October STICKY core inflation is still up 4% YoY (year-over-year)

Core CPI rose 0.3% MoM (as expected) which pushed it up 3.3% YoY (not even close to the 2% mandate)…

Source: Bloomberg

There has not been a single monthly decrease in core consumer prices since Biden too office.

dddd

Between The Fed’s insane monetary policy and Biden/Harris insane fiscal policies, we are living in a world where Ray Bradbury’s novel Fahrenheit 451 becomes a reality. Instead of books burning, it is the US Dollar burning.

NEW YORK, NOVEMBER 26, 2024: S&P Dow Jones Indices (S&P DJI) today released the September 2024 results for the S&P CoreLogic Case-Shiller Indices. The leading measure of U.S. home prices recorded a 3.9% annual gain in September 2024, a slight deceleration from the previous annual gains in 2024.

YEAR-OVER-YEAR The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.9% annual return for September, down from a 4.3% annual gain in the previous month. The 10-City Composite saw an annual increase of 5.2%, down from a 6.0% annual increase in the previous month. The 20-City Composite posted a year-over-year increase of 4.6%, dropping from a 5.2% increase in the previous month. New York again reported the highest annual gain among the 20 cities with a 7.5% increase in September, followed by Cleveland and Chicago with annual increases of 7.1% and 6.9%, respectively. Denver posted the smallest year-over-year growth with 0.2%.

Table 2 below summarizes the results for September 2024. Cleveland and New York top 7% YoY.

The problem with the national debt can’t be fixed with Mitch McConnell still in the Senate and too many Obama-era political hacks still in Washington DC.

The Obama/Biden era began in 2009 and it still exists despite Trump winning the Presidency for 2025. The Obama/Biden regime along with Congressional assistance drove up US Federal Debt to around $36 TRILLION. That is an increase of a staggering 236% since Obama/Biden were sworn into office in January 2009. And Federal spending is up 121%.

Unfortunately, Trump cannot pull a Javier Milei (Argentina’s libertarian President) and obliterate the bloated carcas of Federal bureaucracy. Democrats and RINOs like Mitch McConnell will work overtime thwarting Trump’s efforts to control the bloat.

And don’t forget the $221 TRILLION in unfunded liabilities (promises) that Congress had made to get elected. That will eventually become Federal debt.

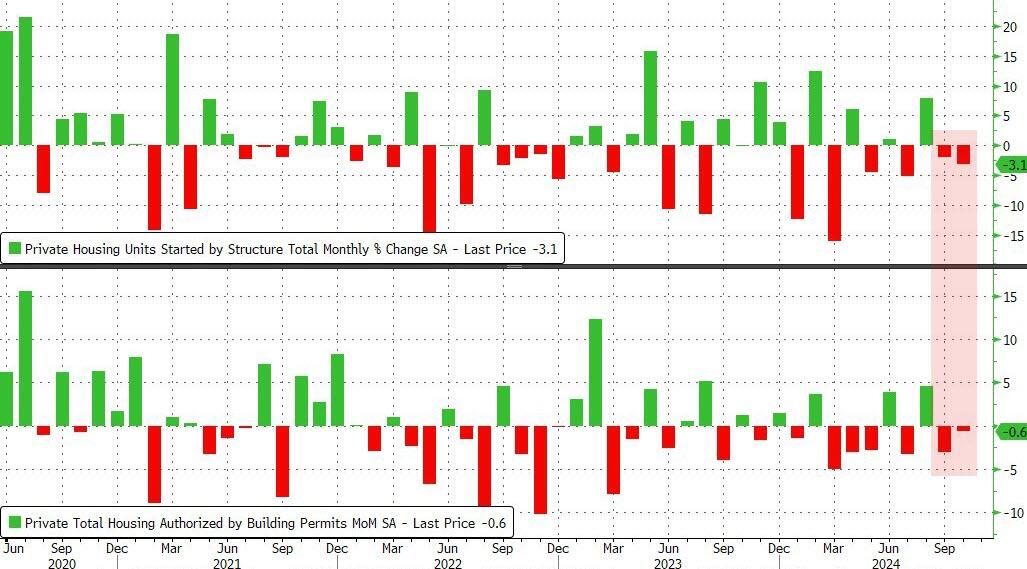

As Biden/Harris approve of Ukraine launching missiles against Russia risking nuclear war, we are witnessing a slow down in the US economy. This time, housing starts and permits.

US Housing Starts and Building Permits disappointed in October with the former dropping 3.1% MoM (-1.5% exp) and -0.6% MoM (+0.7% exp) respectively. This is the second straight month of declines for both measures of housing activity.

Source: Bloomberg

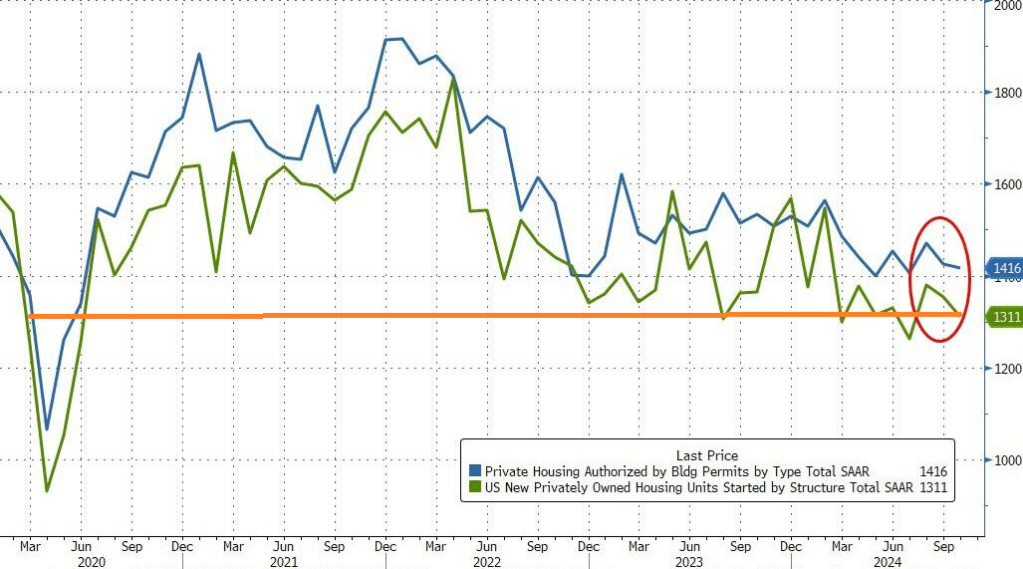

That pulled the SAAR totals down to four month lows – hovering just above COVID lockdown levels…

Source: Bloomberg

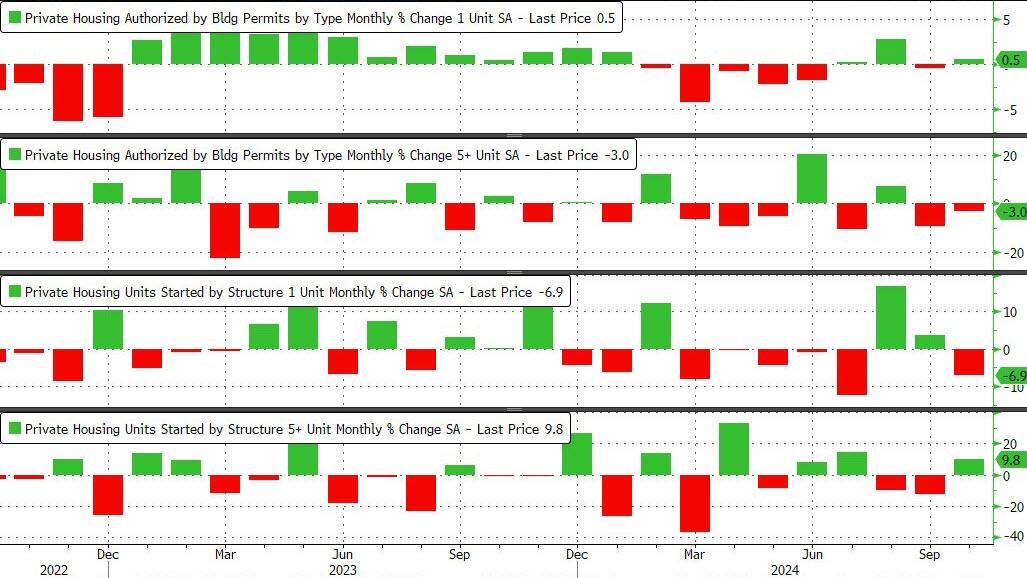

Under the hood, it was very mixed with Single-family permits rising and multifamily permits dropped. Single-family Starts plunged while multi-family Starts jumped…

Source: Bloomberg

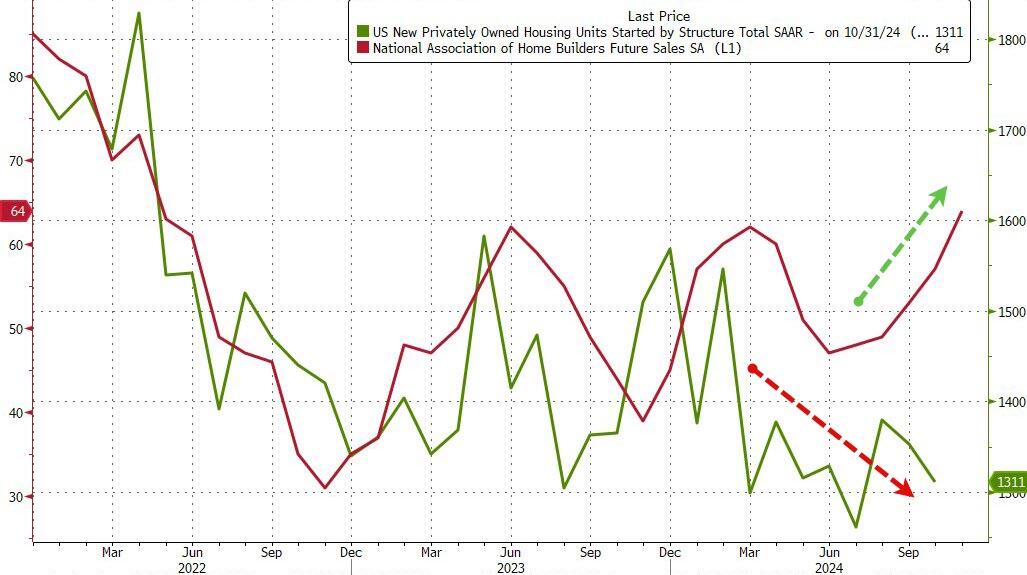

As rate-cut expectations have fallen, so have homebuilders actions it seems…

Source: Bloomberg

But homebuilder ‘hope’ remains high…

Source: Bloomberg

With Trump back in charge, how much will Powell and his pals really want to cut rates now?

There is one way out of the inflation trap. And it’s drill, baby, drill!

For the 53rd straight month, core consumer prices rose on a MoM basis in October with the YoY pace re-accelerating to +3.33%.

The shelter index increased 4.9 percent over the last year, accounting for over 65 percent of the total 12-month increase in the all items less food and energy index.

Thank goodness Harris can’t try to impliment her ridiculous plans to boost housing!

Glad to see Vivek Ramaswamy and Elon Musk (the NEW Two Bobs from Office Space) cleaning up the mess in Washington DC.

The US Treasury yield curve (10Y-2Y CMT) went negative on April 1, 2024. And remains positive.

The US Treasury 10Y-2Y CMT (constant maturity Treasury) peaked locally on March 29, 2024 and then fell, eventually turning negative on April 1, 2024. And remained negative until August 30, 2024 just prior to the election. It looks like the yield curve accurately predicted the election of Trump.

The 10-year Treasury yield is rising with a positive economic outlook under Trump. And with that optimism we see mortgage rates rising too.

The Market Composite Index, a measure of mortgage loan application volume, decreased 10.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 12 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index decreased 7 percent compared with the previous week and was 2 percent higher than the same week one year ago.

The Refinance Index decreased 19 percent from the previous week and was 48 percent higher than the same week one year ago.

“Ten-year Treasury rates remain volatile and continue to put upward pressure on mortgage rates. The 30-year fixed rate last week increased to 6.81 percent, the highest level since July,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Applications decreased for the sixth consecutive week, with purchase activity falling to its lowest level since mid-August and refinance activity declining to the lowest level since May. The average loan size on a refinance application dropped below $300,000, as borrowers with larger loans tend to be more sensitive to any given changes in mortgage rates.”

The refinance share of mortgage activity decreased to 39.9 percent of total applications from 43.1 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 7.0 percent of total applications.

The FHA share of total applications decreased to 15.5 percent from 16.4 percent the week prior. The VA share of total applications decreased to 12.5 percent from 14.6 percent the week prior. The USDA share of total applications increased to 0.5 percent from 0.4 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 6.81 percent from 6.73 percent, with points decreasing to 0.68 from 0.69 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $766,550) increased to 6.98 percent from 6.77 percent, with points increasing to 0.65 from 0.49 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 6.75 percent from 6.55 percent, with points decreasing to 0.87 from 0.94 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 6.21 percent from 6.27 percent, with points decreasing to 0.55 from 0.77 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 5/1 ARMs decreased to 6.05 percent from 6.20 percent, with points increasing to 0.84 from 0.59 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The bond market is reacting to the election of Trump with a clear Bear Steepening.

Bear steepening happens when yields move up across tenors, but long-end yields move up even faster than short-end yields.

This isn’t going to help mortgage applications due to lowering rates.

Congress went wild spending on Covid relief and related wasteful spending. Notice that the impetus for job openings (spending) occurred before “Angry Joe” Biden and Commie-la Harris were sworn in. So, the job creation claims by Biden/Harris were put into motion before they assumed office.

The lag in job openings growth after the surge in spending is clearly visible in the following chart, as is the BURNOUT in job openings growth after Covid spending burned out.

Harris is promising explosive spending if elected. And she is promising MORE regulations! And the regulatory burden will grow.

Mortgage applications were essentially flat last week as rates increased for the fourth time in five weeks, driven by bond market volatility in advance of the presidential election and the next FOMC meeting. The 30-year fixed rate, at 6.73 percent, was at its highest level since July 2024.

WASHINGTON, D.C. (October 30, 2024) — Mortgage applications decreased 0.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending October 25, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 0.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 4 percent compared with the previous week and was 10 percent higher than the same week one year ago.

The Refinance Index decreased 6 percent from the previous week and was 84 percent higher than the same week one year ago.

The US is the expensive tower of power … but it should be cheap. Getting rid of coal power was idiotic and The Left’s fear of nuclear power is laughable.

Europe’s fertilizer plants, steel mills, and chemical manufacturers were the first to succumb. Massive paper mills, soybean processors, and electronics factories in Asia went dark. Now soaring natural gas and electricity prices are starting to hit the US industrial complex.

On June 22, 600 workers at the second-largest aluminum mill in America, accounting for 20% of US supply, learned they were losing their jobs because the plant can’t afford an electricity tab that’s tripled in a matter of months. Century Aluminum Co. says it’ll idle the Hawesville, Kentucky, mill for as long as a year, taking out the biggest of its three US sites. A shutdown like this can take a month as workers carefully swirl the molten metal into storage so it doesn’t solidify in pipes and vessels and turn the entire facility into a useless brick. Restarting takes another six to nine months. For this reason, owners don’t halt operations unless they’ve exhausted all other options.

At least two steel mills have begun suspending some operations to cut energy costs, according to one industry executive, who asked not to be identified because the information isn’t public. In May, a group of factories across the US Midwest warned federal energy regulators that some were on the verge of closing for the summer or longer because of what they described as “unjust and unreasonable” electricity costs. They asked to be wholly absolved of some power fees—a request that, if granted, would be unprecedented.

Michael Harris, whose firm Unified Energy Services LLC buys fuel for industrial clients, says costs have risen so high that some are having to put millions of dollars of credit on the line to secure power and gas contracts. “That can be devastating for a corporation,’’ he says. “I don’t see any scenario, absent explosions at US LNG facilities’’ that trap supplies at home, in which gas prices are headed lower in the long term.

EIA Average Electricity Cost Cents

EIA cost data chart by Mish

EIA Cost Data January 2021 vs May 2022

Residential: 12.69 to 14.92

Commercial: 10.31 to 12.14

Industrial: 6.39 to 8.35

Transportation: 9.61 to 10.79

All: 10.36 to 12.09

Those prices are through May 2022. Much electrical energy comes from natural gas.

US Natural Gas Futures

US Natural Gas Futures courtesy of Trading Economics

US gas prices fluctuated wildly in June and July. I suspect the average price is 7.33 or so for both months. Things are decidedly worse in Europe.

EU Natural Gas Price

US Natural Gas Futures courtesy of Trading Economics

From 25 or even 50 to 200 is one hell of a leap. It’s somewhere between 300% and 700% depending on your starting point vs 100% or so for the US.

Let’s now check the latest PPI data for a look at where things are and more importantly headed.

PPI Electrical Power Index 2020-Present

PPI data from the BLS, chart by Mish

From pre-pandemic to January of 2021, the PPI electrical power index was flat. It has since surged on a relatively steady pace.

From May to July the index went from 231 to 238. That tacks on another three percentage points since the EIA report.

PPI Electrical Power Index 1991-Present

PPI data from the BLS, chart by Mish

Long Term Trend

The long-term trend does not exactly look pretty.

And as Bloomberg noted, Century Aluminum Co. says it’ll idle the Hawesville, Kentucky, mill for as long as a year, taking out the biggest of its three US sites.

The beer industry uses more than 41 billion aluminum cans annually, according to a Beer Institute letter to the White House dated July 1.

“These tariffs reverberate throughout the supply chain, raising production costs for aluminum end-users and ultimately impacting consumer prices,” according to the letter signed by the CEOs of Anheuser-Busch, Molson Coors, Constellation Brands Inc.’s beer division, and Heineken USA.

This letter to the president comes amid the worst inflation in more than 40 years and just months after aluminum touched a multi-decade high. Prices for the metal have since eased significantly.

Whatever victory beer makers and drinkers may have with aluminum prices may not last with US aluminum plants shutting down.

Then again, the cure for everything is likely to be a huge recession.

Zero Consumer Inflation

I am pleased to report there was no consumer inflation in July.

The CPI report resulted in a nonsensical Twitter debate on the meaning of zero. For the record, assuming you believe the numbers, there was indeed zero inflation month-over-month.

The accurate rebuttal is: One month? So what?

Moreover, zero is not as good as it looks. All of it was due to a 7.7 percent decline in the price of gasoline. And year-over-year inflation was a hot 8.5 percent.

Meanwhile, rent and food keep rising and the price of rent will be sticky. Gasoline is more dependent on recession and global supply chains.

The above reports and this one industrial costs puts a spotlight on the silliness of the Fed’s focus on consumer inflation as if that’s all that matters.

The Fed has blown three consecutive bubbles trying to produce two percent consumer inflation while openly promoting raging bubbles in assets and missing the boat entirely on industrial matters.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.