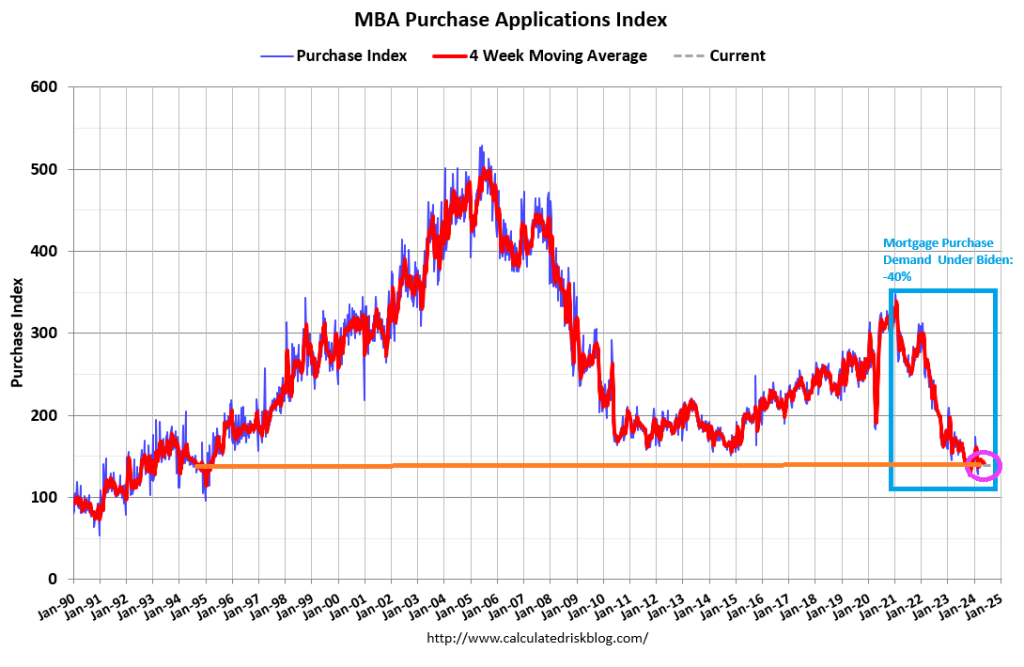

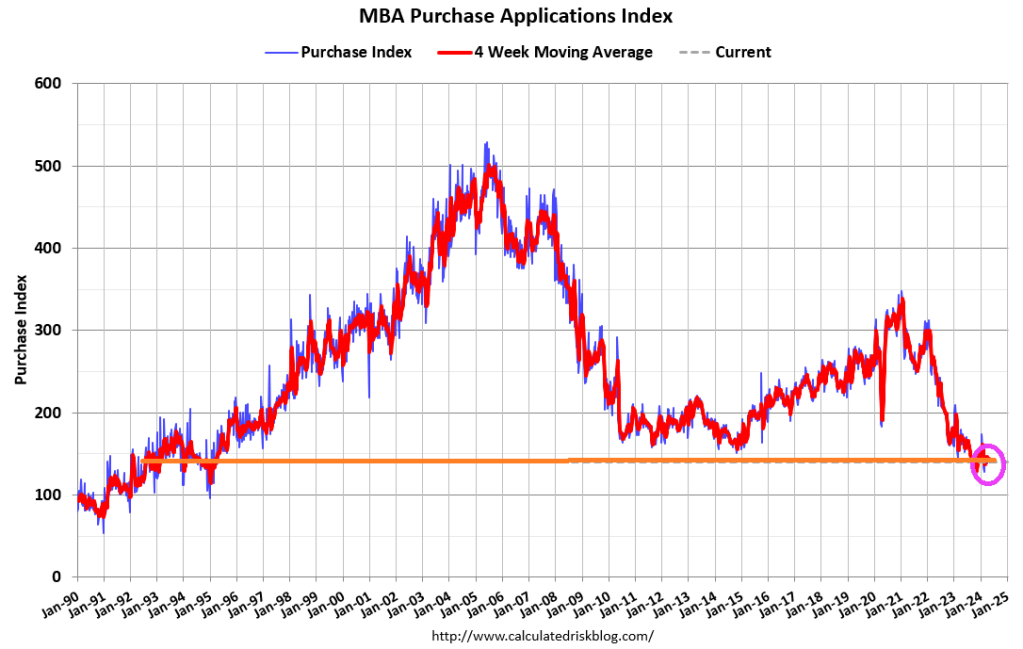

The Market Composite Index, a measure of mortgage loan application volume, decreased 5.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 6.3 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 10 percent lower than the same week one year ago. And -40% under Biden.

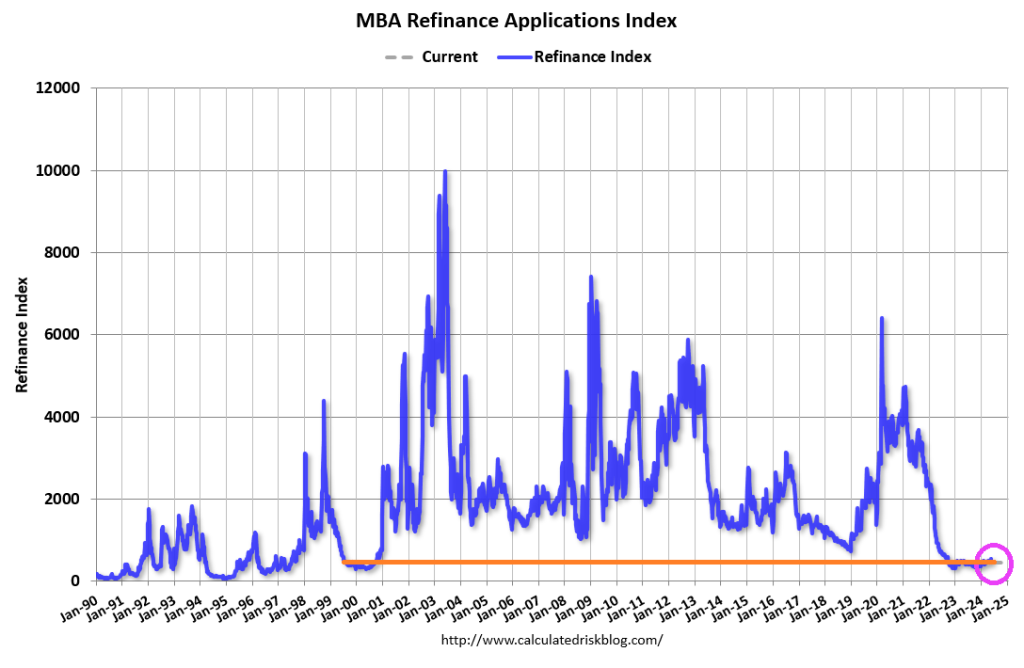

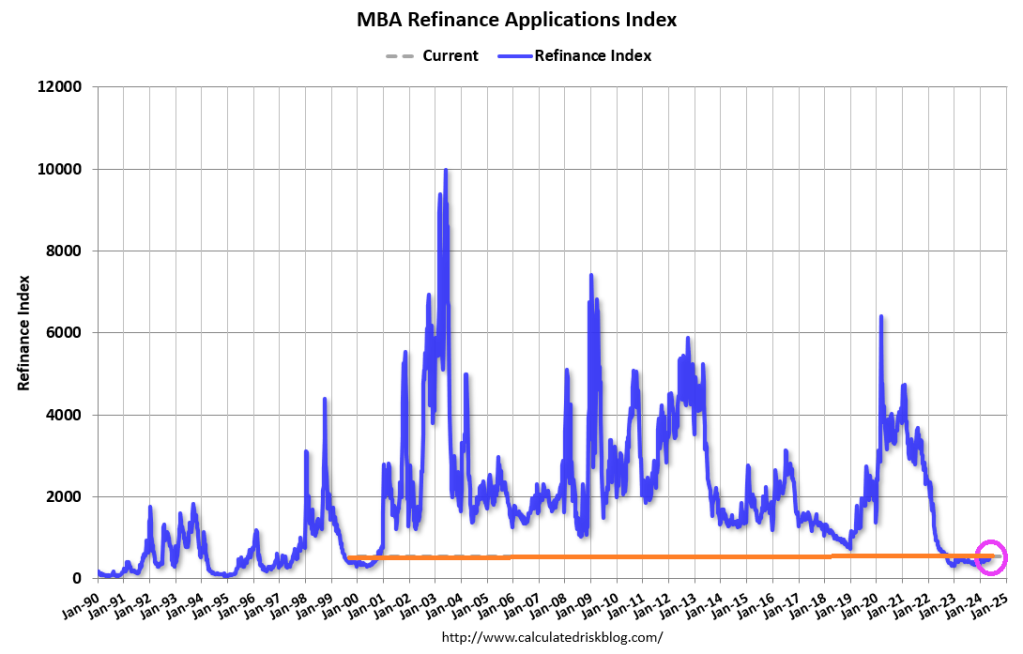

The Refinance Index decreased 14 percent from the previous week and was 12 percent higher than the same week one year ago.

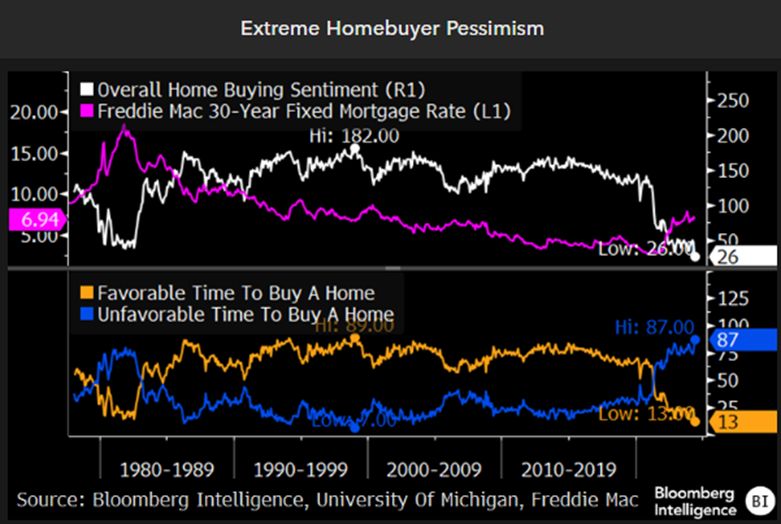

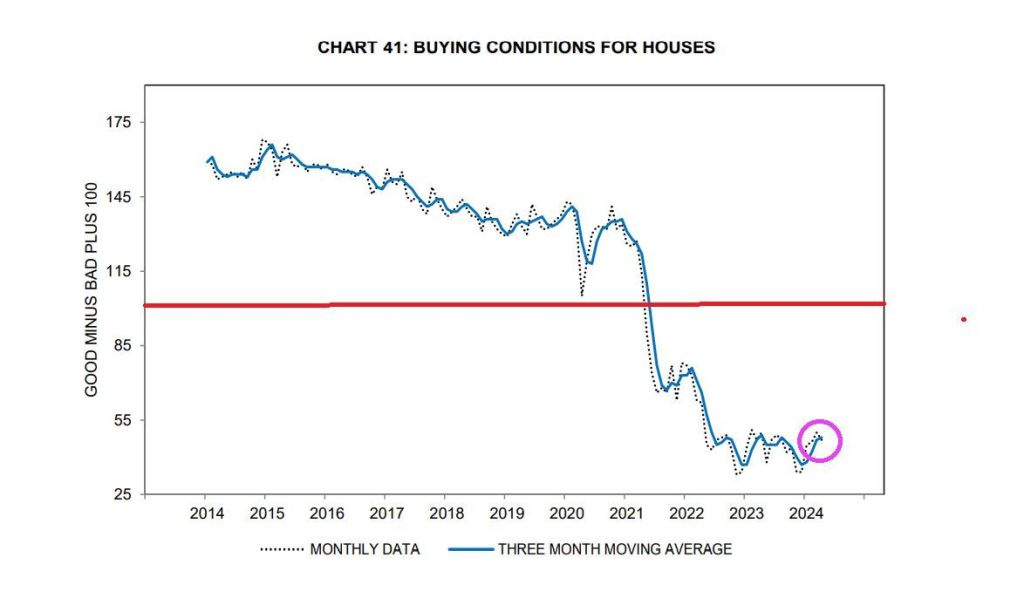

It is still an unfavorable time to buy a home!

From the film “Ronin” that sums up actor Robert DeNiro in one sentence.

Spence (Sean Bean): “You know, you think too hard.” Sam (Robert DeNiro): “Nobody ever told me that before.”

How would DeNiro consider the 40% drop in mortgage purchase demand under Biden?

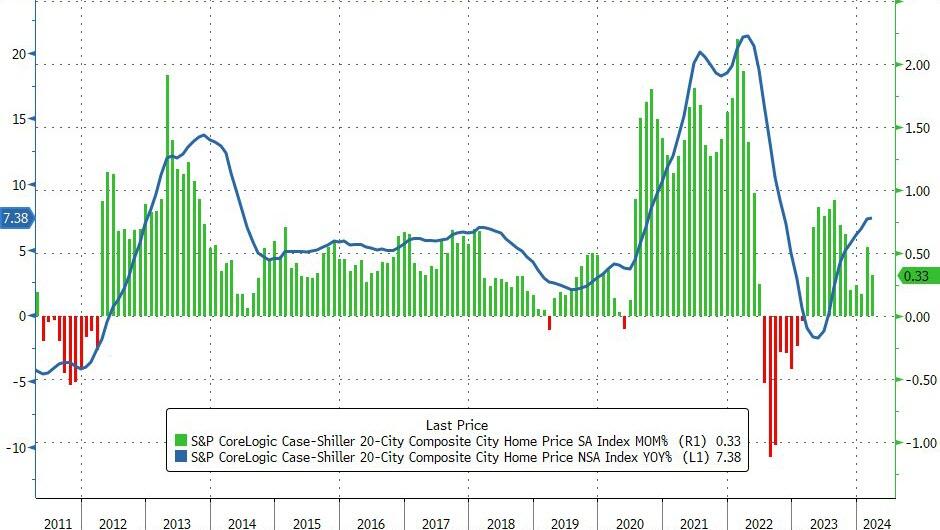

This pushed the price up 7.38% YoY – the fastest rise since October 2022…

“We’ve witnessed records repeatedly break in both stock and housing markets over the past year. Our National Index has reached new highs in six of the last 12 months.” says Brian D. Luke, Head of Commodities, Real & Digital Assets at S&P Dow Jones Indices.

Overall, US home prices reached a new record high in March (as median new home prices began to fall)…

Source: Bloomberg

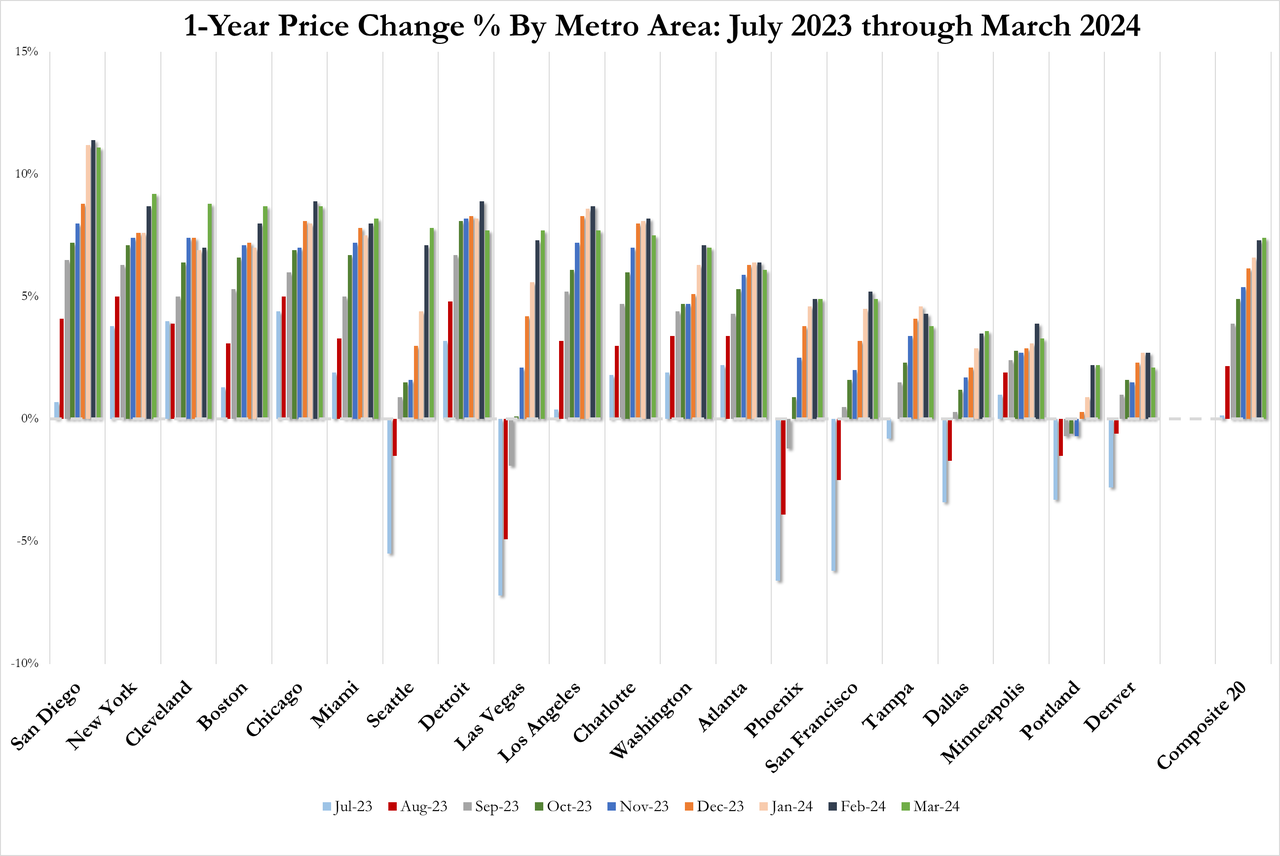

San Diego continued to report the highest year-over-year gain among the 20 cities this month with an 11.1% increase in March, followed by New York and Cleveland, with increases of 9.2% and 8.8%, respectively.

Portland, which still holds the lowest rank after reporting three consecutive months of the smallest year-over-year growth, posted the same 2.2% annual increase in March as the previous month.

Luke suggested this implies “a strong demand for urban markets.”

No city has seen a MoM decline in price in 2024.

Home prices continue to track Fed Reserves closely, but a turning point may come soon…

Source: Bloomberg

Given the smoothing and heavy lag in the Case-Shiller data, it’s hard to find a causal relationship between prices and mortgage rates…

Source: Bloomberg

…but with rates remaining above 7%, it seems hard to believe prices can continue their advance.

Who the heck is HUD Secretary? It was Cleveland’s Marcia Fudge (a typical Biden political appointment). Now it is Adrianne Todman, from the US Virgin Islands and former executive director of the District of Columbia Housing Authority. Not exactly a high-powered resume for a cabinet post, Joe!

I saw former President Obama criticizing former President Trump for not passing “transformative” changes. That is, Trump didn’t sign any Obama-like transformative changes (like Obamacare). Truimp did try to slow down the damage done by Obama and his transformative agenda (e.g., open borders, wealth redistritution, green energy) that Biden has attempted to continue.

As we approach the party conventions and Presidential election of 2024, we saw the Economic Surprise Index (ESI) in May decline to -0.126.

Coupled with Biden’s negative buying conditions for housing (higher mortgage rates and soaring house prices), Obama’s Jacobian transformative economic fantasty is on thin ice.

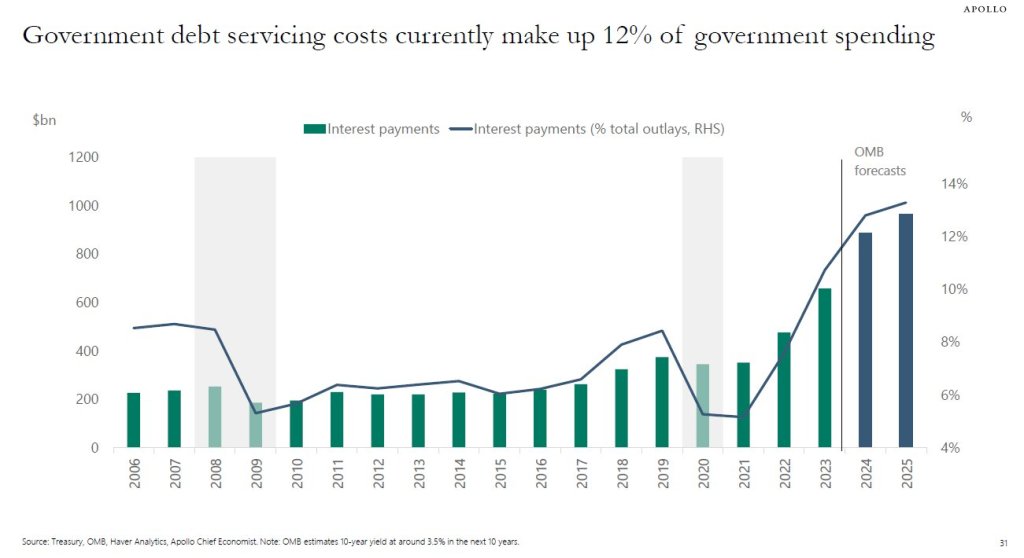

Speaking of higher interest rates, US debt servicing costs currently make up 12% of government spending. Jacobin revolution = Cloward-Piven.

Let’s hope the Obama/Biden Jacobin revolution doesn’t get to this point!

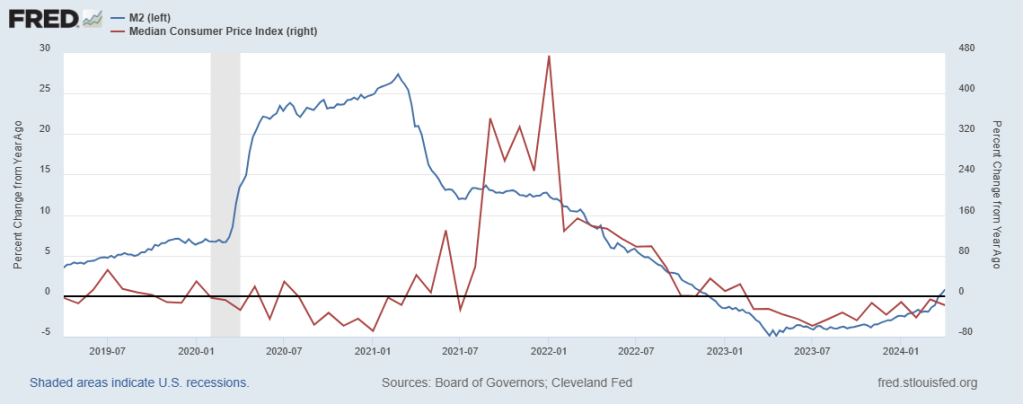

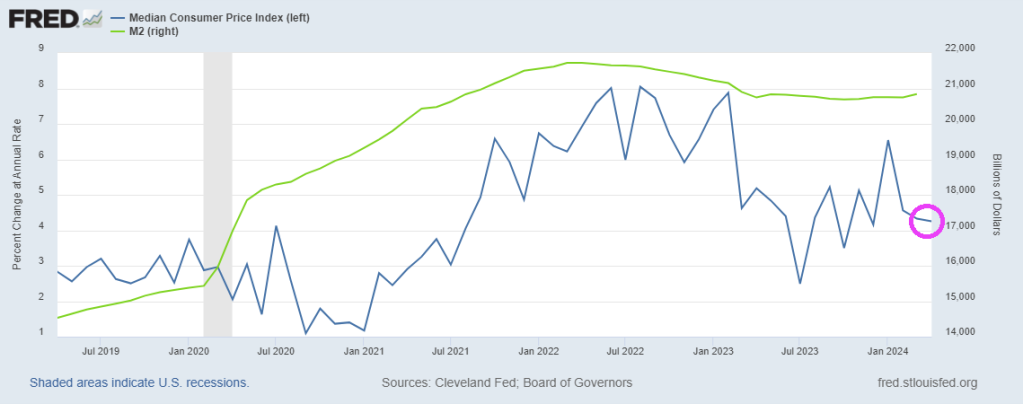

The various talking heads from The Federal Reserve keep jawboning about whether to raise rates or not. One of the major drivers of inflation is … money. M2 Money growth YoY is growing again (blue line)! And with it, inflation has been rekindled.

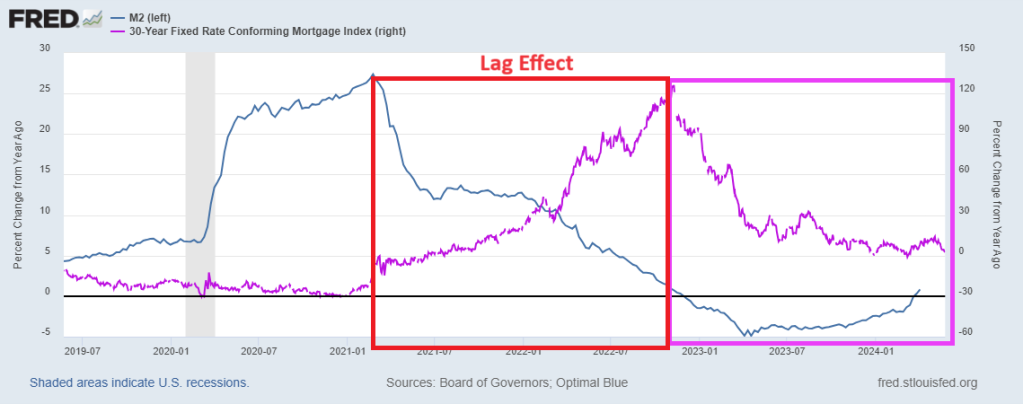

Mortgage rates? There is a lag between M2 Money printing and conforming mortgage rate growth.

Mortgage applications increased 1.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 17, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 1.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 1.1 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 11 percent lower than the same week one year ago.

The 30-year fixed mortgage rate declined for the third straight week, dropping to 7.01 percent – the lowest level in seven weeks. Thus, the Refinance Index increased 7 percent from the previous week and was 21 percent higher than the same week one year ago.

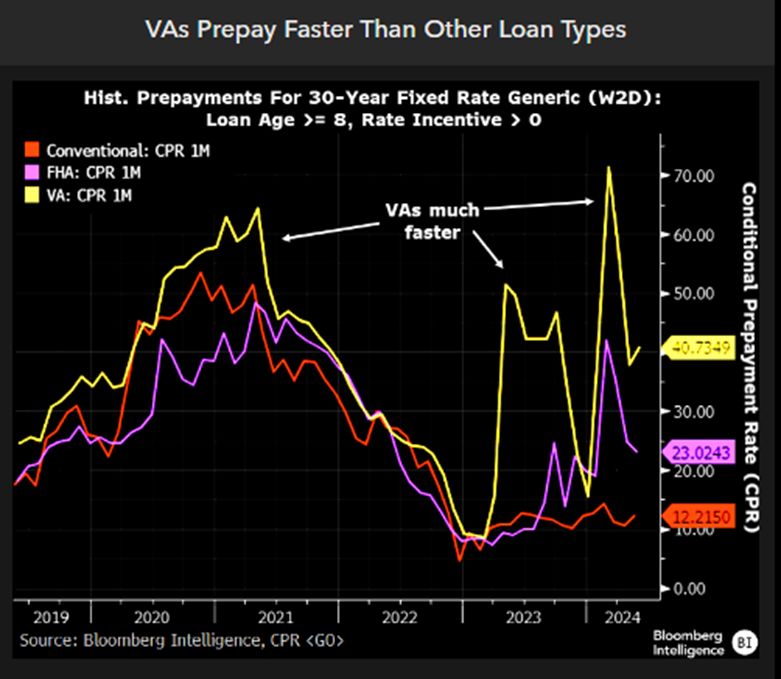

VA-insured mortgages prepay the fastest, followed by FHA-insured mortgages then conventional mortgages.

I know a place where the housing market is hot! Florida and Texas!

I learn something new everyday. Like Biden yesterday claimed has was VP during Covid (uhm, Covid was in 2020 and Biden left the office of VP in 2017). But nothing gets in the way of Biden and a good story! Like his whopper that he inherited 9% inflation from Trump (even CNN fact-checked this whopper and found it was false. It was only 1.4%!)

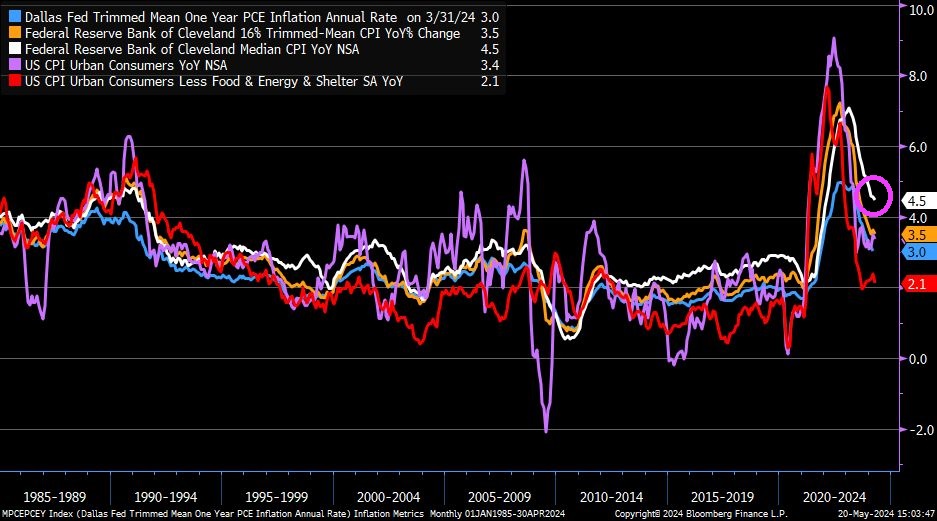

But inflation is still at 4.5%, according to the Cleveland Federal Reserve.

Now, there are many measures of inflation to choose from, from Core CPI of 2.1% YoY to Cleveland Fed’s Median CPI of 4.5%.

The US is on a “Highway to Hell!” thanks to flawed economic policies under Biden.

First, interest and mortgage rates under Biden have soared driving buying conditions for housing to all-time lows. Combine sky-high home prices with high mortgage rates and we have as serious affordability crisis.

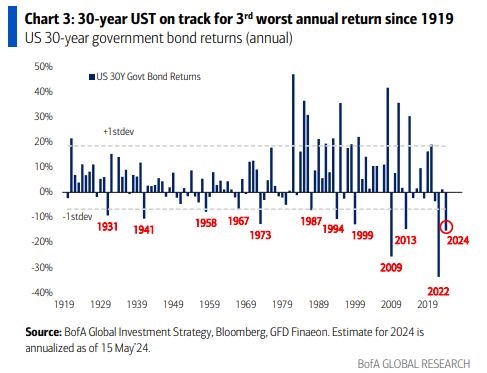

Second, on the interest rate front, the 30-year Treasury bond is on track for the 3rd worst annual return since 1919 and Russia’s invasion of Ukraine. Not not the current invasion, but the 1919 invasion.

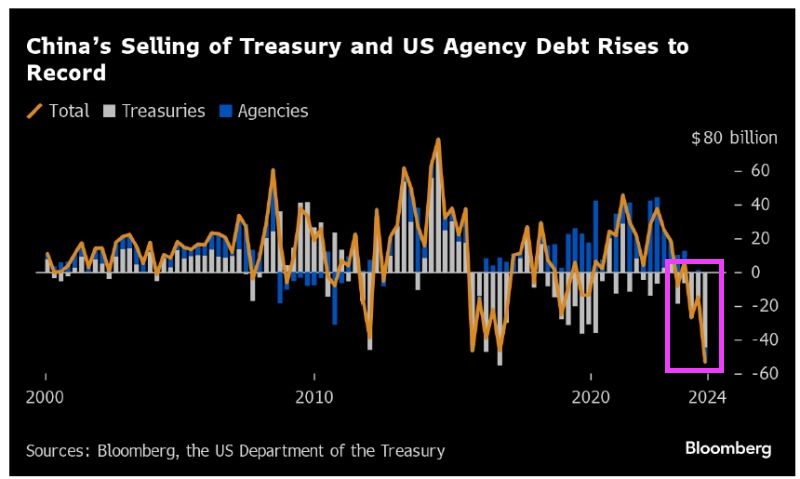

Third, China is dumping their holdings of US Treasuries and Agency Debt at record rates.

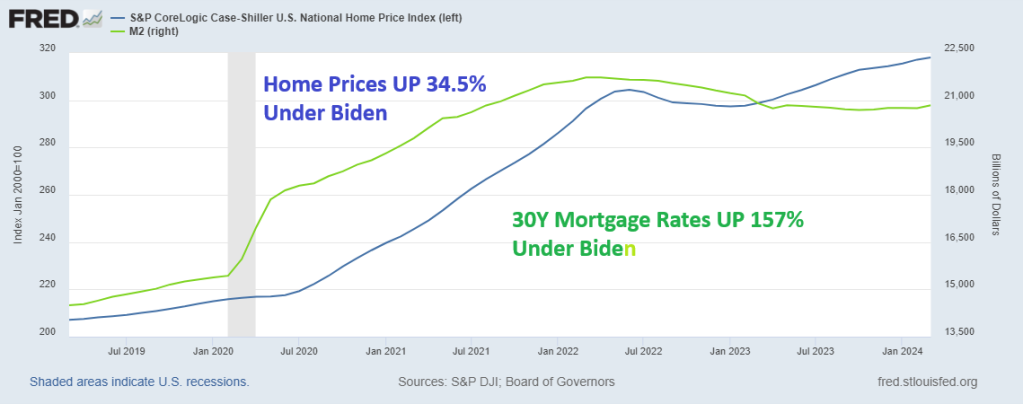

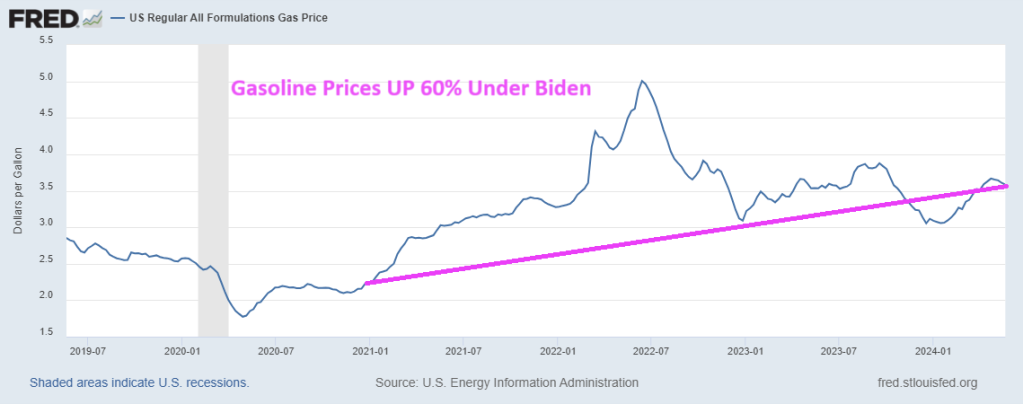

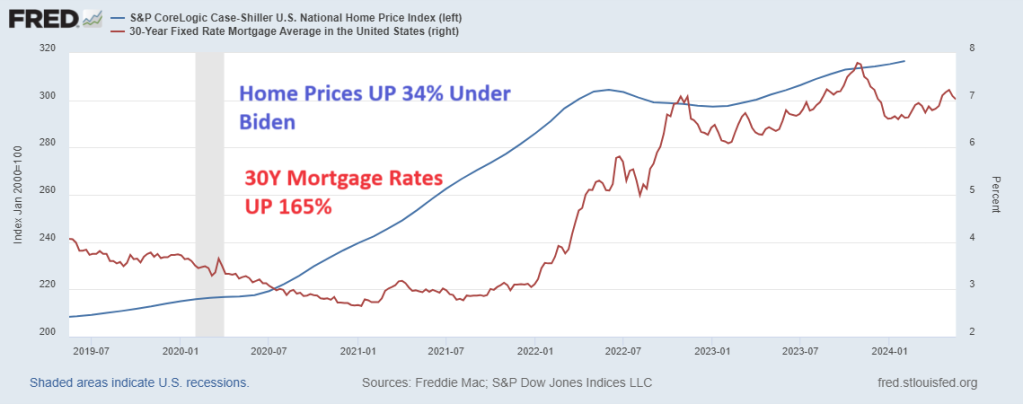

Of course, mortgage rates hit 18% in 1981. So, the term high mortgage rates is relative. The US had low rates for too long (Bernanke/Yellen) and mortgage rates are now in the 7% range, up 165% under Biden. And home prices are up 34% since Biden was sworn-in as President. Wow! Mortgage rates up 165% and home prices up 34% under Biden’s Reign of Error.

The US middle class and low-wage workers are back on the chain gang while the top 1% party hearty.

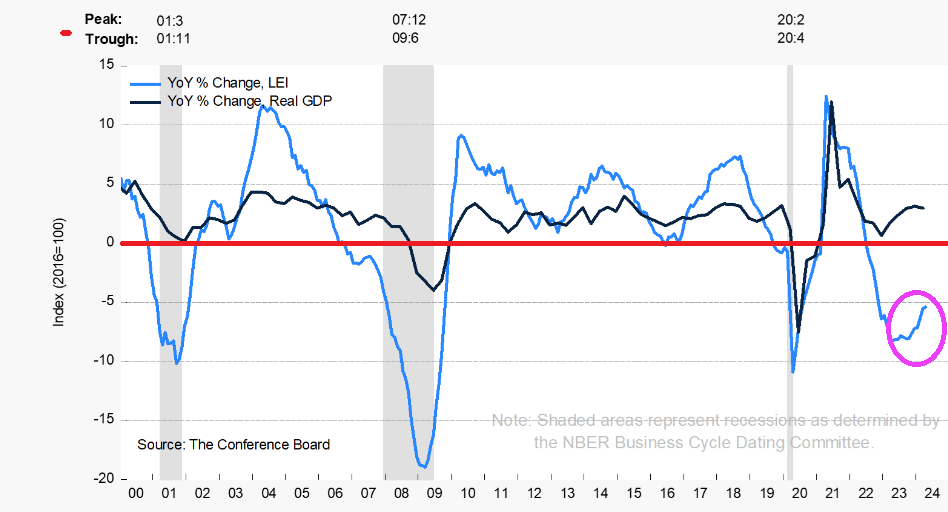

The Conference Board Leading Economic Index® (LEI) for the U.S. decreased by 0.6 percent in April 2024 to 101.8 (2016=100), after decreasing by 0.3 percent in March. Over the six-month period between October 2023 and April 2024, the LEI contracted by 1.9 percent—a smaller decrease than its 3.5 percent decline over the previous six months.

It is surprising that Americans trusts the millionaires in the Administration (like Biden) or Congress (like Schumer, McConnell, etc) to have our backs on the roaring inflation rate. At least Speaker Mike Johnson isn’t a millionaire … yet. But that might explain his selling out conservatives.

Bloomberg reports that PBoC Deputy Governor Tao Ling announced the new 300 billion yuan ($41.5 billion) nationwide program of cheap funding to allow state-owned companies to purchase unsold homes.

Ling said the funding will be directed at 21 providers, including policy banks, state-owned commercial lenders, and joint-stock banks. A rate of 1.75% will be offered. The low-cost loans have a one-year term and can be rolled over four times.

The new program powerfully signals that policymakers are pushing for property policy easing and measures to balance the supply-heavy housing market, which casts a dark cloud over the world’s second-largest economy. This announcement appears to be a step in the right direction in a national-level policy.

Also, on Friday, policymakers eased mortgage rules and removed the mortgage rate floors for first and second homes. PBoC also lowered the minimum downpayment ratio for first-time homebuyers to 15%. The downpayment ratio for second-home purchases was lowered to 25%.

Chinese Vice Premier He Lifeng said that authorities in cities with excess home inventories should purchase unsold properties and convert them into affordable housing. He also urged local governments to repurpose inactive land parcels held by property developers to alleviate their financial troubles.

This was a very policy-heavy week to save the debt-stricken real estate market. Data showed that property investment and new home sales in April experienced larger contractions, while housing prices slid even further.

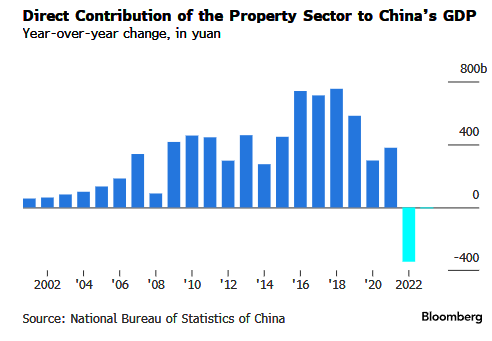

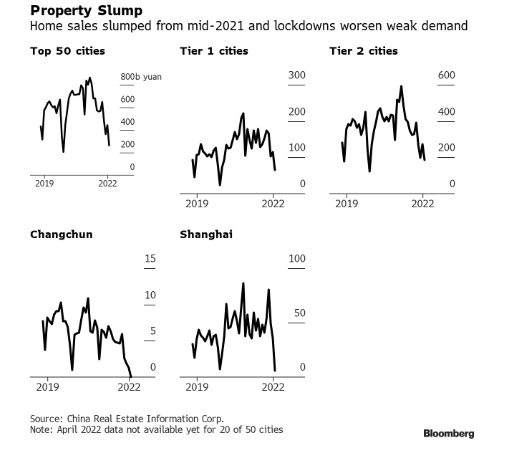

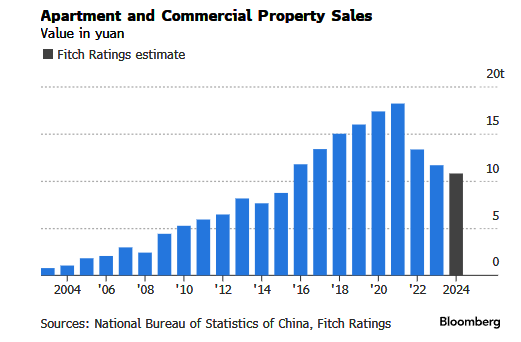

China’s ailing property sector is a drag on GDP.

Housing sales are tumbling.

And apartment and commercial property sales are sliding.

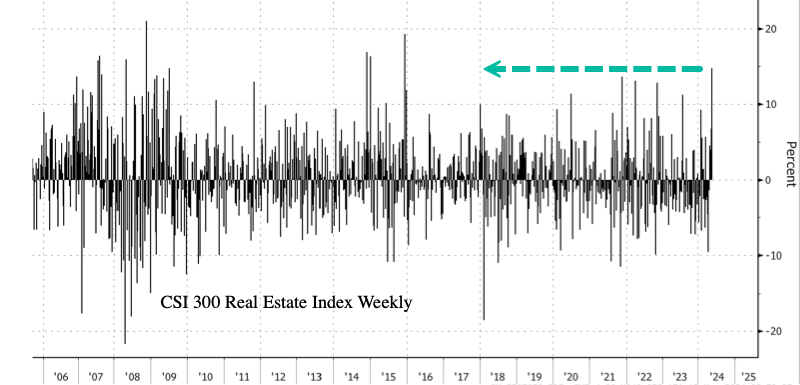

In markets, the CSI 300 Real Estate Index closed up 9%, with gains from April 24 totaling about 36%. Yet the latest gains in the property index are still 68% below the early 2018 peak.

The index’s weekly gain was the most since early December 2015.

It isn’t in a Communist countries’ DNA to let markets solve the problem … like letting prices correct no matter how painful that adjustment is. Biden and his “economic” advisor Jared Bernstein (not an economist but a public policy hack) would likely follow China’s idiotic solutions to the problem.

I debated Bernstein once at a Washington DC conference. He was arrogant but eventually confessed that he didn’t know anything about housing or mortgages. Nice economic advisor, Joe!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.