I wonder if Biden’s Press Secretary Jen Psaki will argue that inflation is transitory … again?

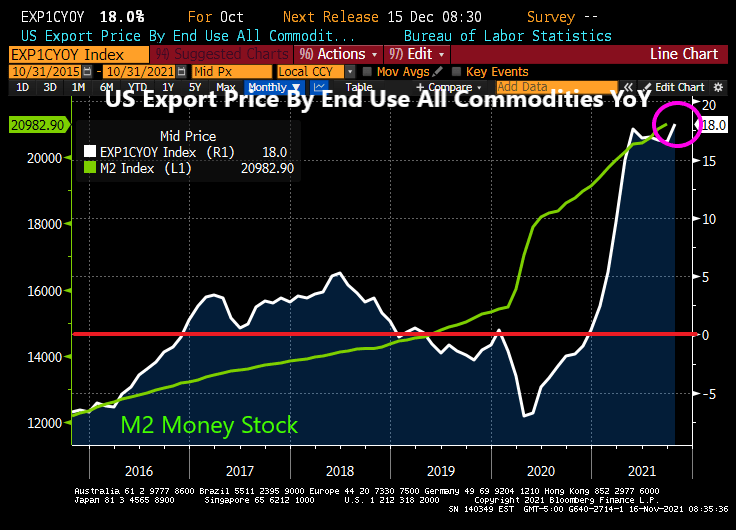

Well, the US is exporting inflation to our trading partners. US Export Prices by end use rose 18% YoY.

Of course, with the Biden Administration shutting down energy pipeline and drilling, it is not surprising.

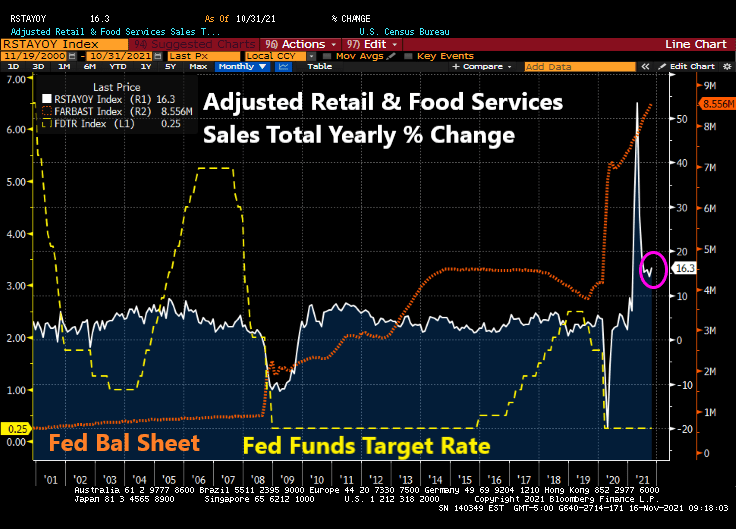

Then we have the advance retail sales numbers for October. Growing at 16.3% YoY with massive monetary stimulus still in play.

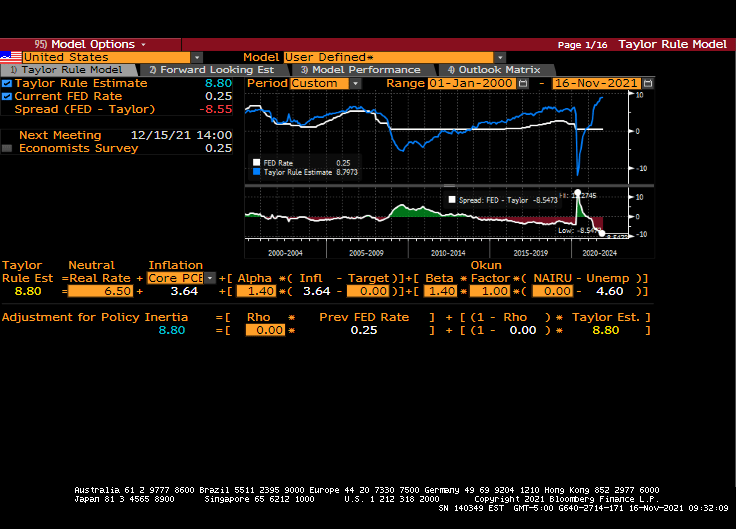

Then we have Federal Reserve Bank of St. Louis President James Bullard saying that the central bank should speed up its reduction of monetary stimulus in response to a surge in U.S. inflation.

You mean like what Mankiw’s specification of the Taylor Rule model suggests??

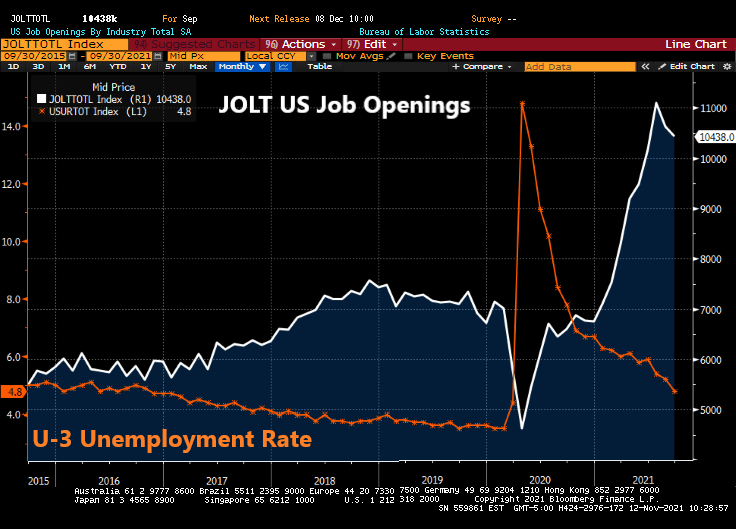

The Federal Reserve continues to JOLT markets with excessive monetary stimulus despite numerous reasons why they should back off.

For example, today’s JOLT report (US job openings) revealed that 10.4 million jobs were open in September. This is the fourth consecutive month of 1 million plus job openings, yet The Fed refuses to raise their target rate.

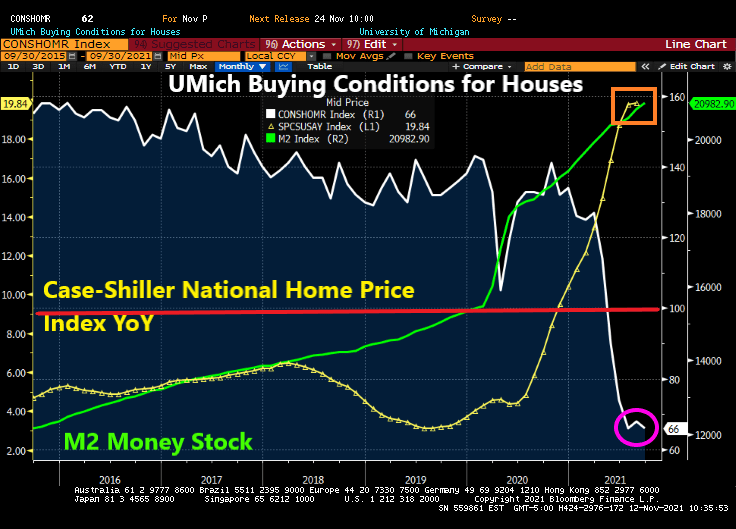

At the same time, the University of Michigan survey revealed that buying conditions for houses dropped to 66 (baseline of 100). To show how bad this is, buying conditions for houses was at 144 this time last year.

UPDATE: UMich revised their number downward to 62, the lowest since 1981.

In The Fed’s mind, they are still chasing at least 3.5% unemployment, the lowest rate under President Trump prior to COVID. But with perpetual million plus job openings GOING UNFILLED, trying to get to pre-COVID unemployment rate of 3.5% is a fool’s errand.

Of course, with The Fed helping to pump up house prices to largely unaffordable levels, it makes sense that enthusiasm for buying expensive homes has crashed.

Meanwhile, The Fed continues to JOLT the economy with excess stimulus.

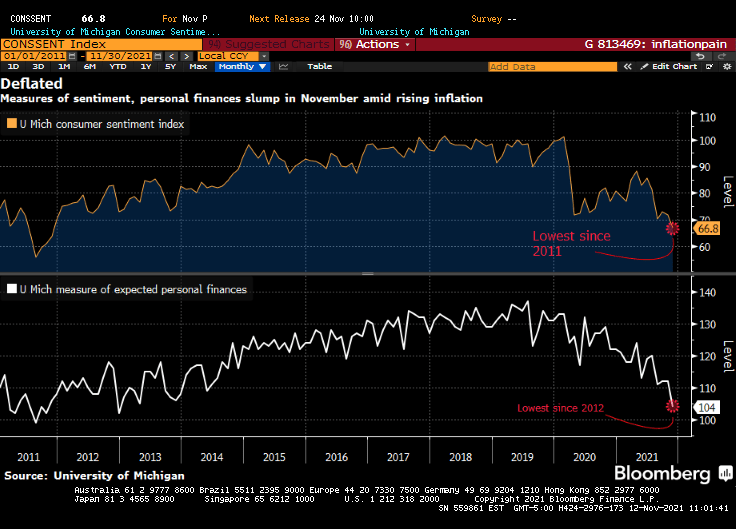

Overall inflation fears are leading to lowest consumer confidence since 2011.

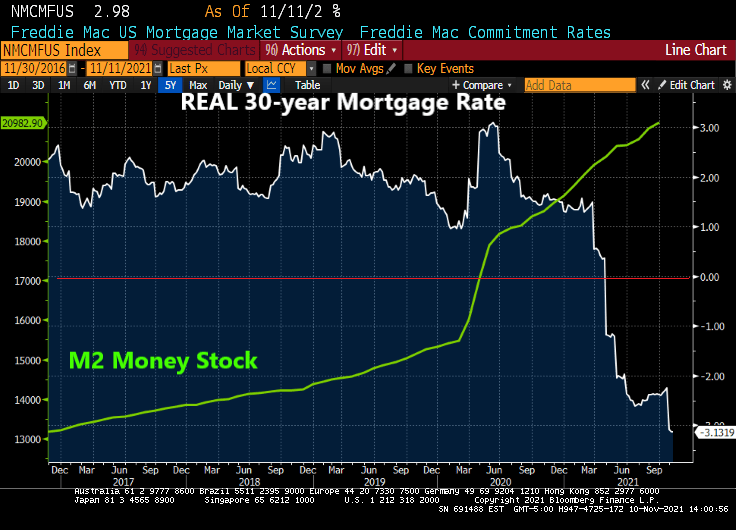

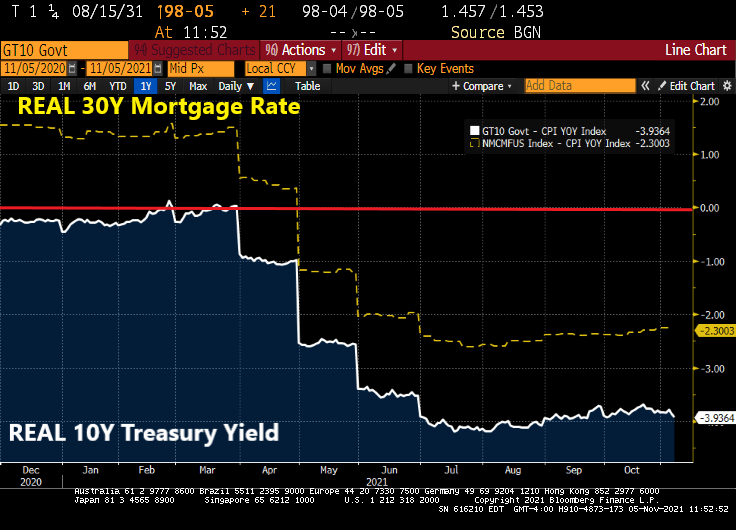

The Freddie Mac 30-year mortgage survey rate fell below 3% today to 2.98%.

And with today’s abysmal inflation report, the REAL 30-year mortgage rate fell to -3.13%.

Yes, President Biden is asking his economic council to do something about inflation. How about 1) telling The Fed to back off its outrageous and damaging stimulus and 2) stop shutting down pipelines.

Here is Joe Biden (aka, the Skipper) eyeing inflation from the White House.

Now that President Biden is interviewing Lael Brainard for Federal Reserve Chair, I am really getting a peaceless, uneasy feeling that The Fed will NEVER raise rates and inflation will be perpetual. To whit, …

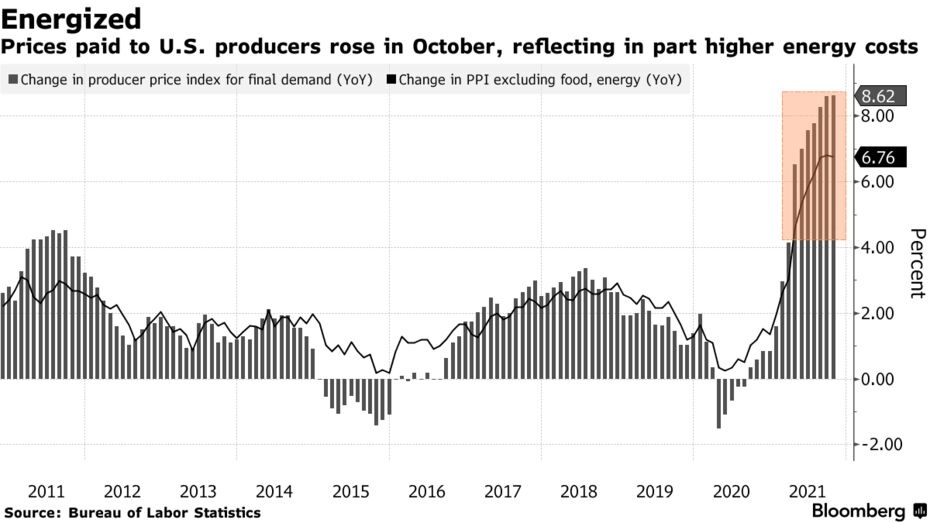

Prices paid to U.S. producers accelerated in October, largely due to higher goods costs, fueling concerns about the persistence of inflationary pressures in the economy.

The producer price index for final demand increased 0.6% from the prior month and 8.6% from a year earlier, matching forecasts, Labor Department data showed Tuesday. The annual advance was the largest in figures back to 2010.

Excluding the volatile food and energy components, the so-called core PPI rose 0.4% and was up 6.8% from a year ago.

More than 60% of the headline increase was due to goods, which jumped 1.2%. Higher energy costs, including that for gasoline, drove the gain. The cost of services rose a more moderate 0.2% for a second month, reflecting a further pullback in the cost of securities brokerages and investment advice.

The report underscores how transportation bottlenecks, materials shortages and increasing labor costs have sent prices soaring across the economy in recent months. Trucking freight costs jumped a record 2.5% from September.

Inflation is a tax created by printing too much money and stupid Federal economic policies (or follicies).

Lael Brainard? Discussing the chairmanship with Brainard could signify that the Biden team is weighing how a break with Powell might help advance their goals for the central bank. Brainard and Powell work closely together on multiple issues and are viewed as holding similar views on monetary policy, but she’s favored a tougher stance on big banks.

Remember, The Federal Reserve is a privately-owned entity independent of The Federal Government. A Brainard appointment would make The Fed the financing arm of the Democrat Party.

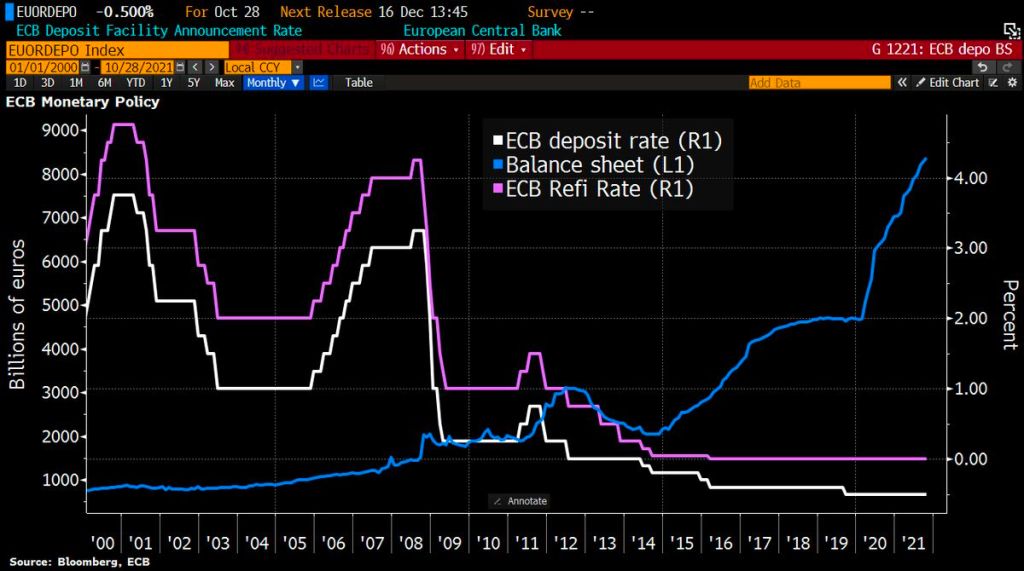

With The Federal Reserve leaving its target rate at 0.25%, but hinting at a tapering (slowdown) of asset purchases, I thought it would be good to present where The Fed sits at the moment.

You can see the rise in the effective Fed Funds rate from 2016 to early 2020, then KABOOM! COVID struck, the effective Fed Funds rate crashed while The Fed dramatically increased their purchases of Treasuries and Agency MBS. Both Treasury and Agency MBS purchases are projected to decline by mid-2022. The Fed’s target rate (purple line) is project to rise to 1% after 2023.

Where SHOULD The Fed Funds Target rate be? How about 8.80% instead of 0.25%.

So we still have over-stimulypto with The Fed projected to raise rates at a snail’s pace.

Face it, Wall Street wants interest rates low, even if inflation burns out of control.

Yes, the US economy has been greatly overstimulated by the Federal government (fiscal stimulus) and The Federal Reserve (monetary stimulus). This has caused inflation that we haven’t seen in a long time.

How overstimulated in the economy? The REAL 10-year Treasury yield (nominal less CPI YoY) is now -3.9364% and the 30-year REAL mortgage rate is -2.30%.

Nothing has been the same since Covid struck in early 2020.

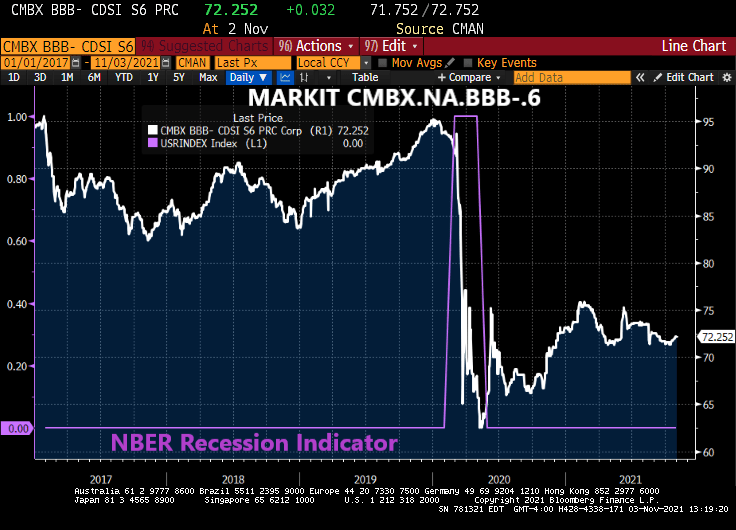

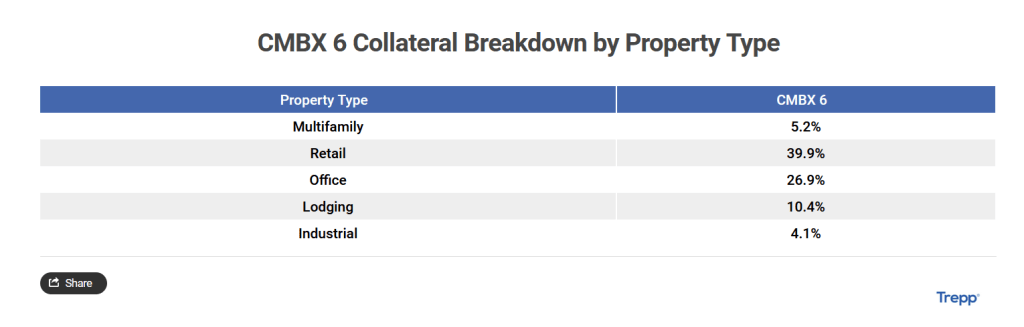

CMBX BBB-, the reference basket for CMBS 6, was climbing to around $95 prior to the Covid outbreak and resulting recession. The CMBX reference basket is now at $72.25.

CMBX 6 is largely composed of retail and office, both hit hard by Covid and the ensuing lockdowns and fearmongering by the Federal government and main street media.

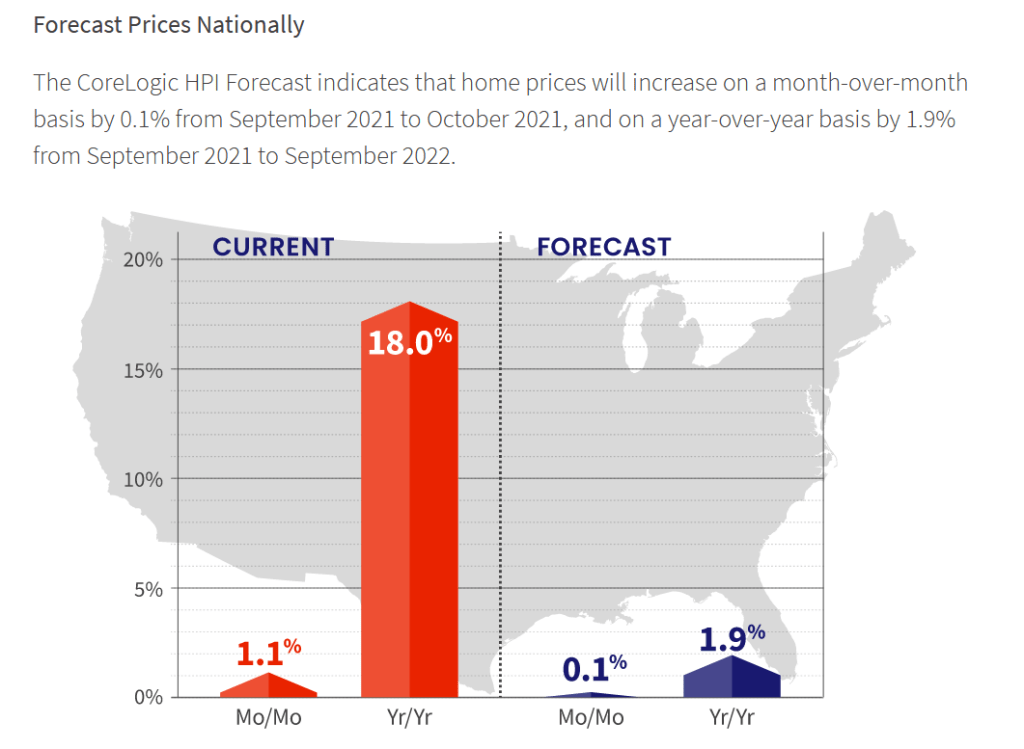

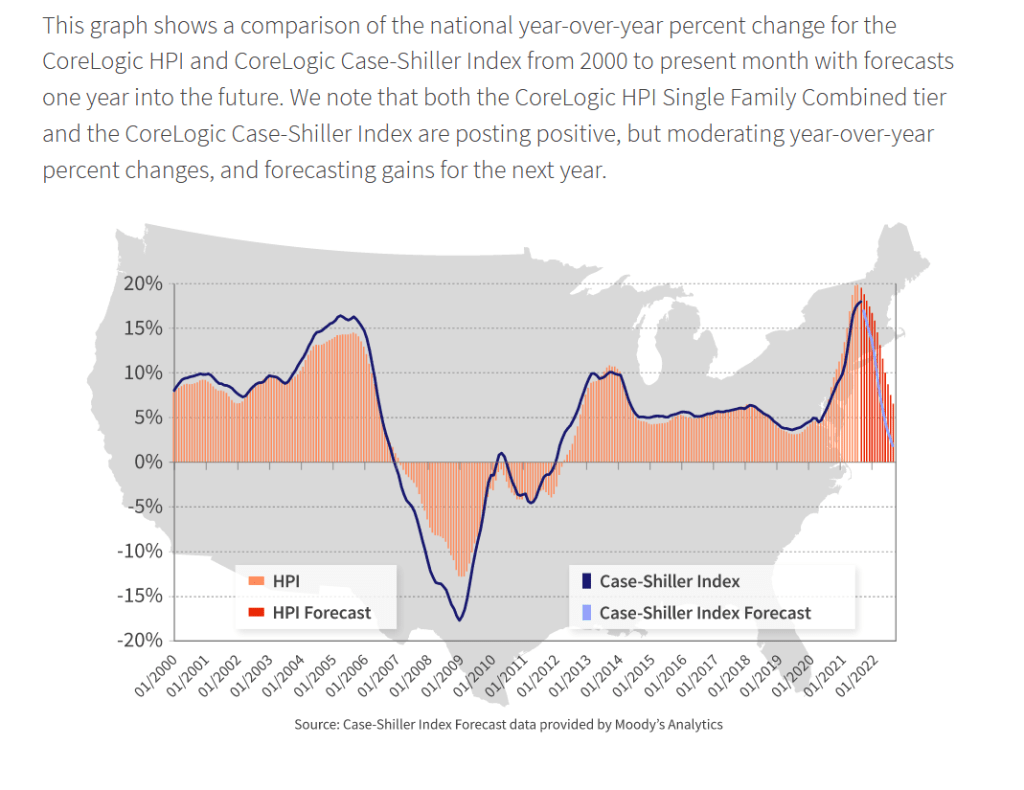

But the forecast for home price growth is for 1.9% YoY in 2022.

As home price growth crashes back to earth as wages don’t keep pace with home prices.

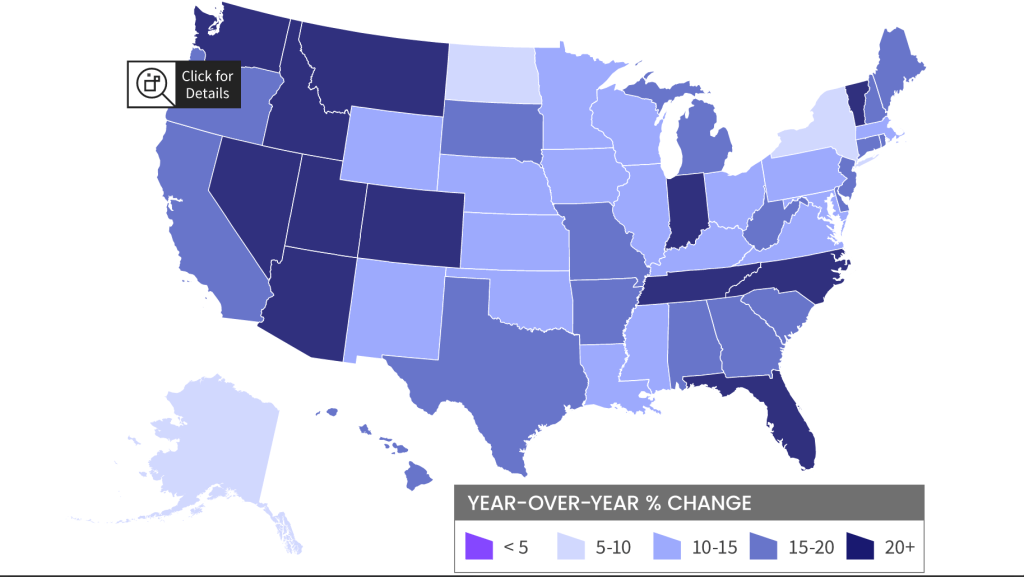

Home prices have been growing in most states out west where The Fed’s money pump has resulted in a boom in second homes and people escaping high tax California and Oregon for Nevada, Idaho, Arizona (again), Utah and Montana. The east coast is seeing the Carolinas booming along with Florida and Indiana. Escape from New York?

Escape from LA … to Arizona, Nevada, Idaho and Utah?

With central banks around the world signalling tighter policy amid rising prices, Lagarde said the ECB had done much “soul-searching” over its stance but concluded that inflation was still temporary, so a policy response would be premature.

Soul-searching? The ECB is just doing what Powell and the Fed (aka, Jerome Jett and the Blackhearts) are doing. Keeping the foot on the monetary gas pedal in the face of inflation.

Let’s start Eurozone inflation. It is now sitting a 4.10% YoY. And core inflation is sitting at 2.10% YoY. Inflation is now the highest since 2009 while core inflation is at the highest since 2001.

Like the Federal Reserve, the ECB still has its foot on the monetary accelerator pedal despite booming inflation.

So, Christine, 19 nations in “Europe” having negative 2-year sovereign yields isn’t low enough for you?

The ECB’s platform in Frankfurt reminds me of a bad TV quiz show where participants try to guess prices next year. Call it “The Price Is Wrong.”

Unless, of course, the ECB sees a massive depression ahead.

(Bloomberg) — The largest owner of U.S. rental houses isn’t seeing any let-up in demand, or in its ability to increase rents.

Invitation Homes Inc., which owns more than 80,000 single-family rentals, raised prices by nearly 11% in the third quarter, according to a statement. The company boosted rents by 8% on renewals and 18% when leasing homes to new tenants. Rates are rising fastest in the Southwest, where rents increased 30% on new leases in Las Vegas, and 29% in Phoenix.

“It’s a little bit crazy,” Chief Executive Officer Dallas Tanner said on a conference call with investors Thursday. “There just isn’t enough quality housing available right now.”

Rising rents have been a staple of the economy since early Covid lockdowns lifted in the middle of last year. Surging purchase prices have pushed homeownership out of reach for first-time buyers.

Invitation’s properties, which tend be more centrally located than those owned by other institutional landlords, have been especially popular. And tenants tended to stay put: The company had a record-low turnover rate in the quarter, which reduced the expenses associated with preparing a house for leasing.

Invitation’s shares rose slightly to $40.77 at 12:49 p.m. New York time after the company raised its expectations for full- year revenue and net operating income. The stock is up 37% for the year.

As Milton Friedman once said, “If you put the federal government in charge of the Sahara Desert, in 5 years there’d be a shortage of sand.” In this case, The Federal government and Federal Reserve were put in charge of the Covid epidemic and we have shortages of almost everything. Including housing.

I don’t have Invitations rent growth chart, but here is Zillow’s YoY rent chart against The Fed’s balance sheet.

The good news? The 11% increase is almost half of the 20% YoY Case-Shiller National home price index.

Here is Treasury Secretary Janet Yellen making housing supply disappear.

You must be logged in to post a comment.