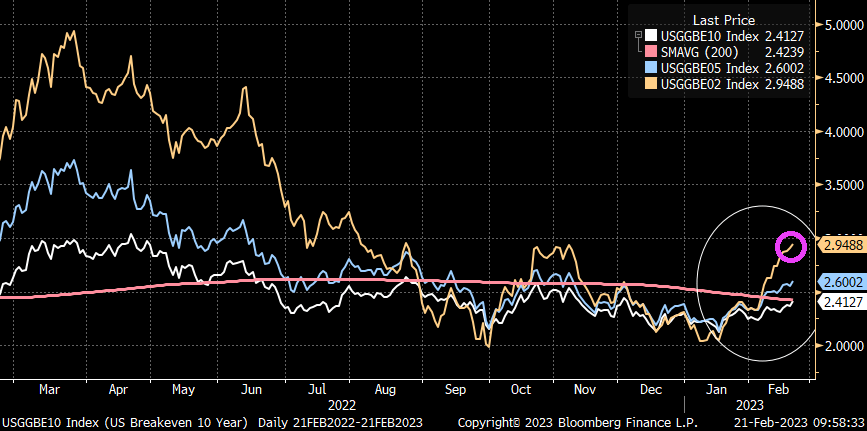

But before I go for experimental therapy for my brain tumor, I will leave you with this diddy. Inflation expectations are on the rise, not falling like Biden and Yellen keep screaming.

On the corporate side, US bankruptcies in 2023 had the worst start to a year since 2010 and the financial crisis.

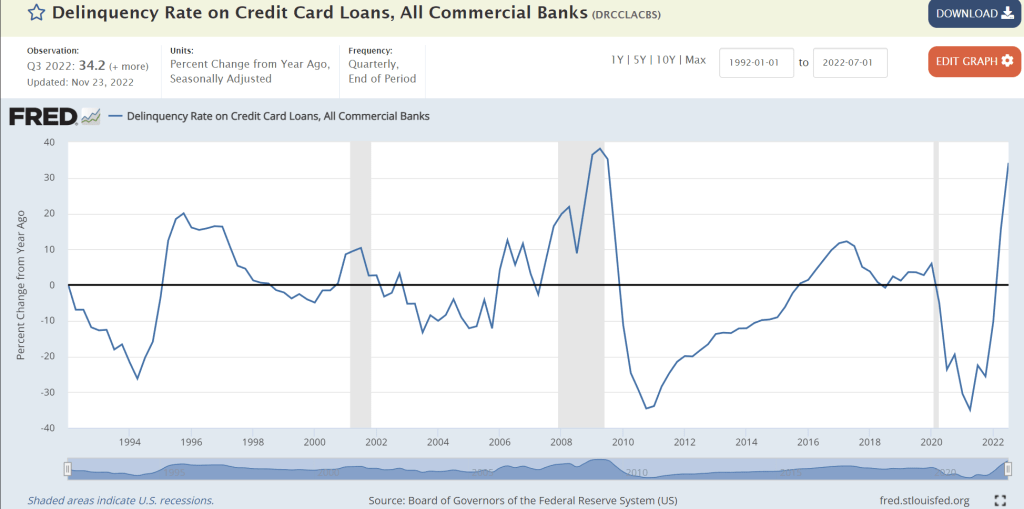

On the personal finance side of the ledger, the delinqueny rate on credit cards is growing at the faster rate since 2010.

Throw in 22 straight months of negative REAL wage growth, and have a scary situation facing middle America.

And the shate of outstanding subprime auto debt (30 days or more delinquent) is up to the highest rate since … well, you know when. The financial crisis of 2009-2010.

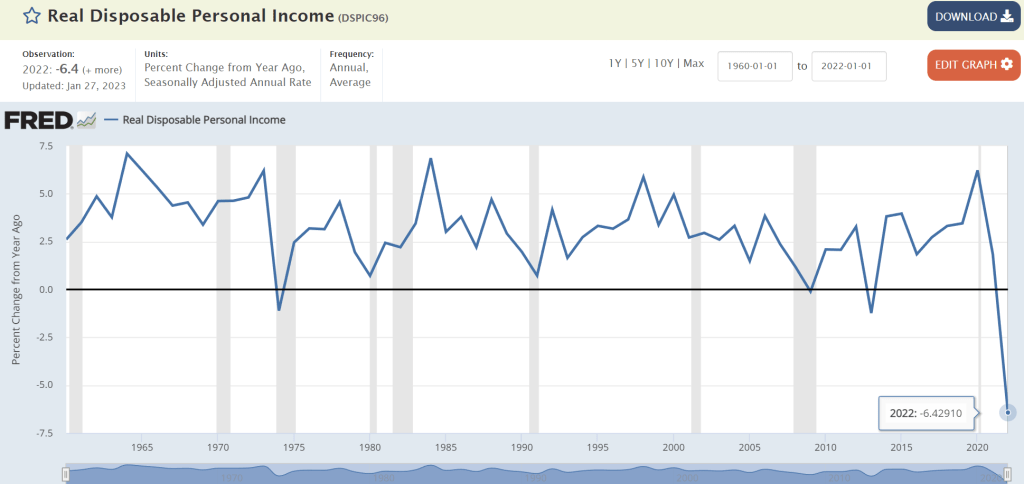

President Biden touts his economic plan as being a great success. But the data says otherwise. Real Disposable Personal Income, for examplge, was down -6.4% year-over-year (YoY) in 2022. That is the WORST reading since The Great Depression.

And to cope with inflation, Americans have expanded their credit useage, but credit card delinquencies are through the roof.

So much for “Middle Class Joe” and The Forgotten Man. Biden hasn’t forgotten, he just doesn’t care.

President Biden loves to demonize his opponents like Republicans over spending and the Federal budget. Biden argued that his budget won’t increase taxes on Americans making less than $400,000 a year and will ultimately cut the deficit by $2 trillion over the next decade. The president has yet to release his budget plan but has promised to do so by March 9.

Of course, Biden ignores “the inflation tax” which is crippling American households (negative REAL hourly earnings growth for 22 straight months). And while he won’t raise taxes on Americans making less than $400,000 (he doesn’t have the authority), he loves to spend money like most of Congress. Without tax increases, The Federal Government will have to issue MORE debt and run budget deficits in perpetuity.

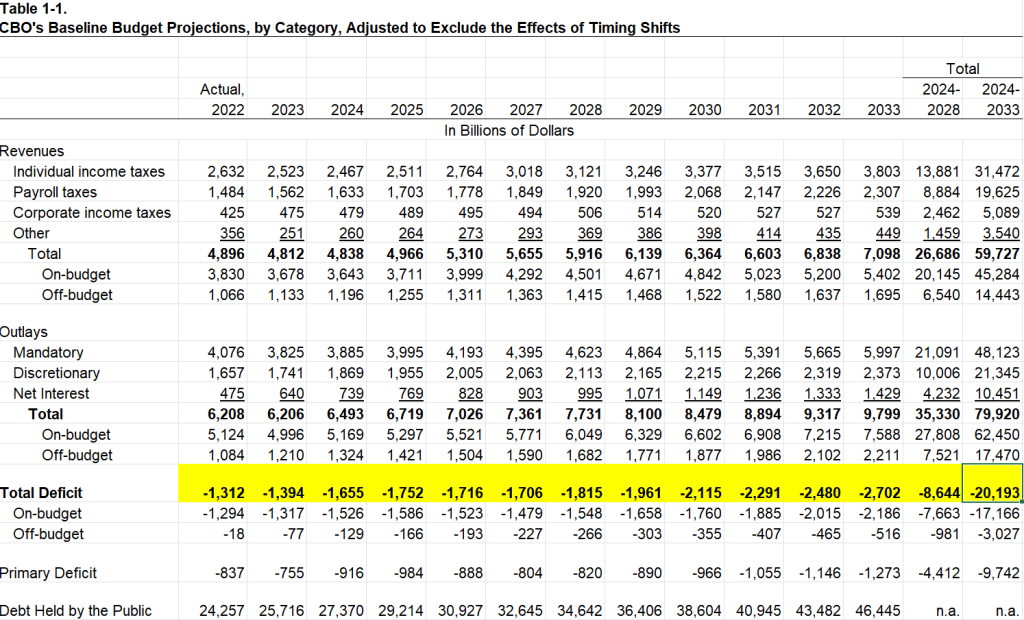

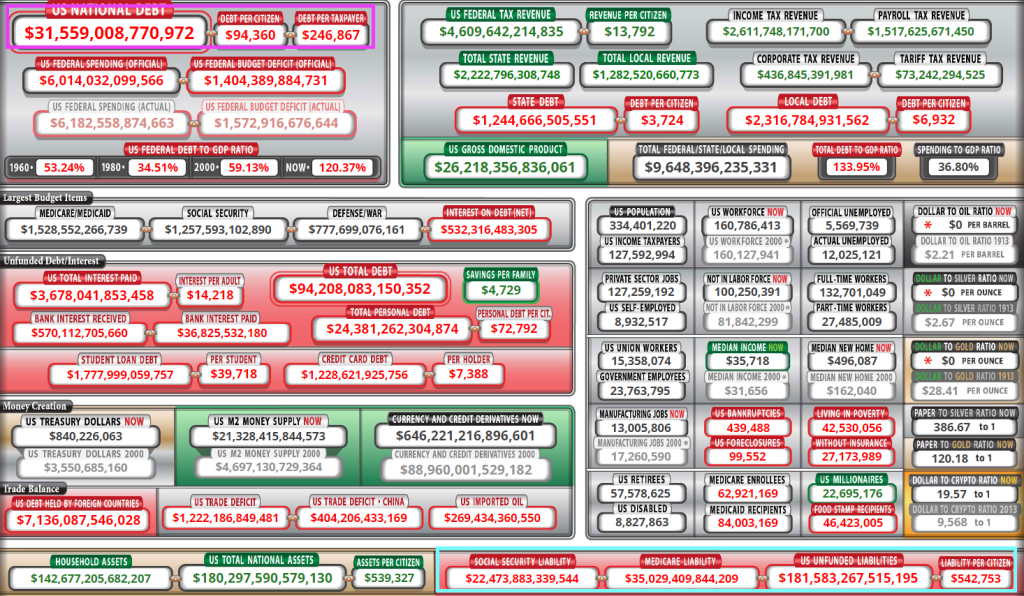

Here is the sickening forecast of Federal budget deficits. Budget deficits are forecast to keep rising and are project to hit -$20 TRILLION over the next 10 years.

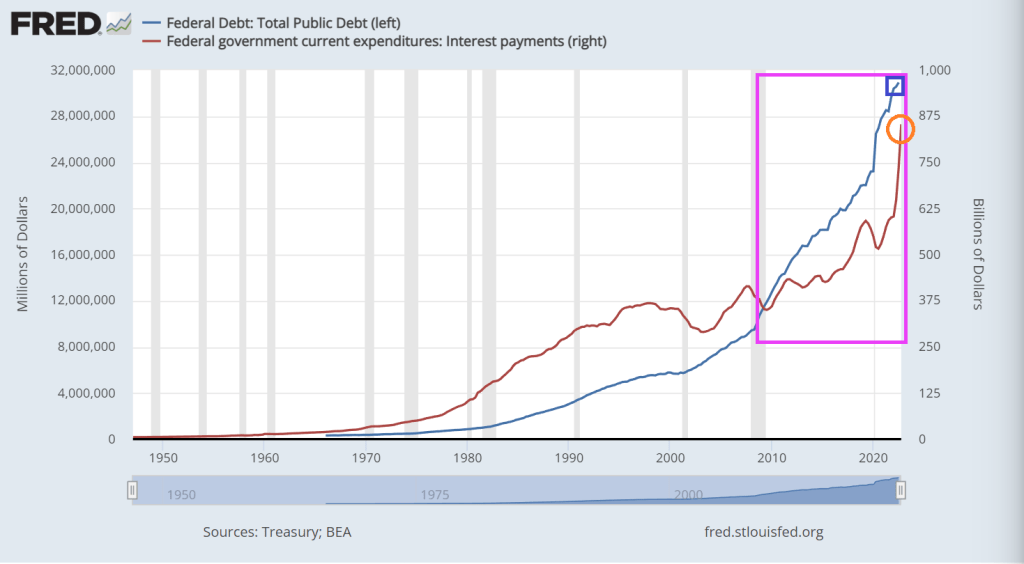

The US is already experiencing irresponsible growth in Federal debt and interest payments on the Federal debt.

Interest costs will nearly triple in the next decade. The Federal Reserve has increased interest rates eight times since early 2022 to combat high inflation — which has contributed to the significant increase in the federal government’s cost of borrowing. In CBO’s projections, such costs would rise from $475 billion in 2022 to $1.4 trillion in 2033. Over the upcoming decade, CBO projects that net interest payments will total $10.5 trillion; relative to the size of the economy, net interest would grow from 2.4 percent this year to 3.6 percent in 2033. In 2030, the ratio of interest to GDP would total 3.3 percent, the highest recorded since 1940 (the first year for which such data are reported).

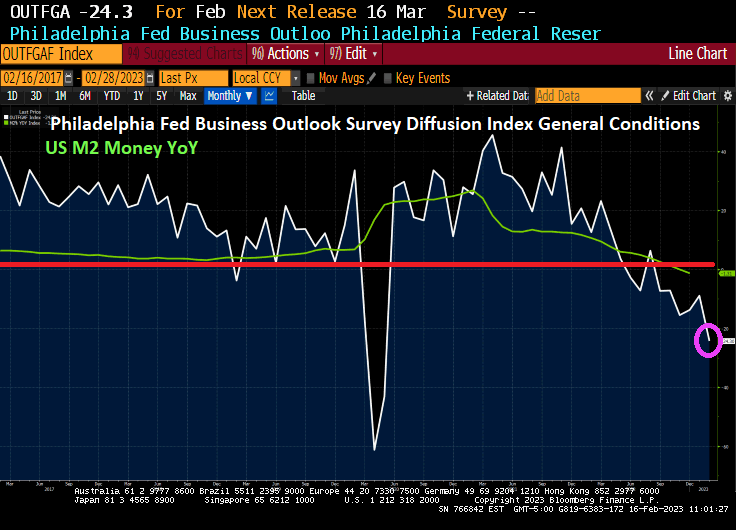

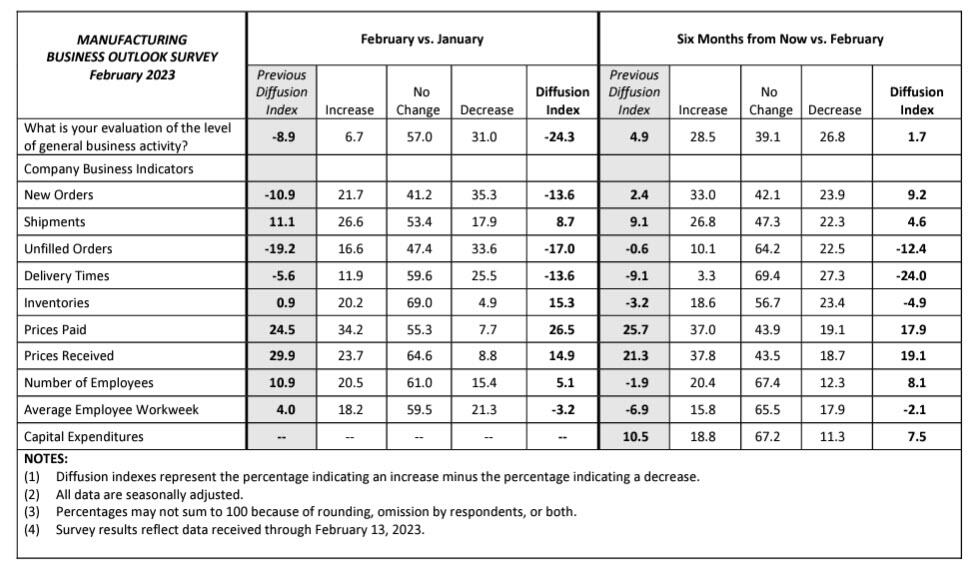

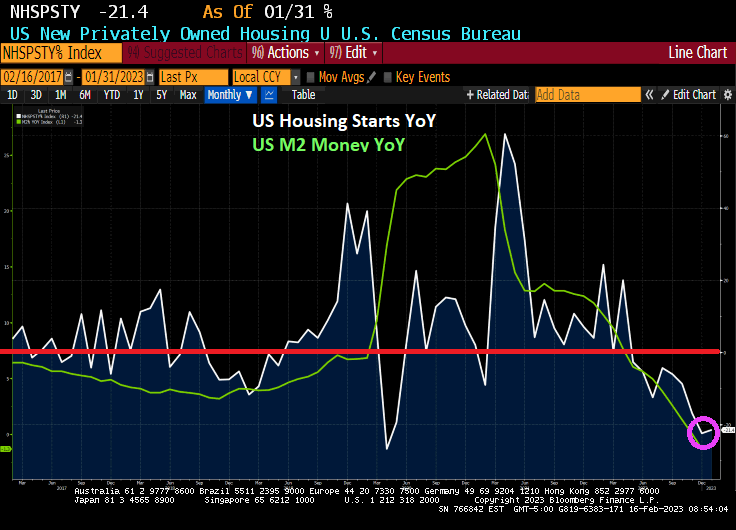

First, US housing starts are now down -21.4% year-over-year (YoY) and down -4.5% month-over-month (MoM) in January 2023 as The Fed removes its massive monetary stimulus.

PPI Final Demand PRICES are still elevated at 6% YoY, so expect more Fed tightening.

Today’s data dump.

On a final note, I am appalled at the Biden Administration’s “response” to the East Palestine Ohio derailment. Where is Mayor Pete, the US Transportation Secretary??

US inflation is causing The Federal Reserve to raise interest rates, and mortgage applications are suffering.

Mortgage applications decreased 7.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 10, 2023.

The Refinance Index decreased 13 percent from the previous week and was 76 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 6 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 43 percent lower than the same week one year ago.

The MBA contract rate rose 3.4% from 6.18% to 6.39% as The Fed tightens.

And if you believe the Taylor Rule (as opposed to The Fed’s current politically-based decisions), The Fed’s target rate should be 10.15% and The Fed is less than half way there at 4.75%.

The Fed is expected (by investors in Fed Funds Futures) to rise to 5.283% by the July FOMC meeting, then decline to under 5% by January ’24.

Speaking of Fed rate hikes, January’s red hot retail sales (up 3% MoM) is surely going to drive inflation UP and The Fed will keep raising rates.

US REAL average hourly earnings fell … again … to -1.8% year-over-year (YoY) from a revised -1.6% YoY in Deember. That makes 22 straight months of negative hourly earning growth.

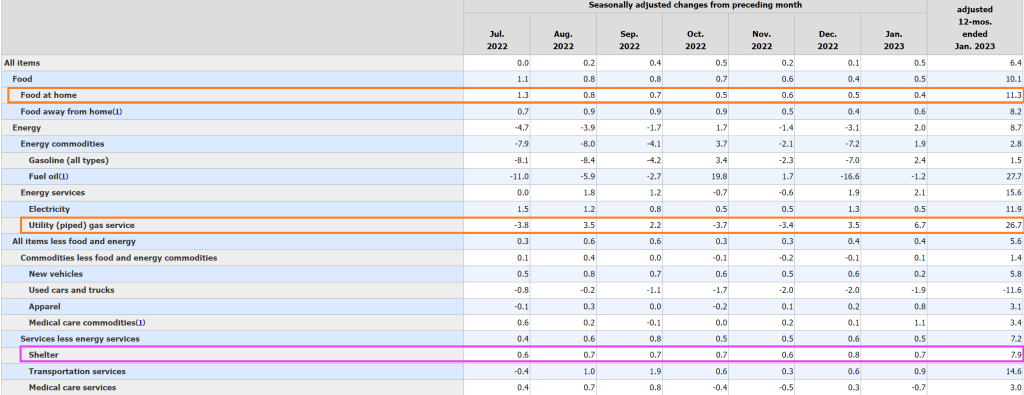

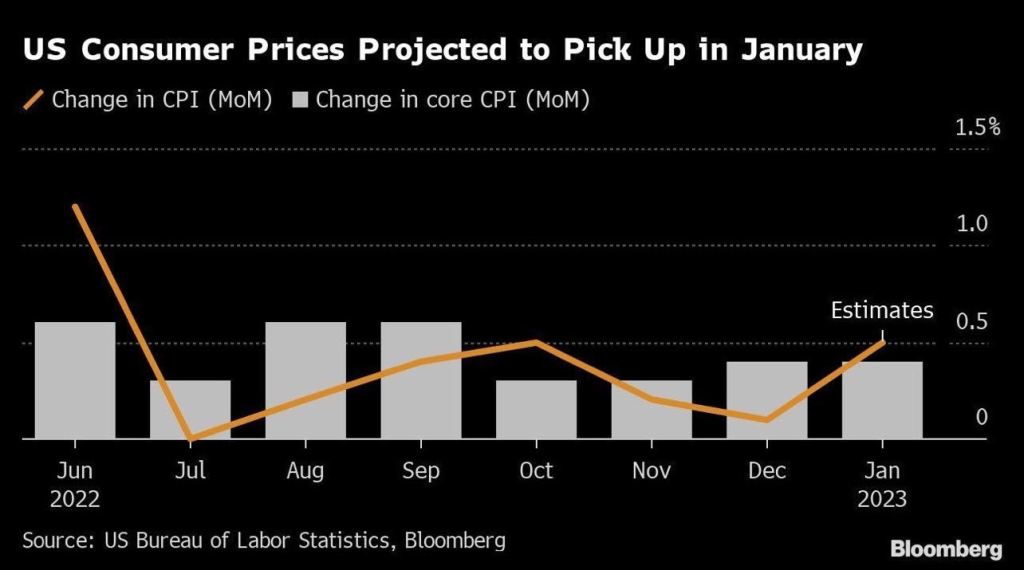

CPI Month-over-month (MoM) was revised upward for December, and increased from 0.1% in December to 0.5% in January. CORE CPI remained unchanged from the upward revision in December to 0.4% MoM.

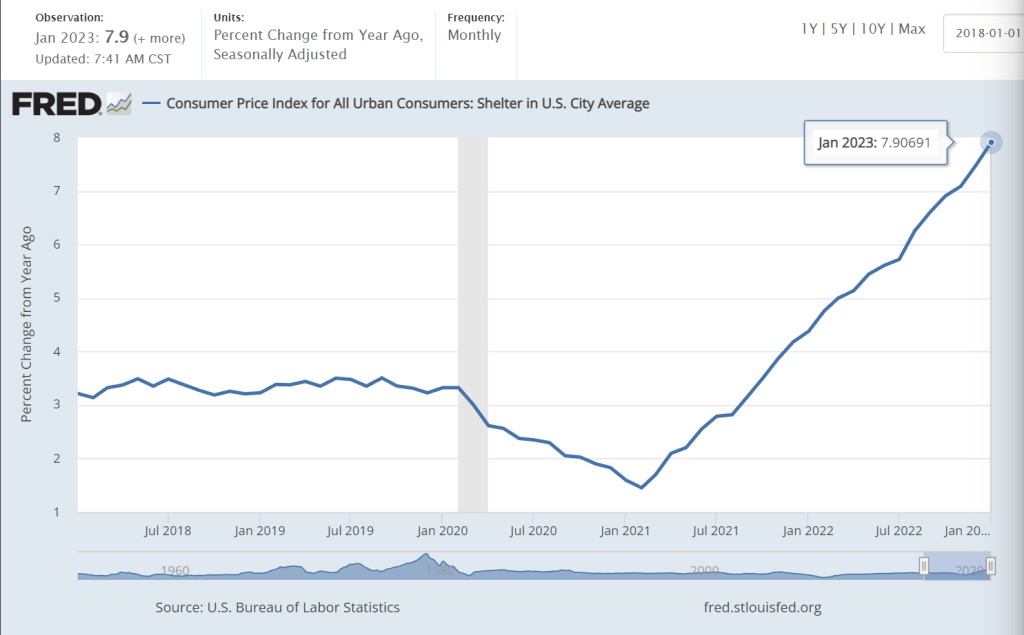

Components of inflation include FOOD AT HOME (up 11.3% YoY), utility (piped) gas service (up 26.7% YoY) and shelter (up 7.9% YoY). So, the middle-class inflation tax (food, heating, housing) remains high.

Do I detect a trend in shelter inflation??

Hey, I thought Treasury Secretary Janet Yellen said inflation was transitory. 22 straight months of negative hourly earnings growth seems more permanent than transitory.

While much of the US is down from 2022 peaks in home price. but it is The West where home prices are down the most (just like 2008 where the Inland Empire of California, Phoenix and Las Vegas crashed in term of home prices).

You must be logged in to post a comment.