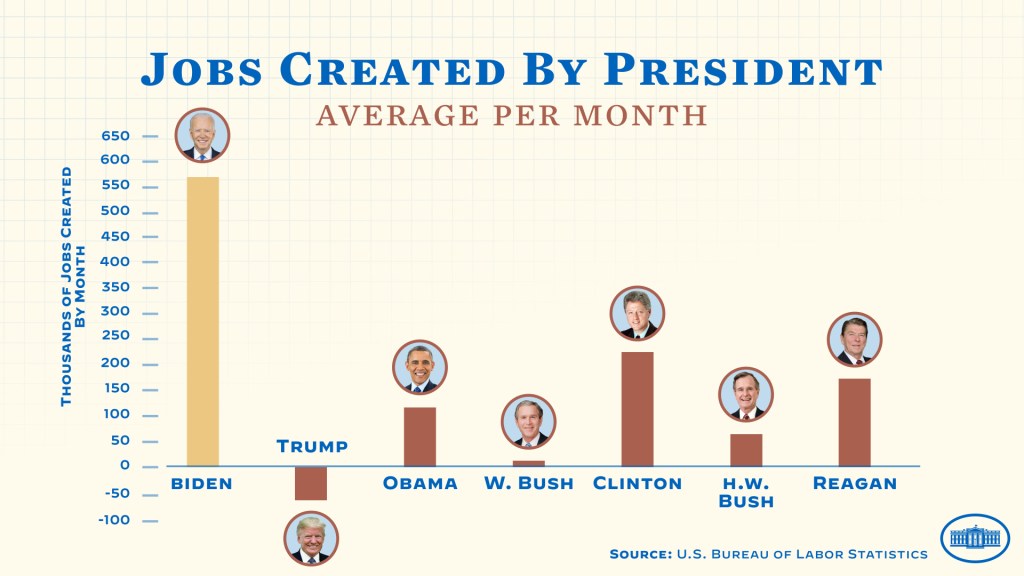

Recently, the White House claimed that the Biden Administration created more jobs (per month) than Trump, Obama, George W Bush, George HW Bush, Clinton and Reagan.

It always helps to be elected President after a recession when the economy naturally snaps back from the economic doldrums (like Obama after the financial crisis, Clinton after the first Gulf War, Reagan after Carter).

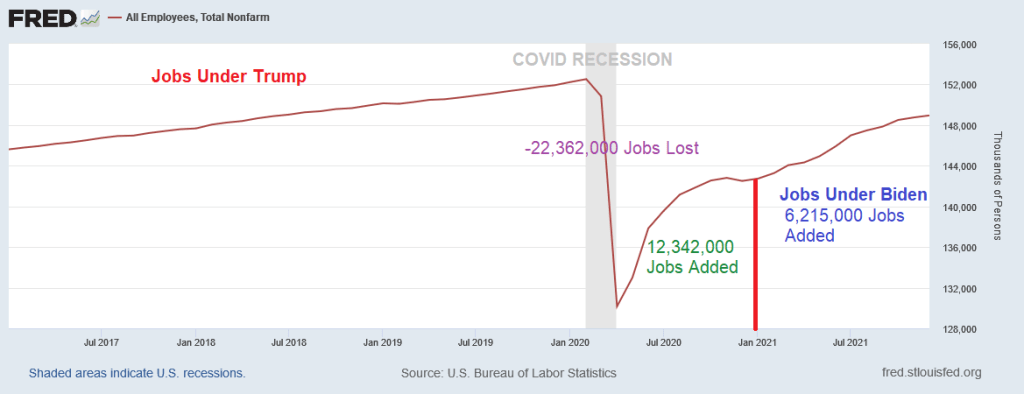

So let’s look at job totals under Trump, the COVID lockdowns, the ensuing economic damage, and the Biden “rebound.” In a brief two months in early 2020 thanks to COVID and lockdowns, the US economy lost 22.362 MILLION jobs. But the snap-back effect under Trump was 12.342 MILLION jobs added back by the time Biden was sworn-in as President.

Under his term as President, Biden has benefited from “Snap-back inertia” and saw 6.215 MILLION jobs added in just a year. Pretty impressive, except that it is about half the snap-back effect experienced under Trump.

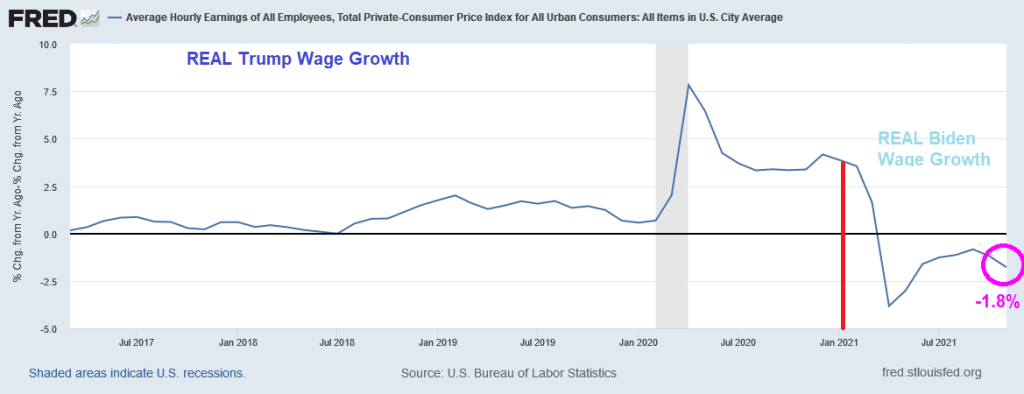

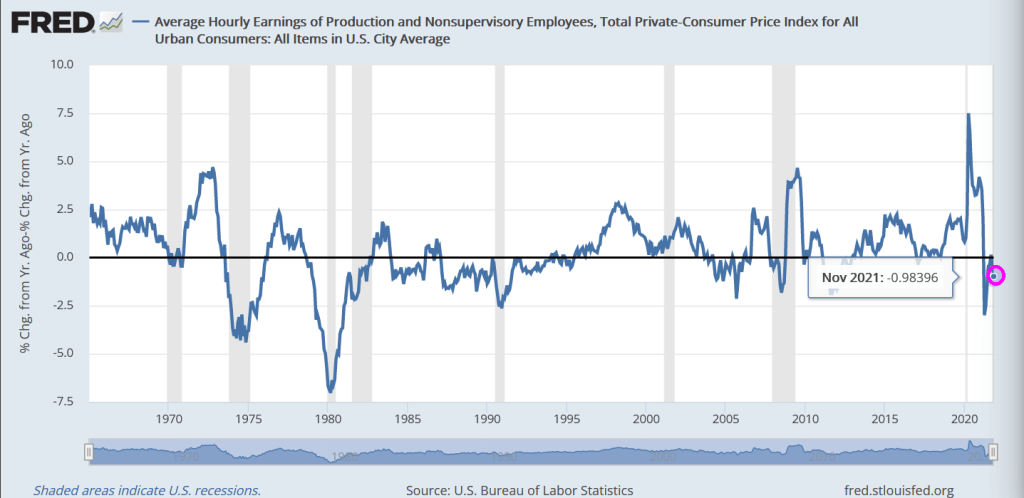

How about REAL wage growth (nominal wage growth less inflation)? Real wage growth was higher under Trump and has been declining under Biden. Strange that the White House isn’t bragging about declining real wage growth under Biden.

Let’s see how Omicron impacts the labor market and whether Biden/Psaki will take credit for the snap-back from Omicron.

Call this the Biden malaise (or Ka-malaise) for wage growth. Where inflation nukes positive wage gains.

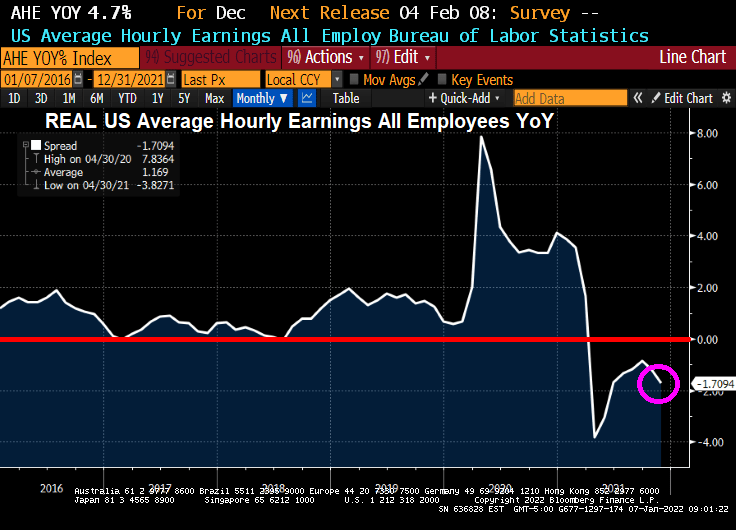

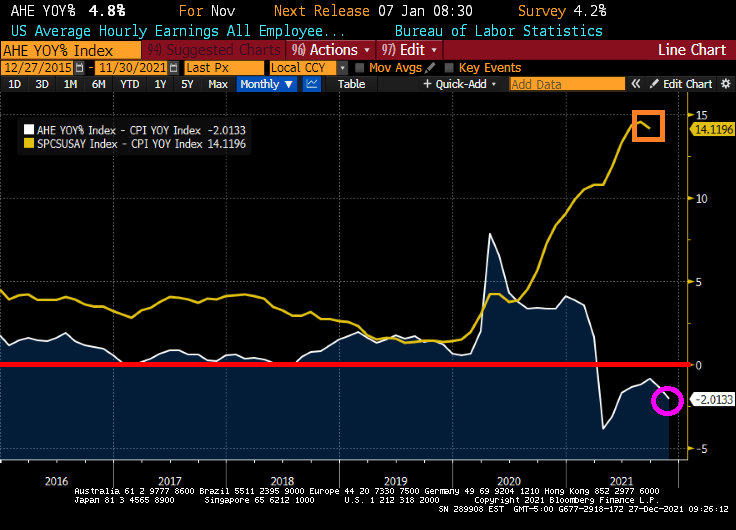

The November jobs report is out and the highlight is that US Average Hourly Earnings GREW at a rate of 4.7% YoY. Unfortunately, inflation is still raging resulting in REAL US Average Hourly Earnings DECLINING at a rate of -1.71% YoY.

REAL US home price growth is slowing and is at 12.856% YoY as REAL average hourly earnings slowed to -1.7094% YoY.

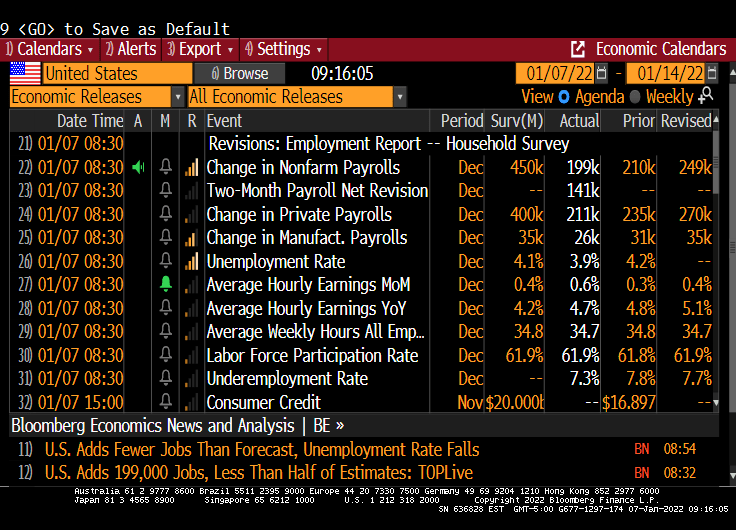

The lowlight of the November jobs report is that only 199K jobs were added versus the 450K jobs expected to be added. At least the unemployment rate fell to 3.9%.

WHERE we the jobs added? Leisure and hospitality led the way! Hey bartender.

Yes, REAL wage growth and REAL home price growth are slowing.

When we look at the Buffett Indicator, we can see how The Federal Reserve’s loose monetary policies (or follycies) are driving up stocks to unsustainable levels that may not survive without The Fed’s “Do Ho Big Bubble Policies.”

How about the Shiller CAPE (Cyclically-adjusted Price/Earnings) ratio? While not up to dot.com levels yet, the Shiller CAPE ratio is climbing with the assistance of The Fed and their insane money printing.

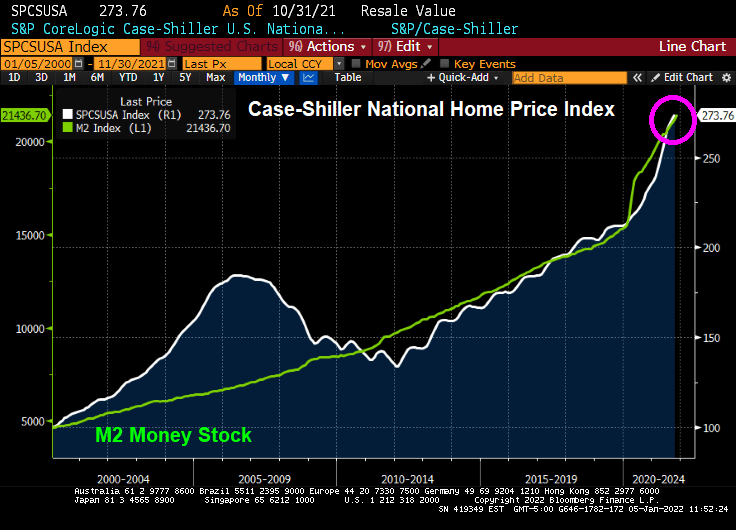

How about house prices? The Case-Shiller National home price index is far above the level last scene during the housing bubble of 2005-2007. Again, with a little help from The Federal Reserve.

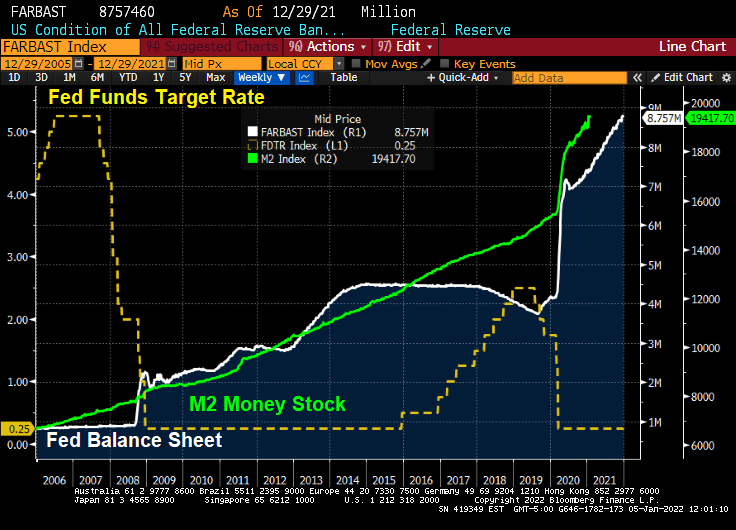

I can’t wait to see how the equity market and housing market reacts IF The Fed actually follows through with reducing monetary stimulus. Probably not just adding more stimulus, just reinvesting the Treasury and MBS proceeds (aka, not shrinking the balance sheet).

A good quote from The Hill story: “Under Biden, the American economy has recovered from its Trump-era lows with remarkable speed.” As Leslie Knope said “That seems like an unfair phrasing.”

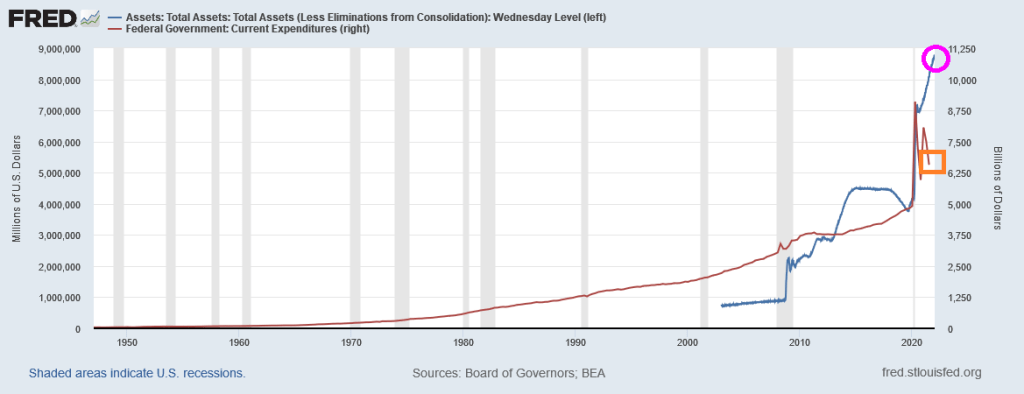

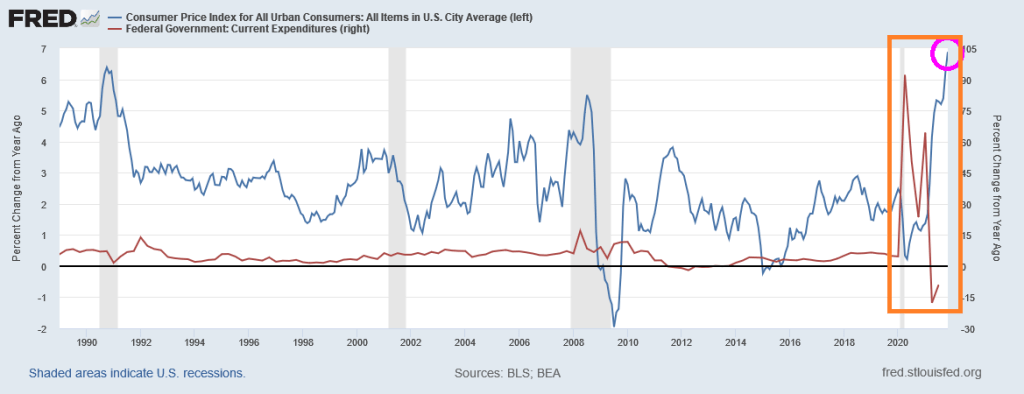

Hmm. Well, here is a chart that best explains the “Biden Miracle.” It shows the growth in Federal expenditures from the previous year during the banking crisis and then the COVID crisis. During the banking crisis, the increase in Federal expenditures (red) was normal. It was the increase in The Fed’s balance sheet (blue) that was staggering. But for the mini-recession related to COVID (only two months so you can barely see it on the chart below), it was the growth in Federal expenditures (red) combined with another round of staggering Federal Reserve stimulus (blue).

A different view of Federal “Stimulypto” is show below. Since COVID and the election of Joe Biden as President, Fed monetary stimulus is at an all-time high and Federal expenditures, while they have slowed, are still above the pre-COVID spending levels.

Please note that the massive surge in Federal expenditures and Fed monetary stimulus began under Trump, but were only continued under Biden. That is why no one notices … it was Trump.

And if we look at the 10Y-2Y Treasury curve slope, the US is slippin’ into darkness since the slope typically rises after a recession, then falls. And we are in the falling (or slippin’) stage.

So, President Biden is benefiting from Trump’s and The Fed’s Stimulypto. I don’t expect partisan outlets like The Hill or crooner Barbra Streisand to look at the data.

With Build Back (Inflation) Better not passing in the US Senate, I fully expect The Federal Reserve to continue “low riding” interest rates. Inflation will probably cool as well as Federal expenditure growth slows.

So, Streisand’s statement should have said “Joe Biden’s economic record in his first year is the best in 40 years. The media largely ignores this … because the unsustainable Federal stimulus began under Trump, not Biden.”

Another thing The Hill and Barbra Streisand left out was declining REAL average hourly earnings growth (that is, average hourly earnings YoY – inflation).

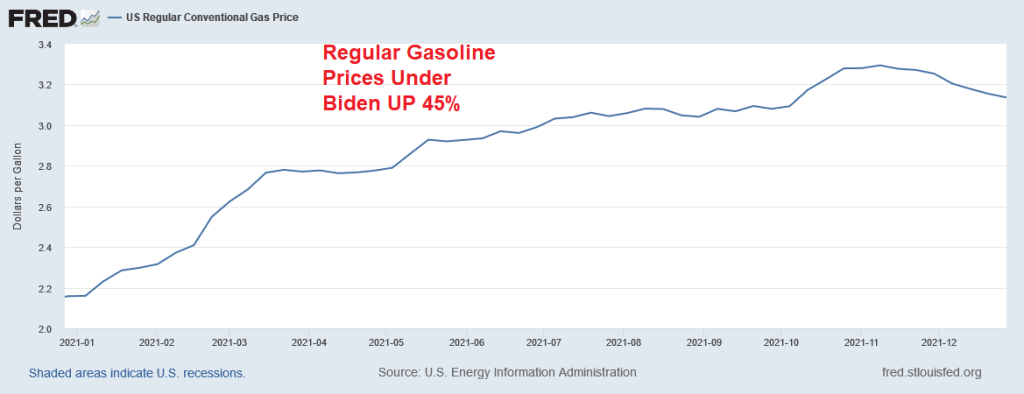

Biden’s real contribution? Anti-fossil fuels actions have driven up energy prices. Regular gasoline prices, for example, are up 45% under Biden.

If The Fed actually follows through and removes COVID stimulus and Congress doesn’t keep the incredible rate Federal spending growing, I sincerely doubt that GDP will continue at this hot pace.

Housing in the US is getting “simply unaffordable.” And it has gotten far worse over the past year. Thanks to BAD government policies.

While wage growth is positive, inflation is sucking the life from consumers. REAL average hourly earnings growth is -2.0133%. Even worse, home prices are rising at a 14.12% pace in REAL terms. So, wages are losing to inflation and housing is pulling away from renters in terms of affordability.`

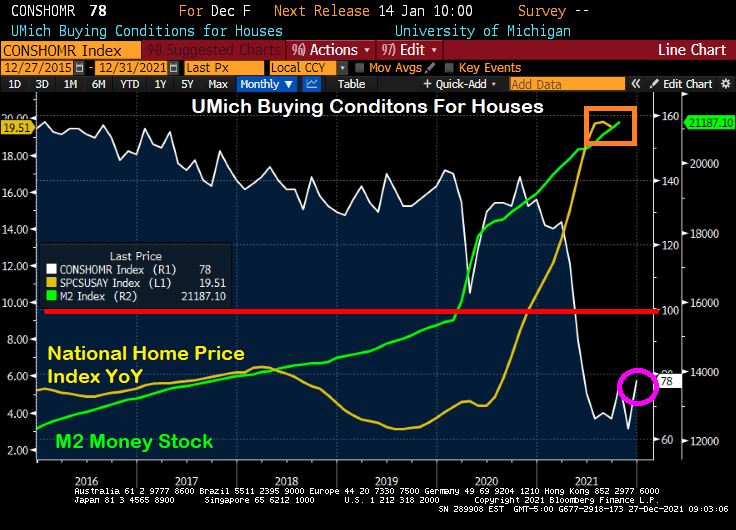

So it is not surprising that the University of Michigan consumer survey for “Buying Conditions For Housing” remains below 100 (meaning that more people think buying conditions for housing are negative than positive). With the Case-Shiller National home price index growing at a 19.51% YoY pace, it is no wonder that consumers are getting scared of the housing market.

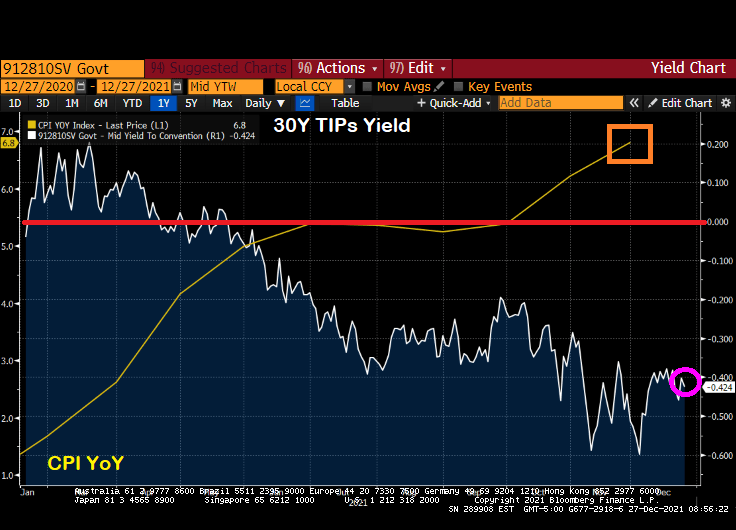

Yes, US inflation is at a 40-year high and the 30-year Treasury Inflation Protected (TIP) yields is at -0.424%. That says quite a bit about the pickle US consumers are in.

US consumer confidence overall has declined to the lowest level since just after the financial crisis and housing bubble burst of 2008-9.

Doctor, Doctor (Yellen), please don’t try to make housing more “affordable” which will result in housing being even LESS affordable.

But I do like how Biden took credit for lowering gasoline prices a little after his anti-energy policies drove up gasoline prices in the first place from $2.20 to $3.40 a gallon, a 55% price increase. Thanks for nothing, Joe!

And with Omicron raging (with few reported deaths), Anthony Fauci, President Biden’s top medical adviser, indicated support for making vaccinations a requirement for domestic fights.

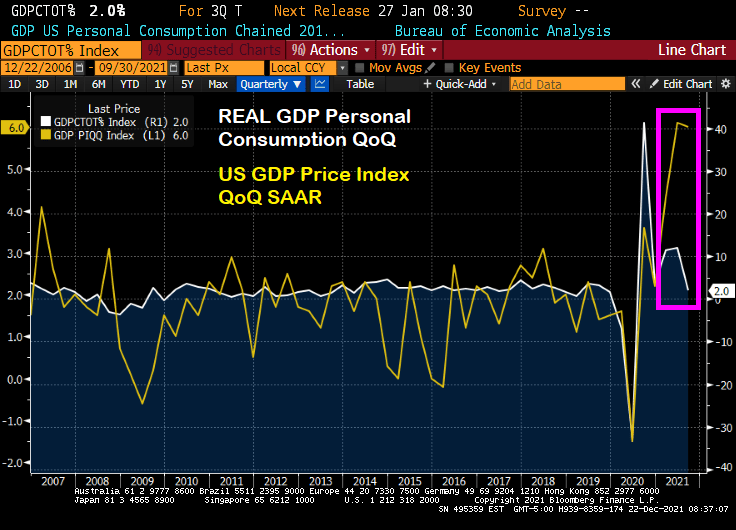

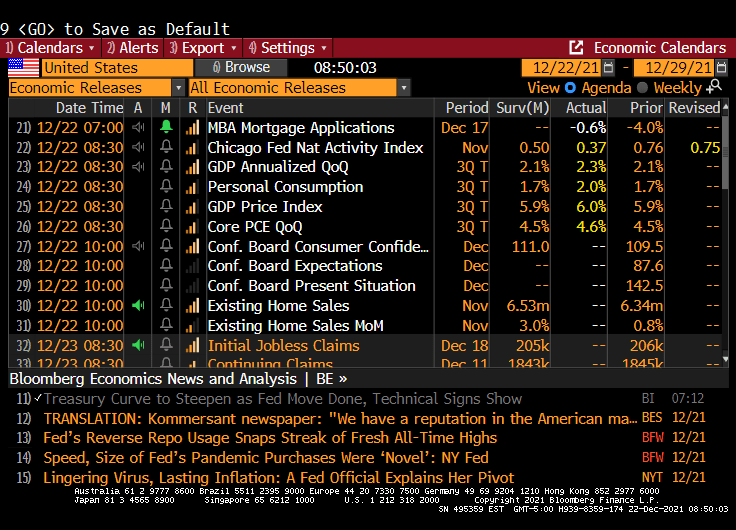

The good news is that US Real GDP grew at 2.3% QoQ in Q3 thanks to massive Federal government and Federal Reserve stimulus. The bad news? Prices are growing at rate of 6% QoQ, three times higher than the growth of real personal consumption.

Runaway inflation, cooling personal consumption. This is the definition of “stimulyltpo”: the excessive spending by Washington DC in conjunction with excessive monetary stimulus from The Federal Reserve.

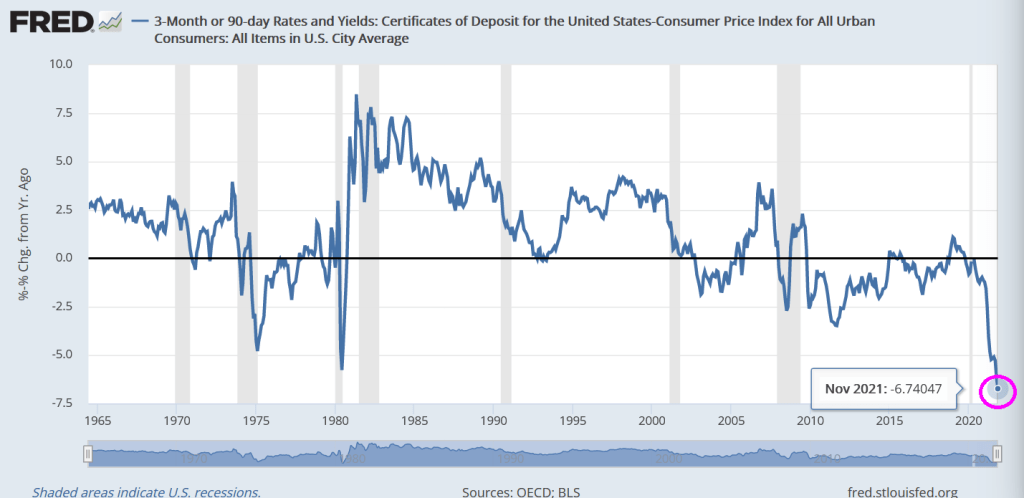

The Federal Reserve’s zero-interest rate policies (ZIRP) has The Fed Funds Target Rate at a measly 25 basis points or 0.25%. While this is great for some, it is disastrous for savers. Once we subtract off the inflation rate (CPI YoY), we find that the REAL 90-day Certificate of Deposit (CD) rate is a horrifying -6.74%.

I don’t think that Congress or the Biden Administration really think about how their spending may contribute to inflation and crush savers. Or the American worker who is seeing NEGATIVE real average hourly earnings growth (yes, Biden said that Americans have more money this holiday season … but not if we account for reduced spending power, also known as inflation.

Here is US Treasury Secretary Janet Yellen singing “Goodbye Savers.”

Goodbye Savers Will we ever meet again Feel sorrow, feel shame Come tomorrow, feel lots of pain

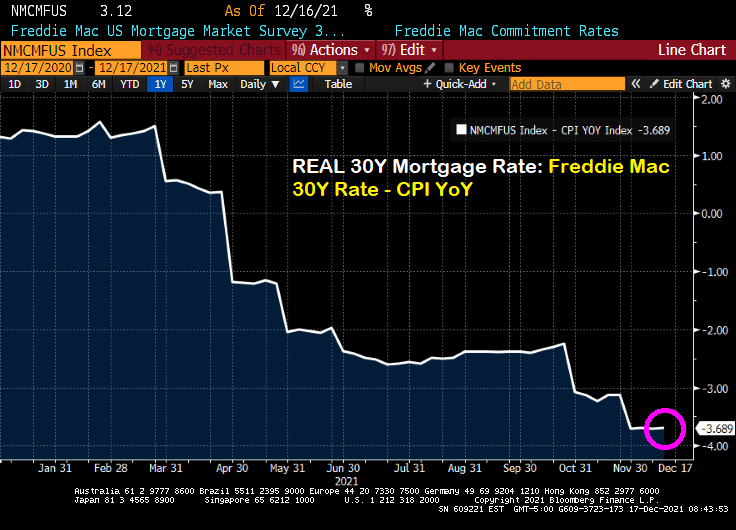

The Freddie Mac 30-year mortgage commitment rate rose to 3.12%. But once we subtract the gut-wrenching inflation rate, the REAL 30-year mortgage rate is -3.689%.

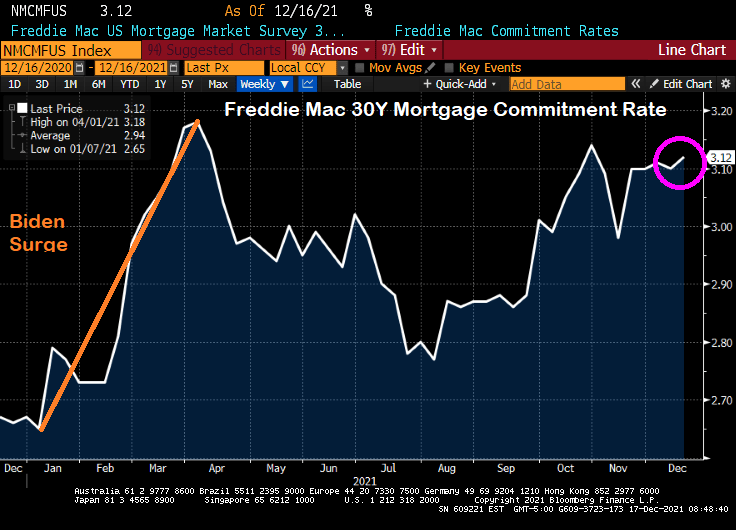

The nominal Freddie Mac 30-year commitment rate rose to 3.12% which is still lower than 3.18% back on April 1, 2021 after surge in rates following Biden’s taking the office of Presidency in January.

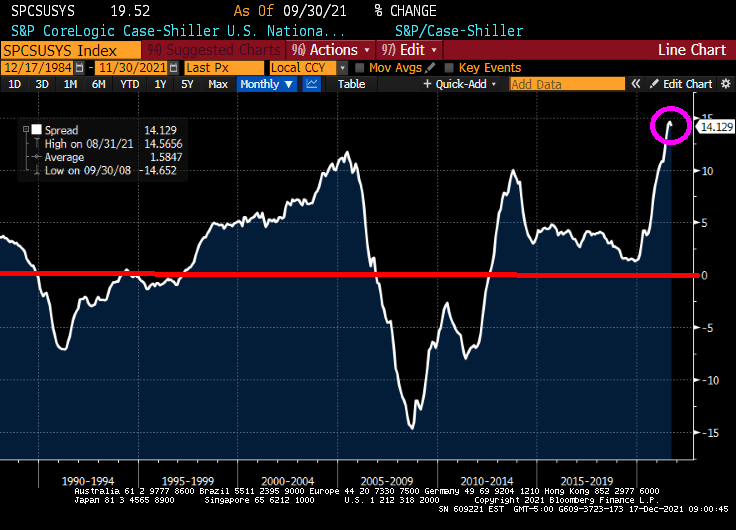

Meanwhile, the REAL Case-Shiller National home price index (CS National YoY – CPI YoY) is growing at the fastest rate in history. Great if you already own a home, but lethal if you are renting and want to move to homeownership.

Meanwhile, REAL wage growth is at -1.94% YoY.

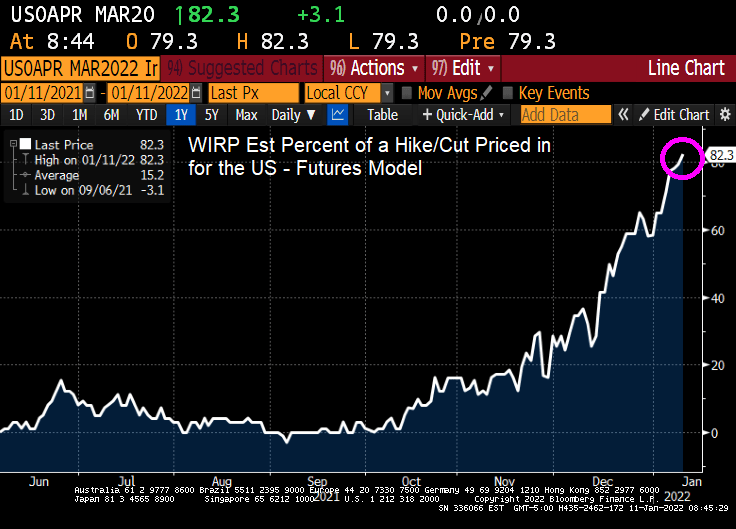

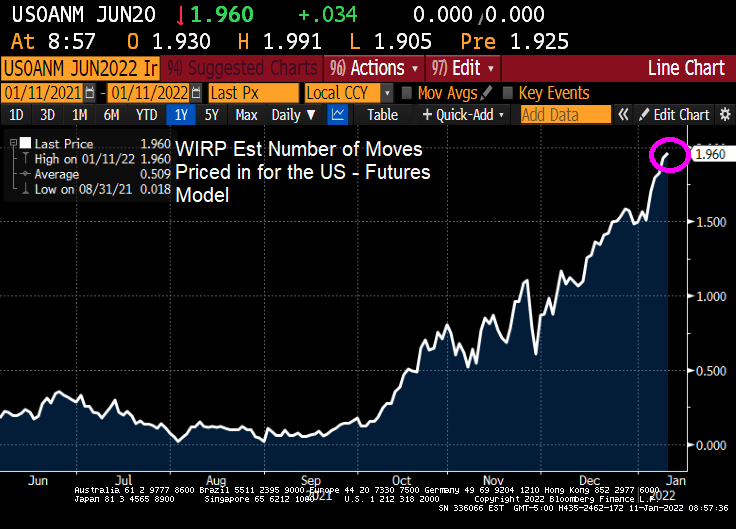

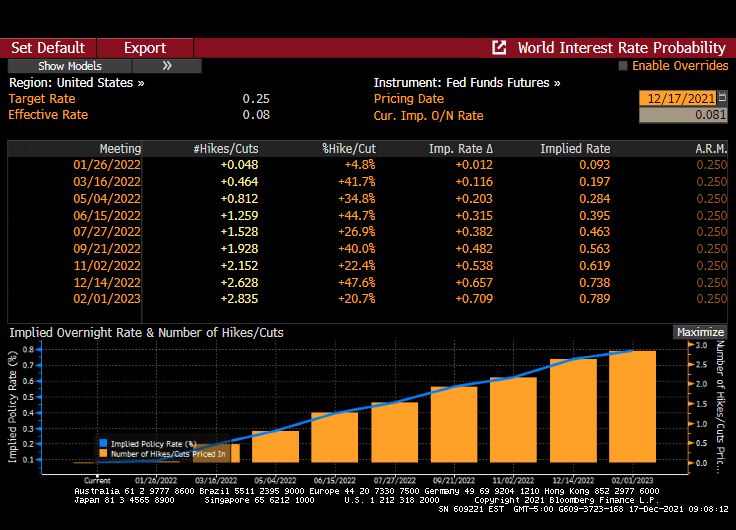

Well, Chairman Powell and The Gang failed to raise the Fed Funds Target Rate yet again, but let us know that they will tighten someday soon. The Fed Funds Futures are signalling a rate hike at the June 2022 meeting and another at the November meeting.

While The Fed couldn’t care less about the Taylor Rule, it is still interesting to note just how out of touch The Fed FOMC is with reality. The Taylor Rule indicates that their target rate should be 16.94% rather than the current target rate of 0.25%.

Keeping the target rate unchanged in the face of gut-wrenching inflation is a bold strategy, Cotton.

Treasury Secretary Janet Yellen said yesterday that “It’s Fed’s Job to Avoid Any Wage-Price Spiral.” Well, The Fed is helping to avoid a wage increase in real terms, since the November jobs report revealed that REAL US Average Hourly Earnings growth YoY fell to -1.378%. In other words, inflation is greater than hourly earnings.

And in other jobs related news, nonfarm payrolls rose by only 210k versus expectations of 550k jobs to be added. Even NOMINAL hourly earnings growth (4.8% YoY) was less than expected (5.0%).

Labor force participation rose a bit to 61.8%, still well below the pre-COVID levels of 63.4% in January 2020.

The U-3 unemployment fell to 7.8%. Still higher than the pre-COVID rate of 7.0% in February 2020, but getting close! As for what this means for The Fed, the new target rate implied by the Taylor Rule is 15.50%.

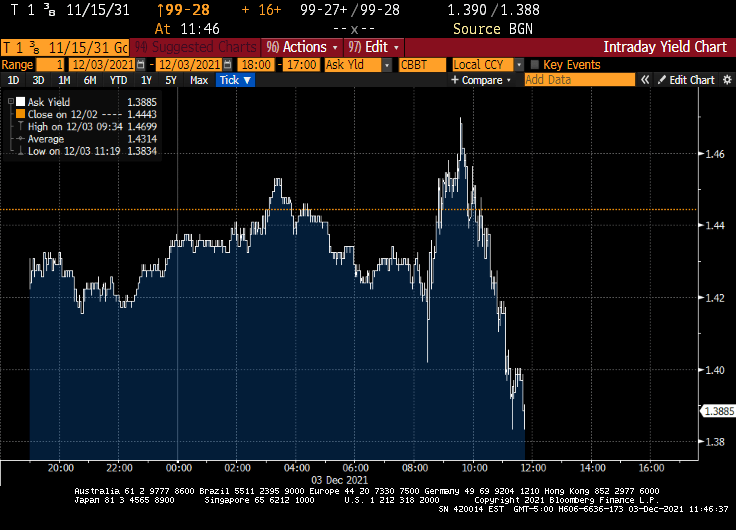

After this lousy jobs report, 10-year Treasury yields dropped … like Biden’s approval ratings.

You must be logged in to post a comment.