Anticipation about Federal Reserve rate hikes over the next 12 months are seeding mortgage rates soaring and mortgage refinancing applications plummeting.

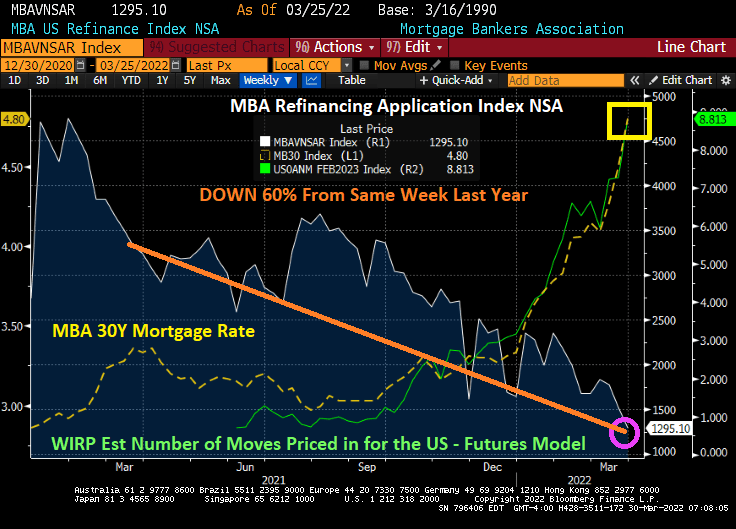

Mortgage applications decreased 6.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 25, 2022.

The Refinance Index decreased 15 percent from the previous week and was 60 percent lower than the same week one year ago.

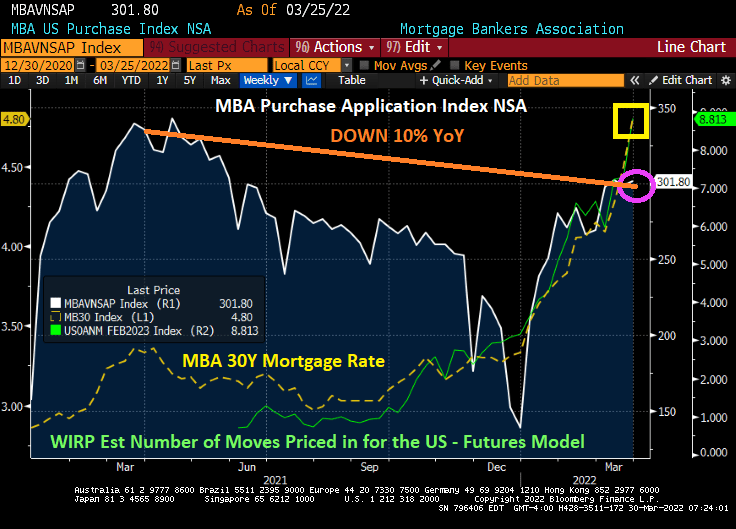

The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 10 percent lower than the same week one year ago.

Yes, I am surprised at the rise in mortgage purchase applications with rising mortgage rates, unless, of course, people are trying to buy ahead of Fed rate increases.

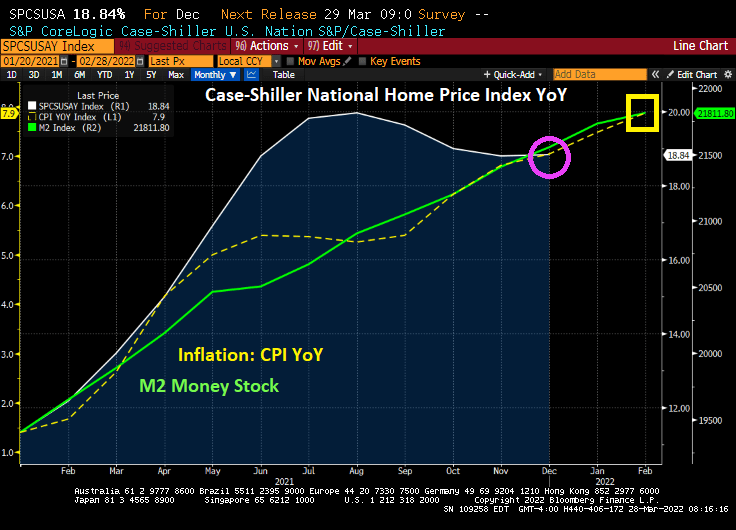

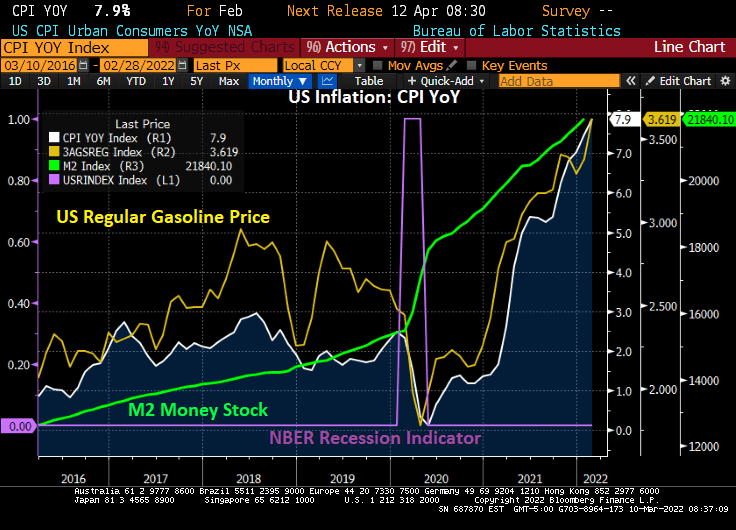

Inflation under President Biden (aka, Bidenflation) has hit 7.9%, the highest in 40 years. And no Joe, the inflation surge was well underway before Russia invaded Ukraine on February 24, 2022.

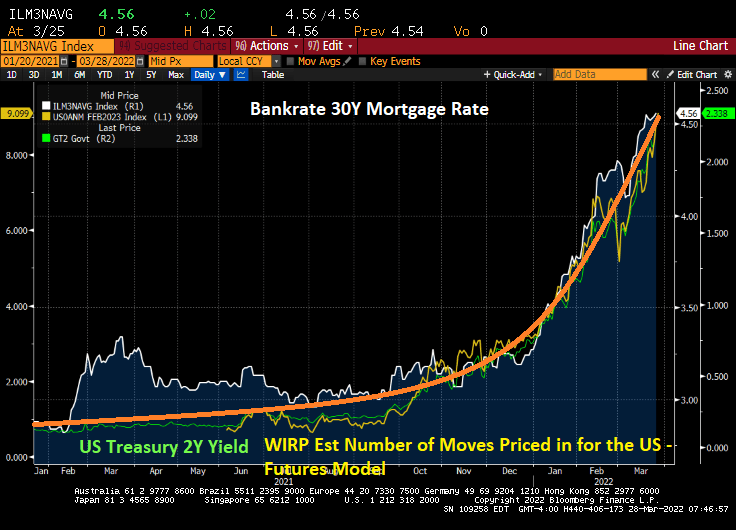

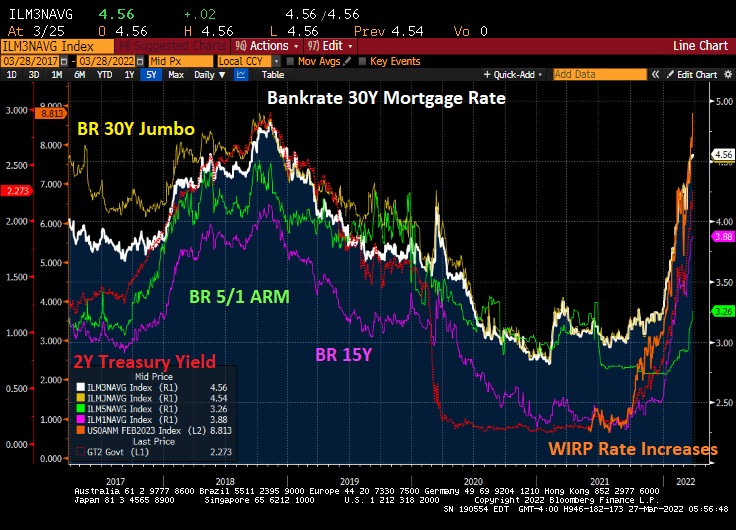

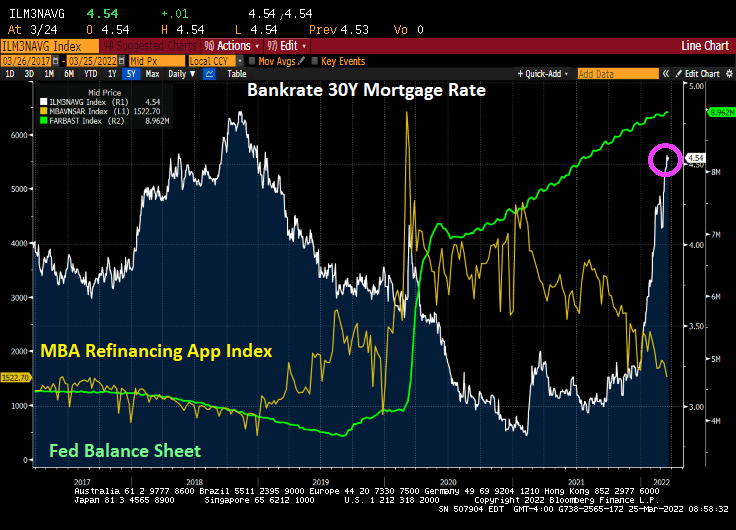

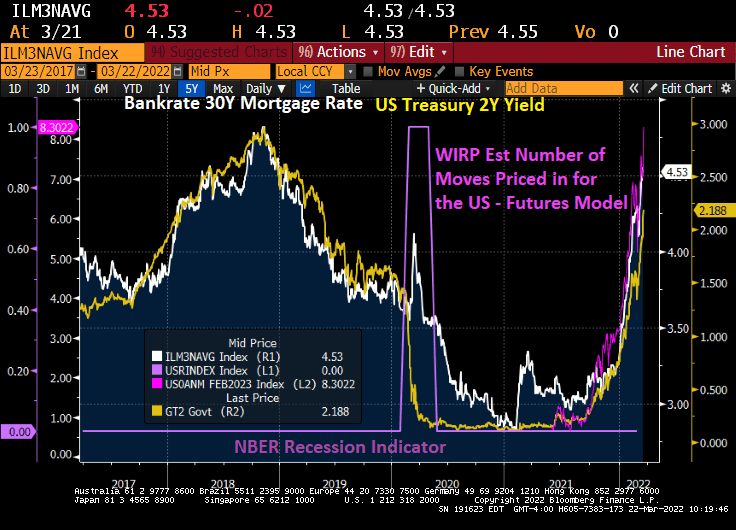

As The Federal Reserve is allegedly going to try to fight inflation by raising their target rate, the 30-year mortgage rate has risen from 2.88% on Biden’s inauguration to 4.56% today.

The surge in mortgage rates from 2.88% to 4.56% represents a 58.3% increase in mortgage rates under Biden. That translates to an increase in the 30-year fixed-rate mortgage (FRM) payment of 23%. Apparently Biden-Powell (not to be confused with Baden-Powell, the founder of the Boy Scouts) are not interested in keeping homes affordable for most Americans.

I summarize the predicament facing Americans in the following chart. Home prices were growing at a 19% YoY pace in December (Case-Shiller updates will be available tomorrow for January). Inflation is growing at 7.9% and M2 Money continues to grow.

US fertilizer prices are up 166% under Biden while regular gasoline prices are up 77% under Biden. But to be fair, fertilizer and gasoline prices jumped with Russia’s invasion of Ukraine. Fertilizer prices were up 66% under Biden BEFORE Russia invaded Ukraine and regular gasoline prices were up 50%.

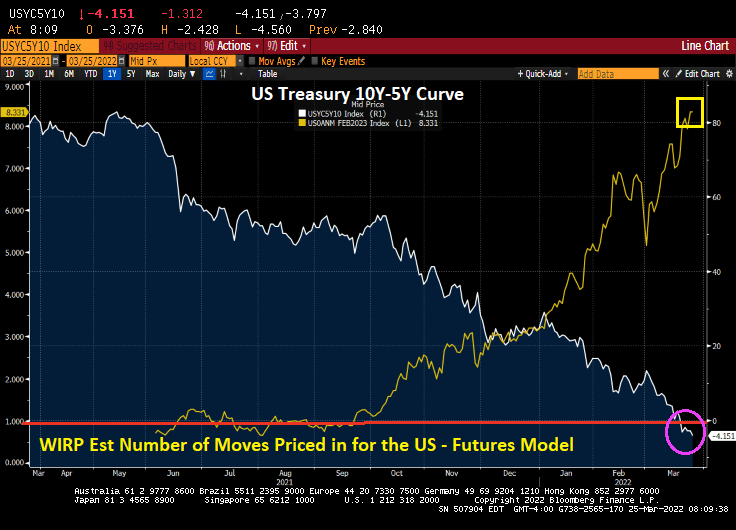

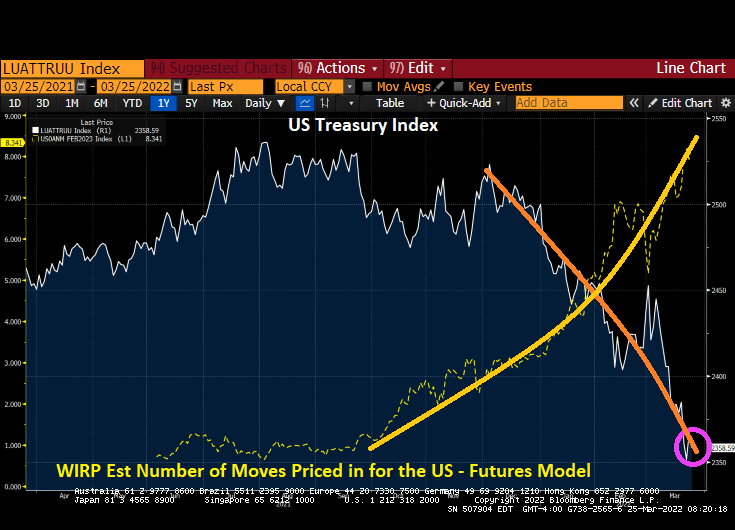

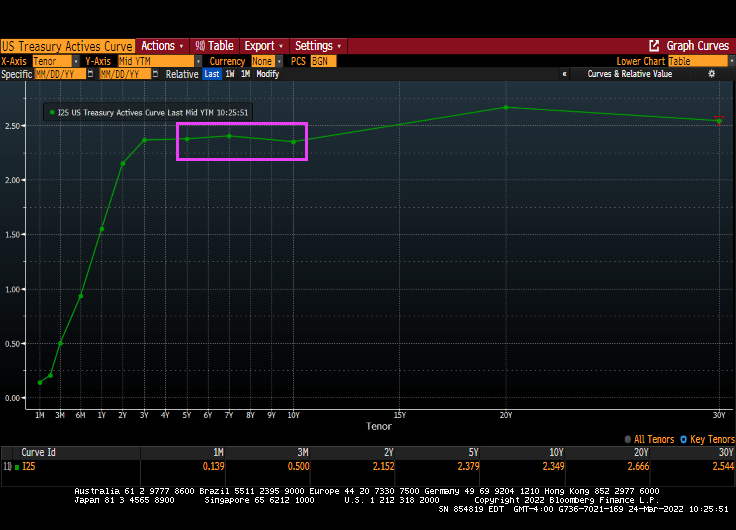

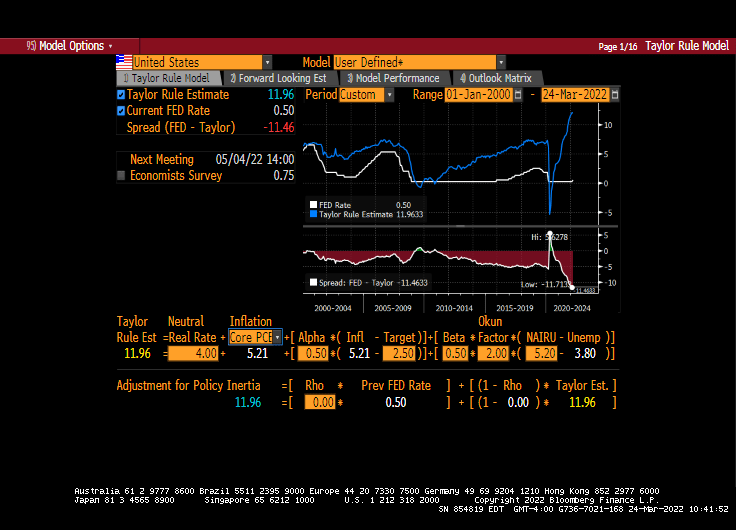

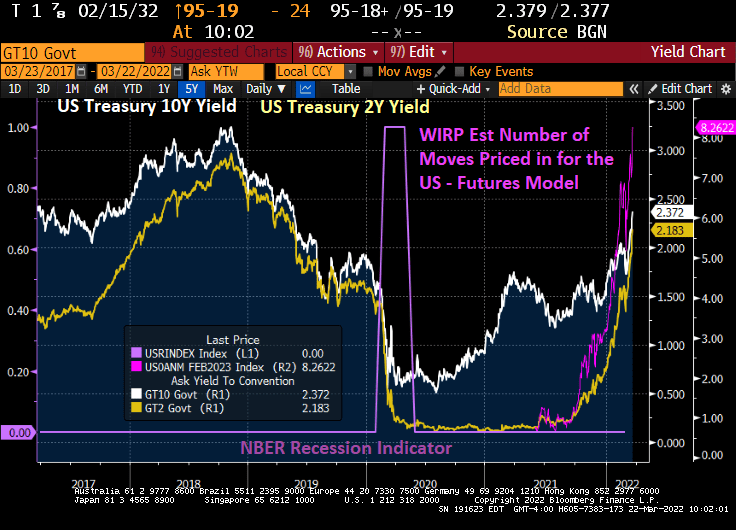

Meanwhile, back at the fixed-income ranch, the US Treasury 10Y-2Y curve has flattened to 14.5 BPS as Fed Funds Futures signal 9 rate hikes over the coming year.

And the US Treasury 10Y-5Y curve continues to invert.

In short, Biden and Congress are anti-fossil fuel, pro-renewable energy helping to drive up energy prices and inflation PRIOR to Russia invading Ukraine. Powell and The Federal Reserve are trying to fight what Biden and Congress did with creating energy-related inflation.

The reason why the fear of ARMs is unwarranted is that ARMs generally have CAPS on rate increases, either in a given period or over the life of the loan. Of course, READ the loan terms to ensure that the ARMs has restrictive caps on rate increases.

Currently, the 5/1 ARM is at 3.26% while the 30-year FRM is at 4.56%, a spread of 130 basis points.

Mortgage rates of all flavors are rising rapidly with the expectation of Federal Reserve Quantitative Tightening (QT). There are several headwinds that could counter The Fed’s QT efforts such as low GDP growth (Atlanta Fed’s GDPNow real-time GDP tracker is at 0.9% for Q1), the Russia-Ukraine invasion, approaching midterm elections, etc. But as of today, The Fed seems on a collision course with rising mortgage rates.

With the increasing likelihood of Fed rate hikes over the next year, we are seeing an increase in US ARM loan share from 4% to 7.9%, almost a doubling of ARM share. But FRMs are still over 90% of all mortgage originations.

Lending institutions would prefer consumers to use ARMs rather than FRMs since ARMs allow for the transfer on long-term interest rate risk to the borrower, while the FRM sticks the lender with long-term interest rate risk. Hence, we have Fannie Mae and Freddie Mac, the Government Sponsored Enterprises (GSEs) that allow lenders to originate FRMs and sell them to F&F. We are the only country with twin GSEs.

So, while most consumers would be better-off with an adjustable-rate mortgage, the structure of the mortgage market (particularly after the financial crisis) encourages lenders to originate FRMs and sell them to Fannie Mae and Freddie Mac.

But FEAR drives many US mortgage borrowers into the FRM space rather than getting an ARM with a lower interest rate, even if ARM caps would prevent the mortgage rate from rising more than 100 basis points over the life of the loan.

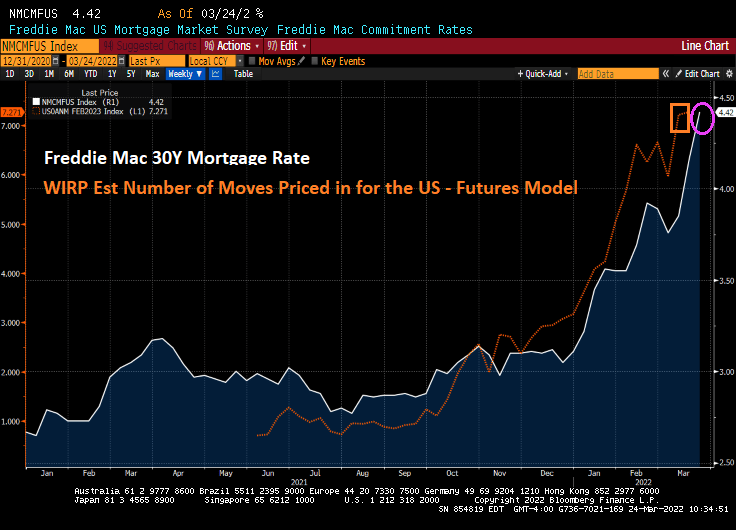

According to Fed Funds Futures data, The Federal Reserve is now forecasting 9 rate increases over the next year.

Fed Funds Futures are pointing to 8.924 rate hikes by the Fed FOMC meeting on February 1, 2023.

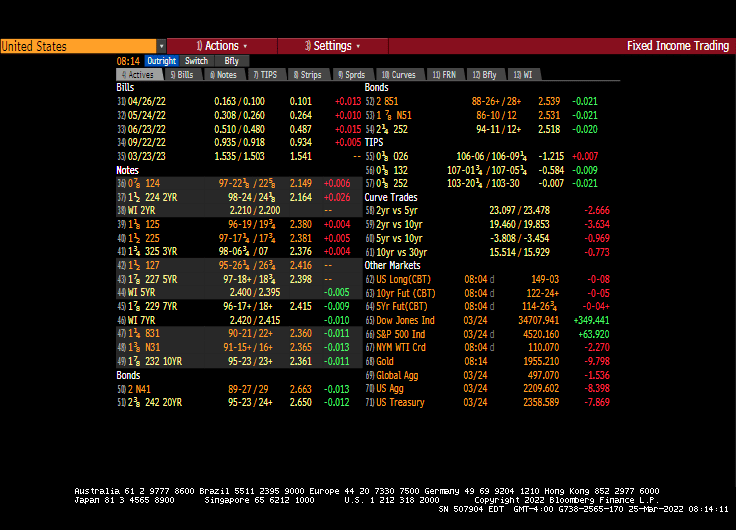

The US Treasury 10Y-2Y curve flattened by 5.5 bps today with the entire curve downshifting.

The Federal Reserve reminds me of The Office episode “Malone’s Cones.” They can’t really explain why they kept rates so low for so long (policy error) and seem to risk collapsing the market with rapid rate hikes without much sensible explanation.

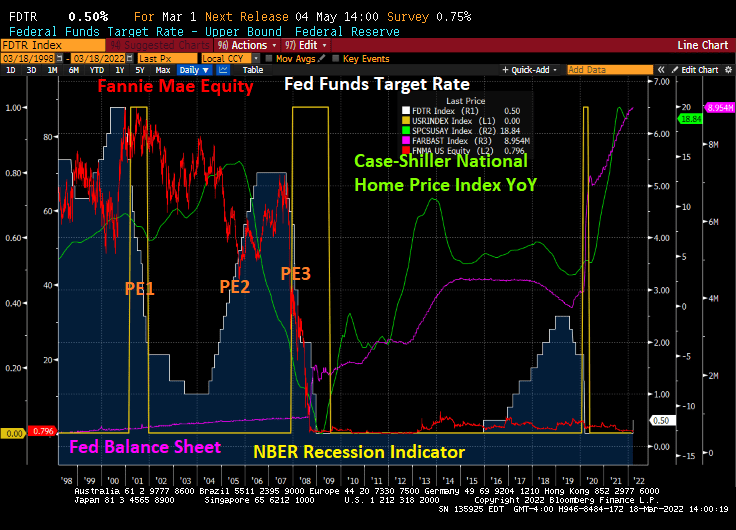

The Federal Reserve is not mentioned in the movies “The Big Short” or “Margin Call”, but The Fed’s policy errors played a big role in the demise of Fannie Mae’s and Freddie Mac’s equity prices.

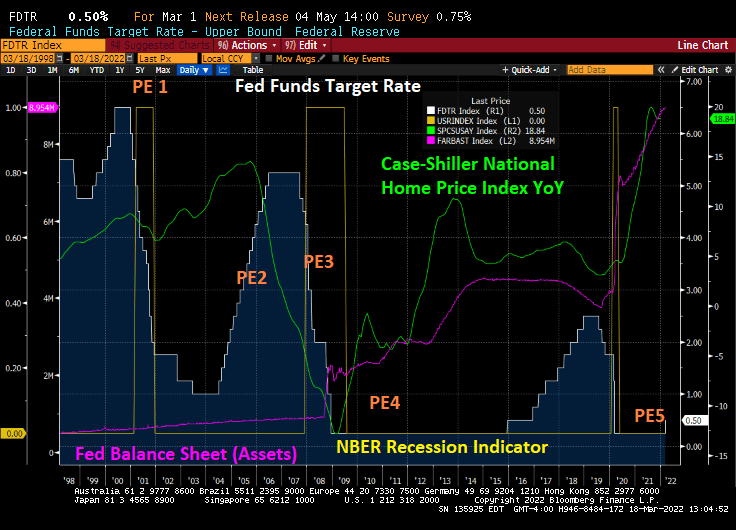

Here is a chart of The Fed’s many policies errors. Let’s start with The Fed lowering rates too fast around the 2001 recession. They pushed their target rate from 6.5% in December 2000 down to 1.75% after one year and then down to 1% (PE1). As home price growth accelerated, The Fed engaged in their second policy error — raising rates too fast resulting in a dramatic cooling of home price growth. Then came Policy Error 3: the dropping of The Fed Funds Target rate from 5.25% in September 2007 to an eventual 0.25% in December 2008.

With the election of President Obama, The Fed engaged in Policy Error 4: keeping The Fed Funds Target rate too low for too long, combined with their massive asset purchase programs (QE).

Finally, The Fed (under Yellen) finally raised The Fed’s target rate ONCE under Obama, but started raising rates once Trump was elected. The Fed also slowed their QE under Trump which as called “Fed policy NORMALIZATION.” Then COVID struck and The Fed engaged in Policy Error 5: keeping rates too low for too long … again while massively expanding their balance sheet.

Fannie Mae and Freddie Mac, the DC mortgage giants were done in by The Fed’s whipsaw Policy Error machine.

Now we are embarking on PE 5: Powell and The Fed Gang not raising rates but signalling that they will. Like the play “Waiting for Godot.”

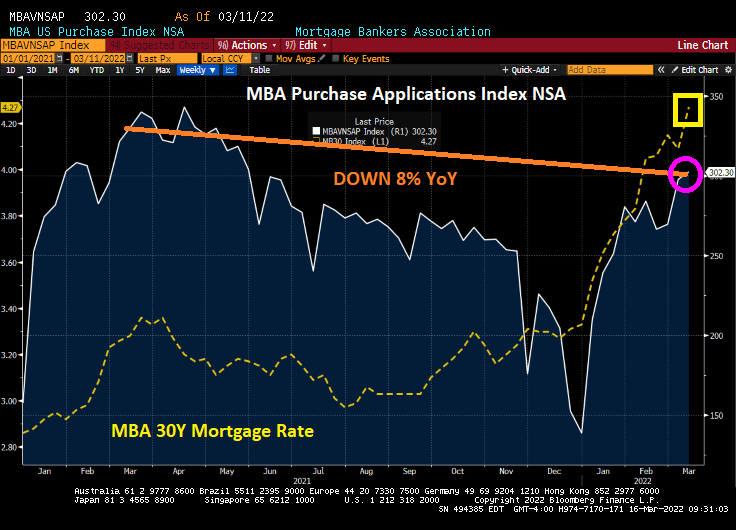

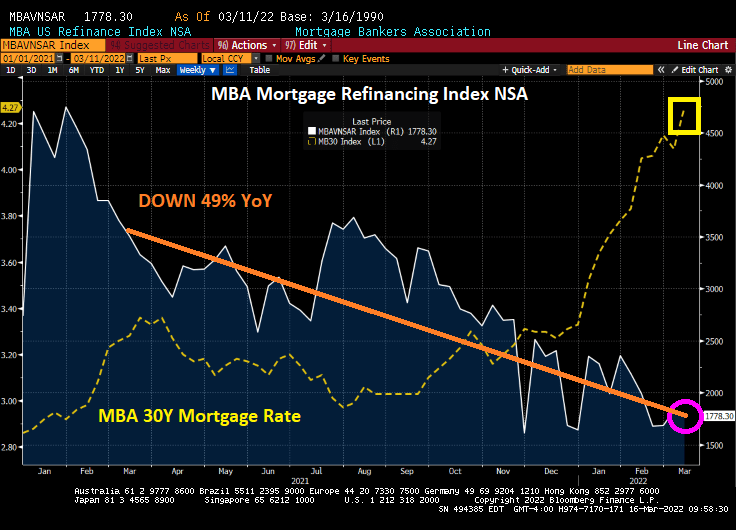

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 11, 2022.

The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 8 percent lower than the same week one year ago.

The Refinance Index decreased 3 percent from the previous week and was 49 percent lower than the same week one year ago.

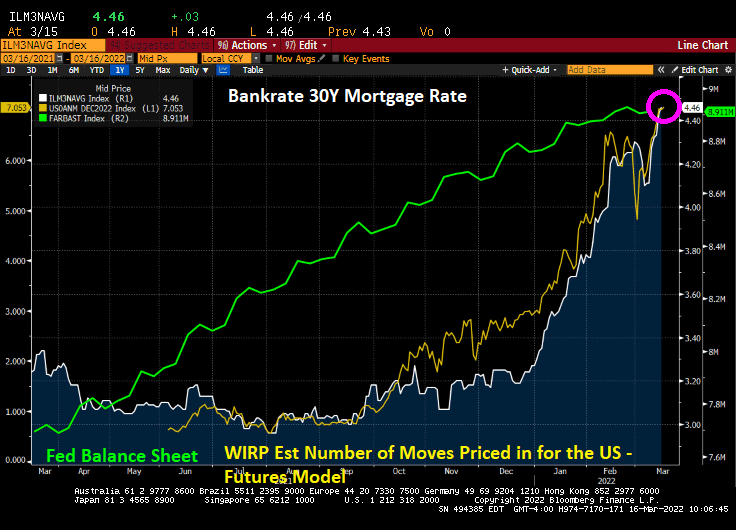

Bankrate’s 30-year mortgage rate has surged to 4.46%.

Here is a photo of alligators in Great Falls, Virginia, up-river from Washington DC. They are likely congregating for the Fed Open Market Committee (FOMC) announcement today.

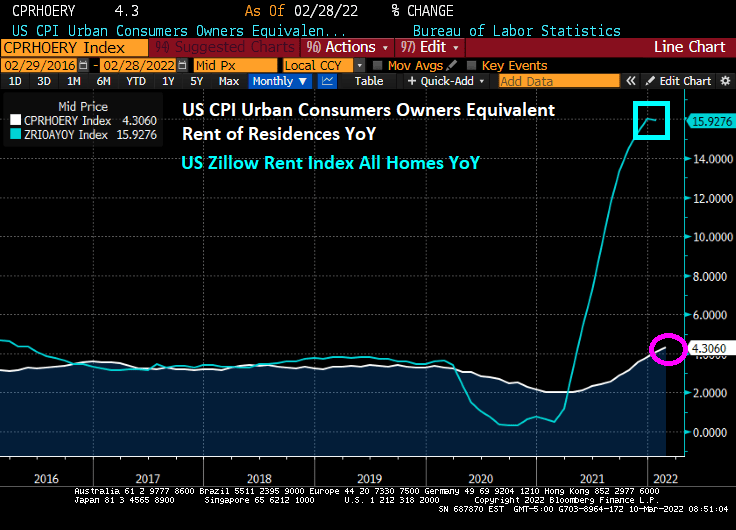

US rent inflation (owner’s equivalent rent of residence YoY) surged to 4.30%. However, Zillow’s rent index last month was 15.93% YoY.

But if we look at US Monthly Rent YoY, we see that rents are climbing at a 17.6% rate.

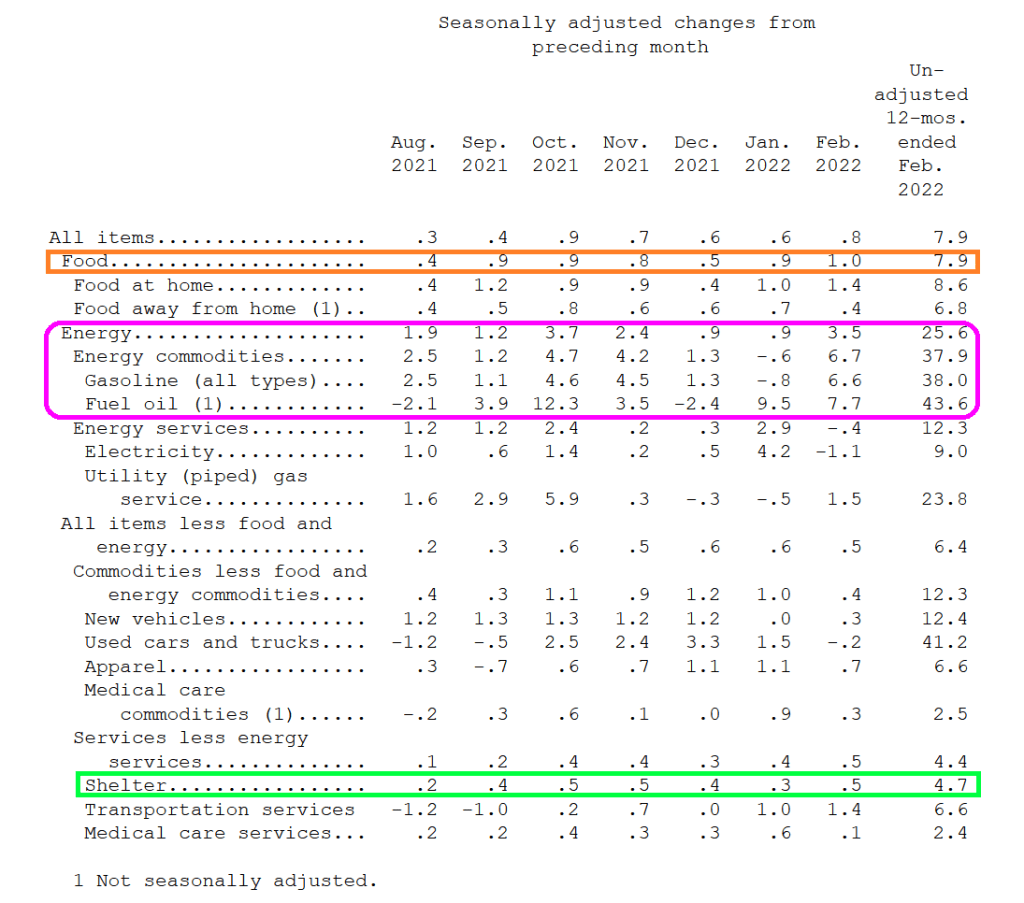

Energy costs soared in February YoY. Gasoline was up 38%. Fuel Oil was up 43.6%. Food was up 7.9%.

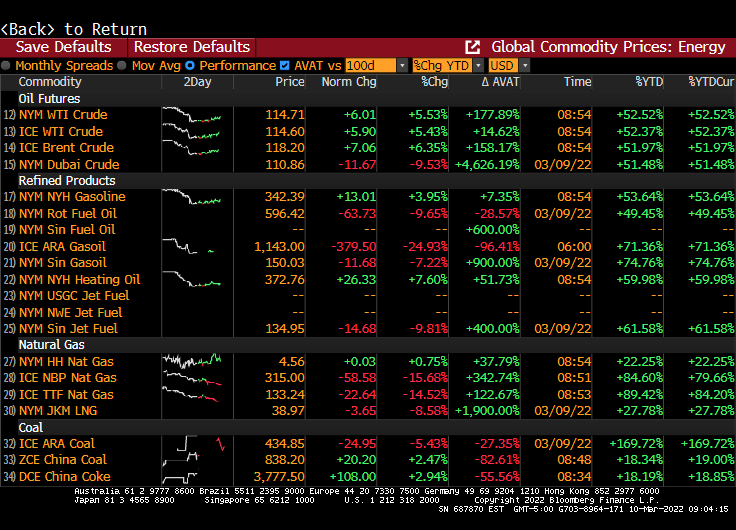

Volatility (AVAT) rages in the energy sector.

There are still 7 rate hikes in the cards from The Federal Reserve.

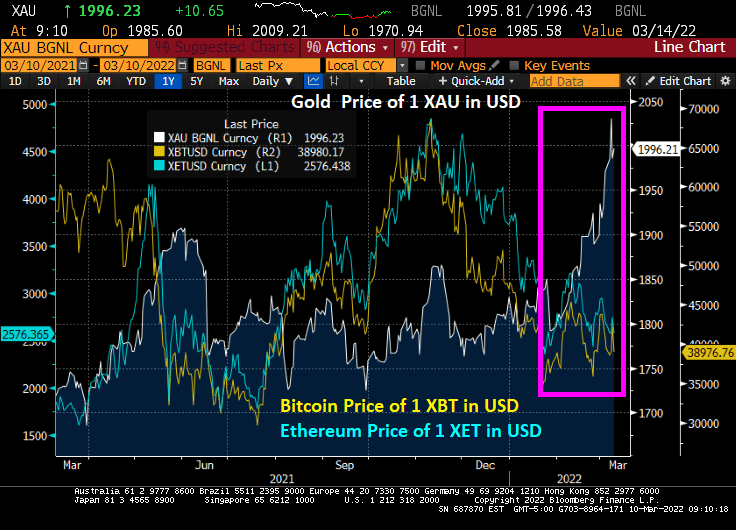

Gold has been climbing as Russia invades Ukraine. Cryptos Bitcoin and Ethereum are steady, even as the Biden Administration issues an executive order to “study” cryptocurrencies.

You must be logged in to post a comment.