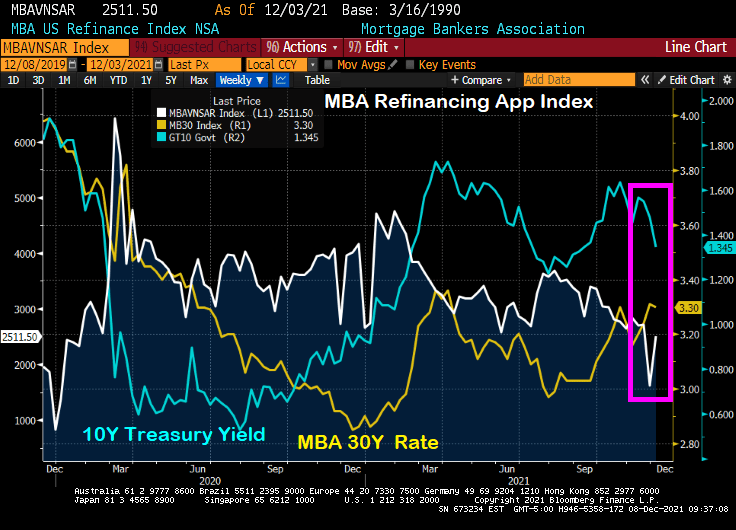

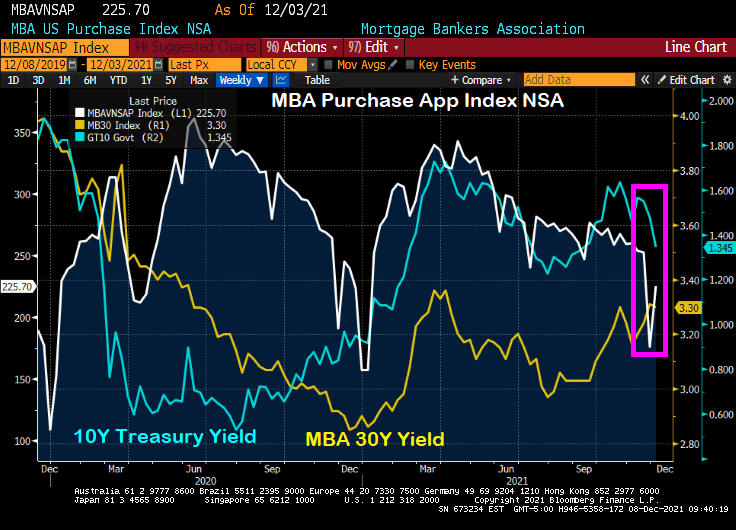

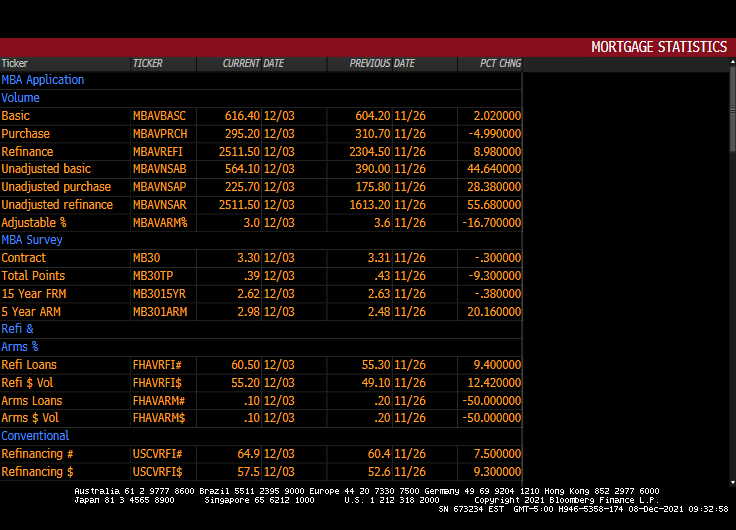

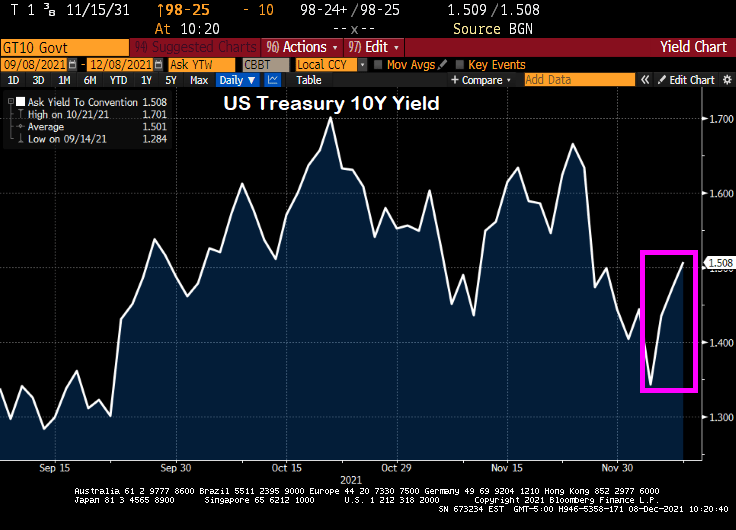

Mortgage rates in the U.S. rose for a third straight week, reaching the highest point in almost two years.

The average for a 30-year loan was 3.45%, up from 3.22% last week and the highest since March 2020, Freddie Mac said in a statement Thursday.

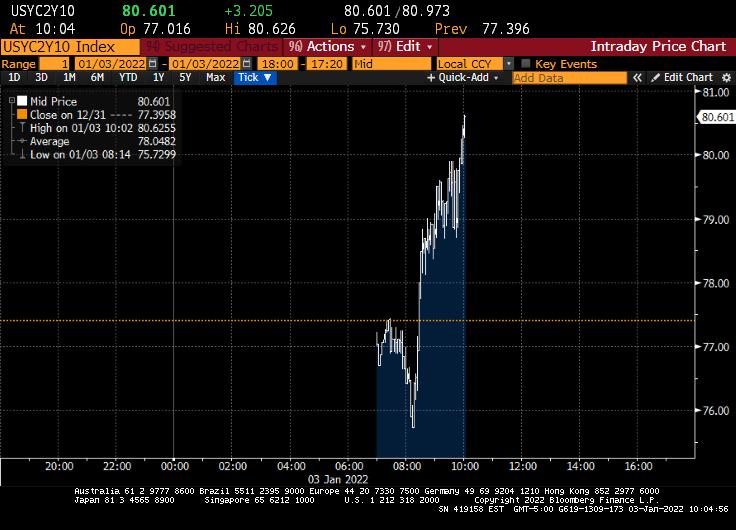

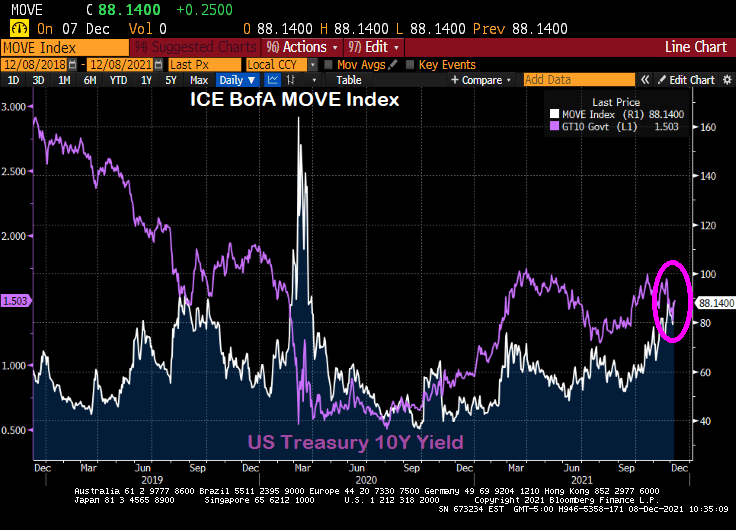

Rates tracked a jump in yields for 10-year Treasuries, which climbed to levels not seen since early 2020, before the pandemic roiled financial markets. Signs point to borrowing costs rising further as the job market improves and the Federal Reserve steps up its efforts to tame inflation.

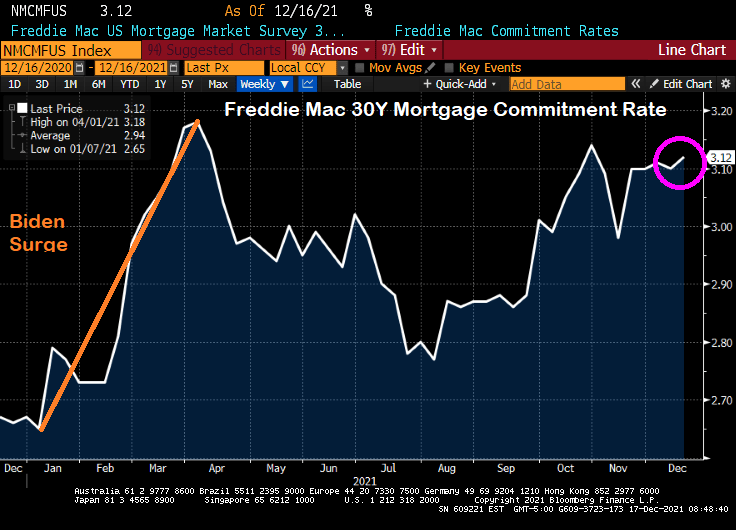

That would increase the burden on homebuyers who are already stretching to afford a purchase. Rates for 30-year mortgages tumbled to a record low of 2.65% a little more than a year ago.

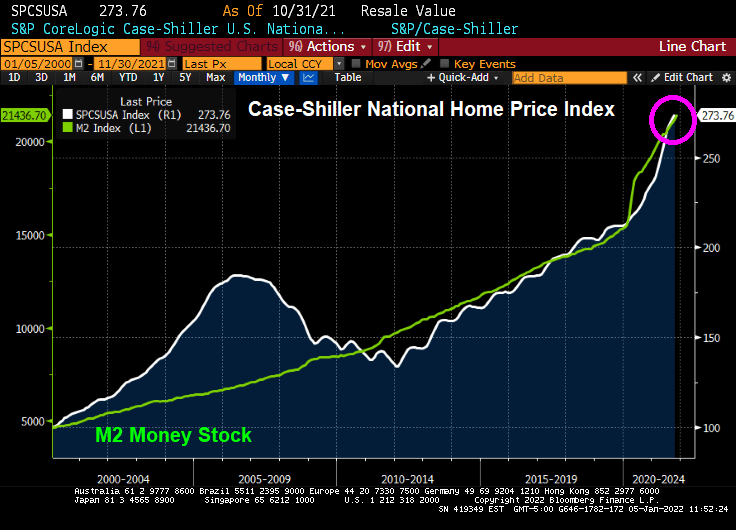

Cheap loans have helped fuel a housing rally that’s still running hot even as home prices soar out of reach for many Americans.

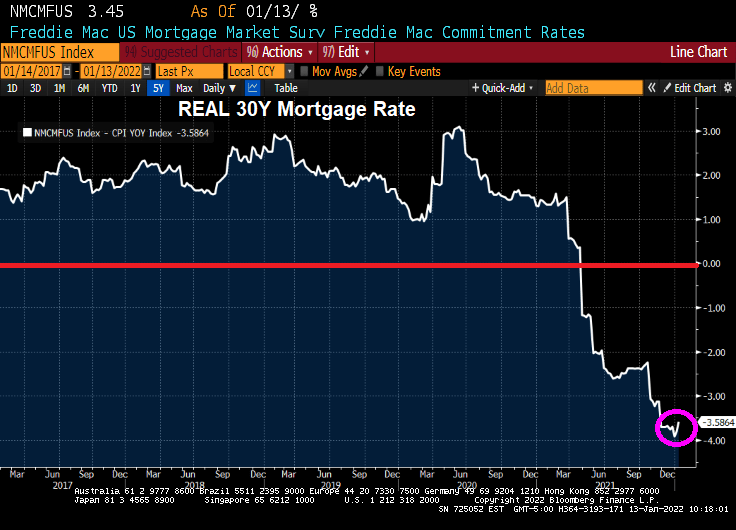

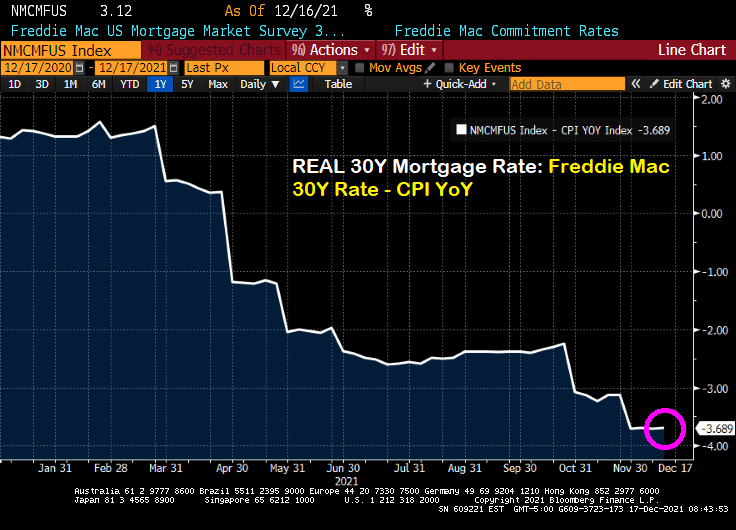

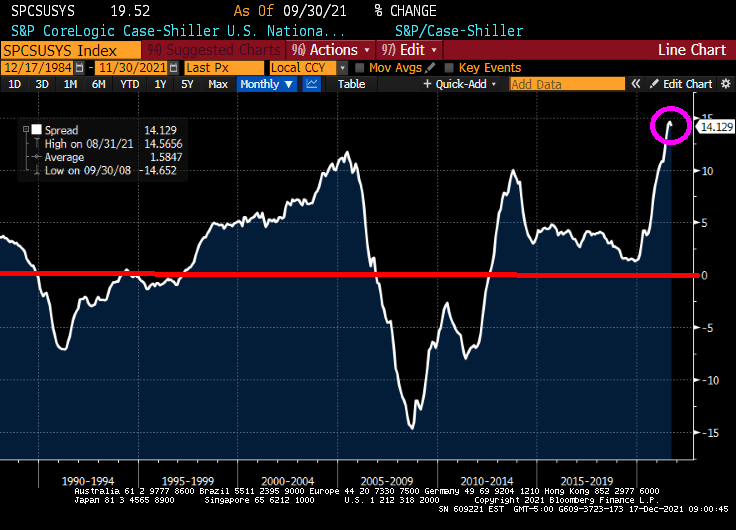

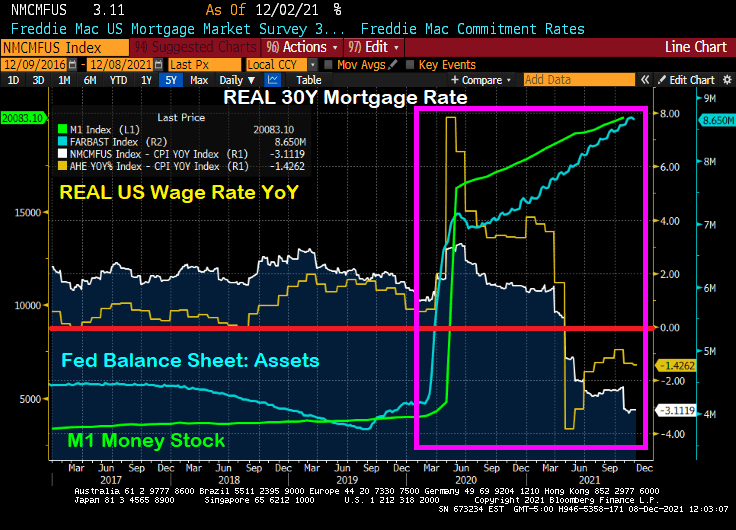

But wait! The REAL 30-year mortgage rate (nominal 30-year rate – CPI YoY) is -3.59%.

Lael Brainard, Biden’s nominee to be Vice Chairman of The Federal Reserve, has been one of the “inflation is transitory” crowd. US Senator Toomey is questioning Brainard in today’s hearing. From Toomey’s opening statement:

Last year, Governor Brainard repeatedly insisted that inflation was transitory. We have now had nine consecutive months where inflation has been more than two times the Fed’s 2% target. That makes it pretty clear that inflation is not transitory. Yesterday’s CPI release of 7.0%—the highest in 40 years—confirms that.

Inflation is a tax that is eroding Americans’ paychecks every day. Even though wages are growing, inflation is growing faster and causing workers to fall further and further behind.

At least the REAL mortgage rate is negative!

I hope Senator Toomey shows Brainard this chart of “transitory” negative wage growth.

Negative wage growth and negative REAL mortgage rates. What a total mess!

You must be logged in to post a comment.