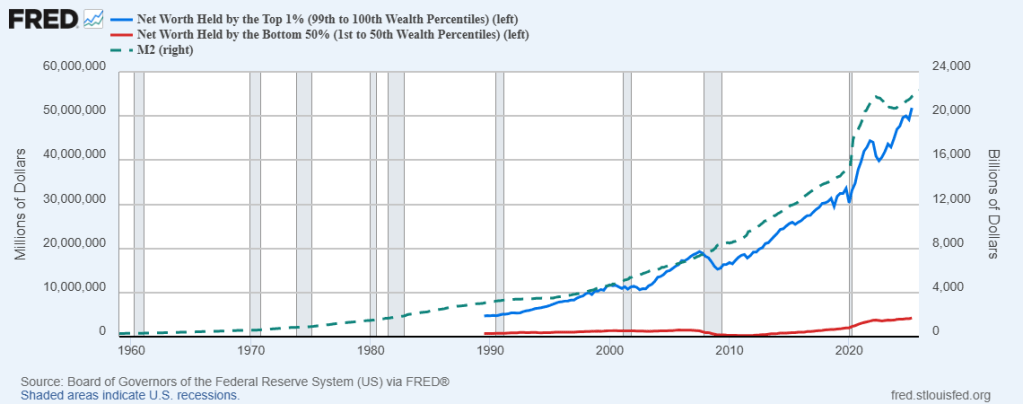

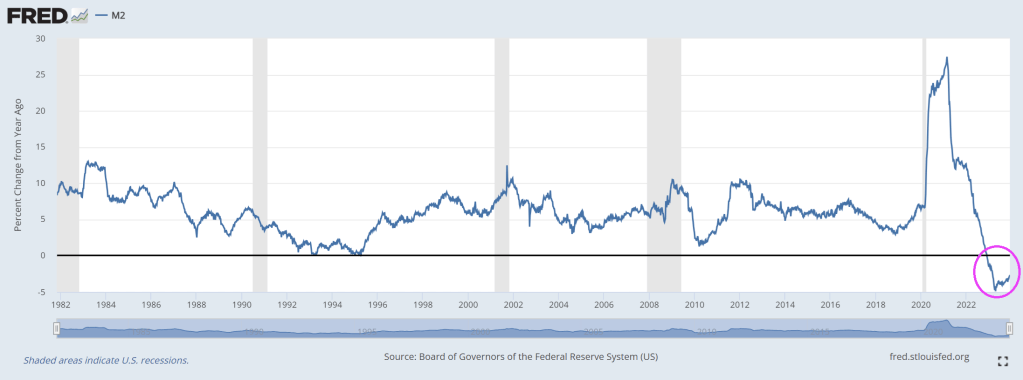

The Federal Reserve prints a lot of money (M2). Unfortunately, it largely benefits elites (the top 1%). The bottom 50% get some benefits, but the gains in net worth largely benefits the elite class.

This sounds like a legal Somali daycare scheme. Perhaps The Fed should be renamed “The Federal Quality Learing Center.”

Yes, Somalis have daycare centers in Columbus Ohio. Thanks Governor Dewine for doing absolutely nothing to reign in their fraud. /sarc

During the first three months of 2023, U.S. office vacancy topped 20 percent for the first time in decades. In San Francisco, Dallas, and Houston, vacancy rates are as high as 25 percent. These figures understate the severity of the crisis because they only cover spaces that are no longer leased. Most office leases were signed before the pandemic and have yet to come up for renewal. Actual office use points to a further decrease in demand. Attendance in the 10 largest business districts is still below 50 percent of its pre-COVID level, as white-collar employees spend an estimated 28 percent of their workdays at home.

A new report from Moody’s offers yet another grim outlook that the commercial real estate downturn is nowhere near the bottom. Elevated interest rates and persistent remote and hybrid working trends could result in around 24% of all office towers standing vacant within the next two years. The office tower apocalypse will result in more depressed values that will only pressure landlords.

“Combining these insights, with our more than 40 years of historic office performance data, as well as future employment projections, our model indicates that the impact on office demand from work from home will be around 14% on average across a 63- month period, resulting in vacancy rates that peak in early 2026 at approximately 24% nationally,” Moody’s analysts Todd Metcalfe, Anthony Spinelli, and Thomas LaSalvia wrote in the report.

In a separate report, Tom LaSalvia, Moody’s head of CRE economics, wrote that the office vacancy rate’s move from 19.8% in the first quarter of this year to the expected 24% by 2026 could reduce revenue for office landlords by between $8 billion and $10 billion. Factor in lower rents and higher costs, this may translate into “property value destruction” in the range of a quarter-trillion dollars.

In addition to remote working trends, Moody’s analysts pointed out that the amount of office space per worker has been in a “general downward trend for decades.”

At the peak of the Dot-Com boom, office workers used an average of 190 sq ft. The figure has since slid to 155 sq ft in 2023.

“The argument for maintaining or even increasing remote work practices remains compelling for many businesses,” the analysts said, adding, “If productivity remains stable and costs can be reduced by forgoing physical office spaces, the rationale for mandating in-office attendance diminishes.”

Related research from the McKinsey Global Institute forecasts that office property values will plummet by $800 billion to $1.3 trillion by the decade’s end.

Moody’s expects vacancy rates to top out as office towers are demolished or converted to residential ones in the coming years.

“Right-sizing will continue over the next decade as the market shakes out less efficient space for flexible floorplans that support our relatively new working habits,” they said.

Earlier this year, Goldman analyst Jan Hatzius pointed out that a further 50% price decline would make office tower conversions financially sensible.

1. Everybuddy: 100% of workforce 2. Wisense: 100% of workforce 3. CodeSee: 100% of workforce 4. Twig: 100% of workforce 5. Twitch: 35% of workforce 6. Roomba: 31% of workforce 7. Bumble: 30% of workforce 8. Farfetch: 25% of workforce 9. Away: 25% of workforce 10. Hasbro: 20% of workforce 11. LA Times: 20% of workforce 12. Wint Wealth: 20% of workforce 13. Finder: 17% of workforce 14. Spotify: 17% of workforce 15. Buzzfeed: 16% of workforce 16. Levi’s: 15% of workforce 17. Xerox: 15% of workforce 18. Qualtrics: 14% of workforce 19. Wayfair: 13% of workforce 20. Duolingo: 10% of workforce 21. Rivian: 10% of workforce 22. Washington Post: 10% of workforce 23. Snap: 10% of workforce 24. eBay: 9% of workforce 25. Sony Interactive: 8% of workforce 26. Expedia: 8% of workforce 27. Business Insider: 8% of workforce 28. Instacart: 7% of workforce 29. Paypal: 7% of workforce 30. Okta: 7% of workforce 31. Charles Schwab: 6% of workforce 32. Docusign: 6% of workforce 33. Riskified: 6% of workforce 34. EA: 5% of workforce 35. Motional: 5% of workforce 36. Mozilla: 5% of workforce 37. Vacasa: 5% of workforce 38. CISCO: 5% of workforce 39. UPS: 2% of workforce 40. Nike: 2% of workforce 41. Blackrock: 3% of workforce 42. Paramount: 3% of workforce 43. Citigroup: 20,000 employees 44. ThyssenKrupp: 5,000 employees 45. Best Buy: 3,500 employees 46. Barry Callebaut: 2,500 employees 47. Outback Steakhouse: 1,000 48. Northrop Grumman: 1,000 employees 49. Pixar: 1,300 employees 50. Perrigo: 500 employees

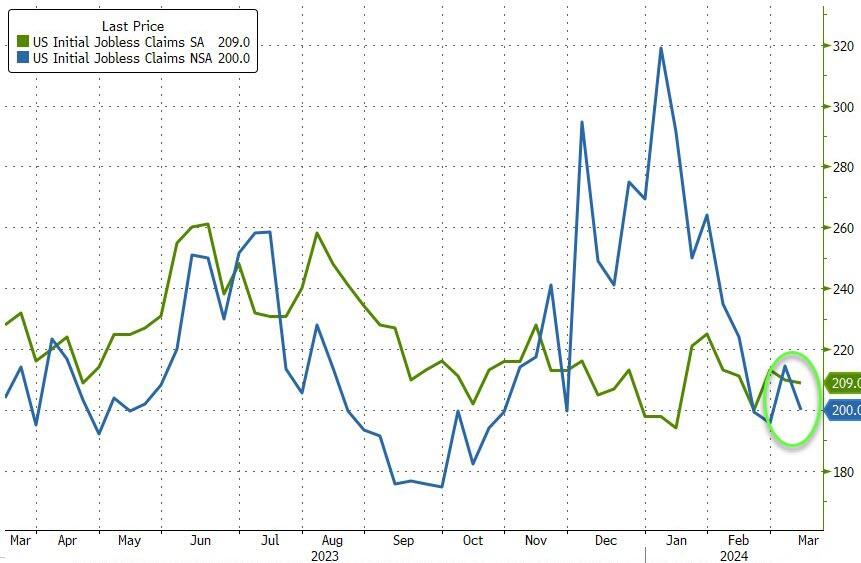

But, according to the government-supplied data…

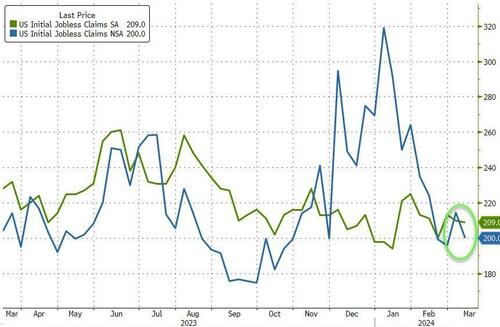

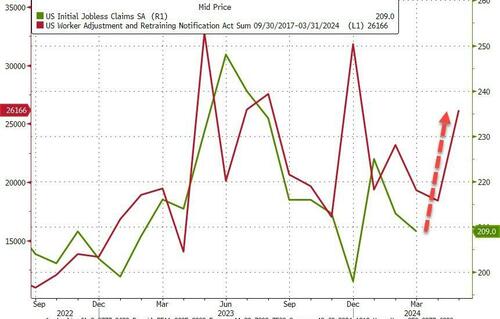

The number of American filing for jobless benefits for the first time last week dropped to 209k (vs 218k exp) with the NSA number tumbling to 200k…

Source: Bloomberg

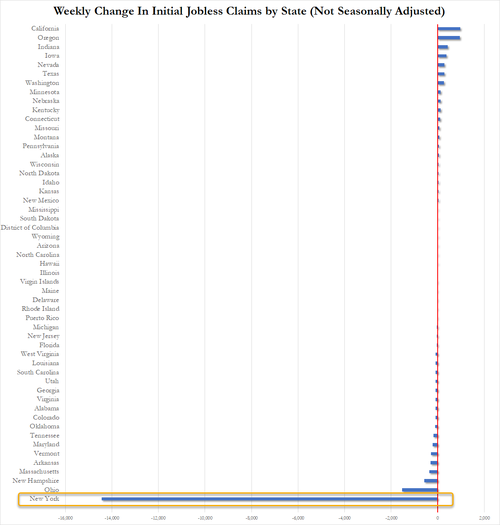

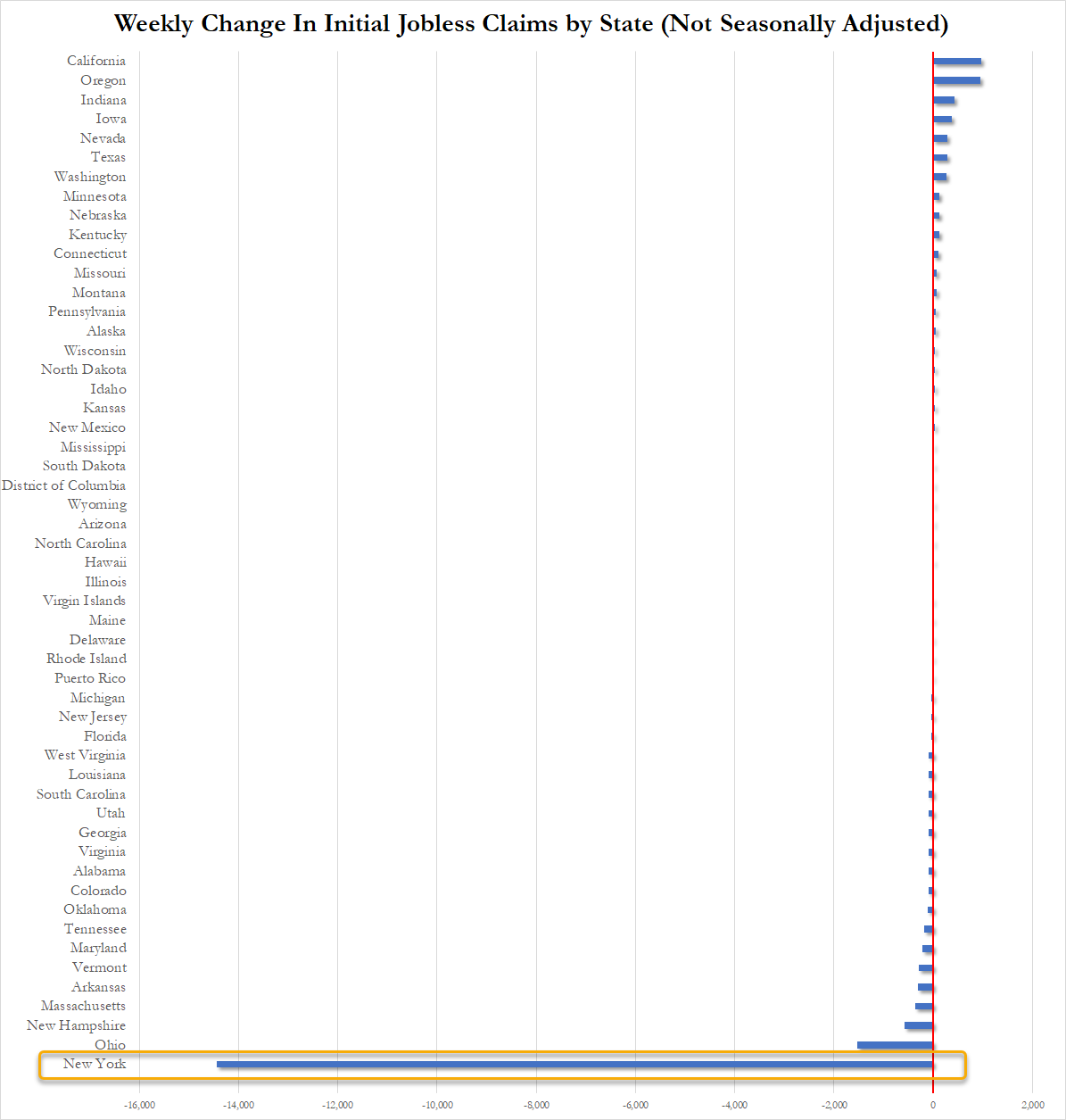

How is this possible, you may ask… well let us show you the ways… New York State claims that its jobless benefits rolls collapsed last week. New York accounted for 99.75% of the weekly change in initial claims across the entire US as shown below…

Source: Bloomberg

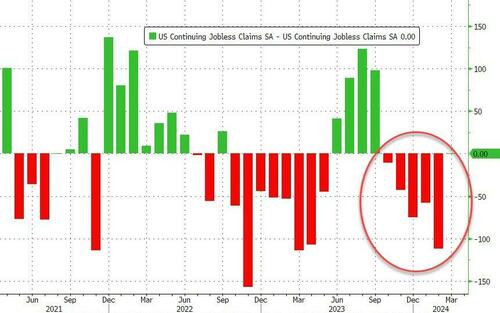

Continuing Claims was a shit show – with a massive 112k person downward revision for last week from 1.906 million to 1.794mm. That is the 5th straight weekly downward revision of continuing claims…

Source: Bloomberg

But thanks to the adjustments, it all looks ‘normal’ and ‘stable’ at around 1.8 million Americans…

Source: Bloomberg

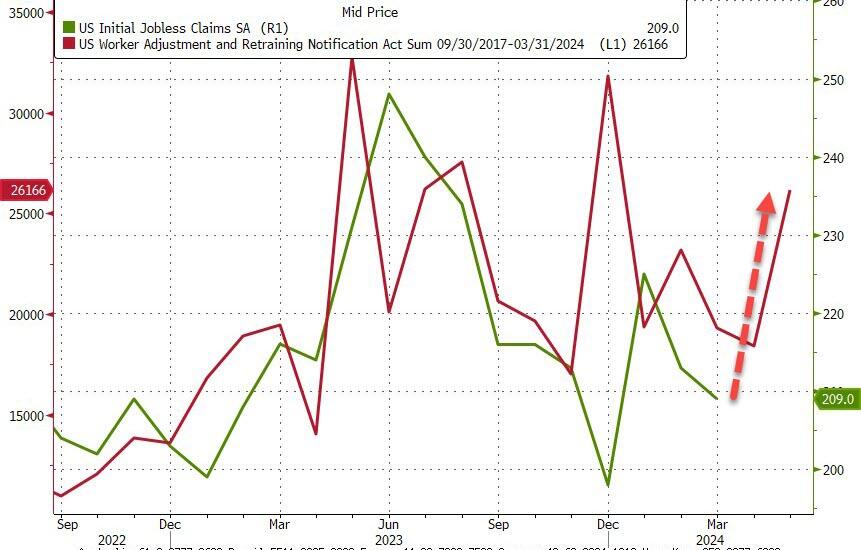

And WARN numbers are rising rapidly…

Source: Bloomberg

As a reminder, if you doubt the accuracy of the Biden admin’s data, here’s what the most recent FOMC Minutes said:

“While the recent trends prior to the meeting had been remarkably positive, Fed officials judged that some of the recent improvement “reflected idiosyncratic movements in a few series.”

Even they aren’t buying it, and neither should you!

Or as Bonnie Beecher almost sang in a Twilight Zone episode, “Come wander with China Joe Biden.” On The White House lawn. Or wander with The Federal Reserve!

The USA is a runaway train with a dead man (China Joe is about as dead as one can be) in the engineer’s seat.The conductor goes through the cars assuring the passengers that everything is fine. . . never mind the screeching wheels on the curves. . . or the blinding strobe effect of low sunlight passing through the trees out the window at a hundred and forty mph. . . or the bump that made half the stuff in the overhead luggage rack jump out. More than half the people on-board are at tachycardia levels of fright — some are screeching — but the other less than half just remain fixed on their phones and laptop screens. They can’t be bothered to look out the window…

Okay, that’s a metaphor.

But if you’re a citizen of our country and care about it, these are the matters you’d better pay attention to, because they are all going off the rails.

The war in Ukraine. We started it in 2014 to mess with Russia and Russia is going to finish it. Who knows what our real motives were. A resource grab? A desperate ploy to erase our national debt by creating a global fiasco? Sheer psychopathic hatred of this Putin fellow? We can’t bring ourselves to acknowledge the failure of this ill-conceived venture. Instead, our feckless allies in Europe are foolishly rattling their sabers, apparently forgetting that you don’t bring a sword to a nuclear missile fight.

Mr. Macron in France affects to offer up his army for slaughter on the blood-soaked plains of Ukraine, just as the Ukrainians offered up a half a million of their young men so that Victoria Nuland could feel good about herself. Mr. Macron is insane, but the society he presides over is collectively insane, so perhaps he represents them well. Similarly, Olaf Scholz in Germany, whose top generals were caught on a leaked recording last week discussing their plan to blow up the Kerch Bridge that connects Crimea to Russia. Do you understand that this would be a direct attack on Russia, an act of War by NATO? And what the obvious consequence would be?

The phantom government of “Joe Biden” is too weak and mindless to join any negotiation. Ukraine and Russia are up to some kind of cross-talk down in Riyadh with Prince MBS. Even Mr. Zelensky went down for a day, though video appears to show him coked-up, sniffling and snarfling, not a good sign. If ever there was a time to end this stupid conflict, it’s now, before the Russian election. After that, terms will only be more difficult for Ukraine, up to direct custodial supervision instead of remaining a nation. It was never any of our business (though the Biden family, BlackRock, and the CIA saw fabulous opportunity to profit there).

Next is the border. You saw last year how the blob elite greeted the transfer of illegal immigrants to their happy little island of Martha’s Vineyard. (They were not amused by Governor DeSantis’s prank, and off-loaded the mutts post-haste.) But that same smug demographic doesn’t care if hundreds of thousands are distributed to the big cities, which are now fiscally destabilized by them to an extreme, probably to bankruptcy.

Of course, that is not the main thing to worry about with what altogether amounts to millions of border-jumpers flooding our land. The main reason to worry is what the blob that invited them here intends for them to do, which, you may suspect, is to unleash mayhem in the streets, malls, stadiums, and upon our infrastructure just in time to derail the election — perhaps even to make war on us right in our homeland. The US government is paying for this whole operation, you understand, funneling our tax money to international cut-out orgs who set up the transfer camps in Panama, and buy the plane tickets for the mutts to cross the ocean, and coordinate with the Mexican cartels to shuttle this horde of mystery people among us to work their juju for the Democratic Party. The pissed-off-ness of the public has passed the red line on this.

A third FUBAR is the lawfare campaign of the Democratic Party and its regime in power against the citizens of this land. This folder includes overt and obvious political prosecutions by DA’s and AG’s who make election promises to “go after” individuals without such niceties as probable cause. It includes the gigantic new scaffold of inter-agency censorship and propaganda. It includes the psychopathic struggle sessions mandated by “diversity and inclusion” policy. It includes election-rigging directed by the likes of Marc Elias and Norm Eisen, getting states to fiddle laws on voter ID and mail-in ballots. It includes the political protection of rogue groups ranging from looter flash-mobs to Antifa anarchists who bust up things and people and burn buildings down. It includes state officials who peremptorily kick candidates off the ballot. It includes a nakedly biased judiciary, and especially the use of the DC federal district court to punish people extralegally, unjustly, extravagantly, and cruelly. In short, lawfare is the complete perversion of law, and we-the -people are entreated by reprobate officials such as Merrick Garland and Letitia James to accept it.

A fourth item on this list is the US economy which has been overwhelmed by maladministration of an overgrown monster bureaucracy, and the gross (perhaps fatal) mismanagement of the government’s money. The people of this land are not being allowed to do business, to find a livelihood, to transact fairly. “Joe Biden’s” shadow string-pullers are messing as badly with the oil and gas producers as they have messed with Ukraine. And they are doing it in pursuit of a laughable mirage: their “green new deal.”

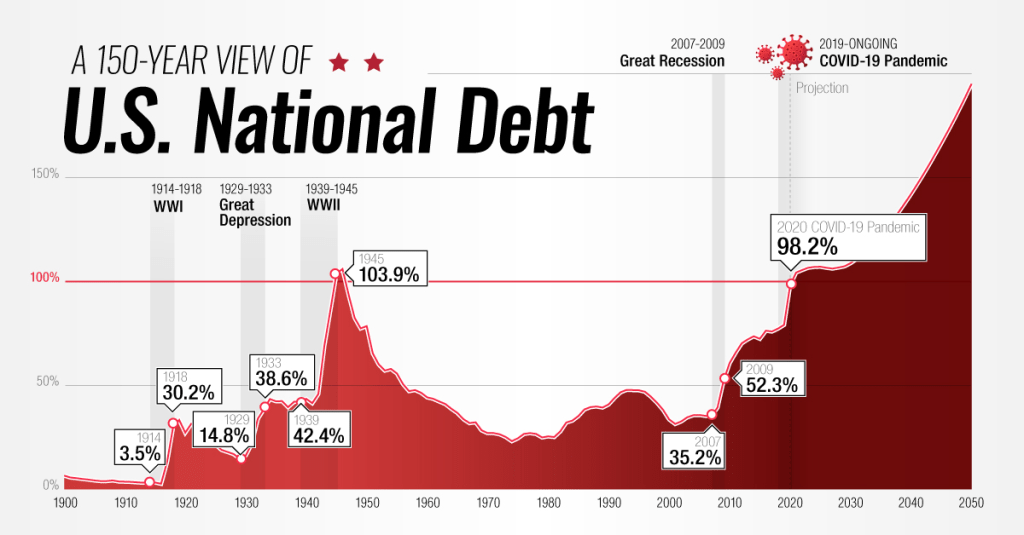

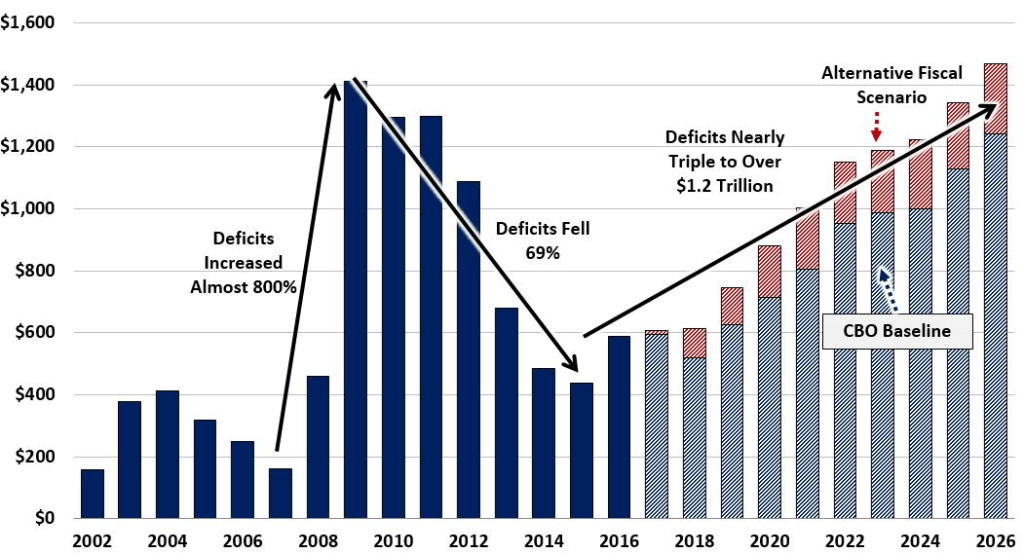

John Podesta, the “clean energy czar” who replaced the Haircut-in-search-of-a-brain called John Kerry, sits on a $370-billion slush fund that can be used to just dole out to anyone and everyone a political patronage payoff, especially to janky “community” orgs and NGOs with fake agendas. This really just amounts to an asset-stripping operation that will leave the American people busted and with broken supply chains for everything. Instead of annual budgets, Congress raises the US debt ceiling by “continuing resolutions” to keep the government from shutting down. The national debt races to the $35-trillion mark. As interest rates on debt rise, our debt payments now exceed our military spending. You can be sure that our country will break down financially very soon.

The capper on today’s list is the nation’s health, the racketeering system we’ve set up to care for it, and the public health agencies of the government that enabled the Covid-19 operation to happen. The CDC continues to push vaccines that have killed millions of Americans and more millions around the world, and has probably compromised the well-being of millions more going forward. Corporate medicine — that is, your doctor, and your hospitals — is a sinking Titanic of grift and chaos. Try to get an appointment to even see a doctor for an emergency. Try to avoid being bankrupted by your treatment. Try to get out of a hospital alive. Yeah, it’s that bad.

The doctors have surrendered your trust in them with their lying and their bullshit. The current director of the CDC, Mandy Cohen and her predecessor, Rochelle Walensky, have knowingly presided over the mass killing and injuries imposed on the mRNA vaccinated. Hundreds of their deputies should be liable for prosecution, and so should many of the other prominent characters in the Covid Saga: Fauci, Birx, Collins, Baric, Bourla, Daszak, Califf, Woodcock, Hahn, and many more.

What are we going to do about any of this? Return to the metaphor. The runaway train is still picking up speed. You can’t just jump off at 150 mph. If you’re one of the passengers watching this in horror, maybe you can decouple your car, or get the conductor to do it by any means necessary. Let’s say that each car behind the engine of this train is a state of the United States. Let the engine up front with the dead man at the controls ride that runaway to its terrible conclusion. Cut loose the cars behind it to take care of themselves, to slow down, get a grip on their situation, and make plans to find a better engine to pull the train. Decouple. Cut loose. It’s the only way.

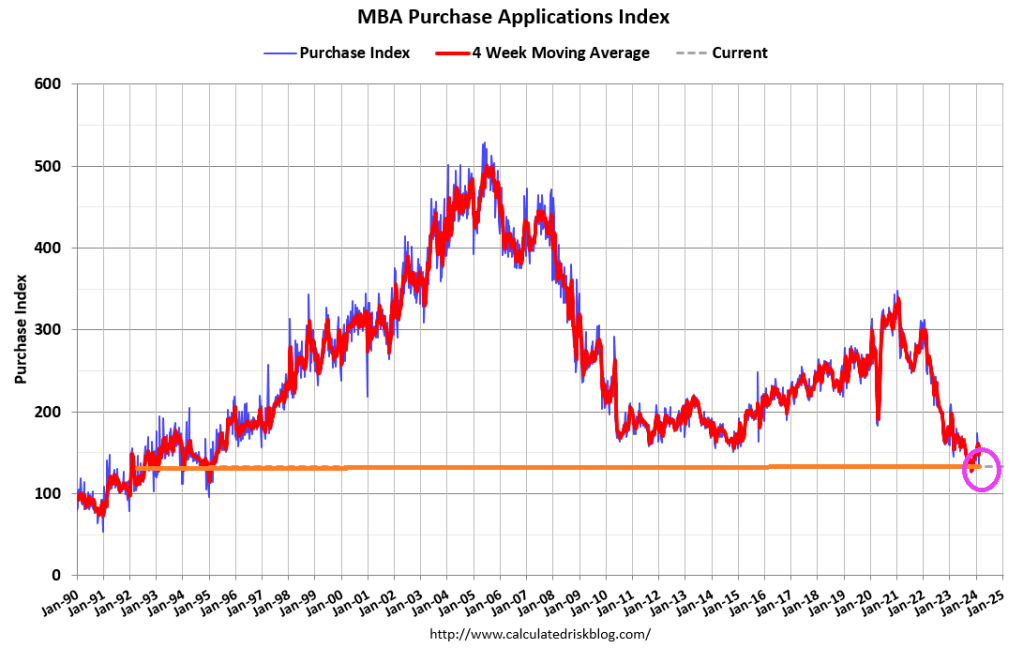

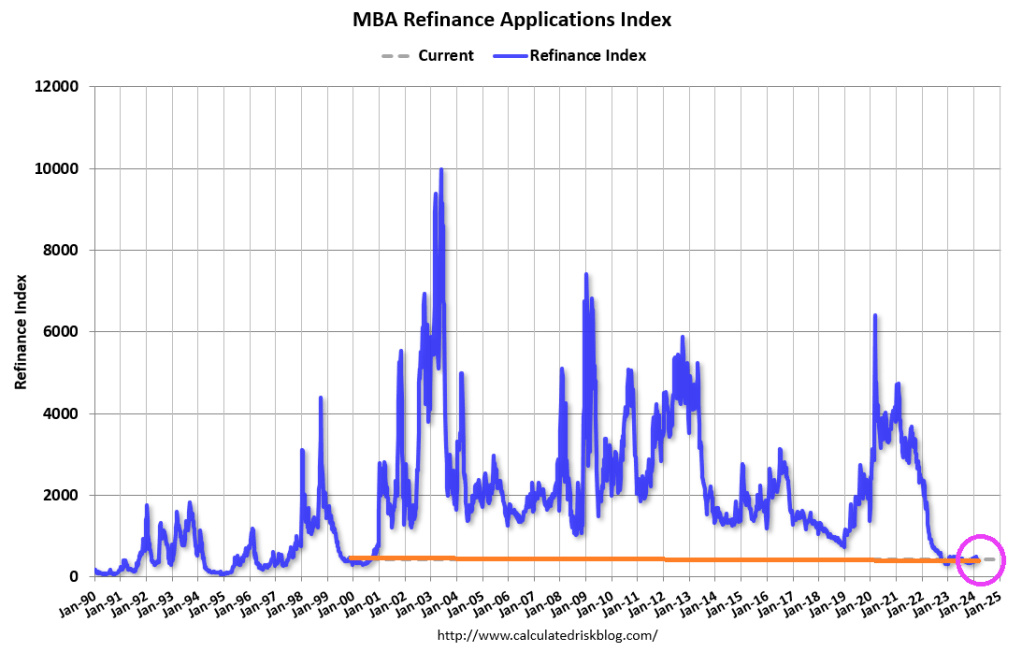

Mortgage applications decreased 10.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 16, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 10.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 8 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 10 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was13 percent lower than the same week one year ago.

The Refinance Index decreased 11 percent from the previous week and was 0.1 percent higher than the same week one year ago.

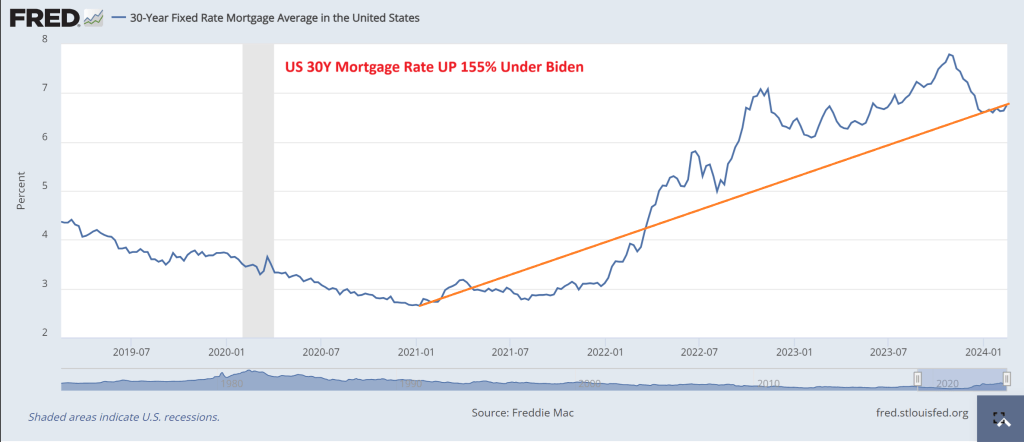

One reason why mortgage demand is so low is that mortgage rates are up 155% under Biden.

Is it sundown for the US mortgage market? And when will it improve?? Probably won’t improve in New York City after Judge Engmoron’s idiotic fine of Donald Trump and family for non-crimes.

I watched Tucker Carlson’s interview with Russian President Vladimir Putin. Putin is an amazing contrast to our 81-year old President with dementia who can barely speak while Putin was articulate. Not at all what Hillary Clinton was raving about (she is still furious about losing to Trump after losing to Obama). One thing that caught my attention was Putin talking about The Fed’s endless printing of money. Well, THAT is how the US grows GDP these days. Borrow and spend with the private sector as an after thought.

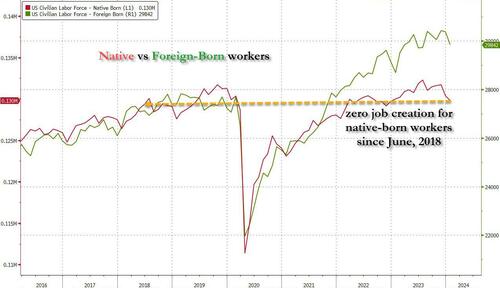

Let’s revisit the HORRIBLE jobs report from December. Not only were all job gains in the past year entirely thanks to part-time workers, but native-born workers plunged by a another whopping 560 thousand, bringing the two-month total drop to just under 2 million.This meant that not only has all job creation in the past 4 years been exclusively for foreign-born workers, but there has been zero job-creation for native-born American workers since July 2018 (don’t believe us? go ahead and check the data directly from the Fed).

So, the Federal government is borrowing trillions of dollars so that 1) part-time jobs are created and 2) foreign born workers have jobs, but not native born Americans?? (Blogger Paul Krugman thinks that immigration will add $7 trillion in real GDP over the next 10 years and this will save Social Security and Medicare. Huh? I admit, millions of immigrants will spend money, but many will be on the Federal and State doles, so its tax dollars going to immigrants to spend.) This seems like Obama/Biden are using Cloward-Piven tactics to overwhelm Social Security, Medicare and other social services, NOT grow the economy as Krugman projects.

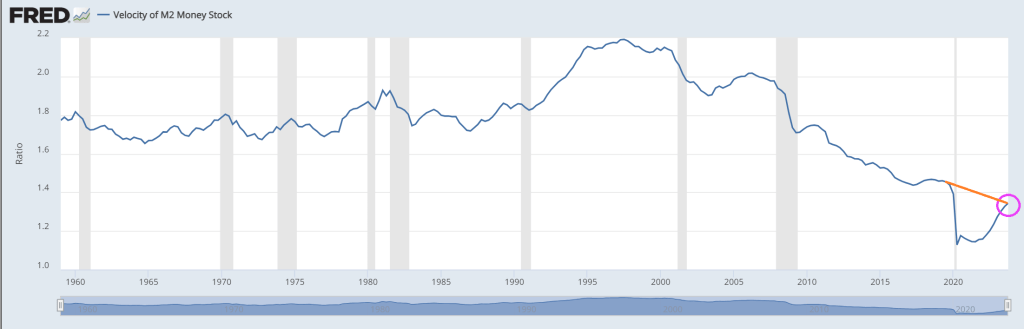

Typically, economists look at measures like M2 Money Velocity (Real GDP/M2). M2 Money Velocity is rising … but still remains below where it was pre-Covid under Donald Trump.

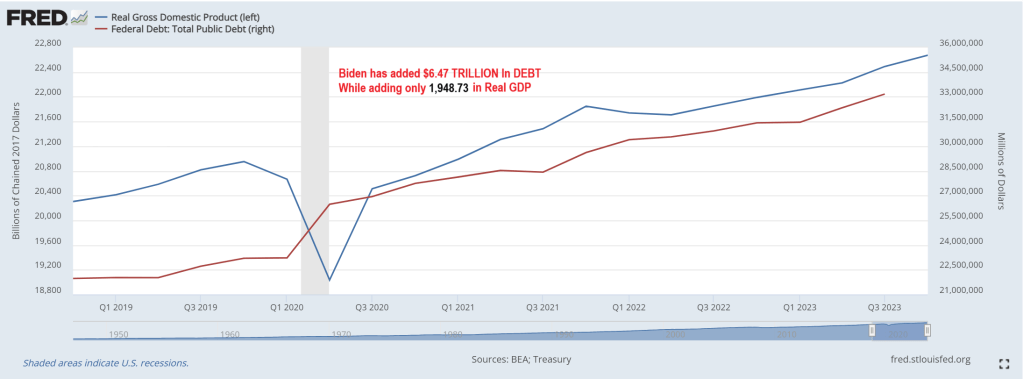

But a more relevant velocity is the velocity of DEBT. As in GDP/Debt. Under Biden, the US has added almost $6.5 TRILLION in debt while real GDP has risen by only $1.949 trillion. That amounts to a DEBT velocity of 0.30. Meaning that the US gets an anemic $30 in real GDP for every $100 in additional Federal debt.

Yes, the US economy is broken and requires endless money printing and debt financing to pay for endless wars and now millions of illegal immigrants getting on “the dole.” Then we have Biden’s forgiving student loan debt (inappropriately) and now Big Tech wants $7 trillion to develop AI (in a normal economy, tech companies would develop AI themselves, but under Obama/Biden, we are not in a normal economy).

Here is Daddy (Ukraine) Warbucks Biden with his biting dog and daughter Ashey.

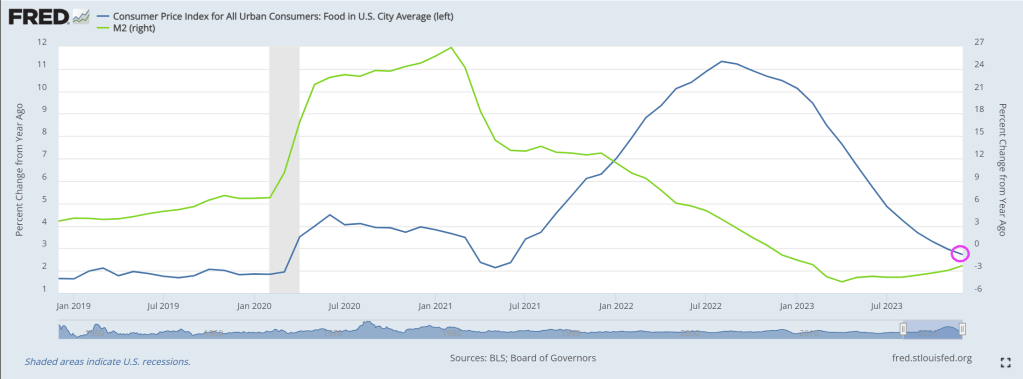

The Biden Administration which motto should be “Make Crime Great Again!” with awful crime in big cities, and millions pouring over the border, not to mention providing jobs for foreign workers and not native born Americans, is likely breathing a sigh of relief as food inflation falling to 2.7% year-over-year, still higher than pre-Covid levels under Trump. But at least food price inflation is slowing as The Fed’s money stimulus recedes.

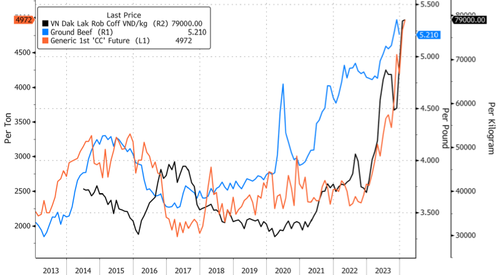

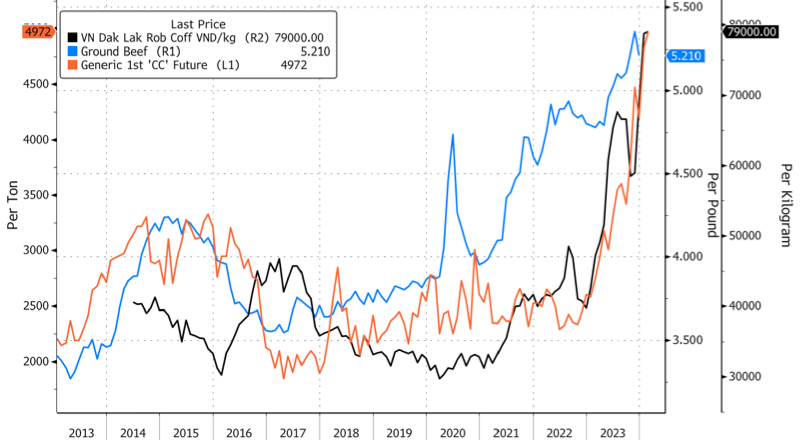

Cocoa prices climbed to a 46-year high this week in New York as concerns about dry conditions across West Africa could reduce yields for the Ivory Coast, the world’s largest producer of cocoa beans, ahead of the mid-crop in April.

In the US, a rapidly shrinking cattle herd, now at the lowest levels in seven decades, has pushed the supermarket price of beef to a record of $5.21 per pound. Rising food prices are the central bank’s worst enemy.

To end the week, breakfast lovers will be disappointed to learn robusta bean prices in Vietnam, the world’s largest producer of the bean, are absolutely out of control.

Local robusta prices in Vietnam hit a record on Thursday, topping nearly 80,000 per kilogram.

“That’s threatening to push prices in London up further, even after the benchmark capped its own all-time high this week at $3,336 a ton,” Bloomberg said, adding the surge in prices was primarily due to farmers “hoarding” the bean.

To recap this week, cocoa bean, beef, and robusta bean prices have been marching higher.

More bad news for Biden. Even though overall food inflation has receded, voters have long memories.

And, as Nomura’s Charlie McElligott highlights this morning, we are also seeing new upside being bot in SOFR Options for “dovish outcome”-hedging again, with Core PCE looming later this week.The market has had bunches of March SOFR Downside structures trading over the past few weeks to play for “Fed cut overshoot,” which has been the right trade YTD, as the implied probability distribution shows March Fed cuts now having been slashed by over half the the past week and a half (~80% priced to now just ~40%), and accordingly now we’ve witnessed some monetization of tactical Downside in recent days…

And we see the swaption surface getting mushed…

As he notes, the “dovish-trifecta” right-tail repricing has gotten us to ~4900… and, he says, the actual “realization” could then certainly push us through 5000:It’s my expectations that we could very well see:1) “March Fed cut” to pick-up Delta again after what is expected to be a “light” core PCE print this Friday…and taking back pricing following the past week’s Fed speak pushback and “too resilient” Labor- and Consumer- data, which has driven March Fed meeting “cut” probabilities being sliced in half over the past one week (~80% on 1/12/24 to today’s ~40%)The next potential dovish catalyst is 2) the QRA est / announcement end of Jan / start Feb, with “binary risk” implications on the direction of Duration and Risk-Assets, as the market generally anticipates resumption of larger Coupon issuance from the US Treasury ahead—but what if there is one final announcement where Bills stay high, Coupon increases but isn’t as large as most anticipate, AND Yellen signals that this is the final expected Coupon increase?!

While we’re at it and relate to the Treasury’s QRA discussion, let’s not forget the “other” market- and economic- backstop being applied by the Biden Administration (and aided by what looks to be Janet Yellen’s “politically activist” US Treasury with TBAC sign-off) – which is the continued willingness to run large fiscal deficits in an attempt to “run the economy hot” in this election year, with much of it being “paid for” via Bills (so to prevent long-end Rates from pushing higher, which would tighten US financial conditions)……this is Green build, CHIPS Act, and even fresh “election surprises” like Biden announcement Friday on “forgiveness” of a fresh $5B of student loans, now making the total loan forgiveness approved by the Biden admin $136.6B

And finally as a derivative of the above mention, another hypothetical Treasury QRA where we’d see “Bill issuance remaining high, yet with Coupon increases not as large as most anticipate” would then mechnically see MMF’s continuing pulling from RRP to buy Bills, which will further accelerate the RRP drain…and as outlined in recent weeks, “low” RRP levels will act as “a” key input to Fed reaction function on determining LCLoR……which will ultimately mean 3) a pulling-forward on the market’s expected timing on the “end of QT”

This “dovish-trifecta” is the macro catalyst behind the “right-tail” scenario which has appropriately been repriced higher by the market over the course of the past month, and we’ve seen clients allocate some protection spend to this “crash-UP” scenarioAnd again, IF the above were to realize… without negative catalysts (Earnings fine, no further Rates selloff / Fed repricing, continued disinflationary trajectory rebuilds “Fed cut” implied probability) around that upcoming Feb VIXpery with all that Dealer “short VIX Calls” positioning being hedged… there is absolutely potential for an Equities slingshot if there are no issues and those customer “Long VIX Calls” bleed-out, which will mean Dealers puke out their UX1 Longs (as hedges) back into the market for a potential “kicker” to goose Spot Equities even higher…For now, no-one is worried about downside based on VVIX being back near post-COVID lows…

So what then is the largest DOWNSIDE RISK to Equities?

Outside of “Mag 7” guidance disappointments, I believe the next worst-case scenario for current positioning in Stocks would be an “Animal Spirits” US data reacceleration which forces the above “dovish trifecta” off-course and blows-out the recently calming “Fed Rates path” distribution again:Why would resumption of better US growth data negatively impact US Equities consensus thematic / singles positioning?Because after the 4Q23 de-grossing of short books and forced “Net-up” to stop the bleed and chase (massive squeeze & cover in low quality / cyclical value / leveraged balance sheet / high short interest “junk”)….2024 YTD has instead seen the market reset the prior “Momentum” regime of “Long Quality / Size / Secular Growth” i.e. MegaCap Tech, while re-shorting that economically-sensitive “low quality / junk” stuff againIn a world of slowing but positive growth to 2% GDP and now with 3m inflation annualizing sub 2% target…you go back to that “QE of old” 2010s -decade playbook of “long stuff that can grow earnings and profits without needing a hot economic cycle”…i.e. long quality, size (liquid) & secular growth / short leverage & cyclical valueBut IF we see the “animal spirits” data reacceleration off the back of the massive FCI easing that the Fed and Treasury have facilitated, plus the persistent wage growth and still too strong labor meaning consumption remains robust, along with ongoing govt fiscal stim / spending…

.

..we risk a chance of inflation pivoting away from the current disinflationary trajectory(God-forbid actual “reflation”) which would could see that “long secular growth / short econ sensitive / cyclical value’ trade get a shock reversal…

…as long-end Yields and accordingly then, financial conditions, re-tighten and smash the “high valuation” Quality / Secular Growth stuff, while the heavily hated / shorted Cyclicals would painfully squeeze higher.Don’t forget, we’ve seen that happen before (yes we know the magnitudes of the inflationary impulse are different, but the timing of the human-emotion/monetary-policy-over-confidence double-rip in inflation is unquestionable)…

So, be careful what you wish for from higher and higher all-time-highs for stocks – the stronger they look (on the back of dovish expectations), the more likely The Fed is to hold back the actual dovish actions so much hope is founded on.

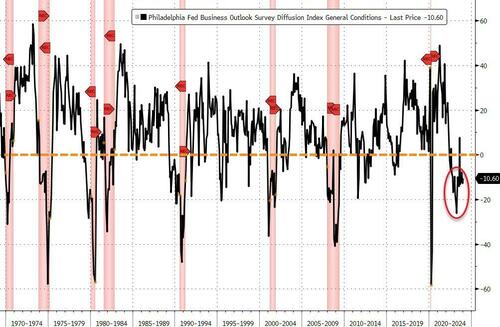

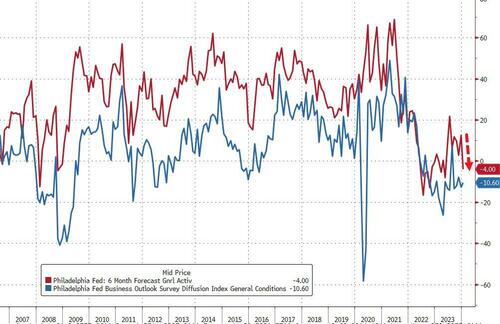

More worrying is the fact that hope appears to be dwindling fast as the six-month-forecast for the survey plunged back into contraction (from +12.6 to -4.00)…

Source: Bloomberg

Philly Fed’s demise is consistent with the collapse of hope as ‘soft’ survey data has slumped in the last month, back to its weakest since July (as ‘hard’ data improves relative to expectations)…

Source: Bloomberg

On the bright side for the doves, the dis-inflationary trend remains in tact as priced paid and prices received both plunged in January. However, we highlight the fact that Philly businesses expect price pressure to return in the next six months…

Source: Bloomberg

Overall, the ‘bad news’ in this report should buoy stocks and bonds (lower inflation and lower growth enables sooner and faster cuts)… But will it.

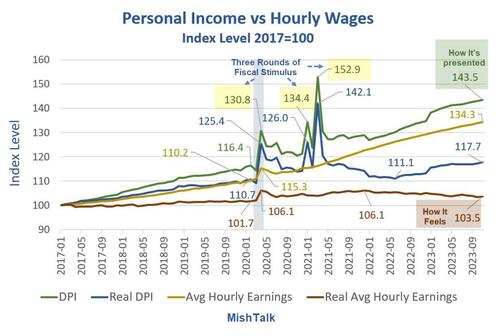

Income is rising and so are wages. Even real income is up. But real wages are another matter.

Personal income data from the BEA, hourly wages from the BLS, real hourly earnings and chart by Mish.

Personal Income vs Hourly Wages Notes

DPI means Disposable Personal Income. Disposable means after taxes.

Real DPI means inflation adjusted using the Personal Consumption Expenditures (PCE) deflator. Real DPI is a BEA calculation.

Average hourly earning are for production and nonsupervisory workers.

Real wages are deflated by the Consumer Price Index (CPI) not the PCE.

The BLS does not report a real hourly wage. I used the CPI-W index for production and nonsupervisory workers, produced by the BLS, as the deflator.

Personal Income Definition

The BEA defines personal income as “Income that people get from wages and salaries, Social Security and other government benefits, dividends and interest, business ownership, and other sources.”

Rental income is a part of other sources.

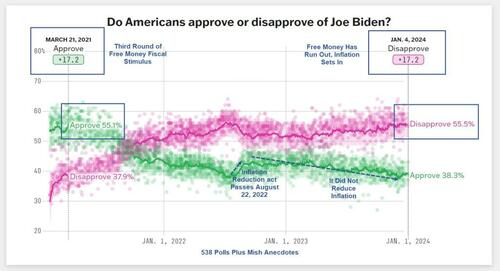

Three Rounds of Fiscal Stimulus

Round 1, March 2020: $1,200 per income tax filer, $500 per child(CARES Act) – Trump

Round 2, December 2020: $600 per income tax filer, $600 per child (Consolidated Appropriations Act, 2021) – Trump

Round 3, March 2021: $1,400 per income tax filer, $1,400 per child (American Rescue Plan Act) – Biden

The three rounds of free money fiscal stimulus (literally a helicopter drop), plus eviction moratoriums put an unprecedented amount of money in people’s hands. In addition, unemployment insurance paid people more to not work than they received working.

The third round of stimulus under Biden was totally unwarranted. However, it is also worth noting that Trump wanted a much bigger second stimulus package than the Republican Congress gave him. Trump is no fiscal hero.

The three stimulus packages, on top of supply chain disruptions, energy disruptions due to the war in Ukraine, and Bidenomics in general, set in motion the biggest wave of inflation in over 30 years.

Biden went from an approval rating of 17.2 percent to a disapproval rating of 17.2 percent.

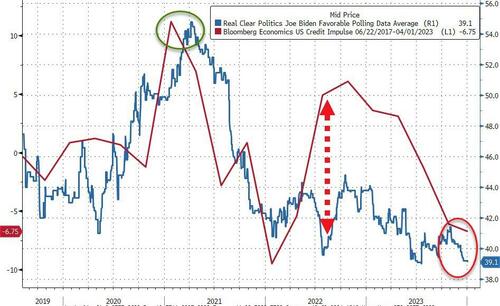

Peak Free Money

In addition to declining real wages, perhaps Biden’s big problem is the free money has run out.

Biden’s popularity peaked in March of 2021 along with stimulus. Was that a honeymoon impact or peak free money?

[ZH: While not a perfect indicator, the lagged US credit impulse perhaps provides a proxy for US fiscal excess and when overlaid with Biden’s approval rating, it is clear that 2022’s re-acceleration did nothing for people’s faith in him… and it’s only got worse…]

I suspect a bit of each coupled with hope of more free money, especially student loan forgiveness.

Sending free money to Israel and Ukraine does not help perceptions of how Biden is doing. And neither does the border or ridiculous energy regulations that cost people money.

Biden keeps telling people what a great job he has done.

I don’t believe it and most don’t either. And that shows up in the polls no matter what reason you assign.

Can Biden scrounge up some more stimulus? Because the private sector is not doing well under “Open Borders Biden.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.