The littany of horror stories about government attempts to make housing more “affordabl;e” at enmdless.

New York mayor Zoran Mandami appointed Cea Weaver as New York City’s housing Tsar allegedly to make housing more affordable. Her proposal? People should pay 30% of their income for housing. if you have no income, you pay zero. Then she decreed that you must offer your multifamilty property to the city first before you sell it in the open market. Allegedly for the “greater good.” Which means a small number of elites will make a fortune (Mandami donors?).

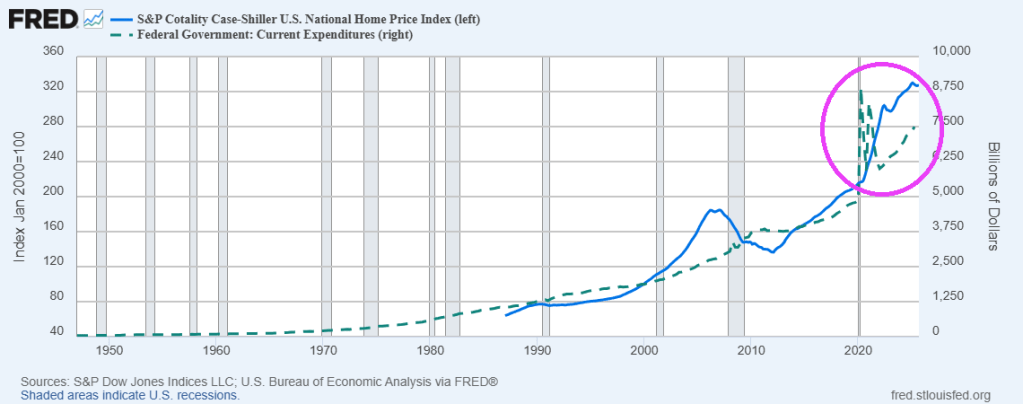

But harken back to the Clinton Administration where they issue a proclamation to make housing more affordable, the national homeownership strategy. This strategy helped usher in an era of lowering credit standards and higher LTV lending. Leading to the mortgage crisis of 2008. Thanks a lot Bill and Hill!

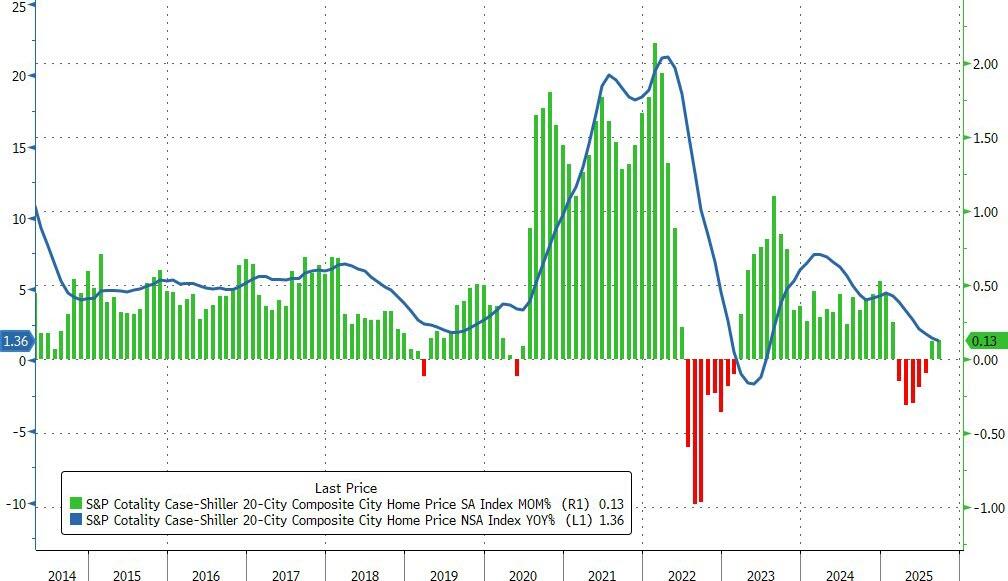

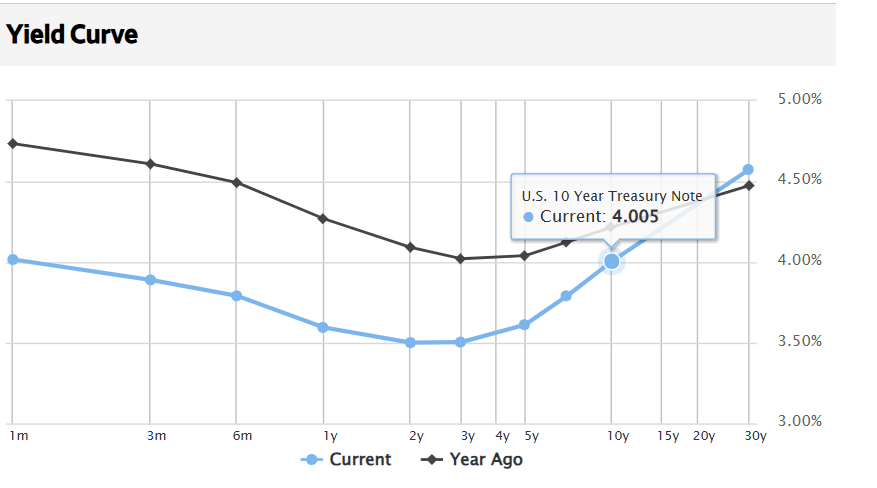

And then we have The Federal Reserve, the master manipulators of interest rates. While mortgage rates have fallen recently to around 6%, they are up 134% from Biden’s Maladministration. So while The Fed contributed to the housing bubble that blew up and nearly destroyed the banking industry.

Government and especially Cea Weaver. A child of privelege.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.