The U.S. merchandise-trade deficit unexpectedly widened in January to an all-time high, reflecting a record value of imports and a drop in shipments overseas.

The shortfall grew to $107.6 billion last month from $100.5 billion in December, according to Commerce Department data released Monday.

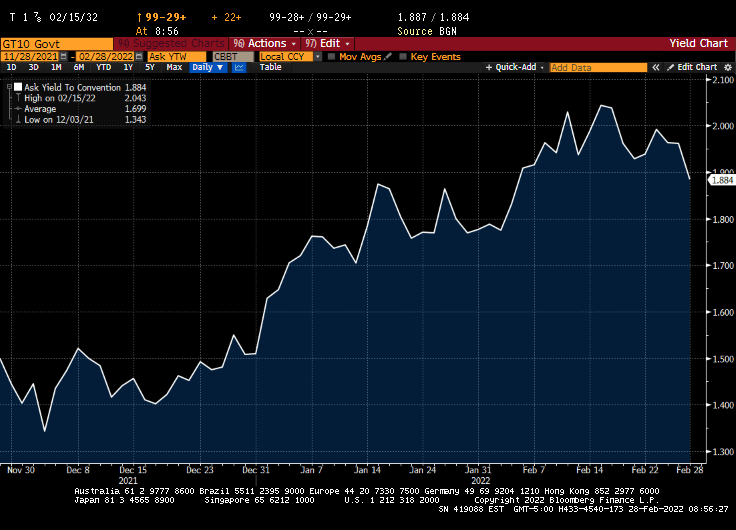

Meanwhile, the US Treasury 10Y yield fell to 1.884%.

The cost for shipping from the US to China has surged.

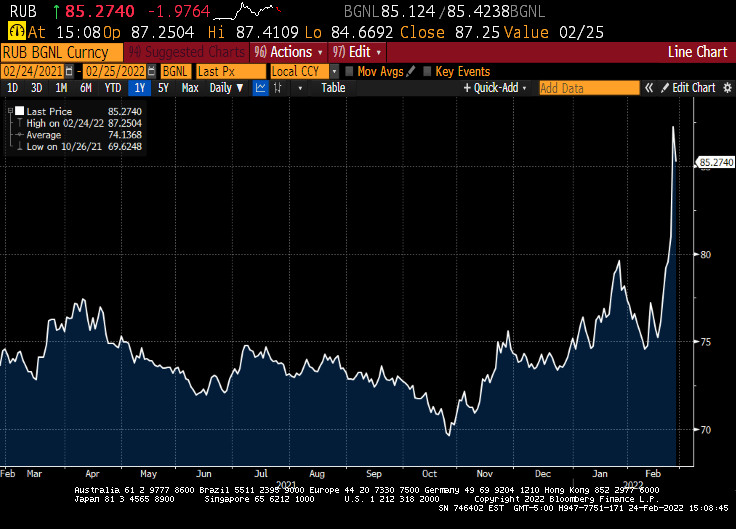

Meanwhile, the Russian Ruble is getting clobbered.

At least Putin hasn’t put himself on Russian currency … yet. Or nyet.

Russia is still attacking Ukraine and I am still seeing stories about actor/comedian Bob Saget’s cause of death. So now for something completely different.

And this doesn’t include the inflation in prices caused by the Russian invasion of Ukraine. Yet.

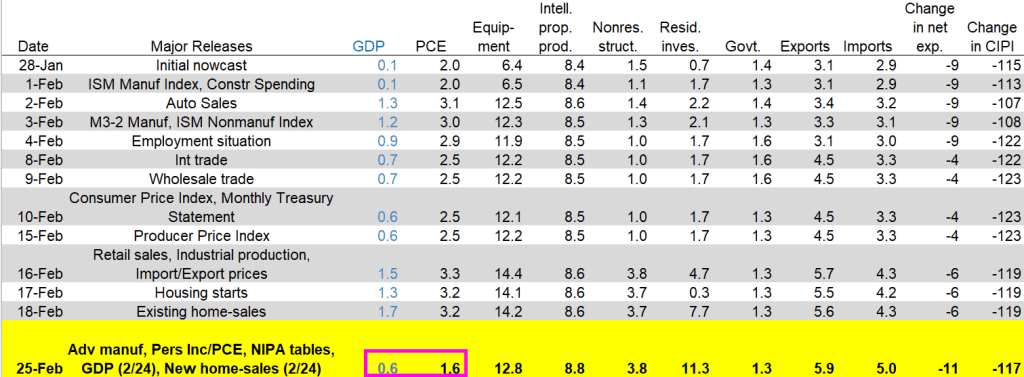

US Personal Consumption Expenditures (PCE) price index rose by 5.2% in January, the fastest rate since mid-1983.

With CPI inflation at 7.5% YoY, the Taylor Rule suggests a Fed Funds target rate of 13.35%, higher than the current rate of 0.25%. Overstimulated much??

We now know that Russia has invaded Ukraine and President Biden really threw the booklet at Putin in a speech today. Rather than removing Russia from the SWIFT banking system which would have really hurt Russia’s trade with Europe, he gave a surprisingly cogent speech about the US and NATO agreeing to do … not much. He did warn us that energy prices would rise (which he helped do when he took office) and told energy companies not to gauge consumers.

The reaction in Russia? Their stock market tanked over 30% (not because of Biden’s speech, but because of negative costs of war).

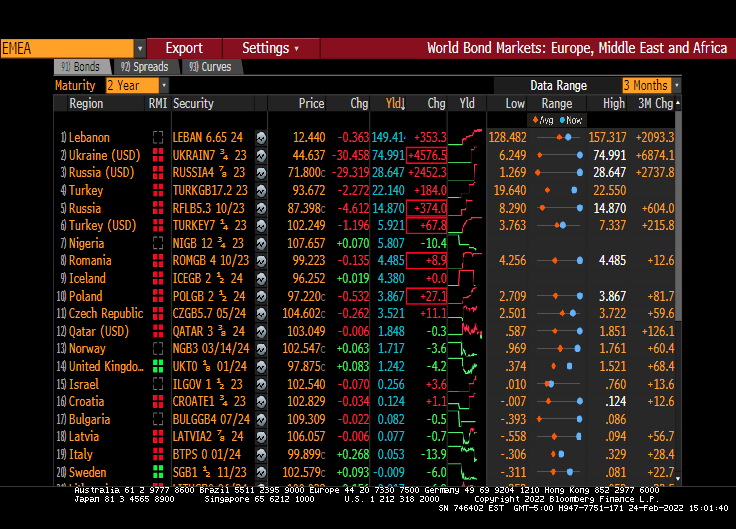

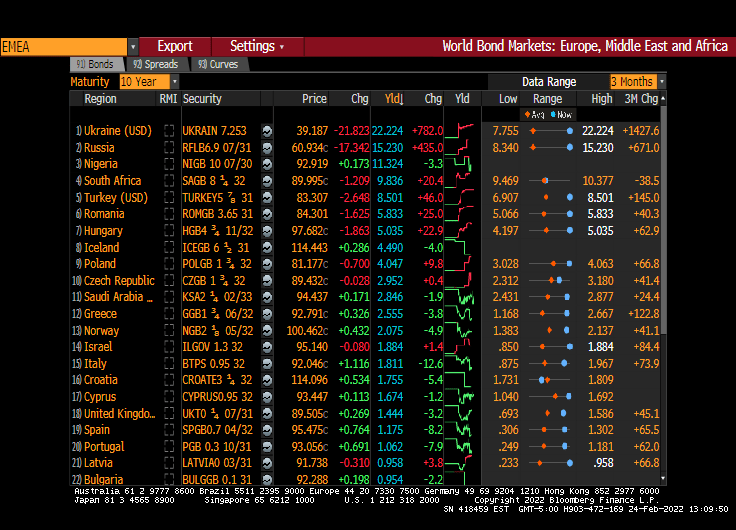

Russia’s 10-year sovereign yield rose to 15.23%.

The Russian Ruble crashed and burned.

UK natural gas prices rose 51% today.

And while 17 Euro nations have negative 2 year sovereign yields, Russia has 2-year sovereign yield of 28.65% which is nothing compared to Ukraine’s 75% 2-year yield (in US Dollars).

The SWIFT system, or Society for Worldwide Interbank Financial Telecommunication, facilitates financial transactions and money transfers for banks located around the world. The system is overseen by the National Bank of Belgium and enables transactions between more than 11,000 financial institutions in more than 200 countries around the world. Removing Russia from the SWIFT system would really hurt Russian trade with Europe. I assume that Europe is scared of soaring energy costs, so probably doesn’t want Russia removed from SWIFT.

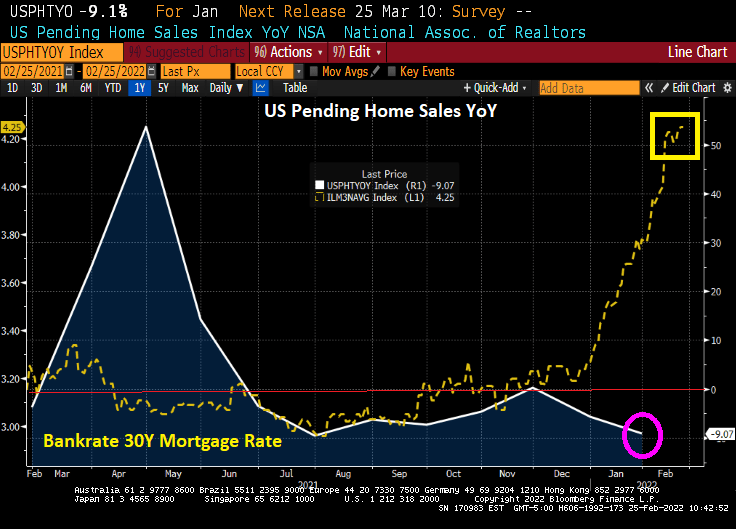

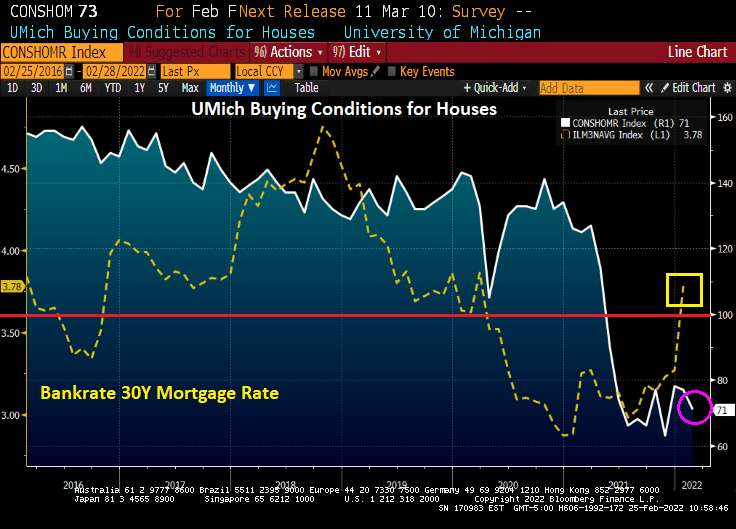

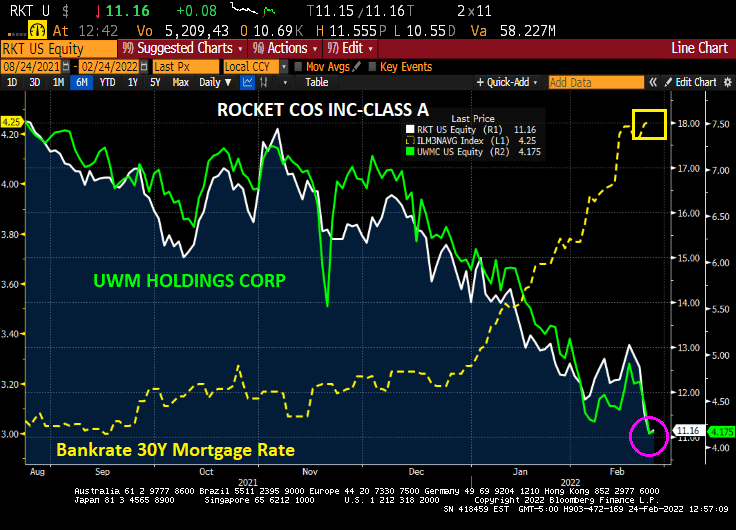

As The Federal Reserve threatens to tighten monetary policy, 30-year mortgage rates have risen to 4.25% leading two major mortgage companies, Rocket Mortgage and United Wholesale Mortgage, to decline to all-time lows.

But wait, Federal Reserve officials signaled they remain on track to raise interest rates next month despite uncertainty posed to the global economy by Russia’s invasion of Ukraine.

While acknowledging the risks created by the conflict, which has triggered one of the worst security crises in Europe since World War II and caused oil prices to surge, U.S. central bankers stressed the need to confront the hottest U.S. inflation in 40 years.

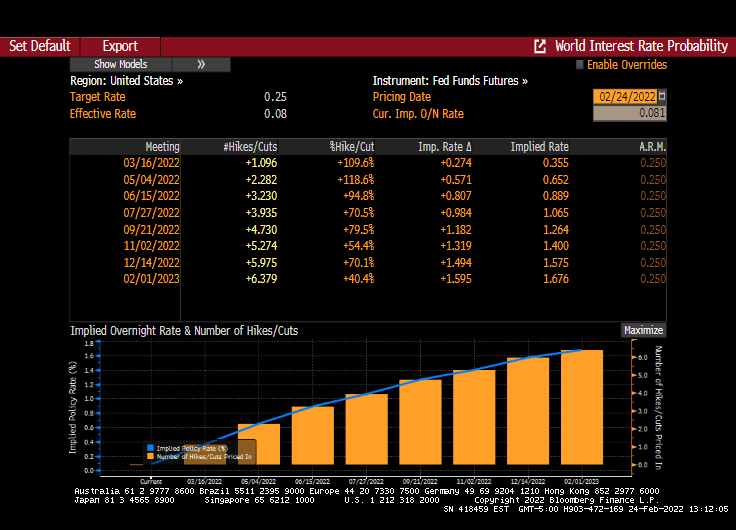

So, The Fed plans to raise rates to fight inflation, even if it tanks the housing and mortgage markets? Fed Funds Futures are still signaling 6 rate hikes over the next year.

At least US Treasury 10Y yields are down just 7.6 bps. Look at 10Y Russian and Ukraine sovereign yields. Now THAT is a yield surge!

I admit, I follow market data to get a signal of what is happening to mortgage rates and I got one. With Putin and Russia invading Ukraine, markets are in turmoil

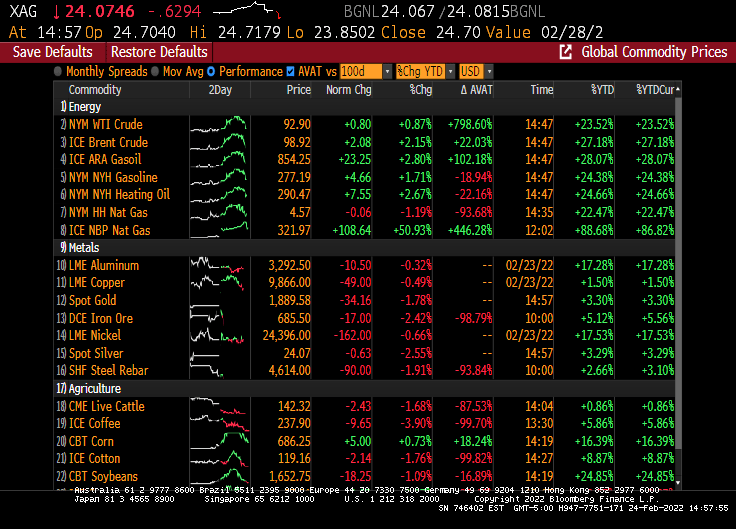

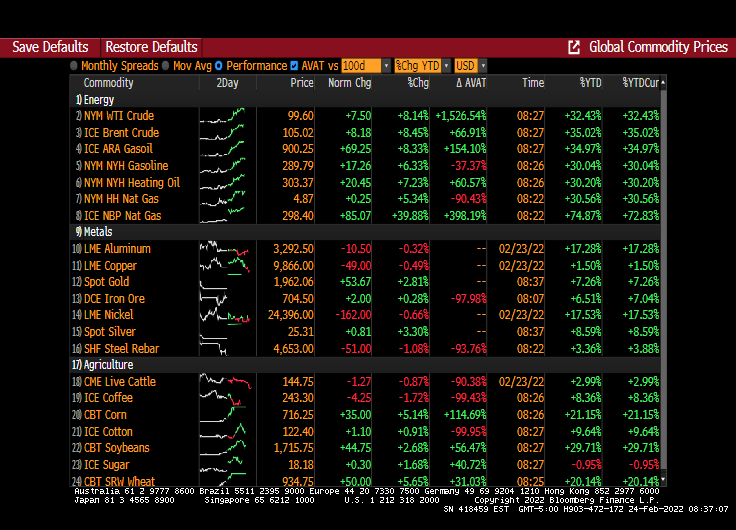

WTI Crude is up 8.14% this morning, Brent Crude is up 8.45% and NBP (UK) Natural gas is up 40%.

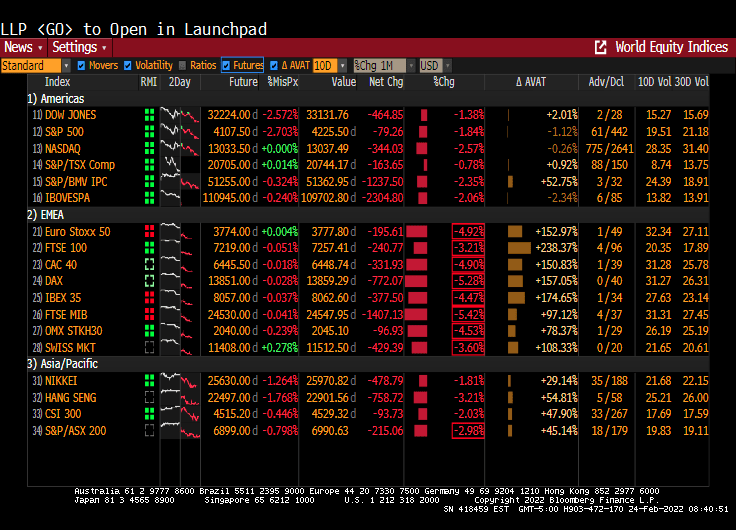

Europe is having a bad day equity market-wise. Eurostoxx 50 was down 4.92%. The US Dow is braced for a 2.5% opening.

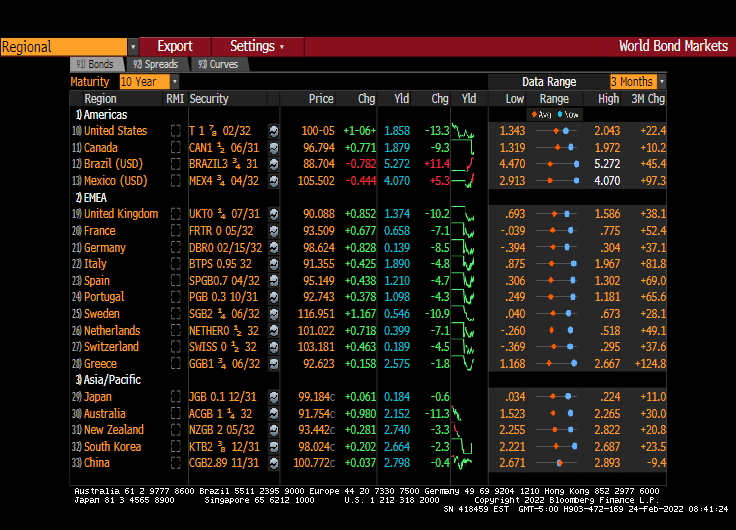

Now to bonds. The 10-year Treasury yield is down 13.3 bps this morning. Sweden and UK are down 10 bps as well.

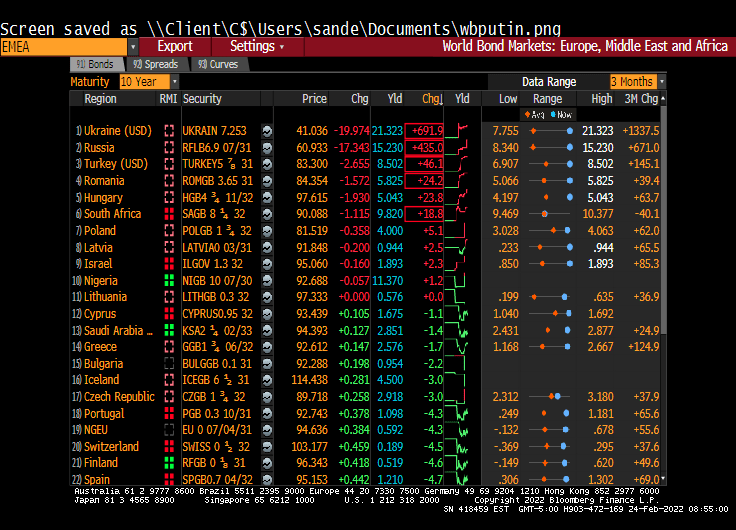

How about the new Russian front? Ukraine’s 10y yield rose 691.0 bps while Russia’s 10Y yield rose 435 bps.

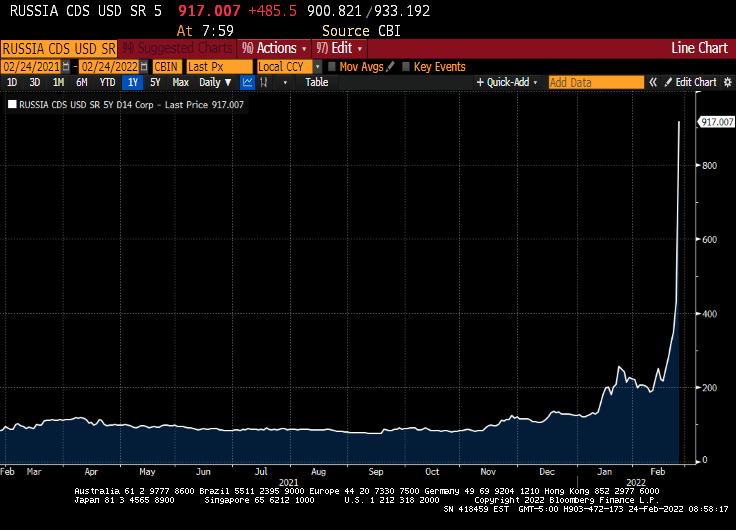

Russian 5Y Credit Default Swaps (CDS) leaped to a Greek-like 917.

Well, it looks like the sanctions imposed by Winken (US VP Harris), Blinken (US Secretary of State) and Nod (US President Biden because he always looks half-asleep) apparently didn’t work as intended.

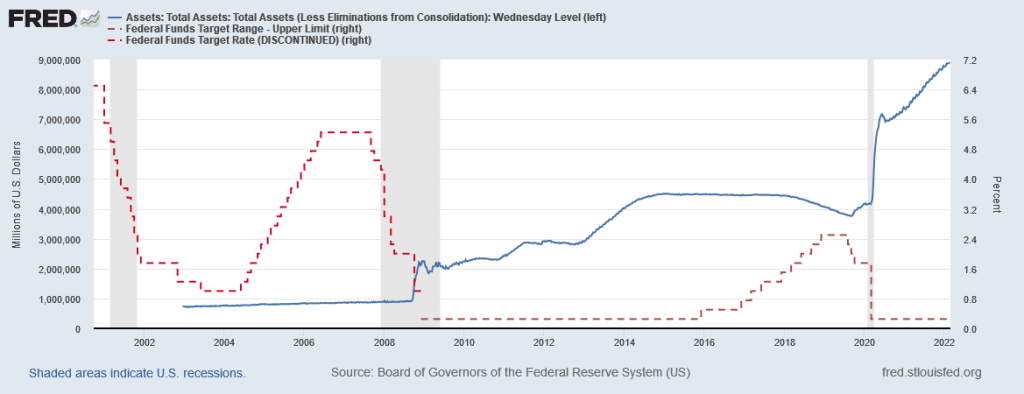

It has been almost 14 years since The Federal Reserve under Ben Bernanke unleashed zero interest rate policies (ZIRP) and quantitative easing (QE) in late 2008. And Fed monetary stimulypto is still running strong after almost 14 year of monetary mismanagement and asset bubble stimulation.

The Federal Reserve under Bernanke and Yellen raised their target rate exactly once under President Obama before the election of Donald Trump. After Trump was elected, The Fed raised their target rate 8 times, lowered it 5 times. There have been no rate hikes under Biden.

There seemingly never-ending Fed monetary stimulus has resulted in the top 1% seeing their share of total net worth soar relative to the share of net worth of the bottom 50%. But note that starting in 2014 just as The Fed was engaged in QE 3. But the real divergence occurred after The Federal government heaped trillions in fiscal stimulus on top of the skyrocketing monetary stimulus.

In terms of income inequality (as measured by the GINI coefficient), it just keeps getting worse and worse.

Let’s see if The Fed actually delivers by reducing their monetary stimulypto.

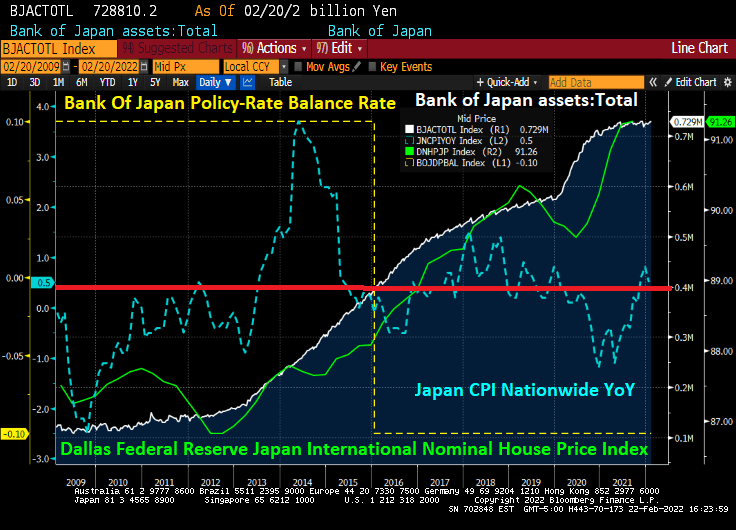

It’s taken nine years and the Bank of Japan supersizing its balance sheet to the $5 trillion mark, but Asia’s second-biggest economy finally has some inflation.

Officials in Tokyo are realizing the hard way, though, that it’s best to be careful what you wish for as bond yields spike.

Granted, the gains in consumer prices Japan is reporting are negligible compared to those in the U.S. and China. And inflation is still a good distance from the BOJ’s 2% target. Still, the 0.5% rise in consumer prices in January year-on-year is already unnerving the bond market. It followed a 0.8% jump in December and marks the fifth straight month of increases.

The worry is that Japan’s inflationis the “bad” kind. Haruhiko Kuroda was hired as BOJ governor in March 2013 to end deflation. Kuroda unleashed tidal waves of liquidity. That drove the yen down 30%, generated record corporate profits and sent Nikkei 225 Average stocks to 31-year highs.

Despite a staggering balance sheet with a -0.10 bps policy rate, Japan has only 0.5% inflation.

And Japan’s yield curve is negative at 3 year tenor and less.

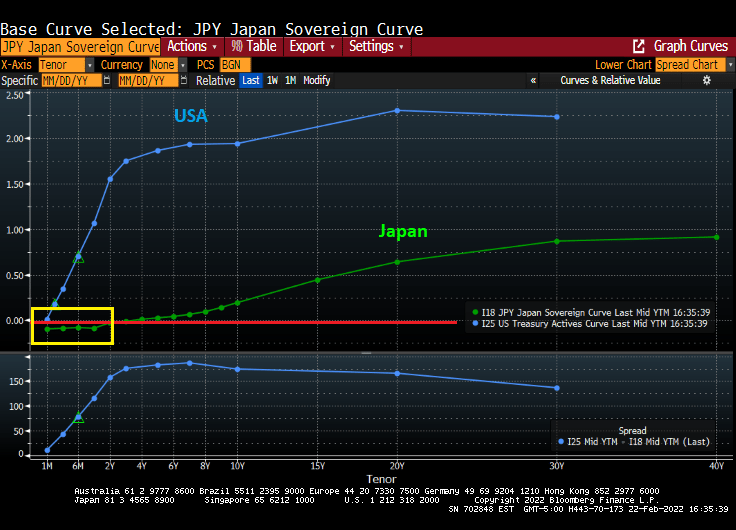

How is it that Japan has virtually no inflation with negative rates but the USA has 7.5% inflation with a 0.25% target rate? Could it be the USA undertook massive fiscal spending related to COVID and reduced energy sources in an effort to go “green” that led to 7.5% inflation??

As US/Russian tensions grow over Ukraine, The Federal Reserve may be forced to postpone or reduce planned rate increases and balance sheet trimming.

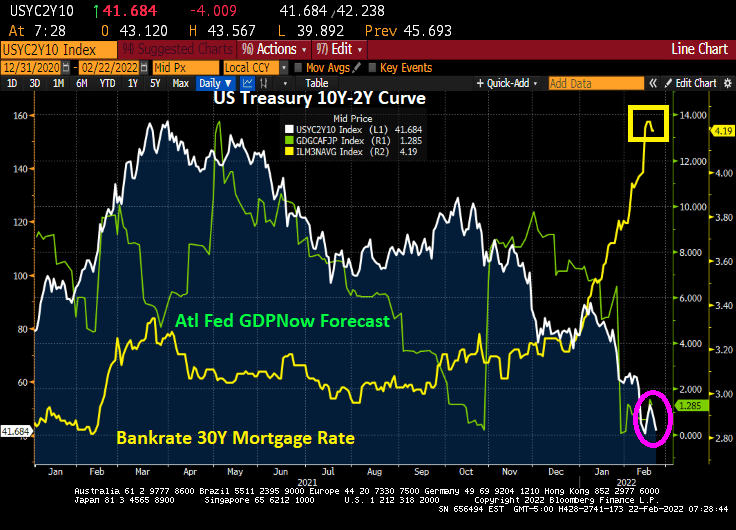

But in addition, we see US GDP slowing to near zero (1.285%) as the US Treasury 10Y-2Y yield curve has flattened to 41.684 BPS. The good news? Bankrate’s 30Y mortgage rate increases have slowed to 4.19%.

On a different note, I noticed the Chicago Bulls logo when turned upside-down looks like a space alien violating a crab.

You must be logged in to post a comment.