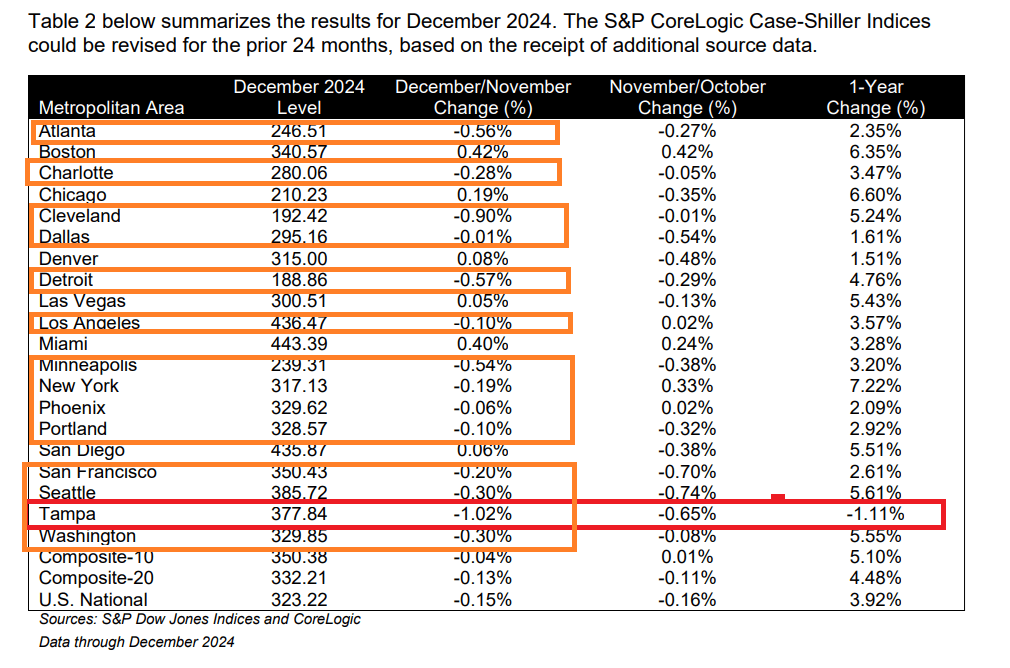

For the second straight month, US home prices accelerated YoY in December (according to the latest data from S&P Global’s Case-Shiller Index). The 20-City Composite saw prices jump 0.5% MoM (faster than expected and the biggest jump since June) and accelerating MoM for the 3rd straight month.

Only Tampa FLA of the top 20 metro areas had a negative YoY price change, but 14 of the top 20 metro areas experienced price declines from November to December: Atlanta, Charlotte, Cleveland, Dallas, Detroit, Los Angeles, Minneapolis, New York, Phoenix, Portland, San Francisco, Seattle, Tampa and Washington DC.

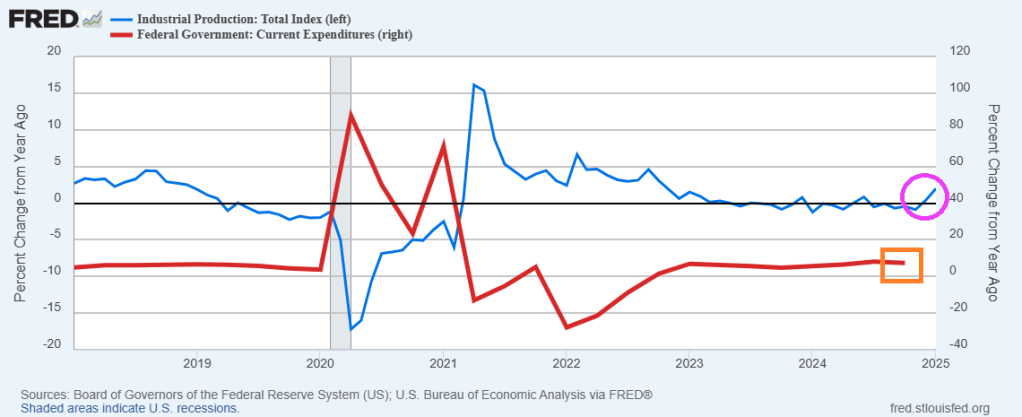

In January, US Industrial Production rose 2.00% YoY, the strongest growth rate since Oct 2022.

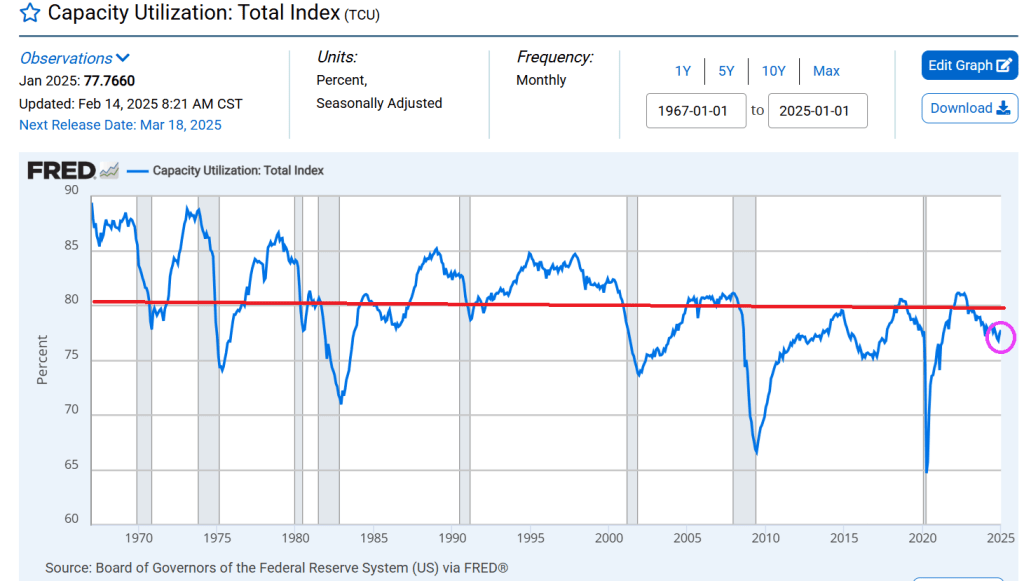

Capacity Utilization accelerated again in January (2nd straight month), rejecting the recessionary red flags. But CAPUTE remains below the critcal measure of 80.

Biden is out and so are the crazy job preferences of his administration (e.g., green energy). There is a new sheriff in town (Donald Trump).

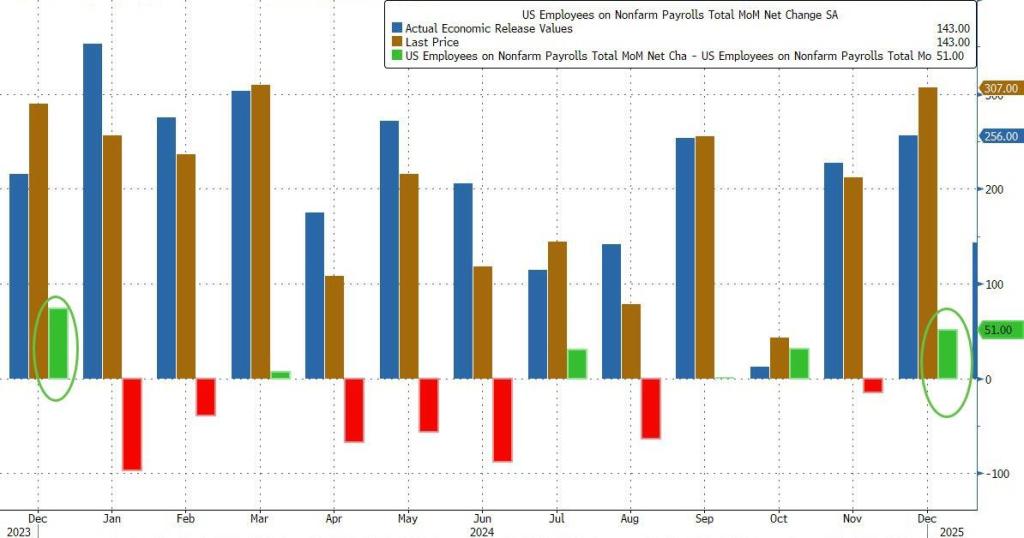

Here’s what the BLS reported in Trump’s first official jobs report since he returned to the White House: total payrolls printed at 143K.

down sharply from an upward revised 307K (256K originally) and missing estimates of 175K.

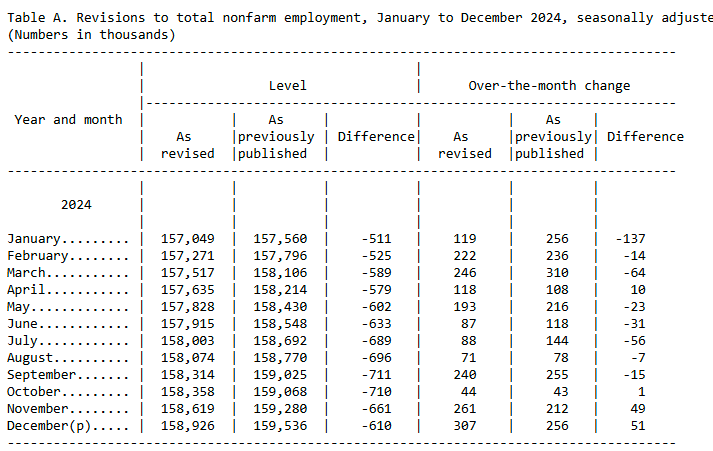

Looking further back, the change in total nonfarm payroll employment for November was revised up by 49,000, from +212,000 to +261,000, and when adding the +51,000 revision to December employment in November and December combined is 100,000 higher than previously reported

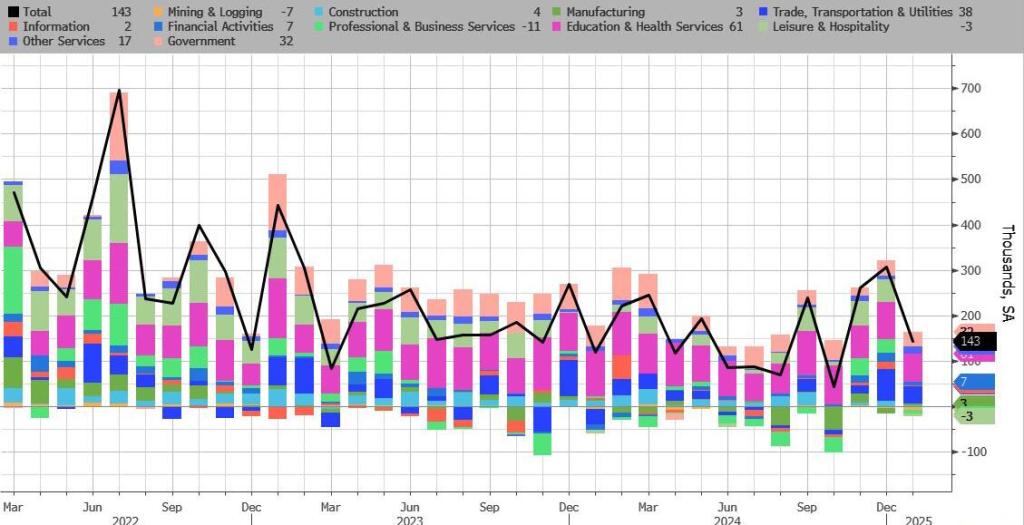

But while the sequential change in the Establishment survey was notable, what was far more remarkable was the Household survey where we saw massive population related revisions (discussed last night), which pushed the civilian labor force higher by 2.2 million to 170.744 million, while the number of employed workers also increased by over 2.2 million to 163.895 million. As a result, the Household survey has finally caught up to Establishment survey.

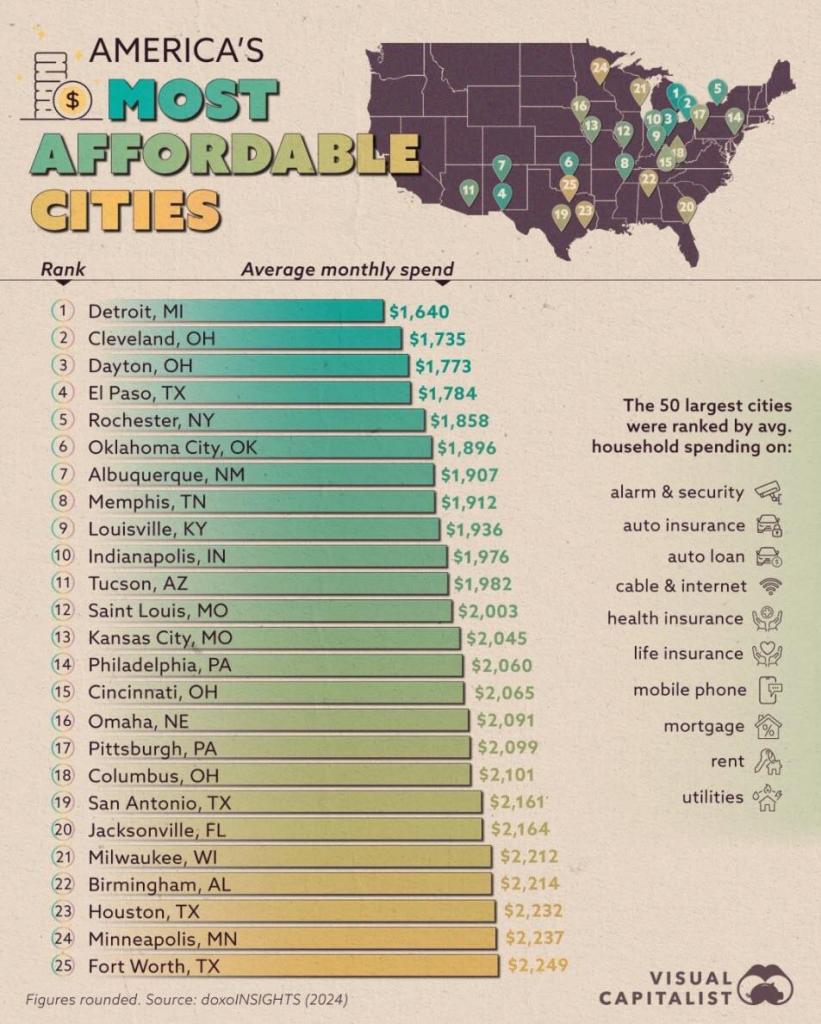

No, its not 1903. Its 2025 and Dayton Ohio is the third most affordable city in the USA.

Ohio, the cradle of American Presidents (McKinley, Grant, Taft, Benjamin Harrison, Hayes, Garfield, Harding), is also home to 4 of the most affordable cities in the USA, according to The Virtual Capitalist.

As expected, the Trump Administration levied tariffs against Canada, Mexico, China, etc. The short-term result? Gold is stable, Bitcoin fell. Or as Gene Autry sang, “South of the Border (Down Mexico Way)”.

The stock market? Down -1.53%.

And then we have the doom porn about Mexico’s “impending” collapse. The Peso is declining, and Senator Chuck Schumer is getting hysterical about Mexican exports to the USA for Super Bowl Sunday. He incorrectly claimed that most beer is imported from Mexico and avacados for guacamole. Avacados are also grown in the USA, Peru, etc.

Bear in mind that Mexico is like California where the Left holds a supermajority. Hence, Mexico employs destructive economic policies (it could only be worse if California Governor Gavin Newsom was President of Mexico. But Mexico’s impending collapse is years in the making and Trump’s tariffs were only the last nudge over the cliff. Mexico COULD try to get control over the drug and human trafficking cartels, stop illegal immigration and stop the flow of fentanyl.

Wow. Money printing by The Federal Reserve went will after the Covid outbreak in early 2020. So did Federal spending. Unfortunately, politicians are addicted to Federal spending. And Senators like Chuck Schumer (D-NY) and Adam Schiff (D-CA) are trying to obstruct any spending cuts by Trump and his DOGE.

Well, M1 Money printing is UP 365% since Covid while M2 Money printing is UP 40%.

Federal current expenditures are up 45% since the Covid outbreak. But were never returned to normal spending levels.

New York senator Chuck Schumer is opposed to Trump’s efforts to cut Federal spending. Is Senator Schumer REALLY the political boss of Tammany Hall, the Democratic Party’s political machine that played a major role in the politics of 19th-century New York City and State?

Sales of new US homes ended 2024 on a high note in December as customers took advantage of incentives from builders, leading to a second straight year of increased purchases.

For the full year, customers purchased 683,000 homes, up about 2.5% from 2023’s total.

Sales of new single-family houses in December 2024 were at a seasonally adjusted annual rate of 698,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 3.6 percent above the revised November rate of 674,000 and is 6.7 percent above the December 2023 estimate of 654,000.

The Visual Capitalist calls most unaffordable cities as least affordable. San Jose California and New York City are the two most unaffordable cities in the USA. According to household spending.

Fortunately, I live in Columbus Ohio. the 18th most affordable city in the USA.

Much of the difference amongst cities is land use and construction restraints. And booming/dying local economies.

As a sad reminder about the last four years, Pete Buttigieg will leave his post as Transportation Secretary having spent $7.5 BILLION to build 8 EV charging stations.

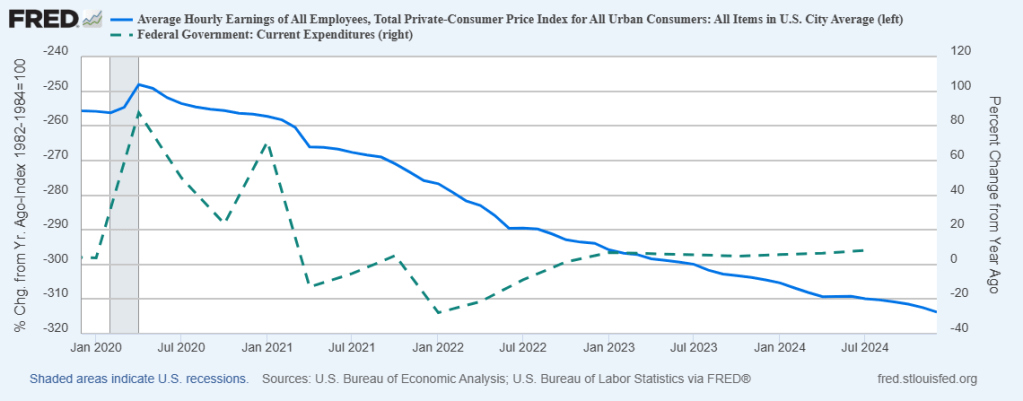

I can’t wait for Billions Biden, The DC parasite who selectively shoves billions of dollars to his friends and nothing for the others. For example, bailing out the LA wildfires but stiffing the people of North Carolina and Florida for hurricane/flood damage. And funding Ukraine while real wage growth is negative. And heavy investment in green energy, the ultimate fool’s errand.

Let’s start with declining real wage growth under Biden/Harris (blue line). Meanwhile, Federal government spending (dashed green line) continues to grow causing inflation.

Meanwhile, Biden/Harris and Congress left Trump with the largest budget deficit in history. Like endlessly funding Ukraine and illegal immigration.

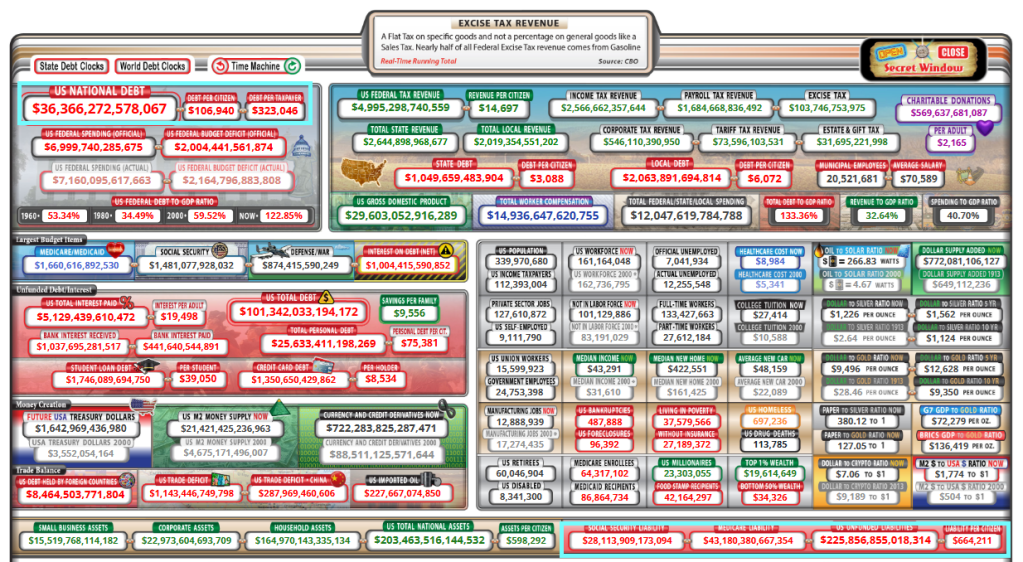

Leaving American taxpayers with growing Federal debt of $36+ trillion. And unfunded liabilities of $226 trillion, over 6 times the national debt.

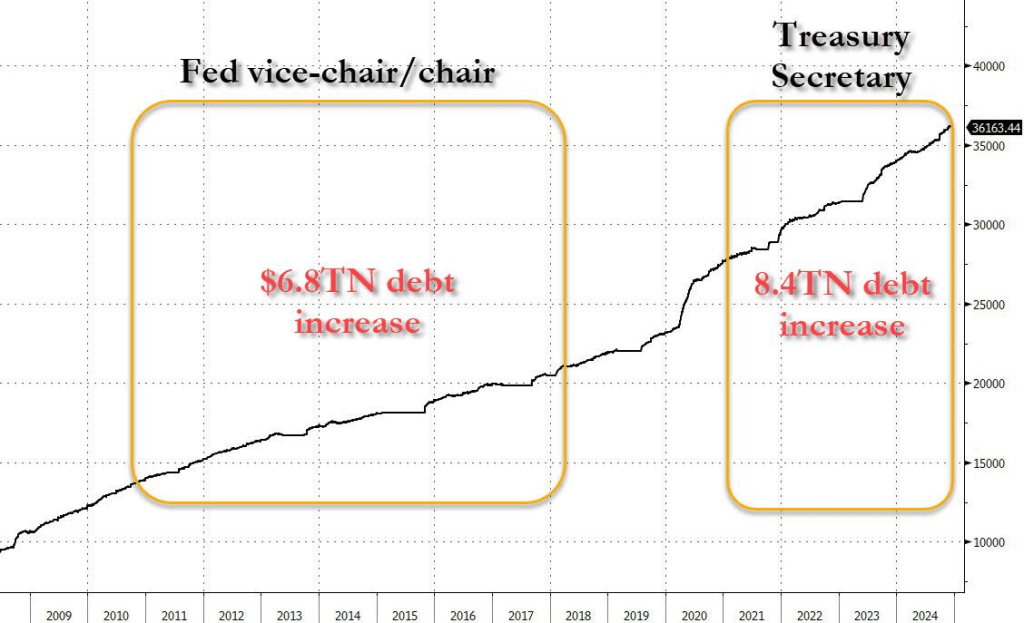

The US will hit its debt ceiling the day after President Trump is inaugurated, and Yellen said that the Treasury will launch “extraordinary measures” to stave off the threat of a national default. Bear in mind, Janet Yellen personally oversaw total debt increase by a staggering $15 trillion. Way to go, Janet!

I wonder how Trump’s Treasury secretary will handle this? At least better than Janet Yellen, I hope!

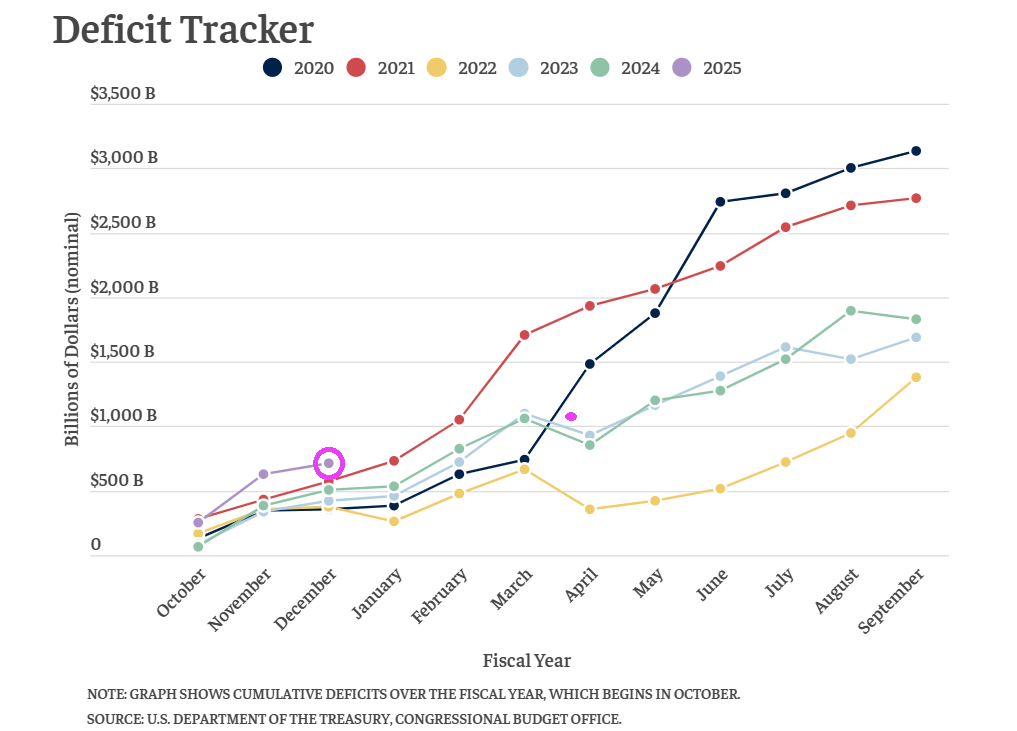

This is the worst start to a fiscal year EVER: – Spending is up 10.9% – Receipts are down 2.2% – FYTD deficit up 39.4% at $711 billion They’re handing Trump a ticking time bomb!

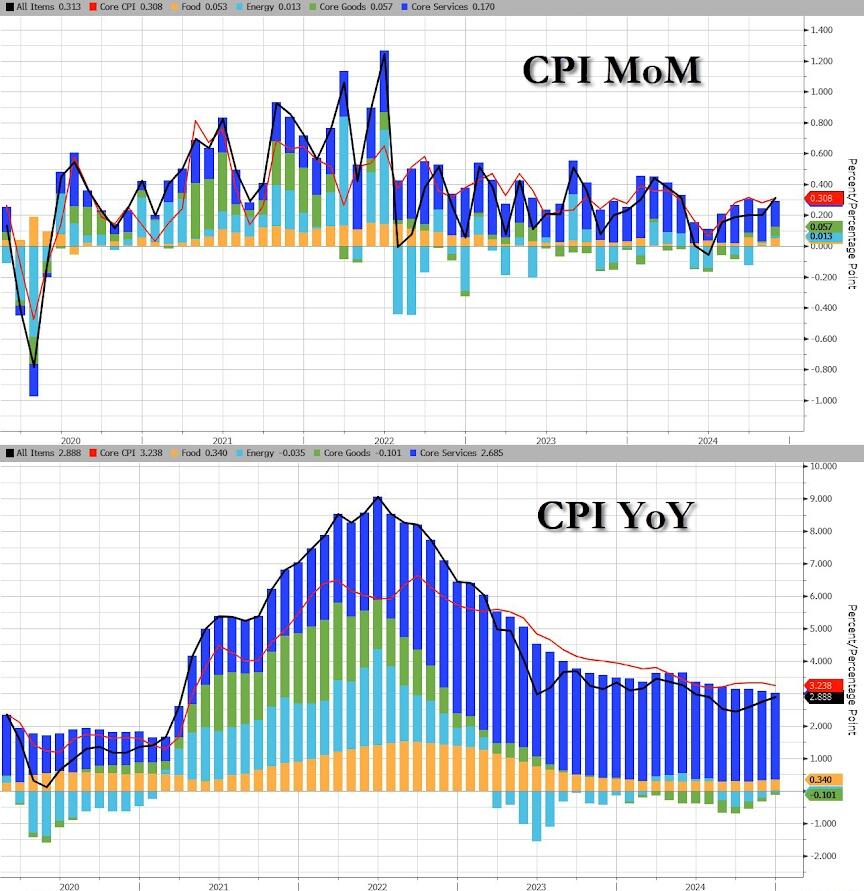

Speaking of Biden handing a ticking time bomb (according to Zero Hedge), after rising for 5 straight months, analysts expected headline consumer prices to continue accelerating in December (+0.4% MoM exp) and it did exactly that – the highest MoM print since March, leading the YoY CPI to rise 2.9% (the highest since July)…

Source: Bloomberg

CPI details:

Food

The index for food increased 0.3% in December, after rising 0.4% in November. The food at home index also rose 0.3% over the month. Four of the six major grocery store food group indexes increased in December. The index for cereals and bakery products rose 1.2% over the month, after falling 1.1% in November. The meats, poultry, fish, and eggs index increased 0.6 percent in December, as the eggs index rose 3.2 percent. The index for other food at home rose 0.3 percent over the month and the index for dairy and related products increased 0.2 percent.

Energy

The energy index increased 2.6% in December, after rising 0.2% in November. The gasoline index increased 4.4% over the month. (Before seasonal adjustment, gasoline prices decreased 1.1 percent in December.) The natural gas index rose 2.4 percent over the month and the index for electricity rose 0.3 percent in December. The energy index decreased 0.5 percent over the past 12 months. The gasoline index fell 3.4% over this 12-month span and the fuel oil index fell 13.1 percent over that period. In contrast, the index for electricity increased 2.8 percent over the last 12 months and the index for natural gas rose 4.9 percent.

All items less food and energy

The index for all items less food and energy rose 0.2 percent in December, after rising 0.3 percent in each of the 4 preceding months.

The shelter index increased 0.3 percent in December, as it did in November.

The index for owners’ equivalent rent also rose 0.3 percent over the month, as did the index for rent.

The lodging away from home index fell 1.0 percent in December, after rising 3.2 percent in November.

The medical care index increased 0.1 percent over the month, after rising 0.3 percent in October and November.

The index for physicians’ services increased 0.1 percent in December and the index for hospital services rose 0.2 percent over the month.

The airline fares index rose 3.9 percent in December, after rising 0.4 percent in the previous month.

The index for used cars and trucks rose 1.2 percent over the month and the index for new vehicles increased 0.5 percent.

Other indexes that increased in December include motor vehicle insurance, recreation, apparel, and education.

In contrast, the index for personal care fell 0.2 percent in December after rising 0.4 percent in November. The indexes for communication and alcoholic beverages also declined over the month. The household furnishings and operations index was unchanged in December

The resurgence of energy costs drove the hot headline CPI along with Core Services…

Source: Bloomberg

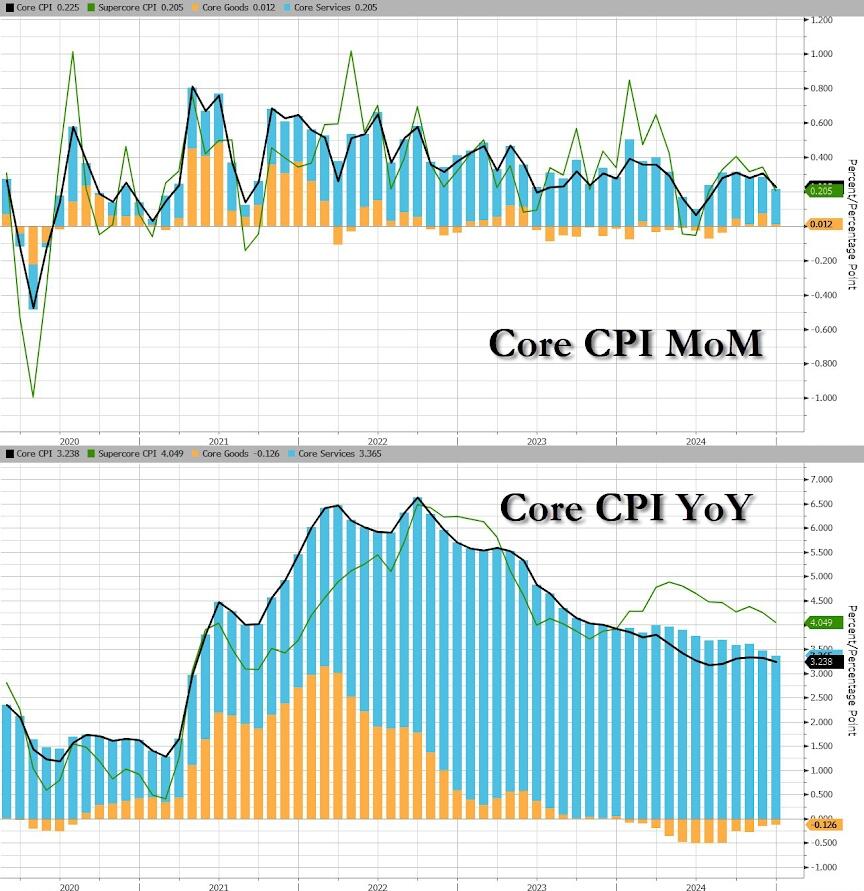

Core CPI (ex Food and Energy) dipped to +0.2% MoM (below the 0.3% exp) and the YoY pace of inflation slowed to 3.24% YoY. Core CPI rose EVERY month under Biden…

Source: Bloomberg

Core Goods price inflation slowed MoM (but deflation is gone on a YoY basis)…

Source: Bloomberg

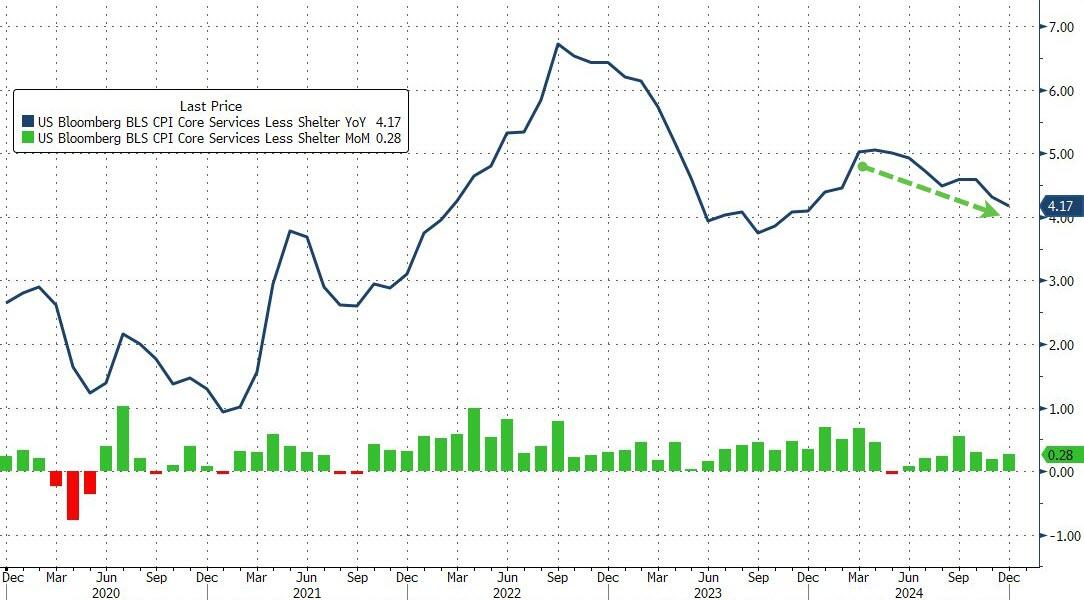

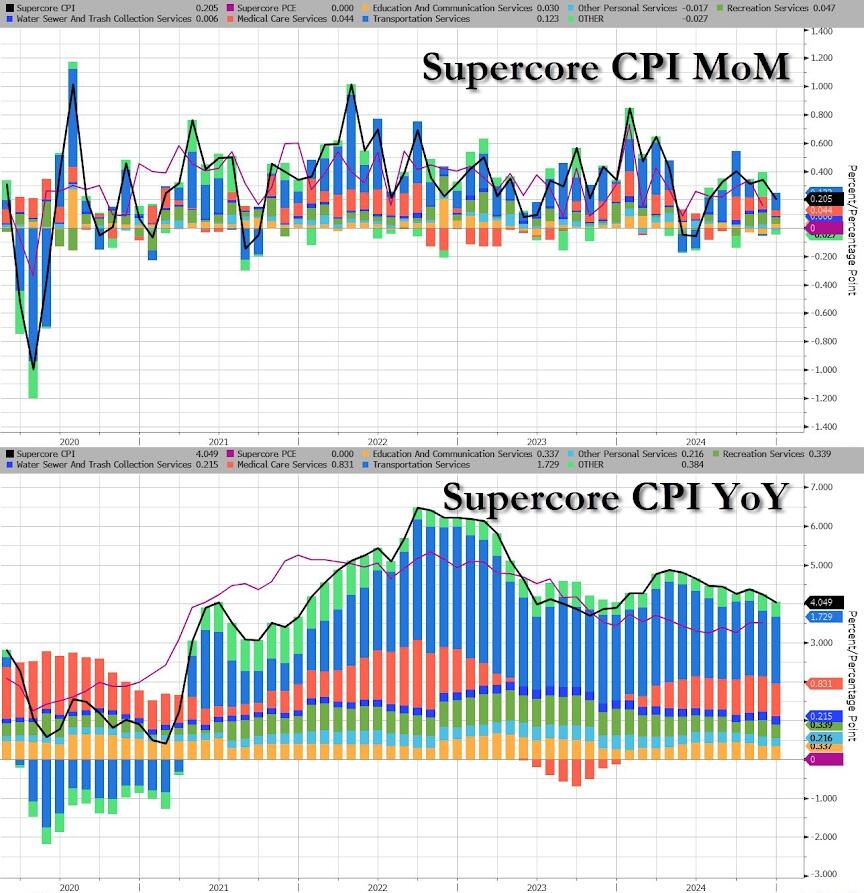

The Fed’s favorite indicator of the CPI bunch – SuperCore or Services CPI ex-Shelter – rose 0.28% MoM (slowing the pace of annual inflation to +4.17%)…

Source: Bloomberg

Transportation Services were not MoM…

Source: Bloomberg

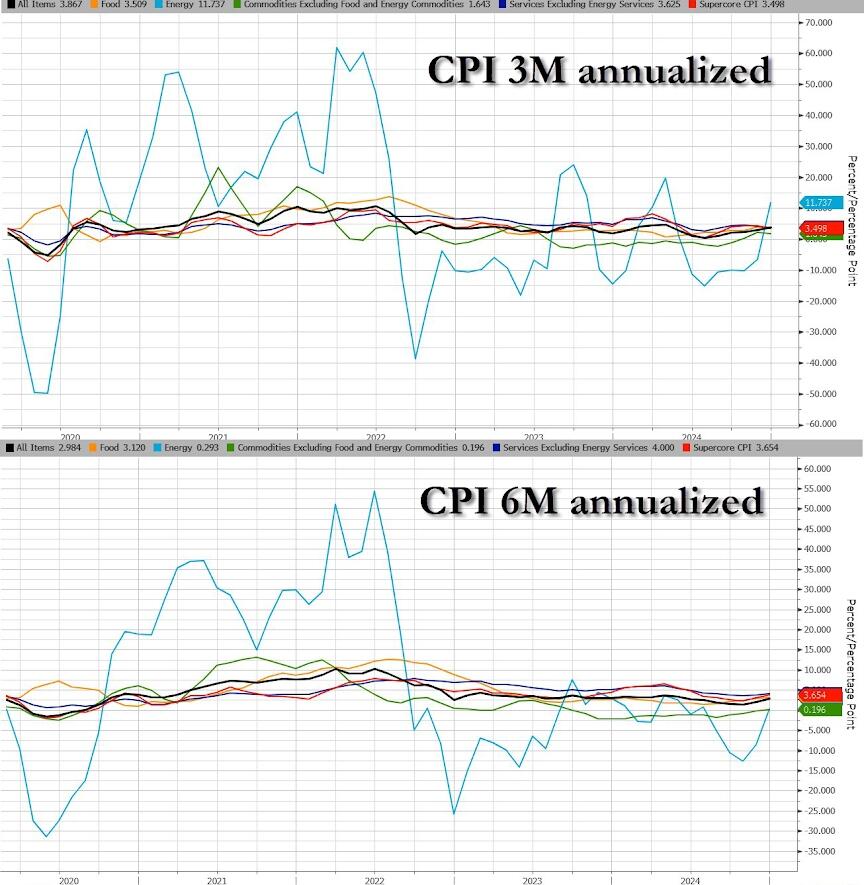

Overall, it’s energy costs that are re-emerging as a drive of inflation… thanks Joe!

Source: Bloomberg

…and Energy prices aren’t going down anytime soon in the CPI world… thanks Joe!

Source: Bloomberg

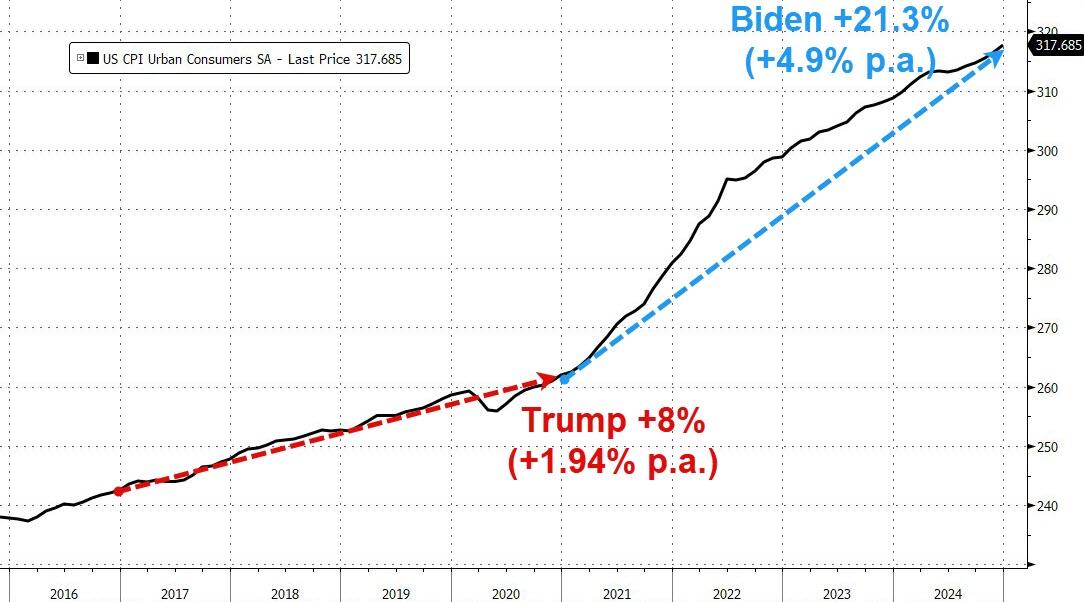

While Producer Prices under Biden rose at triple the rate they did under Trump, Consumer Prices soared 21.25% under Biden (+4.9% p.a.) vs 8%, 1.94% p.a. under Trump…

Source: Bloomberg

Finally, equity traders were braced for a volatile day ahead of the print, with options implying moves of 1.1% in either direction for the S&P 500, the most for a CPI day since March 2023.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.