The Biden Administration and The Federal Reserve together should be called “The Cooler Kings” in that their policies are putting a Big Chill on the mortgage market and equities.

Mortgage rates are skyrocketing thanks to the Federal Reserve.

The 30-year fixed-rate mortgage averaged 5.27% for the week ending May 5, according to data released by Freddie Mac FMCC, -1.62% on Thursday. That’s up 17 basis points from the previous week — one basis point is equal to one hundredth of a percentage point, or 1% of 1%.

House price growth to wage growth is below the all-time high, but remains above housing bubble levels of 2005-2007.

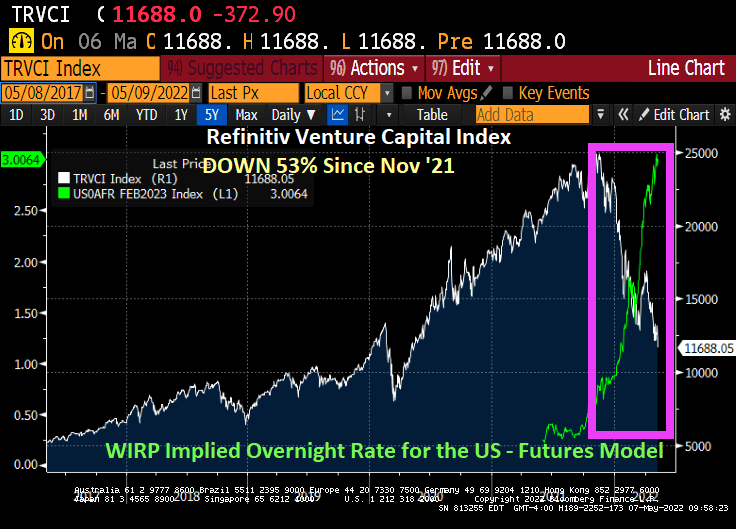

The Refinitiv Venture Capital Index is down 53% since November ’21 as The Fed cranks up interest rates.

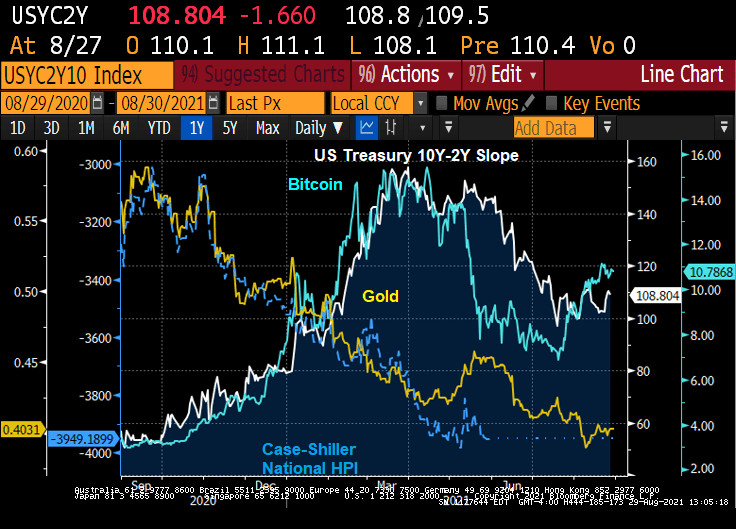

Well, at least commodities are soaring under “The Cooler Kings.” Pretty much everything else is sucking wind.

Home prices are actually falling in some cities, like Toledo Ohio, Detroit Michigan, Rochester NY, and Pittsburgh PA. Even La-La Land (Los Angeles CA) is seeing a drop in median listing price since 2021 of -5.0%.

The question, of course, is whether The Federal Reserve will back off its plans to aggressively raise interest rates in lieu of crashing stock market, venture capital, and possibly home prices.

This is Scorcher VI: Global Meltdown.

You must be logged in to post a comment.