So much for the “Trump has ruined the economy” mantra of politicians and celebrities.

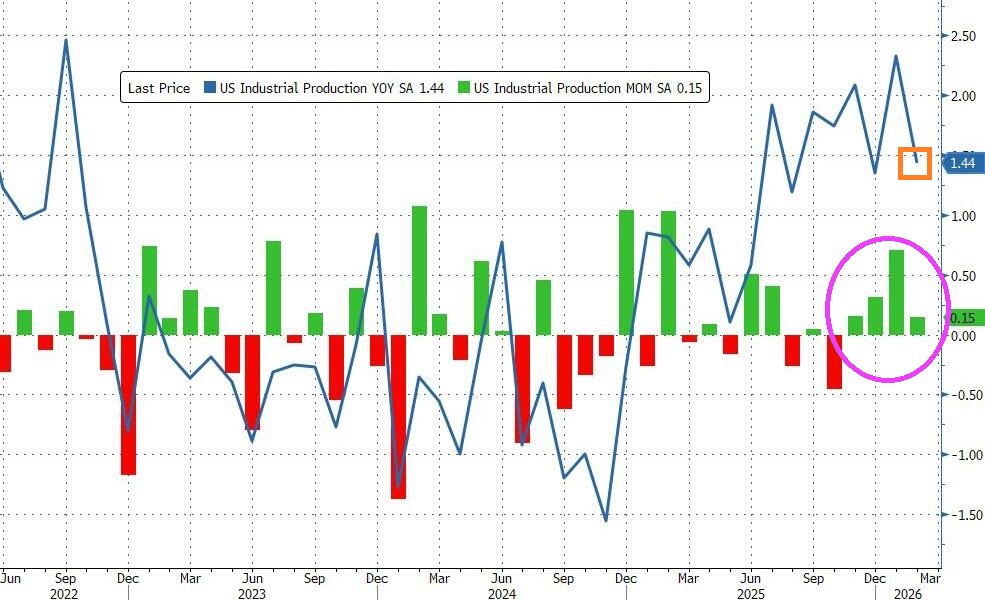

After a strong gain in January, US Industrial Production continued to expand in February, rising 0.2% MoM (better than expected +0.1%) – the fourth straight month of gains with Production up 1.44% YoY.

Source: Bloomberg

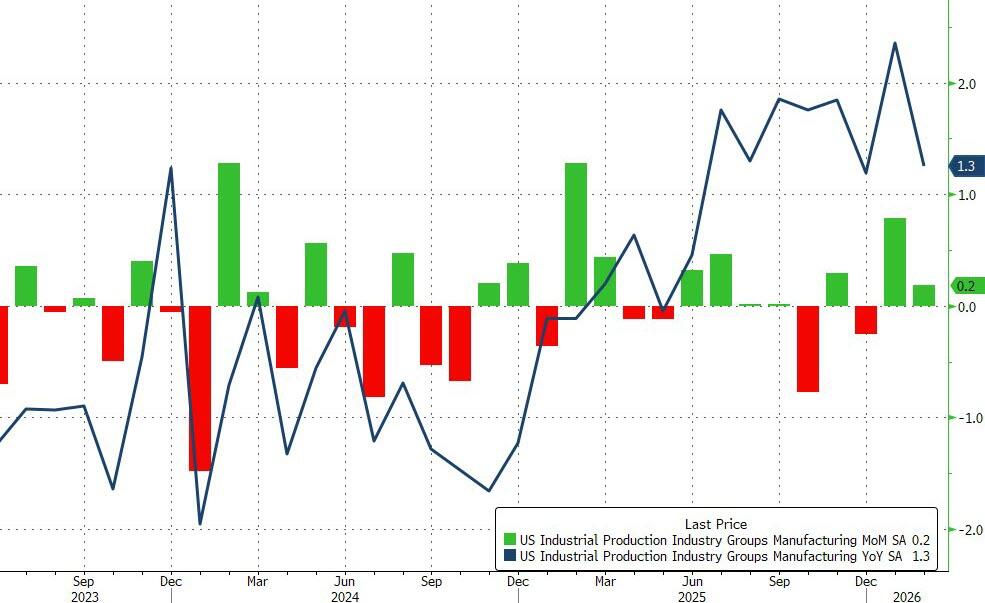

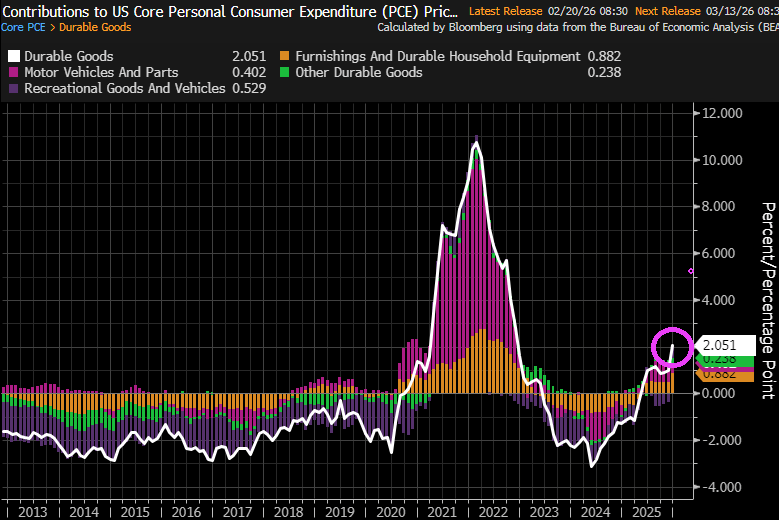

Manufacturing output also beat expectations, rising 0.2% MoM in February.

- Durable manufacturing output edged up 0.1 percent, with mixed results across categories; the index for motor vehicles and parts posted the largest gain, and the index for machinery posted the largest loss.

- Nondurable manufacturing output rose 0.2 percent, with gains in the production of chemicals, of plastic and rubber products, and of paper products outweighing declines in the output of petroleum and coal products and of food, beverage, and tobacco products. The output of other manufacturing (publishing and logging) rose 1.3 percent.

- Mining output increased 0.8 percent in February, following a 0.9 percent increase in January. The output of utilities fell 0.6 percent in February, reflecting no change in the index for electric utilities and a 4.7 percent drop in the index for natural gas utilities.

Source: Bloomberg

Capacity Utilization printed 76.3 (better than expected)…

…maintaining the positive trend since Trump’s second term began.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.