Inflation Joe and Slow-Walking Jay. The bullies of the middle class and low-wage workers.

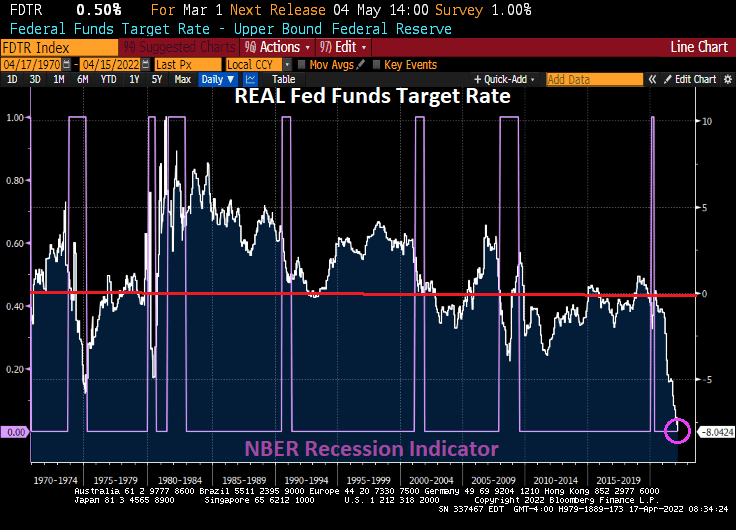

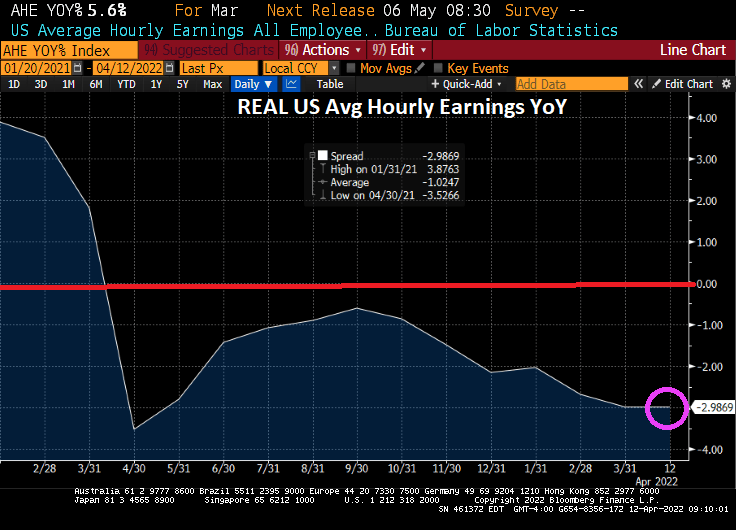

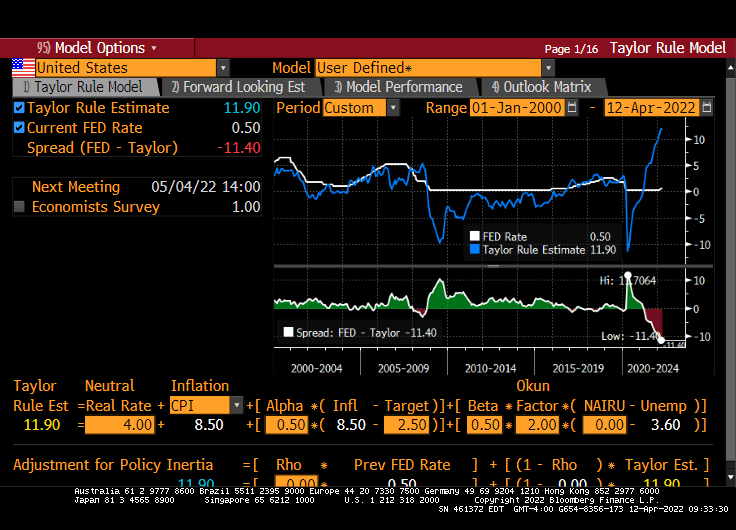

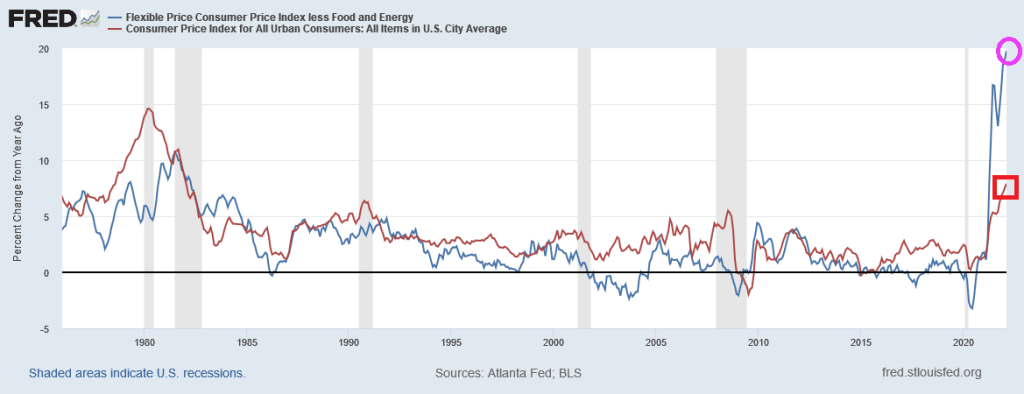

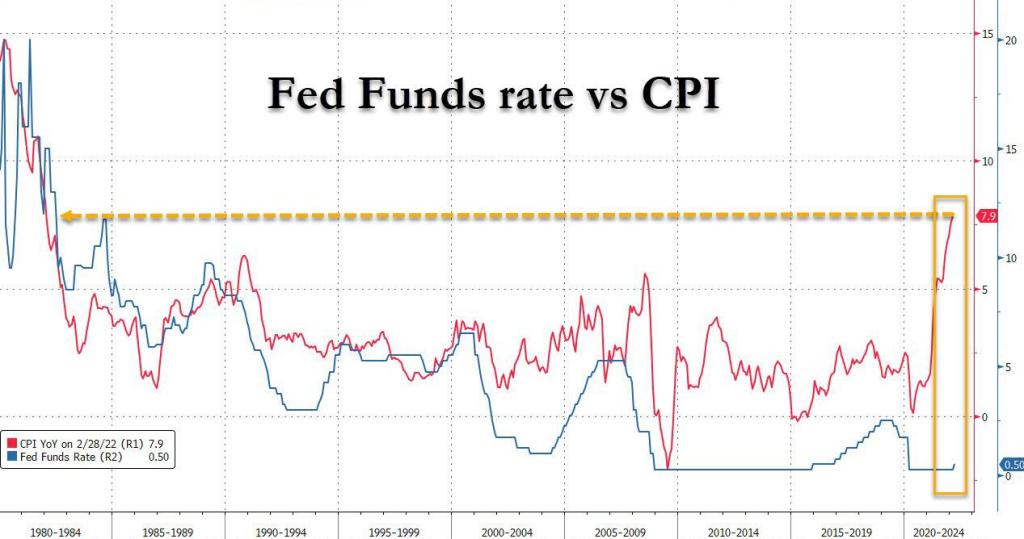

As inflation crushes the middle class and low wage workers, we see that the REAL Fed Funds Target Rate (based on headline inflation) is the lowest in history. Notice that the REAL Fed Funds Target Rate tends to hit its lowest negative reading DURING recessions, although The Fed has had a poor track record since the Dot.com bubble burst and the 2001 recession meaning that the REAL Fed Funds Target rate has been in negative territory (that is, the rate of inflation has exceeded The Fed Funds Target Rate for much of the post-2000 era).

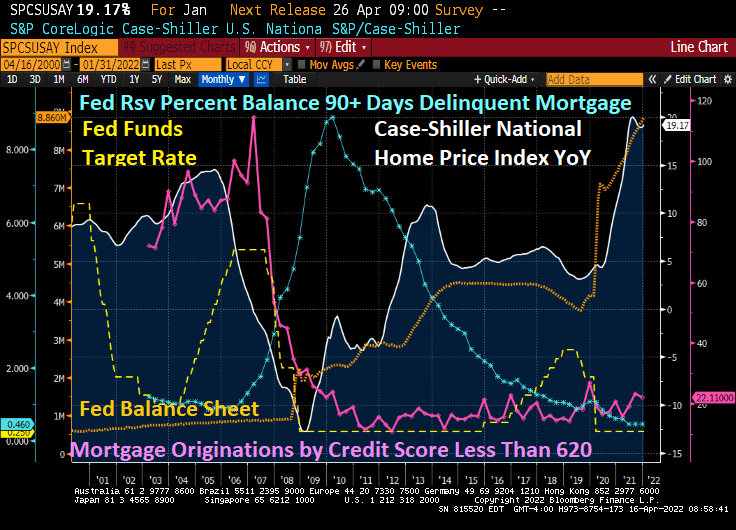

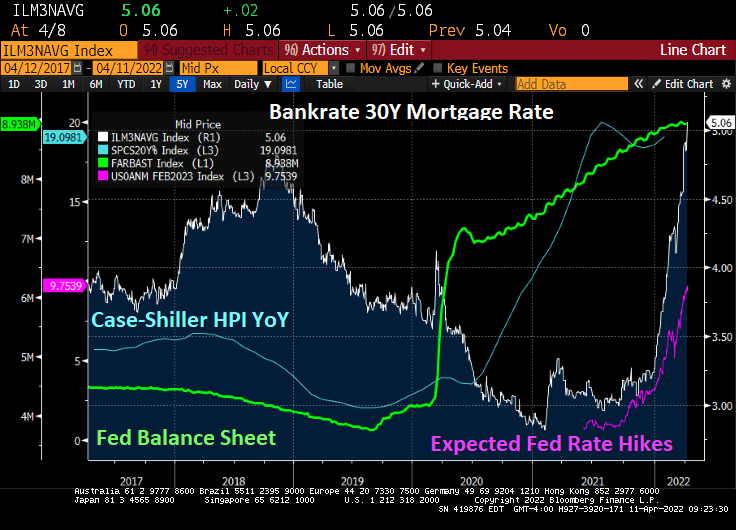

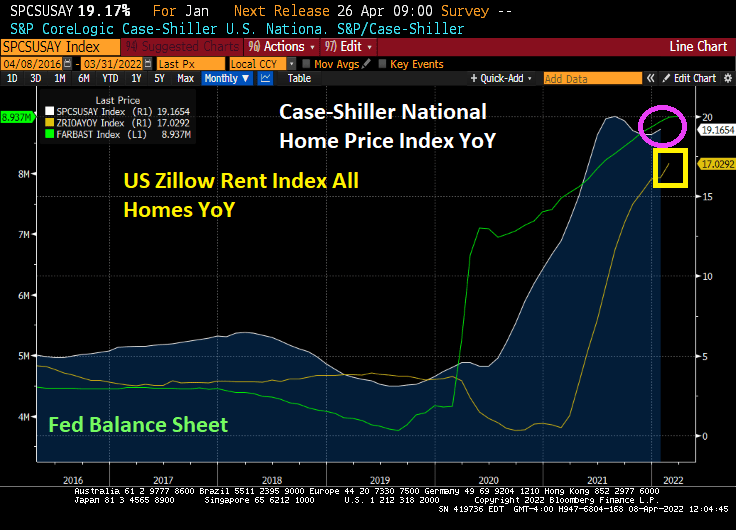

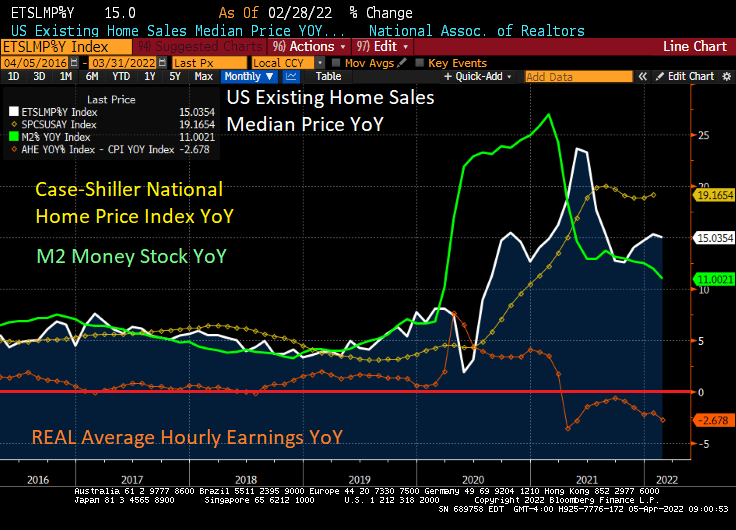

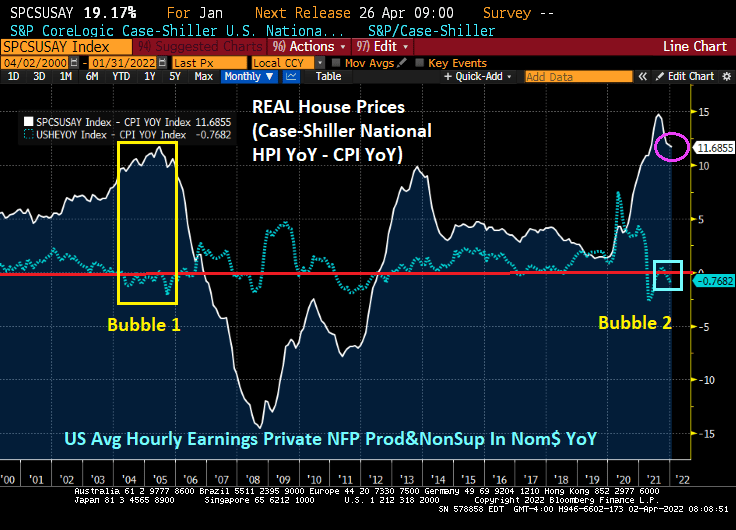

The “good” news? Inflation caused by The Fed’s negative interest rate policy (NIRP?) has actually led to REAL home price growth to slow 11.6855% YoY, lower than the peak of the 2005-2007 house price bubble.

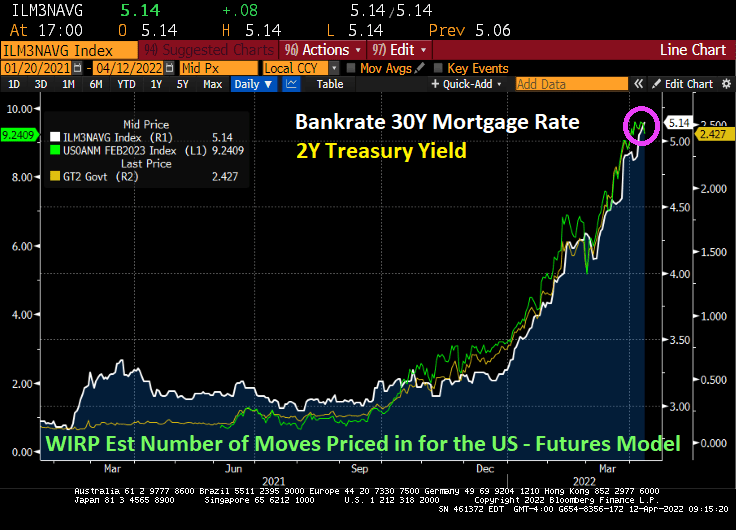

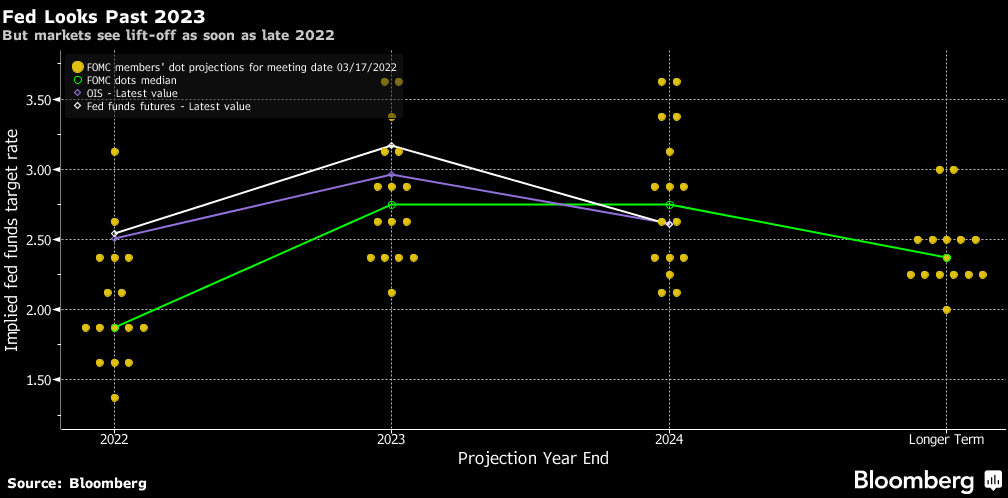

With The Fed’s OVERSTIMULATION of markets with historically low REAL Fed Funds Target Rate, we can see that the US unemployment rate is overheated (that is, below the Congressional Budget Office (CBO) Short-term Natural Rate of Unemployment. Yes, it appears that Slow Walking Fed Chair Jay Powell should be raising The Fed’s target rate AND removing (at least) the Covid monetary stimulus.

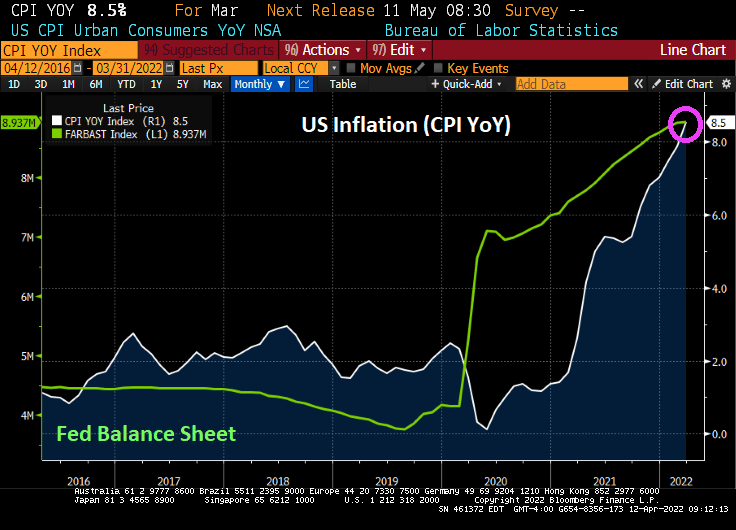

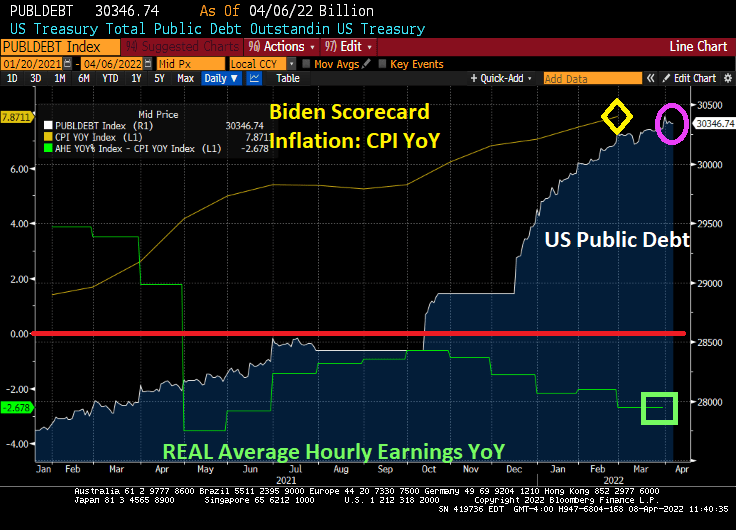

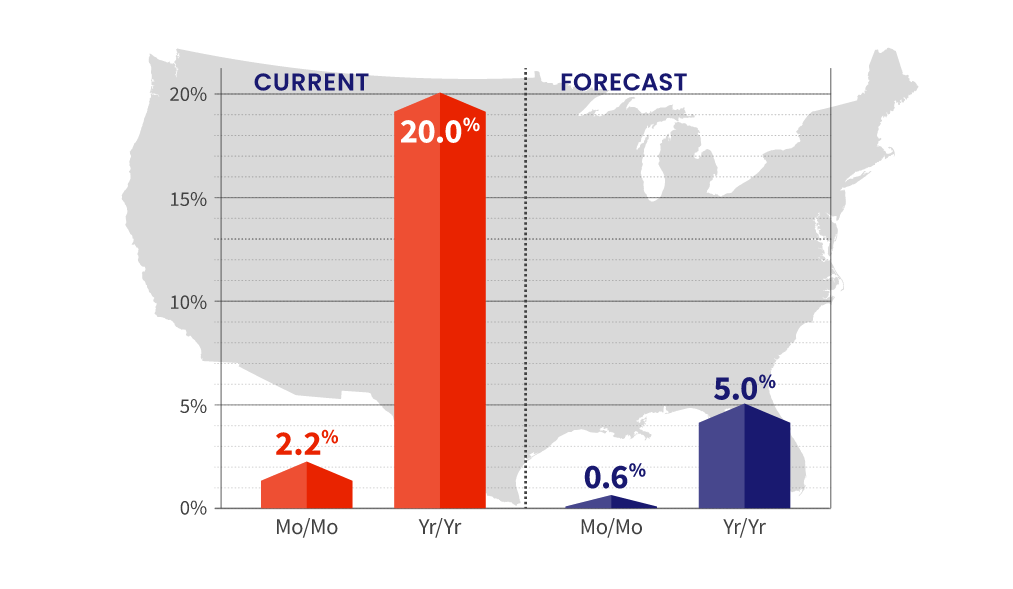

Inflation Joe is a career politician, so it is not surprising that he is trying to blame Russia for the horrid inflation in the US. However, inflation grew from 1.4% when Biden took office to 7.9% when Russia invaded Ukraine. The latest inflation report was 8.5%, so Russia is only partly to blame for rising prices since February 24, 2022. The rest is due to Inflation Joe, Slow Walking Jay and Congress.

Again, Congress helped drive prices through the roof by massive Federal spending (aka, Covid stimulus “relief”). Hence, the Four Horsemen of the Inflation Apocalypse is appropriate. And now Biden is once again pitching massive government spending (Build Inflation Back Better?).

Here is Joe Biden and his inflation bat, Lucille.

Have a peaceful and pleasant Easter Sunday.

You must be logged in to post a comment.