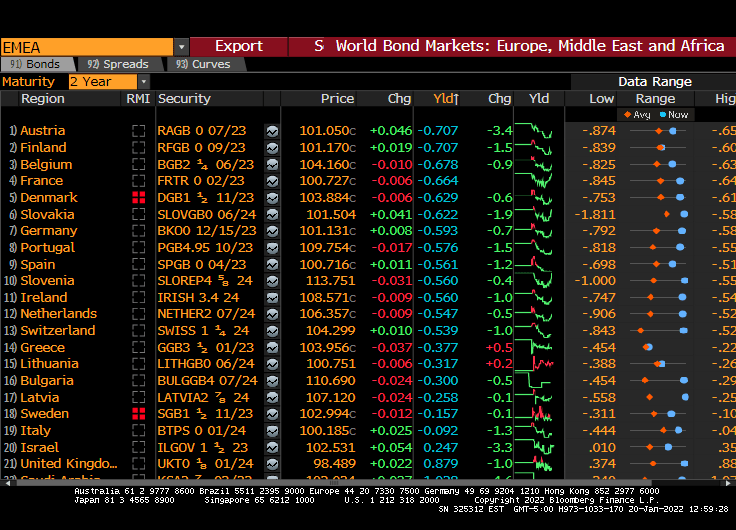

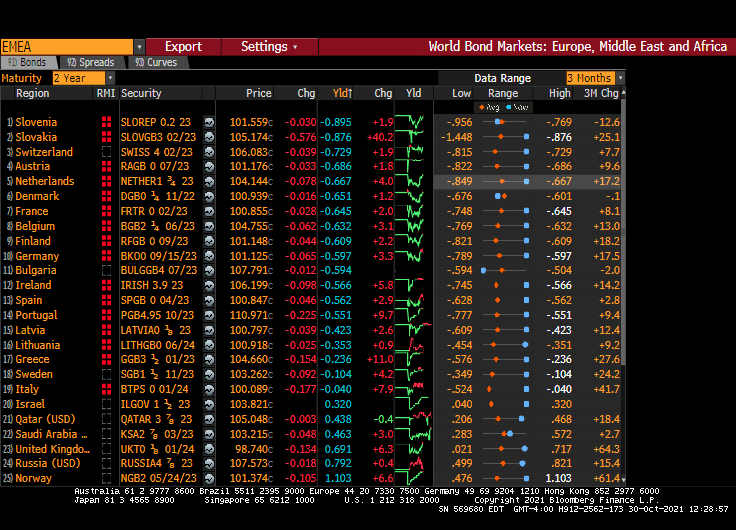

Let’s see how The Federal Reserve is going to compete with other central banks when 19 European nations have negative 2-year sovereign yields. Call them the “Nervous 19.” Note that France has the lowest 2Y yield of the big 3 (France -0.664%, Germany -0.593% and Italy -0.092%).

True, The Fed’s reaction to COVID shutdowns was more extreme than the ECB’s reaction.

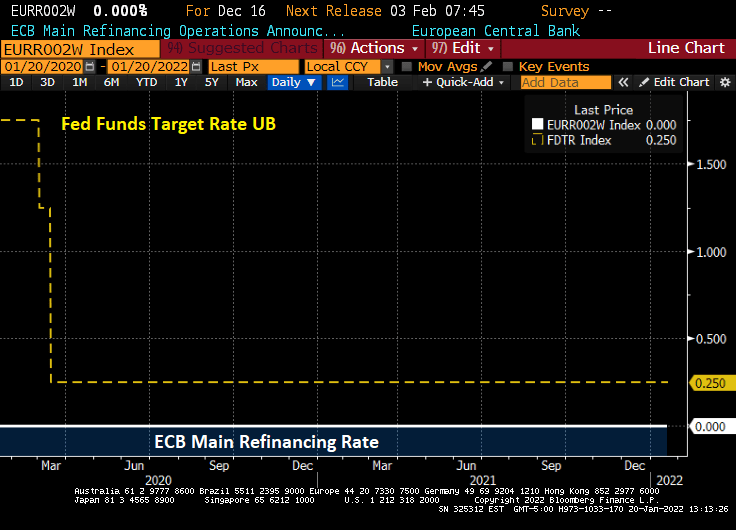

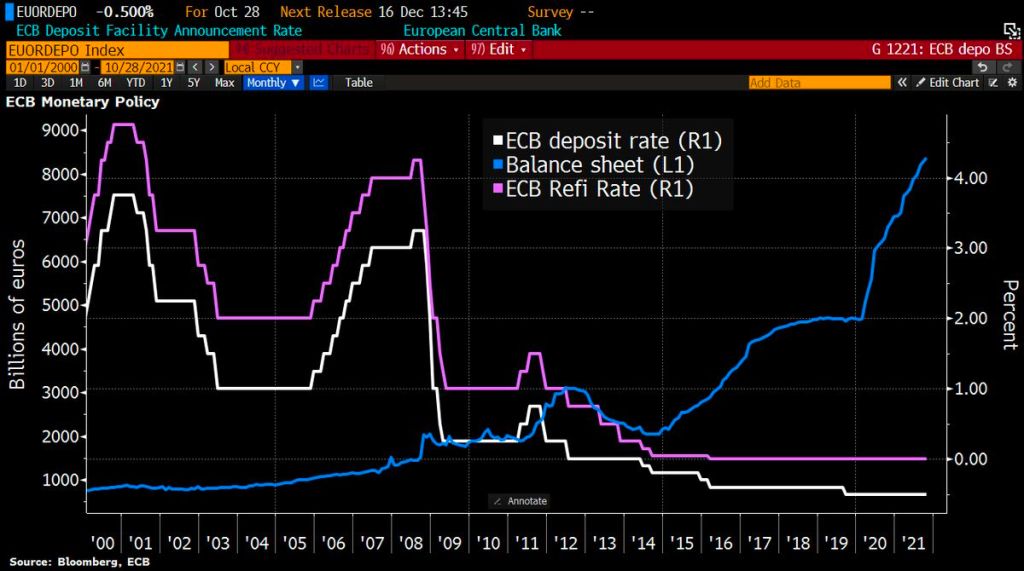

The ECB’s main refinancing rate is 0% and The Fed’s target rate is 0.25%.

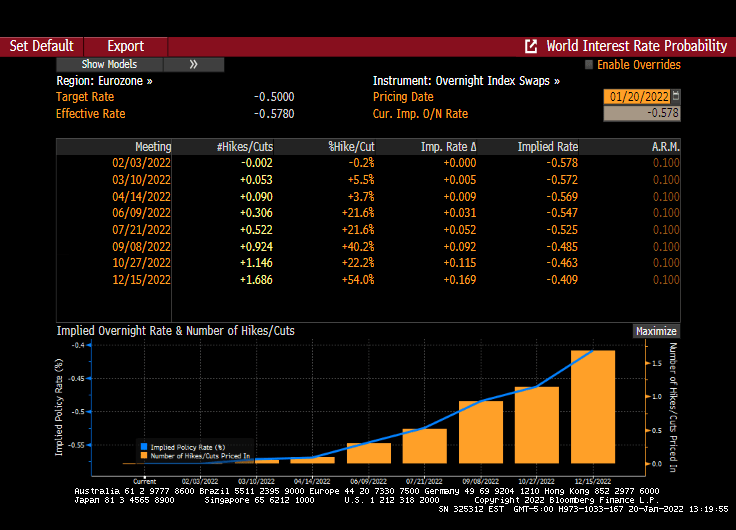

Unlike the US with its 4 expected rate increases, the Eurozone is pricing in only 1 rate increase for 2022 … in October.

The ECB’s monetary policy is as stiff as French President Emmanuel Macron.

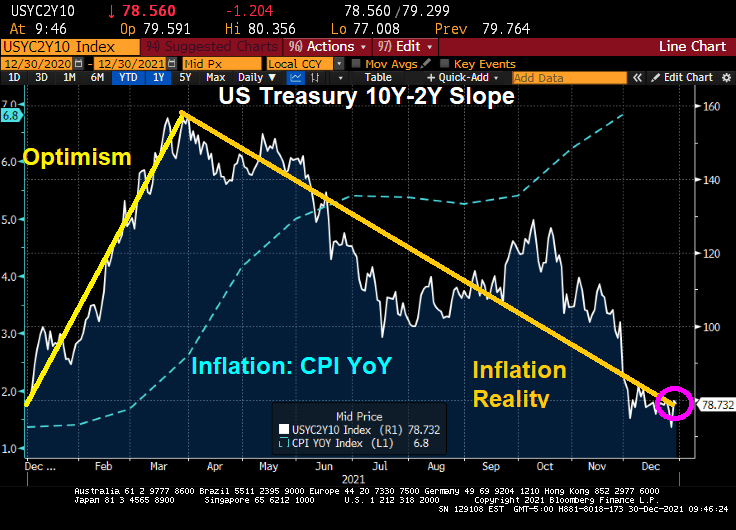

It has been almost a year since Joe Biden has been President of the United States and a Democrat majority took control of The House and Senate. And what has happened to the US Treasury yield curve slope over the past year?

The yield curve is back where it started. There was the “honeymoon effect” where the curve slope rose. After all, Biden was Obama’s Vice President for 8 years and The Democrats has promised so much in the 2020 election. But by early April, the reality of the massive Federal spending (combined with Fed Stimulypto) began showing what was feared: inflation (blue line) started to grow at a rapid rate of speed. With inflation now at 6.8% YoY,

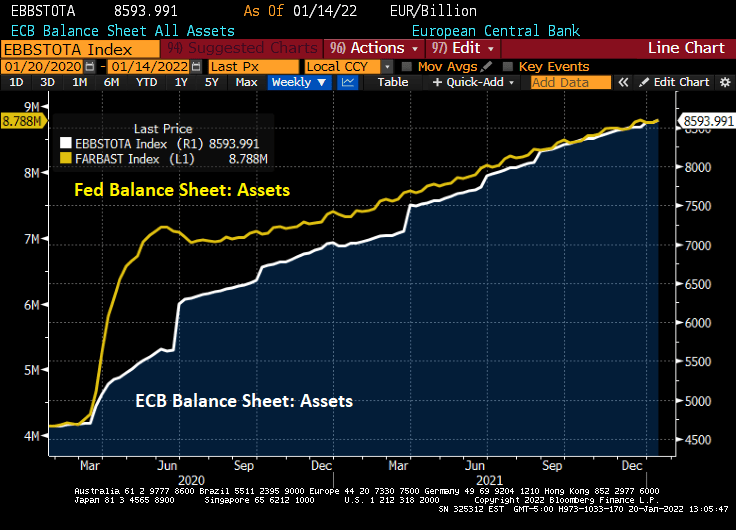

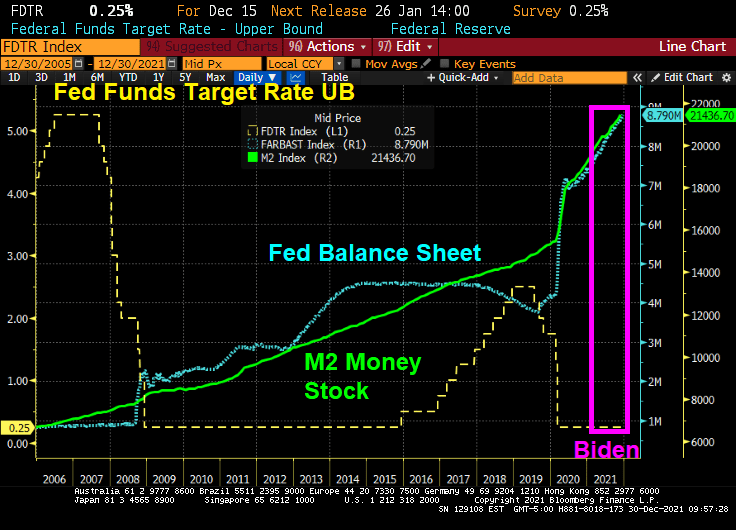

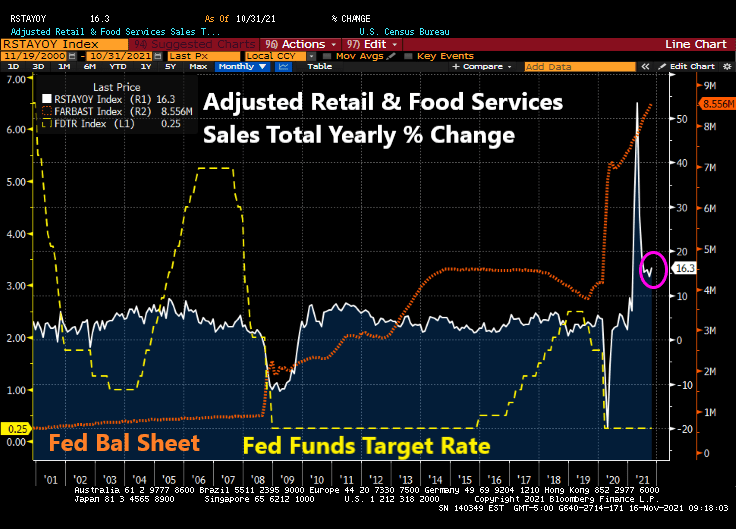

In fairness to Biden, The Federal Reserve has been overstimulating the economy since The Federal Reserve since Ben Bernanke and the Fed Open Market Committee (FOMC) dropped the hammer on The Fed Funds Target Rate once the rate hit 5.25% in September 2007. They kept cutting it reached 25 basis points (or 0.25%) in December 2008. In August 2008, Bernanke and Company began their “Quantitative Easing” or asset purchasing programs. Between The Fed’s Target Rate and QE, The Fed has continued to overstimulate markets ever since. Under Biden, The Fed Funds Target Rate remains at 0.25% and The Fed’s Balance sheet has grown to $8.79 Trillion (bigger than the entire economies of Japan and Germany put together!).

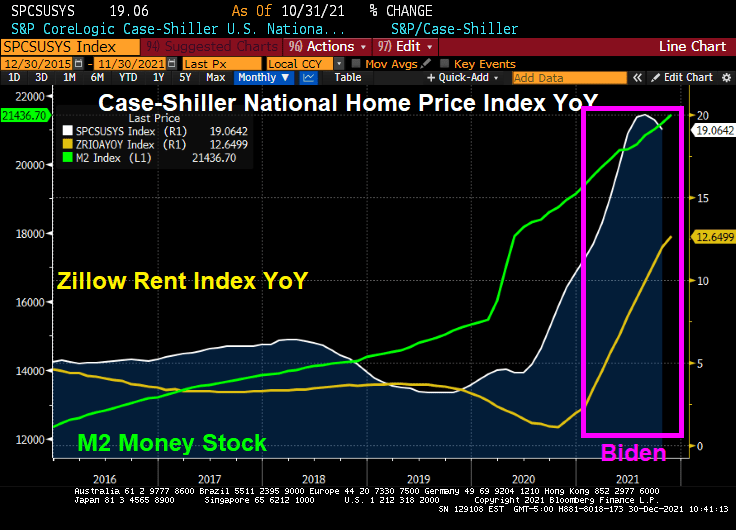

How about housing? Home prices are growing at 19% YoY while rents are growing at 12.65% YoY.

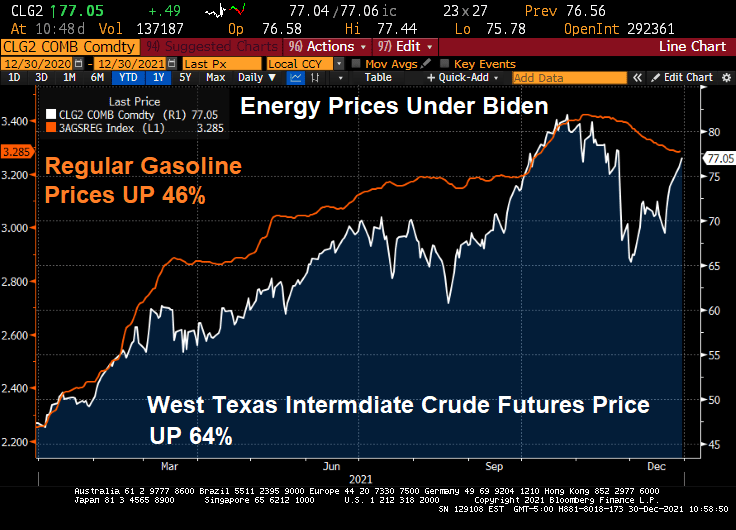

Energy prices have risen dramatically under Biden. Gasoline is up 46% despite a slight reprieve recently. WTI crude prices are up 64%.

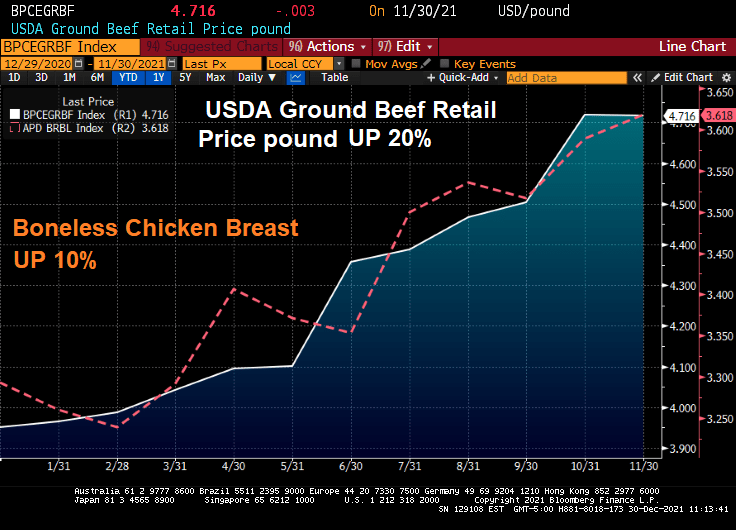

How about food? Beef prices are up 20% and chicken prices are up 10%.

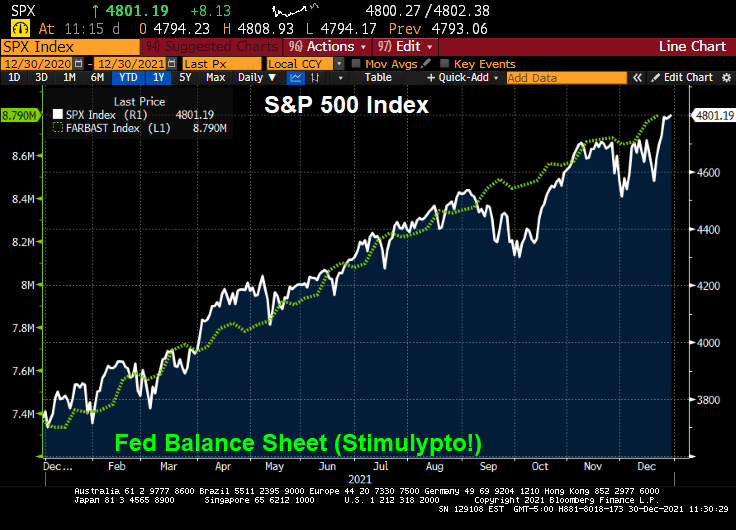

On a positive note, the S&P 500 index has soared … thanks has soared during Biden’s term thanks to Fed stimulus and Federal spending on COVID.

The Build Back Better Act if passed (in its entirety or on a piecemeal basis) will lead to even MORE inflation.

Perhaps Biden’s spokesperson Jen Psaki can recreate the Biden Administration as a lovable, hilarious family like the comic strip Gasoline Alley with old Joe Biden as Skeezix. And insider-trading star, House Speaker Nancy Pelosi as the family matriarch.

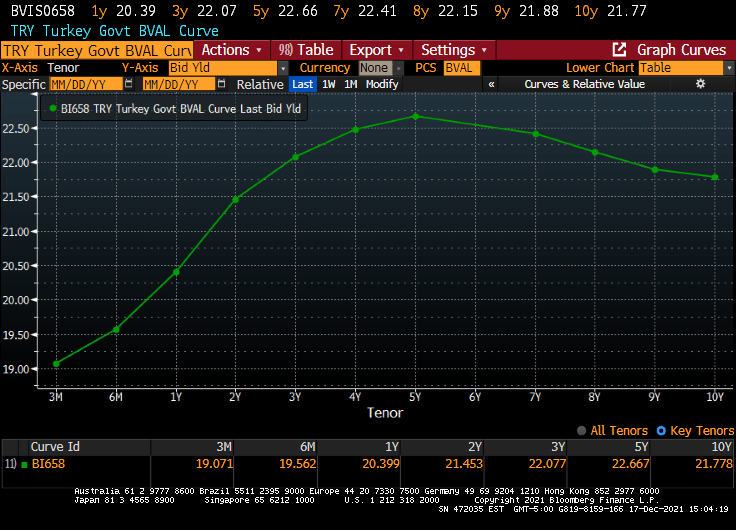

Turkey (the nation, not the bird) is now the Venezuela of Europe/Middle East, where insane government policies are destroying both nations.

(Dow Jones) — Turkey’s central bank intervened to arrest the plunge in the country’s currency, which lost as much as 8% of its value against the dollar on Friday in an ongoing crisis that is straining the country’s financial system.

The crash followed another decision by the central bank on Thursday to cut interest rates under pressure from President Recep Tayyip Erdogan, who favors lower rates as a part of a vision to grow the Turkish economy. Mainstream economists have urged the government to raise interest rates to control Turkey’s rising inflation, which reached more than 21% last month, according to official statistics.

The ongoing plunge is putting increasing pressure on ordinary Turks who have seen their savings evaporate, and adding to pressure on the banking system which has high levels of foreign-currency-denominated loans to repay within the next 12 months.

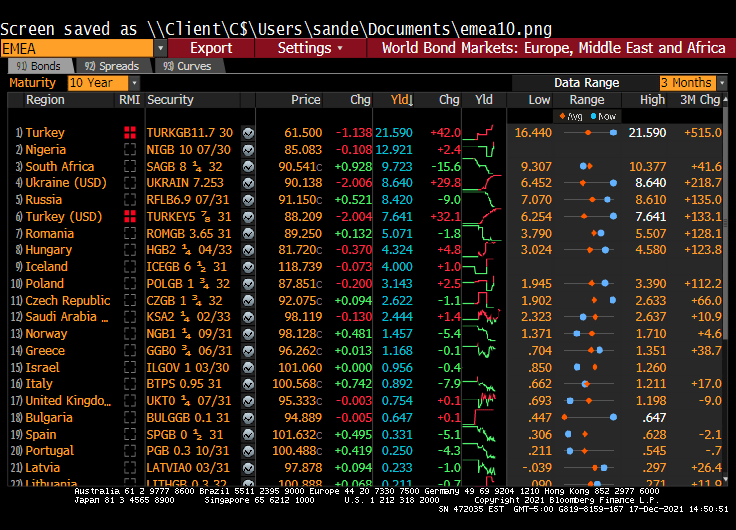

Wow. Turkey’s 10-year sovereign yield rose 42 BPS today to 21.590%. Turkey is looking like the Venezuela of Europe and the Middle East.

The Turkish sovereign curve in their home currency is humped.

But the Turkish yield curve (in US Dollars) looks more like the US Treasury actives curve.

The Turkish Lira is crashing against the US Dollar.

Meanwhile, the Central Bank of Turkey is cutting their repo rate as inflation soars. WTF???

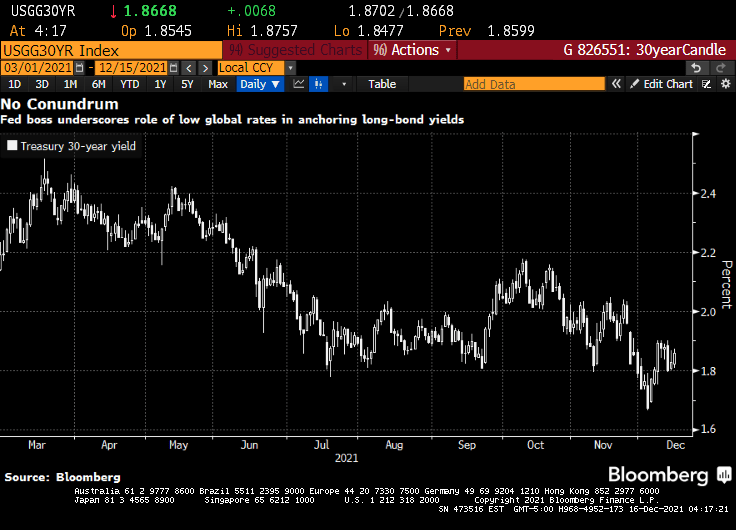

Like John Belushi from The Blues Brothers, Fed Chair Jerome Powell is saying that the markets lackluster response in terms of bond yields to his “hawkish” announcement yesterday “isn’t his fault.”

(Bloomberg)Federal Reserve boss Jerome Powell appears unperturbed by the fact that longer-term bond yields remain low even as officials lay the ground work for tighter policy and inflation is ticking higher.

While the drop in longer-term rates may be viewed by some as indicative of where so-called terminal rates for U.S. policy might ultimately lie, Powell on Wednesday emphasized the impact of ultra-low yields in places like Japan and Germany in helping to keep them anchored.

“A lot of things go into the long rates and the place I would start is just look at global sovereign yields around the world,” Powell said at a news conference following the Fed’s final scheduled policy meeting for the year, which saw officials ramp up the pace of stimulus withdrawal and boost predictions for rate hikes in 2022. The Fed Chair noted that rates on Japanese and German government bonds are “so much lower” than those on Treasuries and that with currency hedging taken into account American debt provides investors with a higher yield. “I’m not troubled by where the long bond is,” he said.

This stands as something of a contrast to the view expressed back in 2005 by one of Powell’s predecessors. Back then, Fed chief Alan Greenspan described a decline in long-term bond yields even in the face of six policy rate increases as a “conundrum.”

Or it could be that no one REALLY believes that Central Banks will ever cut interest rates, despite surging inflation.

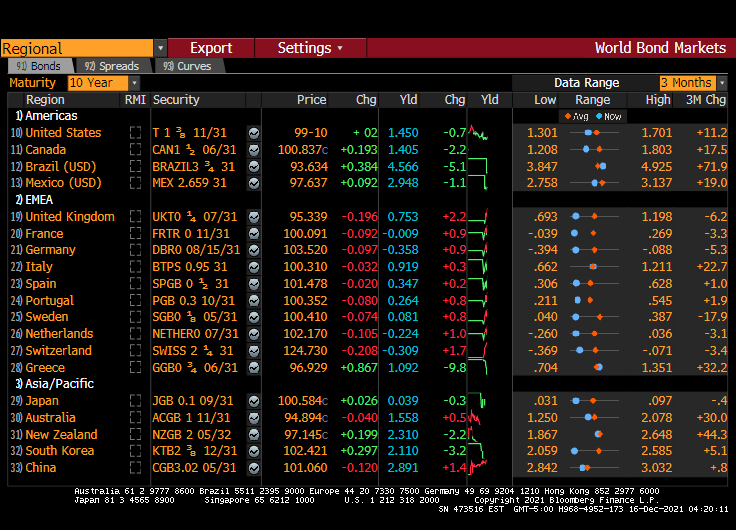

The US Treasury 10-year yield dropped 7 basis points overnight and remains just south of 1.50%. The Eurozone remains below 1% (with Germany at -0.358% and France at -0.009% at the 10-year mark). Japan is at 0.039%. This is what Powell means by low global rates keeping US long-term rates down.

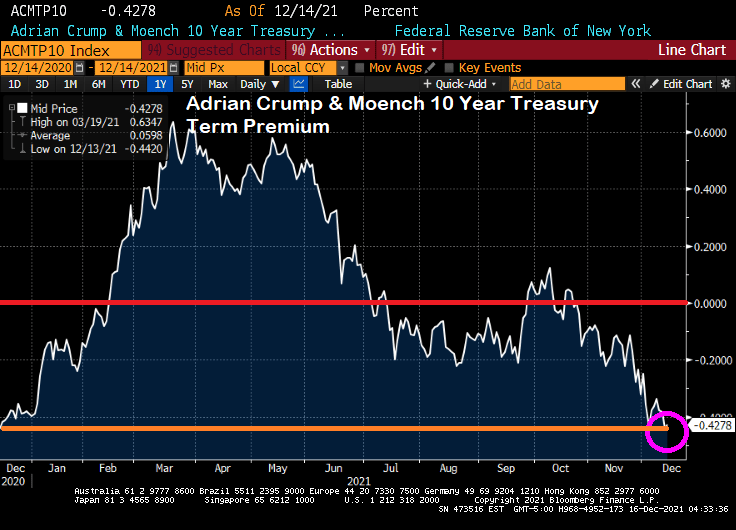

The 10-year Treasury term premium (measured before Powell’s head fake on raising rates) has returned to pre-Biden levels.

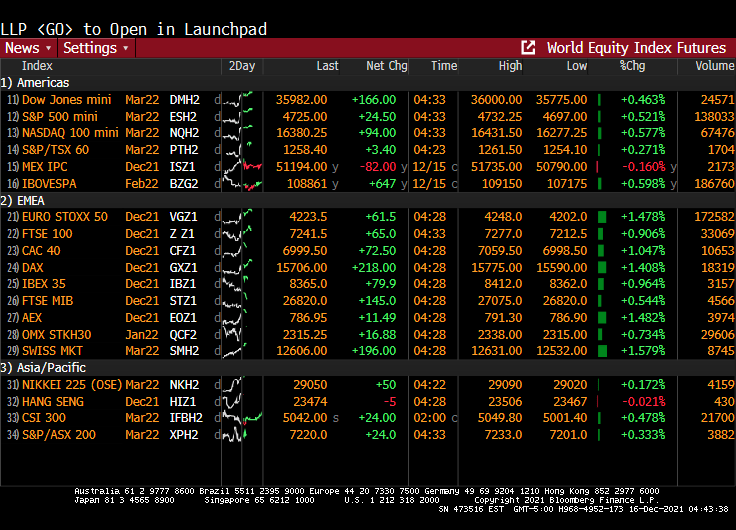

Meanwhile, global equities futures are up across the board (well, except for Mexico).

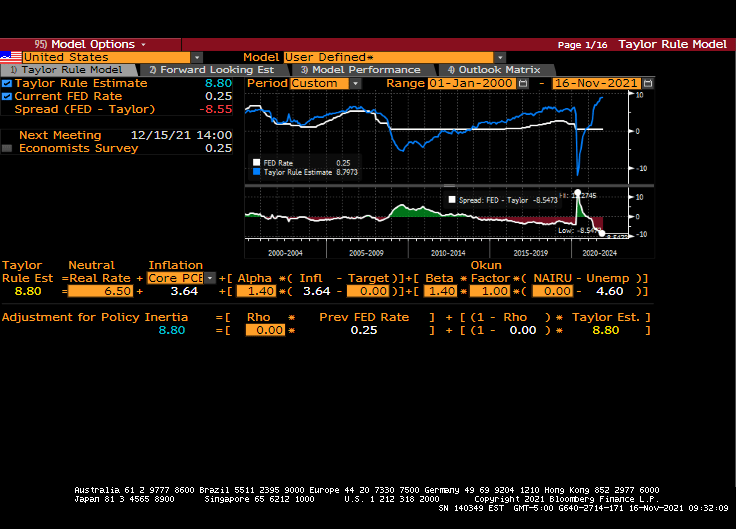

The Fed could have raised their target rate if they were REALLY interested in cooling inflation. The Taylor Rule remains at 14.94% while The Fed is stalled at 0.25%. Even if you don’t like the Taylor Rule, it still highlights how ridiculous Fed Stimulypto is.

Well, we do have a government-propelled economic recovery, but at a cost of declining REAL wages thanks to the highest inflation rate in 40 years.

I wonder if Biden’s Press Secretary Jen Psaki will argue that inflation is transitory … again?

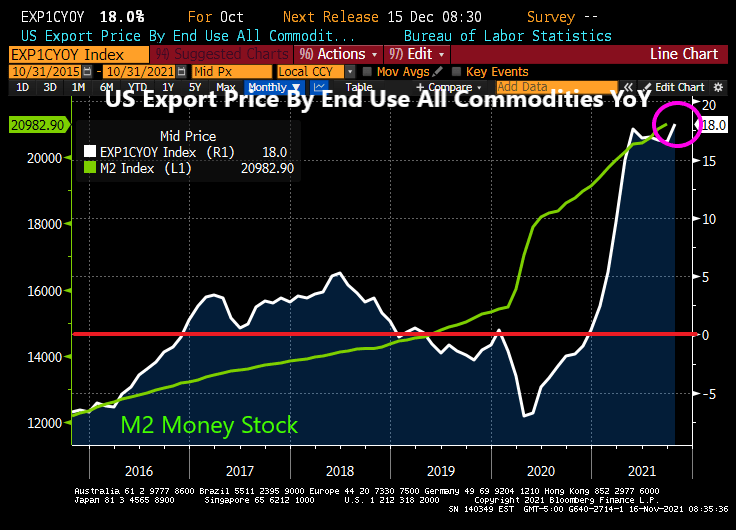

Well, the US is exporting inflation to our trading partners. US Export Prices by end use rose 18% YoY.

Of course, with the Biden Administration shutting down energy pipeline and drilling, it is not surprising.

Then we have the advance retail sales numbers for October. Growing at 16.3% YoY with massive monetary stimulus still in play.

Then we have Federal Reserve Bank of St. Louis President James Bullard saying that the central bank should speed up its reduction of monetary stimulus in response to a surge in U.S. inflation.

You mean like what Mankiw’s specification of the Taylor Rule model suggests??

With central banks around the world signalling tighter policy amid rising prices, Lagarde said the ECB had done much “soul-searching” over its stance but concluded that inflation was still temporary, so a policy response would be premature.

Soul-searching? The ECB is just doing what Powell and the Fed (aka, Jerome Jett and the Blackhearts) are doing. Keeping the foot on the monetary gas pedal in the face of inflation.

Let’s start Eurozone inflation. It is now sitting a 4.10% YoY. And core inflation is sitting at 2.10% YoY. Inflation is now the highest since 2009 while core inflation is at the highest since 2001.

Like the Federal Reserve, the ECB still has its foot on the monetary accelerator pedal despite booming inflation.

So, Christine, 19 nations in “Europe” having negative 2-year sovereign yields isn’t low enough for you?

The ECB’s platform in Frankfurt reminds me of a bad TV quiz show where participants try to guess prices next year. Call it “The Price Is Wrong.”

Unless, of course, the ECB sees a massive depression ahead.

Federal Reserve Chair Jerome Powell sounded a note of heightened concern over persistently high inflation as he made clear that the central bank will begin tapering its bond purchases shortly but remain patient on raising interest rates.

“The risks are clearly now to longer and more persistent bottlenecks, and thus to higher inflation,” Powell said Friday during a virtual panel discussion hosted by the South African Reserve Bank and moderated by Bloomberg’s Francine Lacqua.

“I would say our policy is well-positioned to manage a range of plausible outcomes,” he said. “I do think it’s time to taper and I don’t think it’s time to raise rates.”

Good luck with that, Jay! You are going to raise the short-end of the yield that will lead to a flattening of the Treasury yield curve. But you are going to continue to buy Treasuries and Agency MBS in order to monetize the rampant spending by Congress and the Biden Administration? C’mon man!

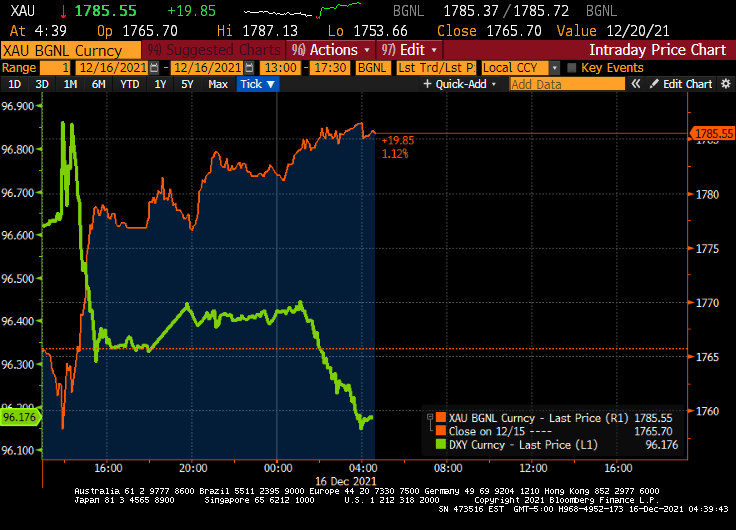

You can see where Powell spoke today. It is when gold tanked along with the 10-year Treasury yield. Both rebounded a bit, but the 10-year Treasury yield continue its fall to 1.6324%.

The US dollar (green) fell when Powell opened his pie-hole. But Bitcoin (blue) fell in advance as if they knew what Powell was going to say.

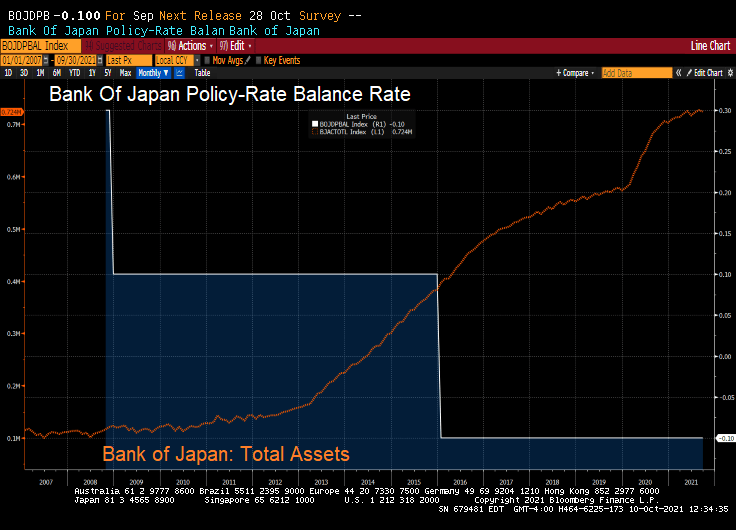

What’s left of it is that the BoJ (and Bank of Japan Governor Haruhiko Kuroda) now holds about half of the huge pile of the central government’s debt. With their target rate at -0.10% and a gargantuan balance sheet, what could go wrong?

But BOJ’s QE has ended. The BoJ’s overall assets stopped growing, and its holdings of government bonds have started to decline.

As of the BoJ’s balance sheet dated September 30, released on Thursday, total assets declined to a still monstrous ¥724 trillion ($6.4 trillion), below where it had been in May 2021.

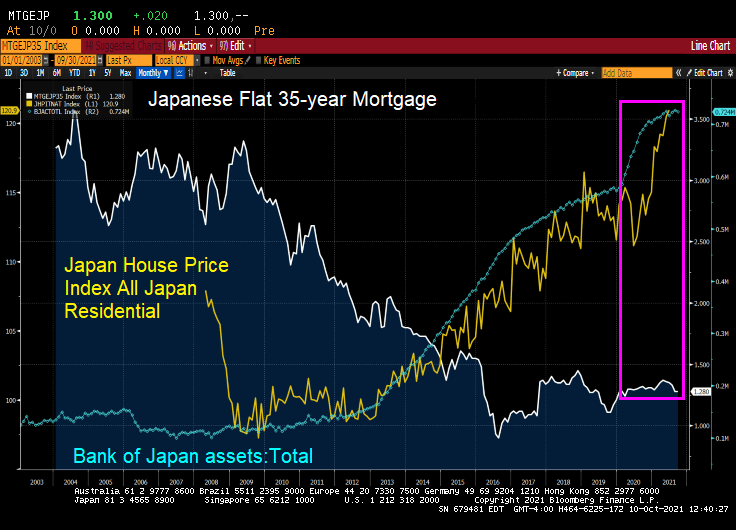

But look at Japanese home prices with the growth of the BOJ’s balance sheet and general decline in mortgage rates. Like the USA, there was a balance sheet spike associated with Covid and a resulting spike in home prices.

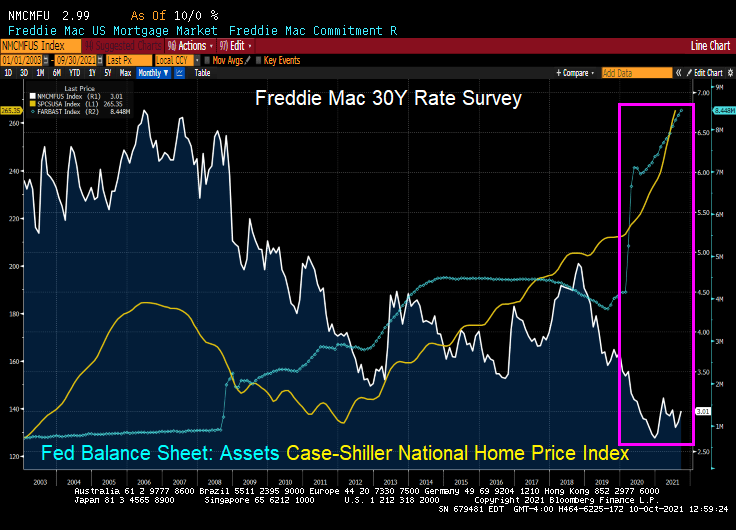

The USA? We also saw a surge in home prices following The Fed’s monetary “stimulypto.”

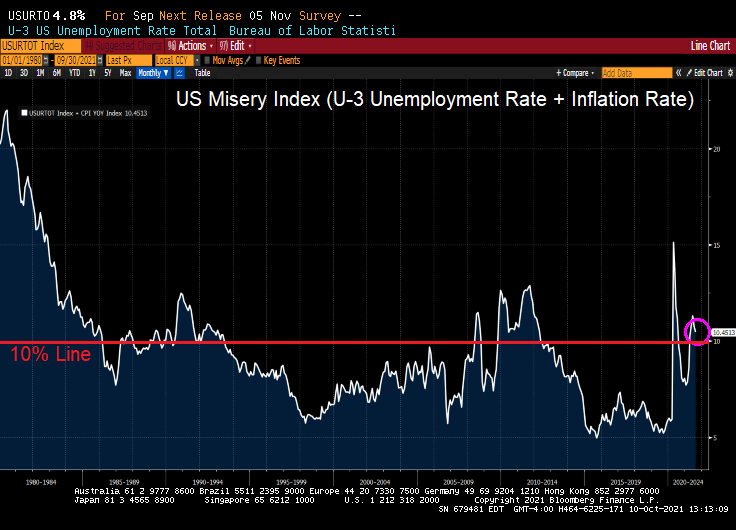

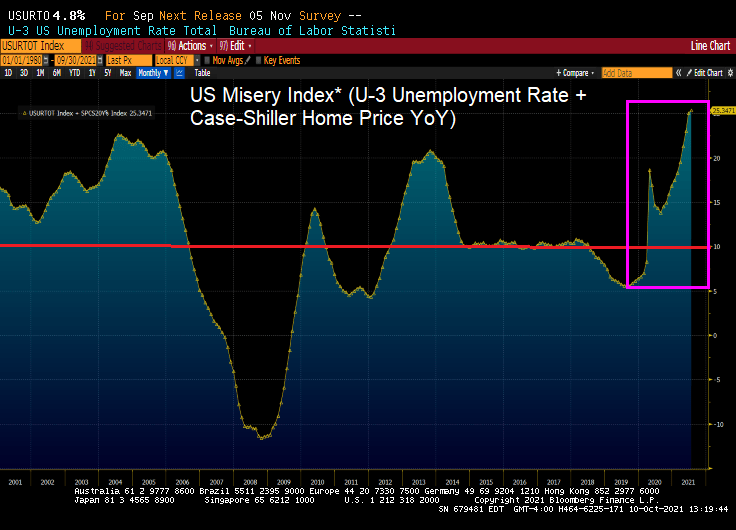

Bear in my that the US Misery Index is above 10% (U-3 unemployment + inflation).

And if I define the US Misery Index as U-3 unemployment + home price growth, we can see we are at record misery rates. Miserable for households that don’t own a home or are trying to move to a higher housing price area).

Central banks are turning “hawkish” in the face of inflation.

(Bloomberg) — Treasuries fell, sending 10-year yields to a three-month high, as traders braced for a testing week of heavy bond auctions and continued to digest the prospect that central banks in the U.S. and Europe will step up the pace of policy tightening.

The yield on 10-year Treasuries reached 1.51%, the highest since June, before settling at 1.48%. The yield has climbed 16 basis points over the past week as the Federal Reserve signaled it may start reducing its asset purchases in November and raising rates as soon as next year. Yields on two- and five-year Treasuries hit their highest levels since early 2020, with a combined $121 billion of the securities set to be sold Monday. A seven-year auction is due Tuesday.

While Treasuries briefly extended the selloff after a report showed durable goods orders exceeded economists’ forecasts, they started to pare losses after U.S. equity futures soured.

Bond yields increased across the globe last week as central banks move to reduce pandemic stimulus. The Bank of England surprised markets by raising the prospect of increasing rates as soon as November, and Norway delivered the first post-crisis hike among Group-of-10 countries. In the U.S., traders pulled forward wagers on an interest-rate increase to the end of 2022 following last week’s Fed meeting.

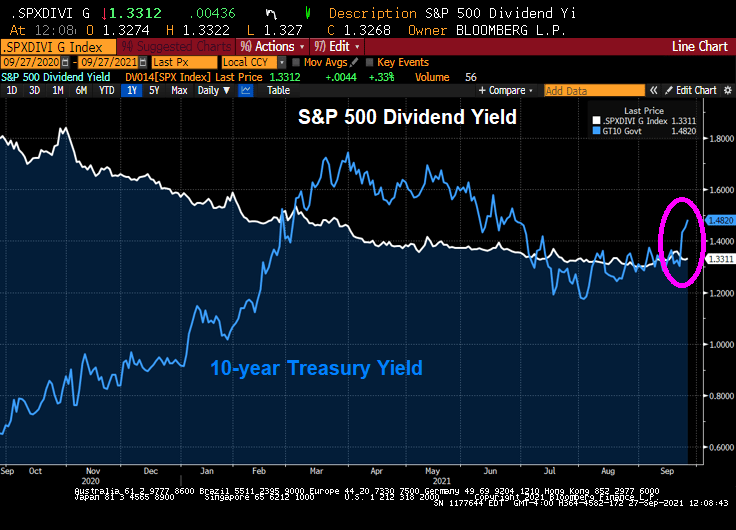

On the equity side, FAANG stocks trail the S&P 500 as 10-year Treasury yield climb.

We have the 10-year Treasury yield climbing above the S&P 500 dividend yield.

(Bloomberg) — The S&P 500 Index extended its decline past 2% Monday afternoon amid growing investor jitters about China’s real estate crackdown potentially sparking a financial contagion. And the Hang Seng fell 3.30% overnight.

The benchmark gauge was down 2.1% as of 12:08 p.m. in New York. All of the 11 major industry groups declined, with the energy, financials and materials sectors leading the losses. The tech-heavy Nasdaq 100 index slumped 2.4%, while the blue-chip Dow Jones Industrial Average retreated 1.9%.

By 2:33pm, the Dow is down 2.55%, NASDAQ down 3.15%.

Volatility also soared, with the Cboe Volatility Index — often called Wall Street’s “fear index” — jumping as much as 29% to 26.75, the highest level in over four months.

“While the Evergrande situation is front and center, the reality is, stock market valuations are overstretched and the market has enjoyed too long of a break from volatility and Monday’s stock market declines are not surprising,” said David Bahnsen, chief investment officer at the Bahnsen Group, a wealth management firm.

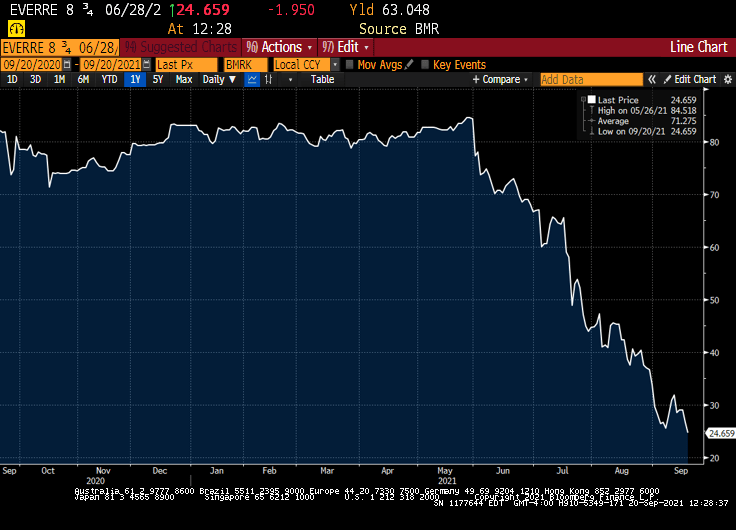

As Evergrande bonds continue to tank.

Meanwhile, most commodity prices are falling … except for UK Natural Gas Futures which are up 16.5%!

You must be logged in to post a comment.