Powell and The Fed’s policies have veered from their mandate requiring Chairman Powell to meet 350 times with Congress to sell The Fed’s policies.

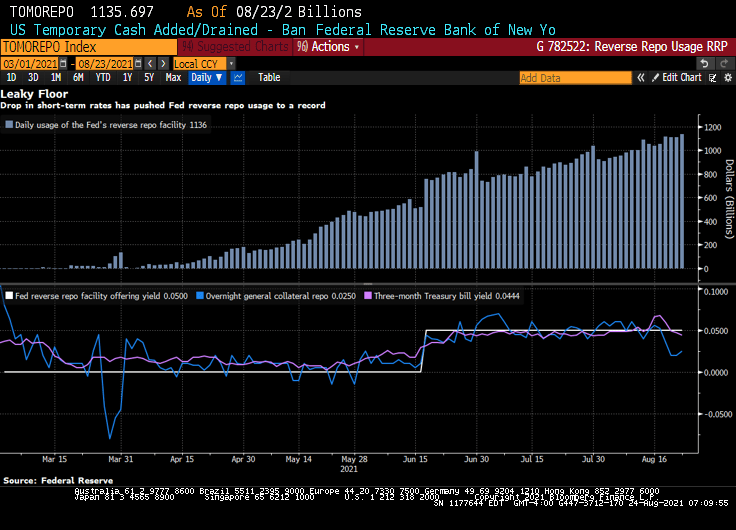

Bloomberg) — The Federal Reserve’s floor for overnight funding markets is proving to be no match for the deluge of cash.

Money-market securities ranging from Treasury bills to repurchase agreements continue to trade below 0.05% — the offering rate on the overnight reverse repo facility, which is supposed to act like a floor for the front end. The Fed at its June meeting had raised the rate by five basis points to help support the smooth functioning of short-term funding markets.

Still, usage of the tool climbed to a record $1.136 trillion on Monday, eclipsing the previous high of $1.116 trillion on Aug. 18.

Demand for the so-called RRP facility has surged as a flood of dollars threatens to overwhelm funding markets. That’s in part a result of the central bank’s long-standing asset purchases and drawdowns of the Treasury’s cash account, which is pushing reserves into the system. As a result, liquidity has been swelling, especially as the Treasury cuts supply to create more borrowing room under the debt ceiling.

The pressure pushing down overnight rates toward zero is proving a major headache for money-market funds. It hampers their ability to invest profitably, and can lead to further disruptions as they begin to waive fees to avoid passing on negative rates to shareholders. A number of firms including Vanguard Group shut down prime money-market funds last year after struggling to cover operating costs in the low-interest-rate environment.

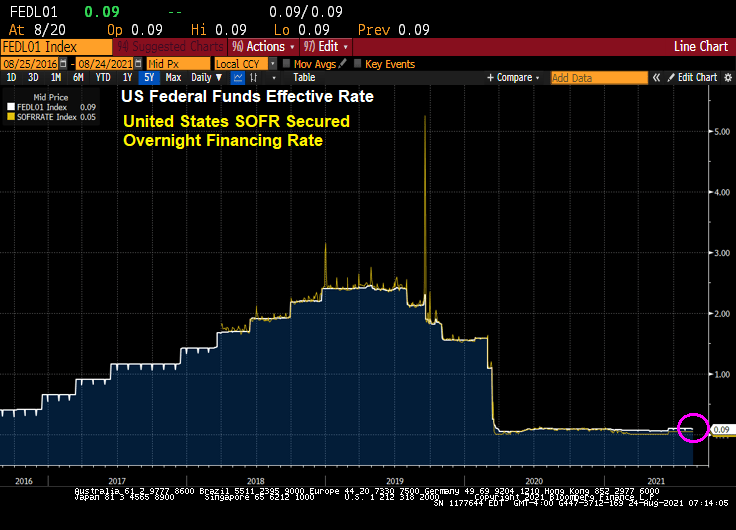

Yes, overnight rates such as the US SOFR rate, are near zero.

Powell’s Charm Offensive in Congress Positions Him to Keep Job

Perhaps that is why Federal Reserve Chair Jerome Powell is acting as a lobbyist with Congress for The Fed’s nontraditional approach to monetary policy.

(Bloomberg) Since he took the helm of the Fed in February 2018, through June of this year, he’s held at least 350 meetings, dinners or phone calls with members of Congress, according to his monthly calendars. That’s almost nine per month, and many of those included more than one lawmaker. The tally doesn’t count at least 16 appearances as chair before numerous congressional committees.

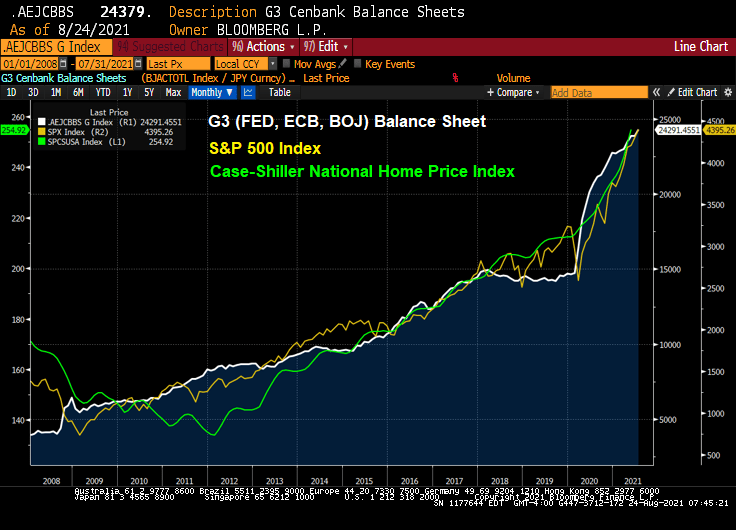

Well, the stock market has zoomed-up since Bernanke and The Fed adopted zero-interest rate (ZIRP) policies and the now famous quantitative easing (QE) policies in late 2008.

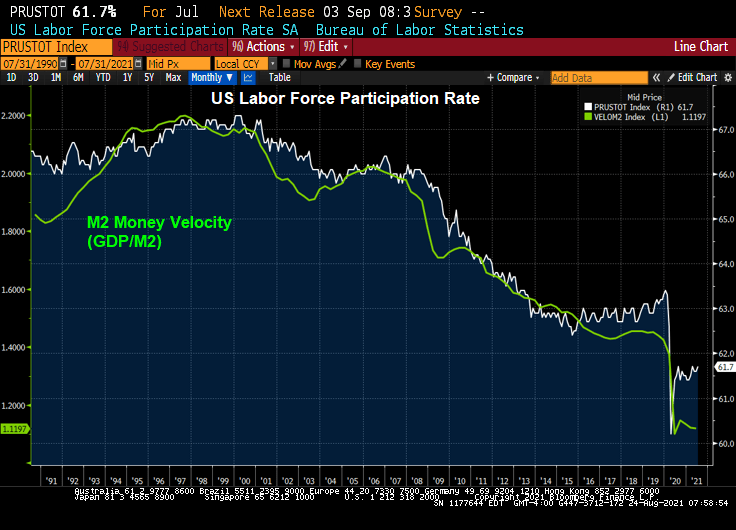

Congress member Alexandria Ocasio-Cortez asked Fed Chair Powell about the Fed helping with US unemployment. We are already at zero rates (on the short-end), and Congress should look at their policies on why labor force participation is slow to recover from the Covid epidemic.

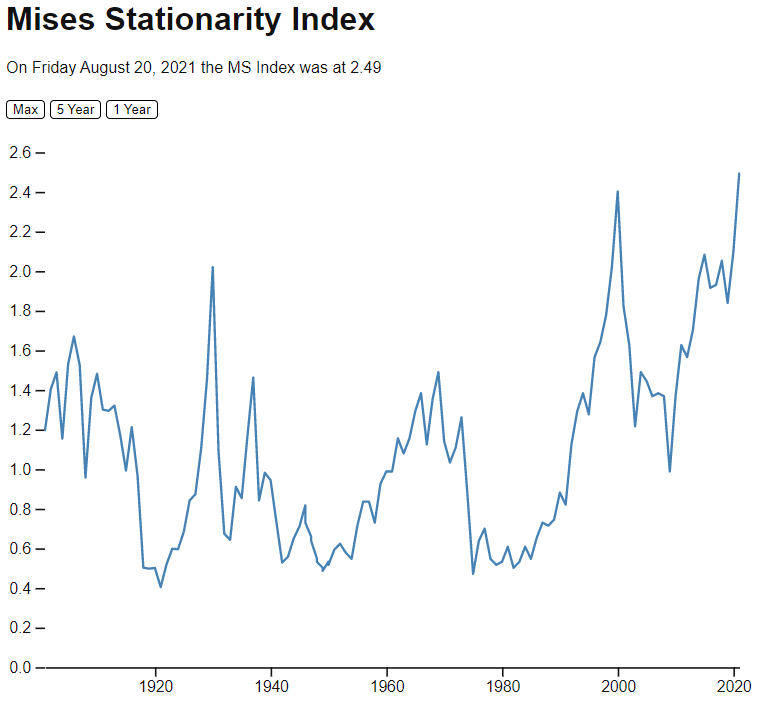

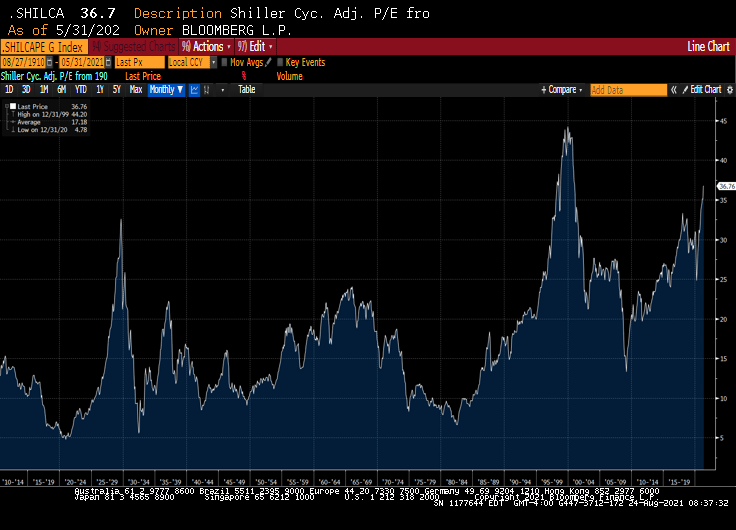

The Mises Stationarity Index is different than the Shiller CAPE index, which is showing equities as being overpriced, but not yet in dot.com bubble zone.

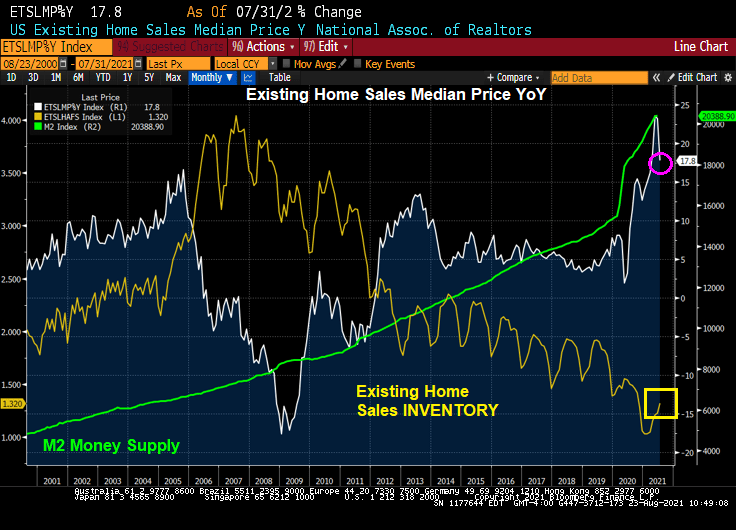

US existing home sales in July rose to 5.99 million SAAR, beating expectations. But the inventory of home available for sale remains low by historic standards.

The median price of existing homes declined to 17.8% YoY with The Federal Reserve pumping money into the system like there is no tomorrow.

Bloomberg had the following headline: “Sales of Existing Homes in U.S. Rise as Inventory Picks Up.” While that is a true statement, existing home sales inventory is still down 12% YoY.

I wonder if the attendees at the Jackson Hole Fed conference will be discussing the gut-wrenching home price growth? Rumor has it that Fed Chair Powell will use J-Hole as a platform to suggest paring back on the monetary stimulus.

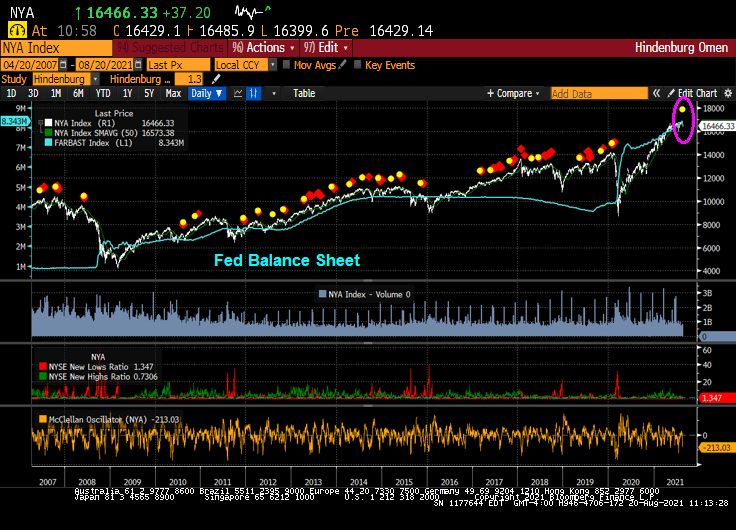

The famous Hindenburg Omen, the technical indicator that predicted the 2008 correction in the stock market, has just flashed “ALARM” again.

To be sure, there hasn’t been a major correction in the stock market since the financial crisis, primarily because The Federal Reserve has constantly goosed the markets since late 2008.

Just as the Shiller CAPE ratio is signalling ALARM!

As is the Buffet Indicator.

I have no doubts that the Fed will withdraw its monstrous stimulus from the market after the Jackson Hole Fed conference. … NOT!!!!

Maverick Capital posted this nugget today showing The Buffet Indicator (US equity market cap/GDP) and US Corporate Profits / GDP. All I can say is “simply unsustainable.”

Headline! “Fed’s Kaplan says delta variant could cause him to rethink his tapering view”

Face it, the Federal Reserve may alter its growth path on asset purchases of Treasuries and Agency Mortgage-backed Securities, but it is doubtful that they will pare back their balance sheet. Call it “A Never-ending balance sheet for you” world.

Why? Seemingly never-ending Covid crisis, etc.

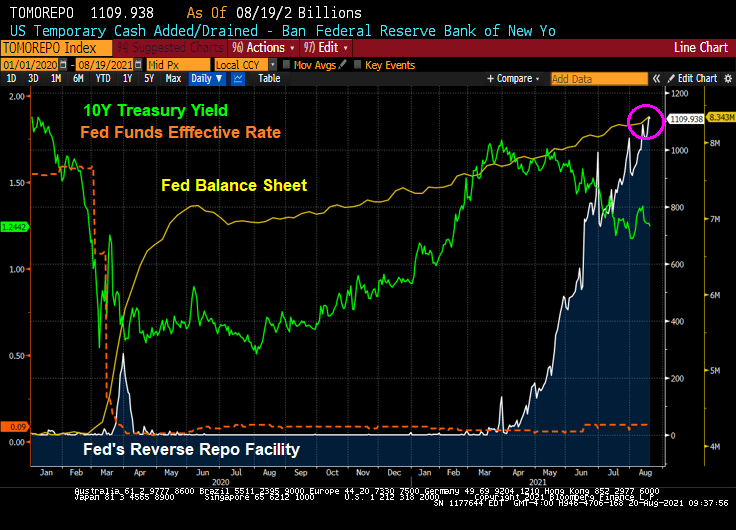

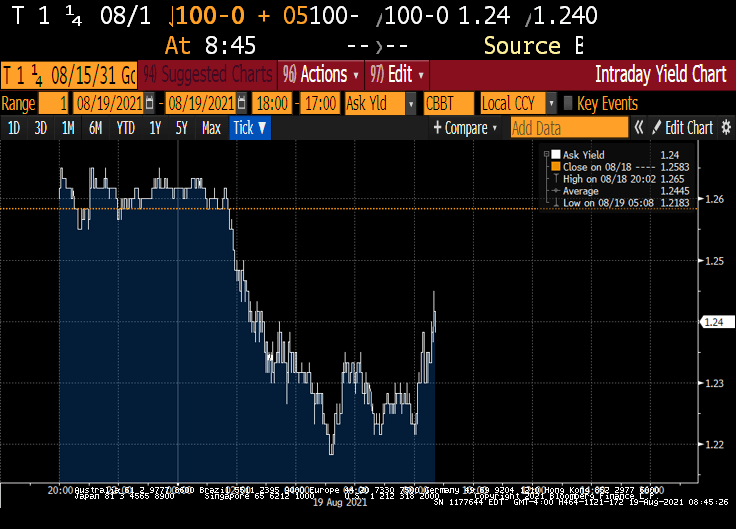

Let’s look at US Treasury yields today. The 10-year Treasury yield is up slightly to 1.25% as of 10am EST.

Here is a chart of the 10-year Treasury yield, Fed Funds effective rate, Fed Balance sheet and reverse repos since the Covid outbreak and Fed massive intervention. Bottom line, the have repressed the short-term interest rates and put downward pressure on the 10-year Treasury yield.

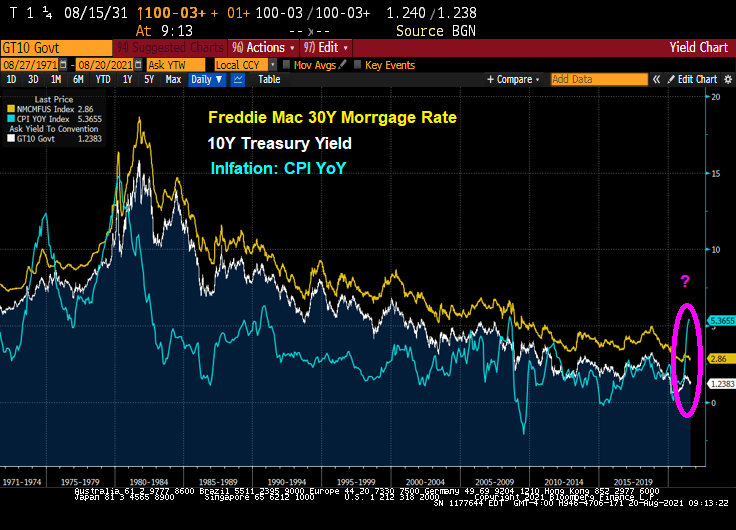

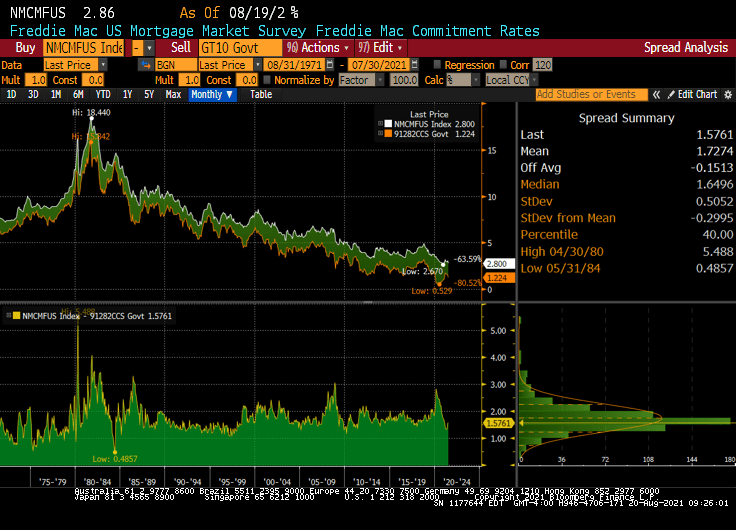

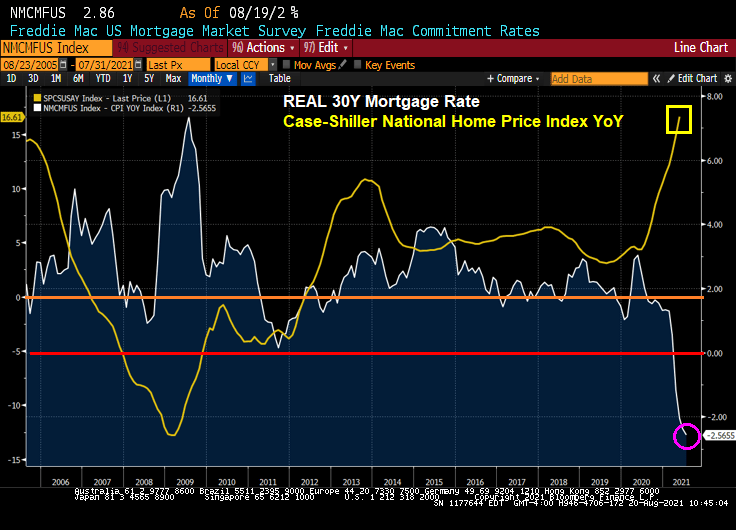

As the 10-year Treasury yield remains repressed DESPITE HIGHEST INFLATION RATE SINCE 2008, the Freddie Mac 30-year mortgage rate remains repressed as well. Yes, that mean NEGATIVE REAL MORTGAGE RATES.

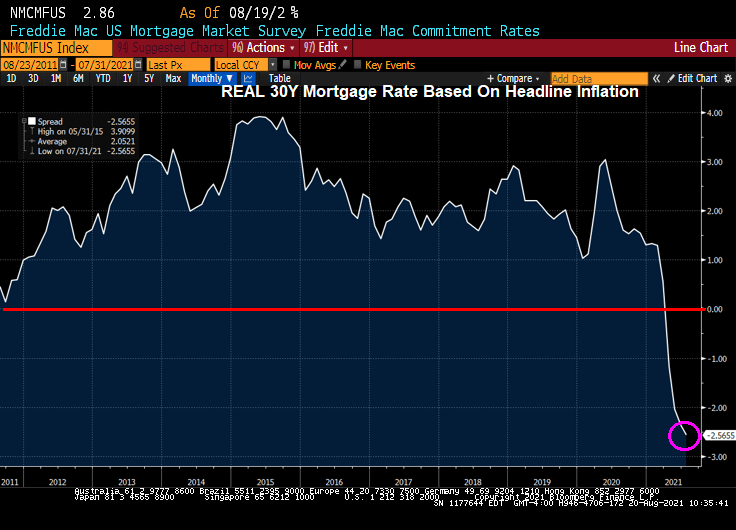

This produces a REAL mortgage rate of -2.56%.

The spread of mortgage rates over the 10-year Treasury yield is about 173 basis point since 1971.

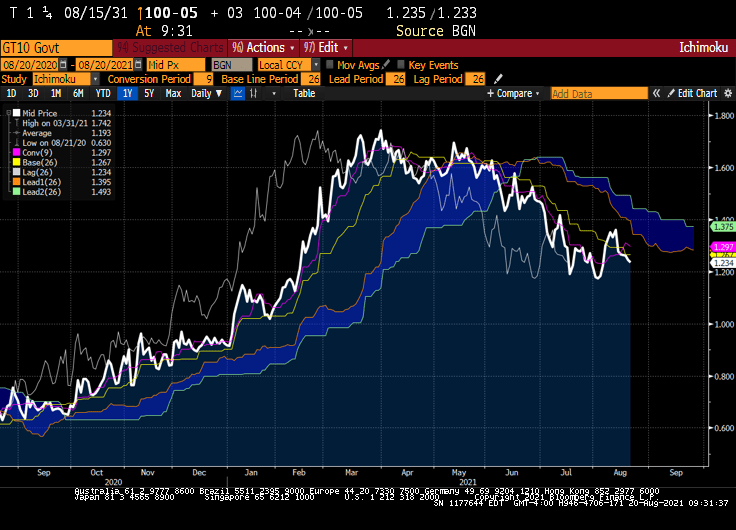

Where will Treasury yields go from hear? If we believe technical analysis like the Ichimoku Cloud, the 10-year Treasury rate will likely rise.

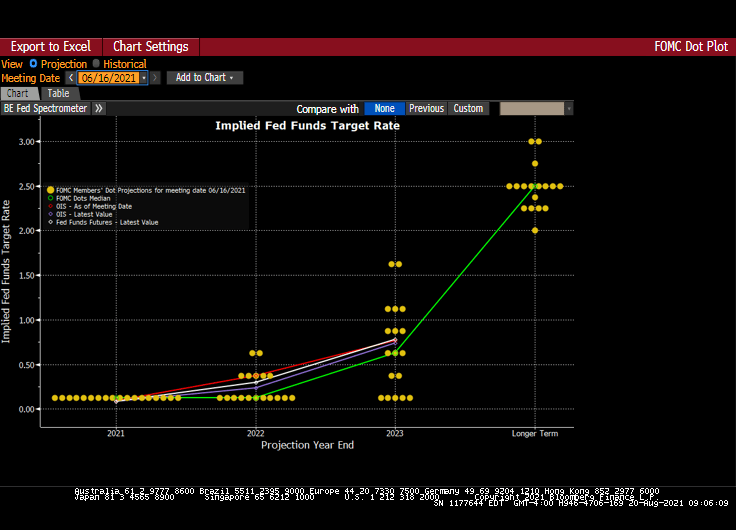

And The Fed’s Dots project also see rates rising (at least on the short-end.

Negative real mortgage rates and blistering home price growth?

Will the attendees at the KC Fed Jackson Hole conference discuss these matters? Or will it just be a Federal Reserve Soul Shake (dance)?

The minutes of the July Fed meeting suggest officials may signal an impending start to asset purchase tapering at the September gathering — provided jobs numbers remain on track in the interim — and make an announcement in November.

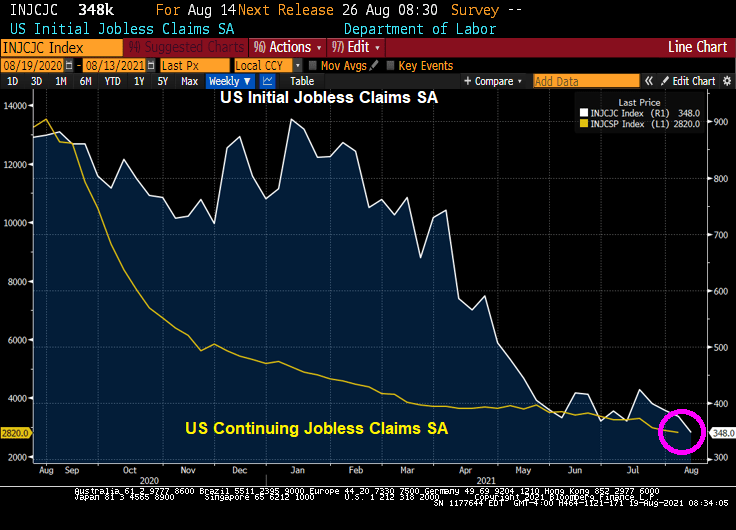

Rising infections counts have not spurred an uptick in new jobless claims. High-frequency data show some customers are shying away from eating out, but the overall impact on restaurant reservations is limited. The bigger challenge for many companies is retaining and hiring enough workers to meet strong demand, evident in low layoff counts and persistent mention of labor shortages.

In other words, IFF Covid doesn’t cause further economic damage (or governments don’t shut down economies), then The Fed will consider a mild taper of their balance sheet.

But as of this morning, The Fed’s reverse repo facility keeps on rising along with The Fed’s balance sheet. At least M2 Money Supply growth has leveled off.

That should result in an increase in Treasury yields and mortgage rates, all things being equal. And assuming the Biden Administration and governors don’t panic and go into economic lockdown … again.

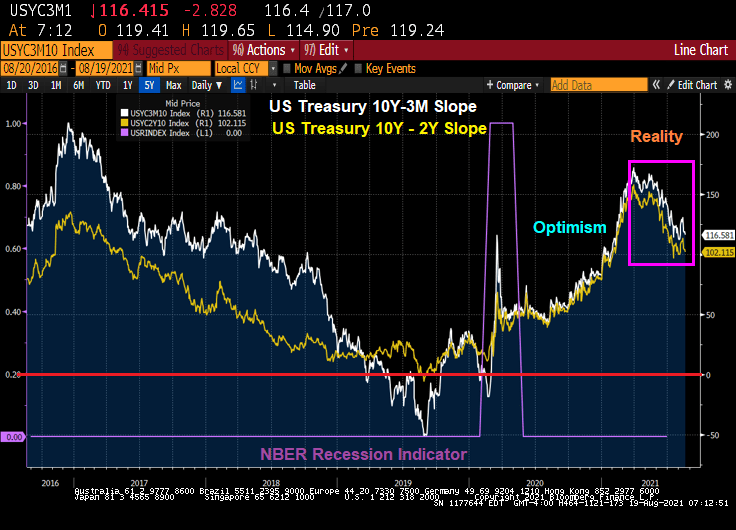

The US Treasury curves since the Covid recession of 2020 have shown optimism in recovery … then reality dawned.

Well, it looks like The Fed will start tapering after all.

Initial jobless claims fell again to 348K and continuing jobless claims fell to 2,820K.

Unless Biden’s disastrous Afghanistan withdrawal sends shock waves through the global economy (or Covid Delta/Lamba variant strains get worse and hurt the economy), we should see The Fed start tapering their balance sheet.

The 10Y Treasury yield rose slightly on the jobs report.

The Tapir, the symbolic mascot of The Fed’s tapering programs.

United Wholesale MortgageUWMC has announced plans to become the first national mortgage lender to accept cryptocurrency for home loans.

What Happened: CEO Mat Ishbia previewed the Pontiac, Michigan-based company’s expansion into the cryptocurrency realm during the second-quarter earnings call on Monday.

“We’ve evaluated the feasibility, and we’re looking forward to being the first mortgage company in America to accept cryptocurrency to satisfy mortgage payments,” Ishbia said. “That’s something that we’ve been working on, and we’re excited that hopefully, in Q3, we can actually execute on that before anyone in the country because we are a leader in technology and innovation.”

In an interview with the Detroit Free Press, Ishbia offered more details on which cryptocurrencies would be considered in transactions.

“I think we’re starting with Bitcoin, but we’re looking at Ethereum and others,” Ishbia said. “We’re going to walk before we run, but at the same time, we are definitely a leader in technology and innovation and we are always trying to be the best and the leader in everything we do.

“That’s the plan,” he added. “Obviously there’s no guarantees – we’re still working through some details. But absolutely.”

Why It Matters: One of the first homebuying deals in the U.S. involving cryptocurrency took place in 2014 with the $1.6 million sale of land in Lake Tahoe for a home site. The transaction was completed with payment via Bitcoin (CRYPTO: BTC).

However, the heavily regulated and risk-averse mortgage industry hasn’t embraced cryptocurrency. The government-sponsored enterprises that dominate the industry’s secondary market, Fannie MaeFNMA+ Free Alerts and Freddie MacFMCC+ Free Alerts, will not accept any transaction in a digital asset.

If UMC plans to package its cryptocurrency-based loans for secondary market sale, the borrower’s cryptocurrency payment would have to be converted into dollars and the borrower would need to provide documentation to verify ownership of the digital assets as part of the loan underwriting process.

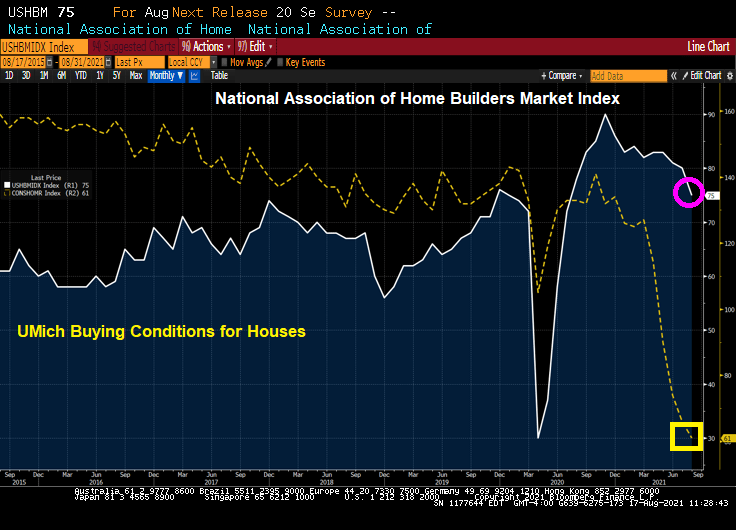

Of course, then we have the University of Michigan conditions for buying a home crashing as well.

Rising home prices and rising construction material costs? Yikes.

Of course, the NAHB had this to say:

“Our expectation is that production bottlenecks should ease over the coming months and the market should return to more normal conditions,” NAHB Chief Economist Robert Dietz said in a statement.

Perhaps, but The Fed needs to slow down its money printing as well.

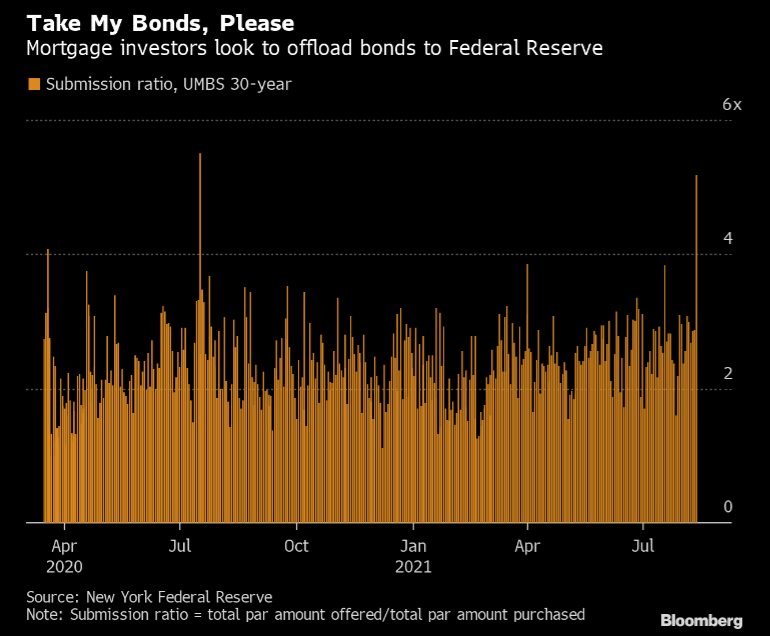

(Bloomberg) — Last week was notable for the tsunami of agency mortgage bonds offered to the Federal Reserve during its routine purchase operations on Friday.

The central bank’s quantitative easing schedule called for it to buy $2.9 billion of 30-year uniform mortgage bonds Friday, and that was nothing outside of its usual pattern. However, mortgage investors flooded the Fed with $15.06 billion of bonds for sale, the largest daily amount offered during a single operation since April 1, 2020.

In terms of how that compares to the total amount purchased, investors offered 5.2 times as much as were eventually taken down by the central bank. That is well above the 2.3 times average for 30-year uniform mortgage bond operations seen during all of this round of quantitative easing, and the second-highest overall. The highest submission ratio was the 5.5 times seen on July 16, 2020.

There are a number of reasons this could have happened. Investors may have wished to lighten their positions before the summer doldrums of late August, when many desks are lightly staffed due to vacations. Also, tight sector valuations or concerns about a sooner-than-expected taper may have played a part.

While this may simply be a one-off event and no reason for concern, it is certainly something to keep an eye on in case it heralds a change in investor sentiment.

In related news, the Treasury’s overnight reverse repos purchases remain about $1 trillion.

You must be logged in to post a comment.