No, its not 1903. Its 2025 and Dayton Ohio is the third most affordable city in the USA.

Ohio, the cradle of American Presidents (McKinley, Grant, Taft, Benjamin Harrison, Hayes, Garfield, Harding), is also home to 4 of the most affordable cities in the USA, according to The Virtual Capitalist.

As expected, the Trump Administration levied tariffs against Canada, Mexico, China, etc. The short-term result? Gold is stable, Bitcoin fell. Or as Gene Autry sang, “South of the Border (Down Mexico Way)”.

The stock market? Down -1.53%.

And then we have the doom porn about Mexico’s “impending” collapse. The Peso is declining, and Senator Chuck Schumer is getting hysterical about Mexican exports to the USA for Super Bowl Sunday. He incorrectly claimed that most beer is imported from Mexico and avacados for guacamole. Avacados are also grown in the USA, Peru, etc.

Bear in mind that Mexico is like California where the Left holds a supermajority. Hence, Mexico employs destructive economic policies (it could only be worse if California Governor Gavin Newsom was President of Mexico. But Mexico’s impending collapse is years in the making and Trump’s tariffs were only the last nudge over the cliff. Mexico COULD try to get control over the drug and human trafficking cartels, stop illegal immigration and stop the flow of fentanyl.

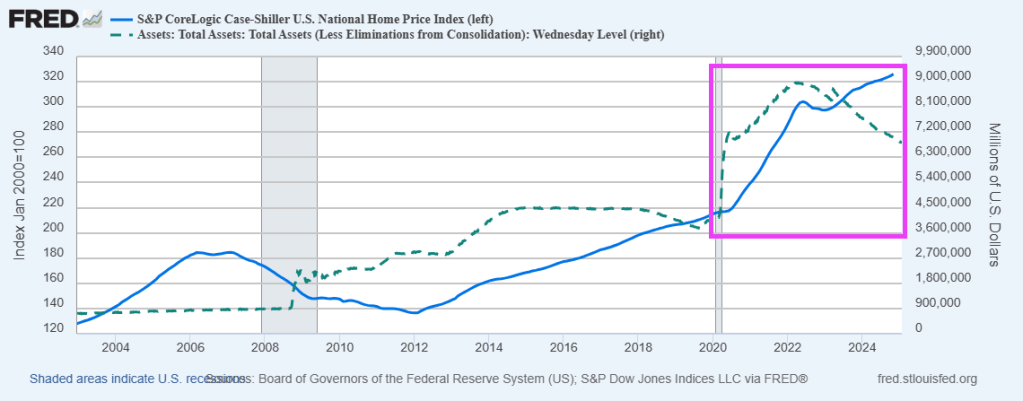

One reason that US home prices remain high (and unaffordable for many) is The Federal Reserve (aka, The Green Slime). Former Fed Chair (and Biden’s Treasury Secretary is no Luciana Paluzzi, the Italian beauty from the James Bond film Thunderball. Yellen is just a far-left economic hack.

Look at the Case-Shiller national home price index compared with The Fed funds target rate.

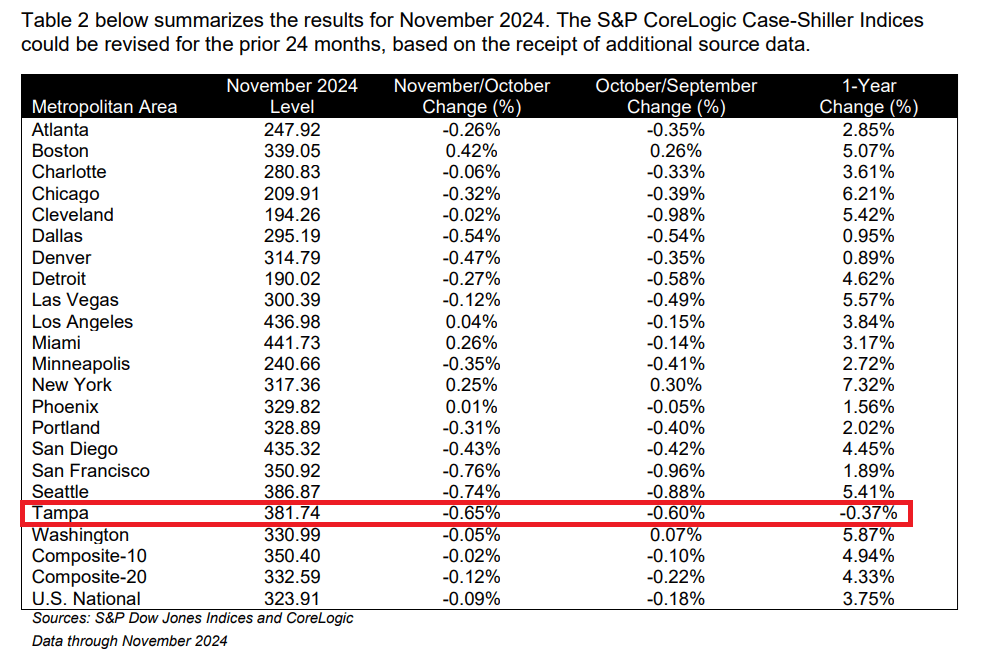

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.8% annual return for November, up from a 3.6% annual gain in the previous month. The 10-City Composite saw an annual increase of 4.9%, recording the same annual increase in the previous month. The 20-City Composite posted a year-over-year increase of 4.3%, up from a 4.2% increase in the previous month. New York again reported the highest annual gain among the 20 cities with a 7.3% increase in November, followed by Chicago and Washington with annual increases of 6.2% and 5.9%, respectively. Tampa posted the lowest return, falling 0.4%.

The pre-seasonally adjusted U.S. National, 20-City, and 10-City Composite Indices’ upward trends continued to reverse in November, with a -0.1% drop for the national index, while the 20-City Composite saw a -0.1% decline and the 10-City Composite was unchanged.

While the Fed Funds target rate gyrates, The Fed’s balance sheet remains high.

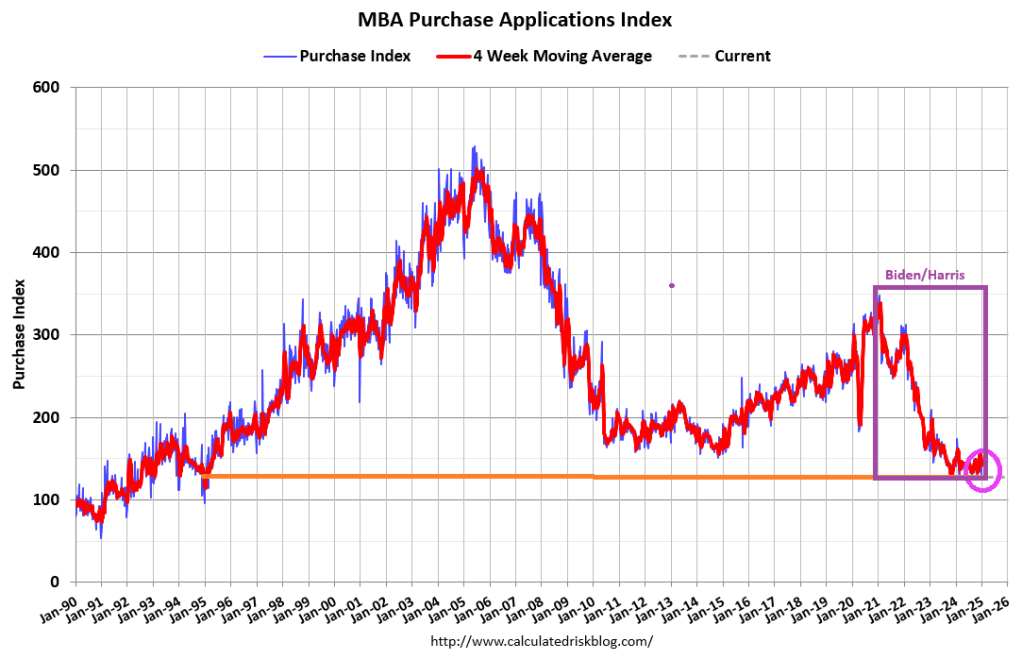

Mortgage applications decreased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 3, 2025. This week’s results include an adjustment for the New Year’s holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 47 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 7 percent from one week earlier. The unadjusted Purchase Index increased 43 percent compared with the previous week and was 15 percent lower than the same week one year ago.

Purchase application activity is up about 2% from the lows in late October 2023 and is now 15% below the lowest levels during the housing bust.

The Refinance Index increased 2 percent from the previous week and was 6 percent lower than the same week one year ago.

Was Freddie King correct? Is the US economy going down??

The US Treasury yield curve (10Y-2Y) has inverted to the positive side after a prolonged NEGATIVE inversion (from July 6, 2022 to Sept 5, 2024) marking the longest period of negative inversion since August 18, 1978 – May 1, 1980. Each negative inversion was followed by a recession.

The UST 10Y-3M yield curve tells a similar tale. The 10Y-3M curve inverts prior to recessions but goes positive just prior to recessions.

Yes, if the yield curve is a good predictor of recession, the US economy is going down.

Freddie King is playing a Gibson ES-355TDC guitar.

The fact that economic conditions are getting worse is certainly not good news, but it is better to know in advance what is coming. After four years under Joe Biden, the U.S. economy is a giant mess. We have been witnessing a slow-motion collapse right in front of our eyes, and those at the bottom levels of the economic food chain have been experiencing more pain than anyone else. Of course this is one of the biggest reasons why Donald Trump won the election.

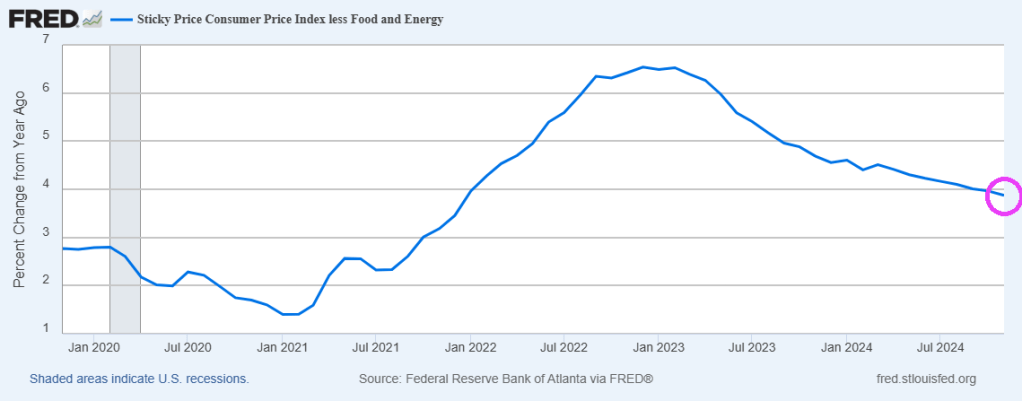

Example? Sticky inflation remains far higher under Biden/Harris than it did when Trump was President. Prices remain elevated as you will notice when Christmas shopping!

#1 When the economy is in good shape, holiday spending increases each year. In 2024, only 16 percent of Americans say that they are going to spend more than last year and 35 percent of Americans say that they are going to spend less…

Americans this holiday season say they are seeing a ghost of Christmas past: inflation.

The CNBC All-America Economic Survey finds inflation is still haunting the buying public, leading to what’s shaping up to be just an average season for retailers. Just 16% of respondents say they will spend more, down two points compared to last year. Forty-eight percent said that they’ll lay out the same amount for holiday gifts, up five points. At the same time, 35% say they’ll spend less, down two points as well.

#2 The number of job openings in the U.S. is now the lowest it has been since January 2021, but unlike January 2021 we don’t have a pandemic to blame our poor performance on…

US job openings tumbled last month to their lowest level since January 2021, a sign that the labor market is losing some momentum. Still, posted vacancies remain well above pre-pandemic levels.

The Labor Department reported Tuesday that the number of job openings dropped to 7.4 million in September from 7.9 million in August.

Economists had expected the level of openings to be virtually unchanged. Job openings fell in particular at healthcare companies and at government agencies at the federal, state and local levels.

#3 The manufacturing numbers that we are getting are extremely dismal. For example, the Philadelphia Federal Reserve Manufacturing Index just experienced an extremely sharp decline…

The Philadelphia Federal Reserve Manufacturing Index, a critical gauge of the general business conditions in Philadelphia, has reported a significant drop. The actual figure stands at -16.4, a sharp decline that suggests worsening conditions for manufacturers in the region.

This figure starkly contrasts with the forecasted number of 2.9, highlighting a more severe downturn than initially predicted. Analysts had anticipated a positive shift, indicating improving conditions, but the actual data presents a different, more concerning situation.

Moreover, when compared to the previous index value of -5.5, the current reading of -16.4 further emphasizes the severity of the decline. This continuous drop indicates a concerning trend for manufacturers within the Philadelphia Federal Reserve district.

#4 Thanks to rapidly rising mortgage rates, the average U.S. homebuyer just lost $33,250 in purchasing power in just six weeks…

Mortgage rates hit 7% on October 28, the highest level since the start of summer and up nearly one percentage point from the 18-month low they dropped to in mid-September.

A homebuyer on a $3,000 monthly budget can afford a $442,500 home with a 7% mortgage rate, the daily average 30-year fixed rate on October 28. That buyer has lost $33,250 in purchasing power over the last six weeks; they could have purchased a $475,750 home with the 6.11% average rate on September 17. That was the lowest level since February 2023.

#5 Our cost of living crisis is officially out of control. According to Bank of America, almost a third of all households “spend more than 95% of their disposable income on necessities such as housing costs, groceries and utility bills”…

Many Americans are still in a tough spot: Nearly 30% of all US households this year said they spend more than 95% of their disposable income on necessities such as housing costs, groceries and utility bills, according to a Bank of America Institute report, up from 2019 levels.

#6 A recent Lending Tree survey discovered that nearly a quarter of all households couldn’t pay their entire power bill at some point within the past year…

LendingTree’s findings about electricity bill costs comes as it reported 23.4% of Americans experienced an inability to cover their entire energy bill or portions of it in the last year, based on Census Bureau Household Pulse Survey data.

#7 The same Lending Tree survey found that about a third of all households had to reduce spending “on necessary things” within the past year in order to pay utility costs…

Needing to cover utility bills prompted 34.3% of Americans to curb their spending on necessary things – or eliminate some altogether – in at least one instance in the prior year, LendingTree said.

#8 As I discussed last week, demand is at record levels at food banks all over the nation…

Why is demand at food banks all over the country higher than it has ever been before? The media keeps insisting that economic conditions are just fine, but it has become quite obvious to everyone that this is not true. In particular, the rising cost of living has been absolutely crushing households from coast to coast. In the old days, most of the people that would show up at food banks were unemployed. But now food banks are serving large numbers of people that actually do have jobs but that don’t make enough to pay for all of the basics. The ranks of the “working poor” are growing very rapidly, and this is creating an unprecedented crisis all over America.

#9 During normal times, troubled retailers would at least wait until after the holiday season to throw in the towel. But we haven’t even reached Christmas and Party City has already announced that it will be closing all stores…

Party City is closing down all of its stores, ending nearly 40 years in business, CNN has learned.

CEO Barry Litwin told corporate employees Friday in a meeting viewed by CNN that Party City is “winding down” operations immediately and that today will be their last day of employment. Staff were told they will not receive severance pay, and they were told their benefits would end as the company goes out of business.

Big Lots is beginning ‘going out of business’ sales at all its stores across the US, as it prepares to close its remaining locations.

The discount retail chain filed for Chapter 11 bankruptcy in September, and has already shut hundreds of stores nationwide.

In a press release Thursday, the company said it would begin the sales at its 963 remaining locations, after a sale to a private equity firm fell through.

#11 As of the end of November, more than 7,000 store closings had been announced in the United States. That is a 69 percent increase from last year…

According to a report from CoreSight Research, U.S. retailers had announced more than 7,100 store closures through the end of November 2024, which represents a 69% increase compared to the same time in 2023. These closures are spread across numerous different sectors of retail from auto parts to restaurants to pharmacies, leaving many consumers wondering which companies will survive. This brings us to GameStop, the beloved retail gaming store, which has not only been closing hundreds of retail store locations since 2020, but also appears to be on track to close hundreds more of its locations in the very near future.

Look at all of these beautiful Christmas decorations at the Crocker Galleria mall in San Francisco. It’s 4:47 PM and everybody should be shopping and buying Christmas presents for their family, but nobody is in this mall.

There are only three stores left that are open here. The escalators hum on inside this beautiful but empty decorated mall.

Outside on Market Street the fentanyl addicts lay folded over while a street performer sings Last Christmas to an empty Street.

Of course the lack of shoppers at that particular mall is just the tip of the iceberg.

California’s biggest downtown areas are crumbling under the weight of homelessness and drug addiction, causing a vital part of its economy to dry out.

Cities like Los Angeles and San Francisco have made countless headlines since the pandemic about their drug-infested streets where businesses are quickly pulling out due to high crime rates and low consumer passage.

The number of drug addicts in America is at the highest level ever.

The number of homeless people in America is at the highest level ever.

They are victims of our slow-motion economic collapse, and the holidays will not be very happy for them.

So if you still have food on the table and a warm home to sleep in, you should consider yourself to be incredibly blessed.

Sadly, more Americans are being forced out into the streets with each passing day as the slow-motion collapse of our economy accelerates.

It is a brave new world as the US attempts an Argentina-like shift from an over-regulated, corrupt economy to a more free economy. While Argentina has Javier Milei, the US is stuck with greedy Democrats and RINOs and their bloated spending sinking any attempt to cut wasteful spending.

So as we transition from woefully corrupt and demented Joe Biden to Donald Trump, the labor market is … terrible. The job finding rate of unemployed workers has collapsed.

This occurred as the Philly Fed Business Outlook plummeted.

Here is Javier Milei of Argentina and The View’s image of a libertarian leader, Javier Bardem from No Country For Old Men.

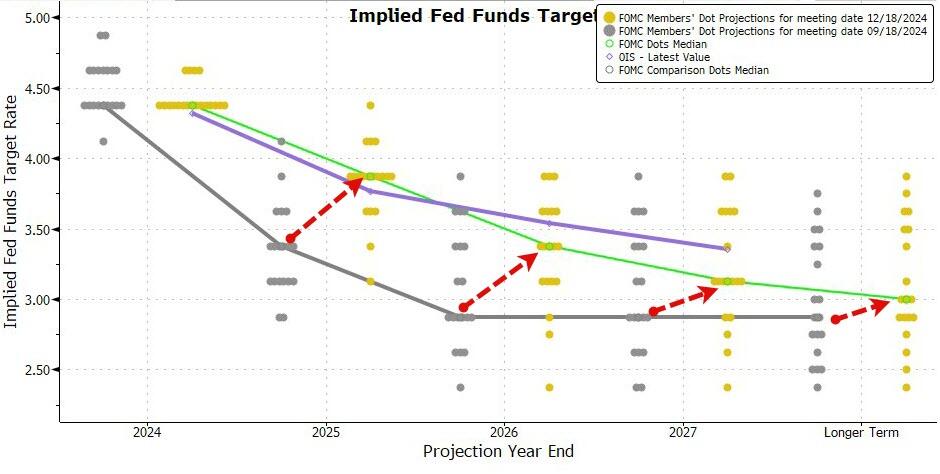

As expected, Powell and The Fed dropped their target rate by 50 basis points yesterday, deflating some of the air in the asset markets, More rate cuts will come, but at a slower rate.

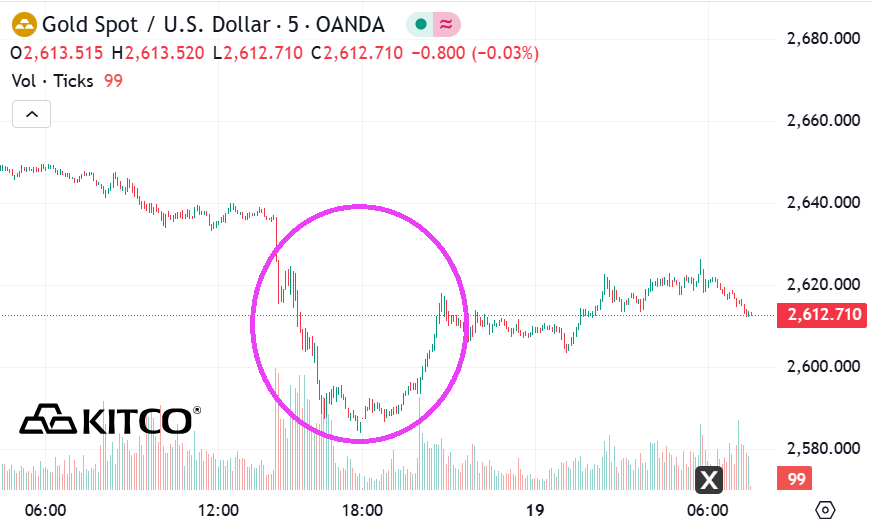

Gold got clobbered but has somewhat rebounded.

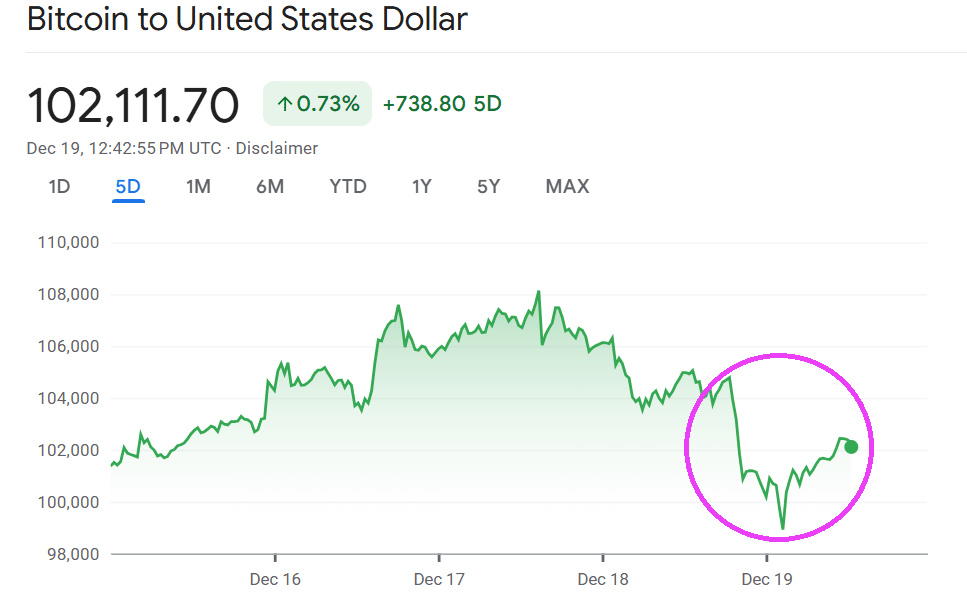

Bitcoin did likewise: dropping like a rock then bouncing back somwhat.

But gold and bitcoin/ethereum are down again.

The CBOE VIX volatility index exploded upwards.

Powell is looking old, like most of Congress and Biden.

Joe Biden is leaving the Presidency with an attrocious record. While saying he is leaving Trump with the strongest economy in modern times, the is actually leaving Trump and Republicans with a hollow shell for an economy. It is the final punch in the jaw from an angry, failed President.

The following chart shows that in October and November, the US deficit exploded to a staggering $624.2 billion, and even though this included several calendar adjustments – which explains the freak September surplus which as we said was due to calendar effects – the November deficit of $367 billion was $14 billion more than consensus estimates of $353 billion. Worse, combining October and November we find that not only was the combined number of $624 billion some 64% higher than the corresponding period one year ago, but it was also the highest deficit on record for the first two-months of the year (and that includes the spending insanity during the covid crisis).

Putting the deficit in context, the budget deficit in October and November – the first two months of fiscal 2025 – are now officially the worst start a year for the US Treasury on record.

No wonder even Statist Janet Yellen (Treasury Secretary who failed utterly at her job) apologized that her abysmal performance. “I am concerned about fiscal sustainability and I am sorry that we haven’t made more progress,” she said adding that “I believe that the deficit needs to be brought down especially now that we’re in an environment of higher interest rates.” Meanwhile Biden keeps handing out $$$ to Ukraine, Africa, Syria, illegal immigrants and anything else that asks … unless it it American citizens. Man, does Biden HATE America!

Here is Yellen’s record on debt. A total of $15.2 TRILLION under her leadership.

Under Biden/Yellen (don’t forget Senate fools like Schumer and McConnell!), debt interest has surpassed Social Security and Medicare as the second largest government agency expense.

Biden is a classic progressive Democrat, spending other people’s money like a wild man (sort of like California Governor “Greasy Gavin” Newsom’s father. Or grandfather. And let’s not forget the $222 TRILLION in UNFUNDED liabilities such as Social Security and Medicare.

“See Joe, I can destroy California’s economy just like you destroyed the US economy!”

October STICKY core inflation is still up 4% YoY (year-over-year)

Core CPI rose 0.3% MoM (as expected) which pushed it up 3.3% YoY (not even close to the 2% mandate)…

Source: Bloomberg

There has not been a single monthly decrease in core consumer prices since Biden too office.

dddd

Between The Fed’s insane monetary policy and Biden/Harris insane fiscal policies, we are living in a world where Ray Bradbury’s novel Fahrenheit 451 becomes a reality. Instead of books burning, it is the US Dollar burning.

{kind=link}

You must be logged in to post a comment.