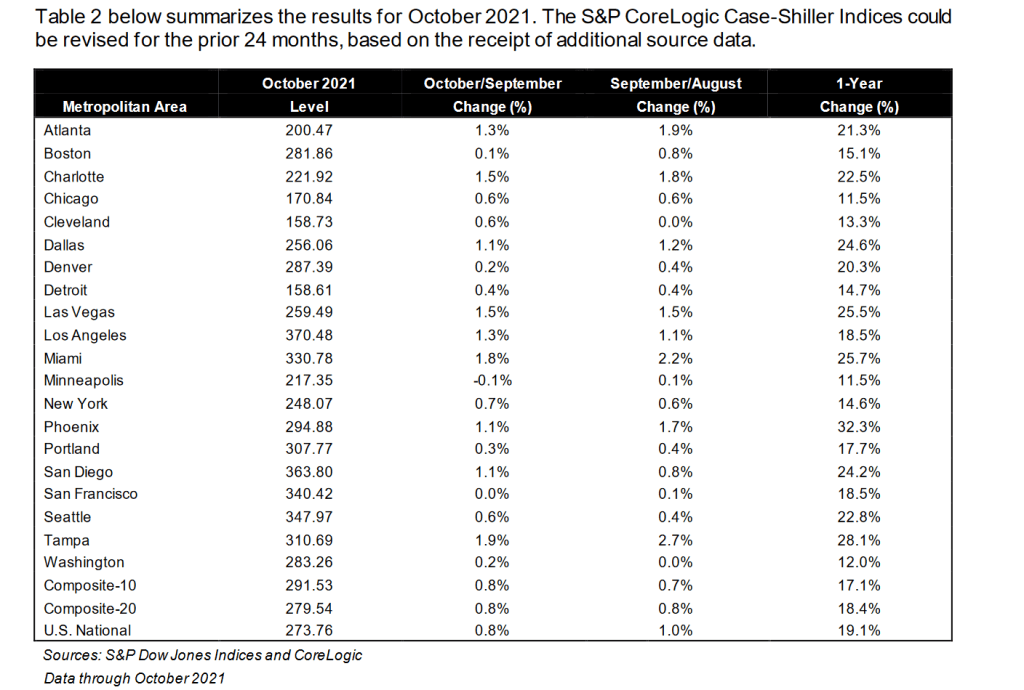

By metro area, Phoenix AZ once again leads with 32.3% YoY. Minneapolis MN is the slowest growing metro area in terms of home prices at 11.5% (tied with Chicago, IL).

The global economy has certainly been turned on its head by the COVID outbreak in early 2020. Not so much by the virus itself, but by Central Bank hysteria in terms of rate lowering and balance sheet expansion. Which The Fed has not yet unwound.

Let’s look at what has happened since the mini-recession caused by COVID in early 2020. The shortest recession in US history, a measly 2 months. The Fed expanded its balance sheet from $4.17 million in February 2020 to $8.79 million today. That is, The Fed over doubled the size of their balance sheet in reaction to the shortest recession in US history. Overreaction much?

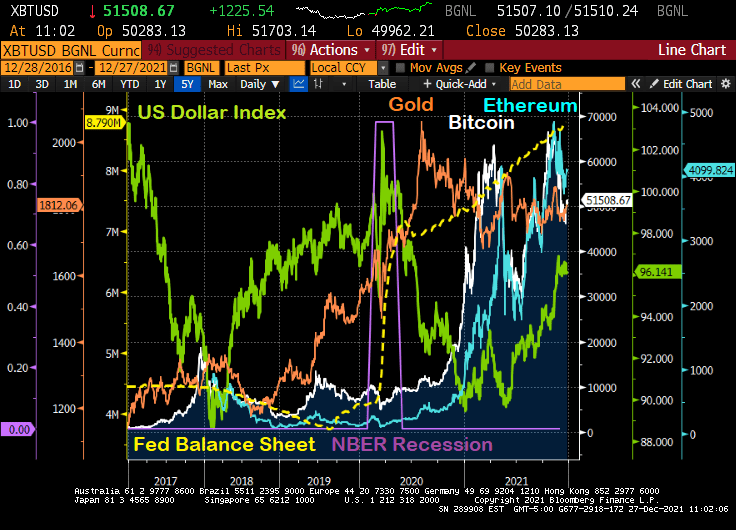

What has happened since the mini-recession and The Fed’s massive overreaction?

First, gold (gold line) surged then calmed down. Then cryptocurrency Bitcoin (while line) surged, then calmed down, then surged again only to calm down again. Then crypto Ethereum surged, calmed, surged, calmed. Meanwhile the US Dollar Index crashed only to start rising again.

The Fed’s overreaction and failure to withdraw excessive stimulus has led to the rise of alternatives to the deflating dollar due to inflation.

When will The Fed ACTUALLY start removing the overreaction stimulus? Let’s get it started.

Perhaps only April Ludgate can kill The Fed’s overreaction stimulus.

You must be logged in to post a comment.