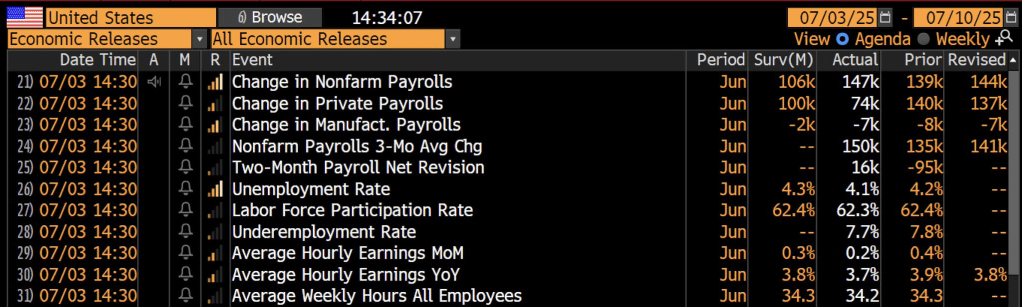

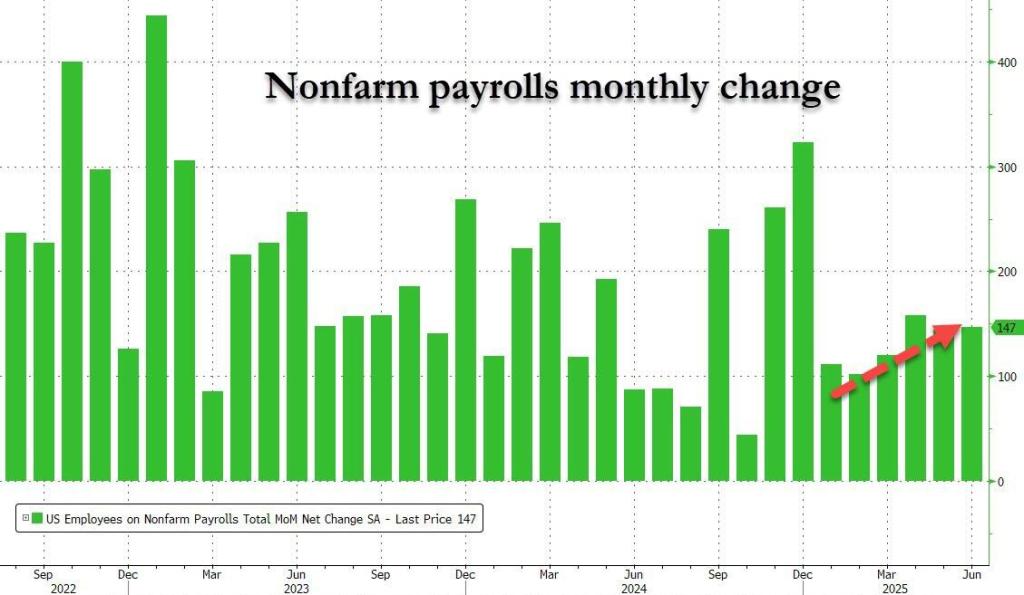

So much for the doom porn about tariffs or anything Trump. The US economy is booming. Example? Non farm payrolls (NFPs) in June rose by 147k jobs added.

As opposed to yesterday’s negative ADP report, the NFP continued to grow despite fears of tariffs, etc.

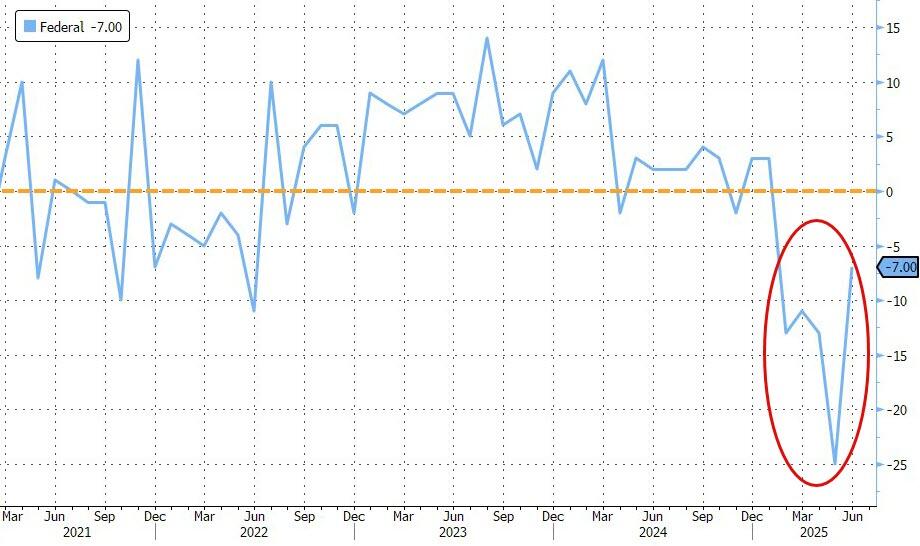

- Government employment rose by 73,000 in June. Employment in state government increased by 47,000, largely in education (+40,000). Employment in local government education continued to trend up (+23,000). Job losses continued in federal government (-7,000), where employment is down by 69,000 since reaching a recent peak in January.

- Health care added 39,000 jobs in June, similar to the average monthly gain of 43,000 over the prior 12 months. In June, job gains occurred in hospitals (+16,000) and in nursing and residential care facilities (+14,000).

- In June, social assistance employment continued to trend up (+19,000), reflecting continued growth in individual and family services (+16,000).

The positive jobs report likely killed any chance of a Fed rate cut at the next meeting.

You must be logged in to post a comment.