Under President Biden’s Reign of Error, inflation is the highest in 40 years. But Powell and The Fed are still overstimulating the economy, and Congress is contributing to the inflation disaster with short-sighted political policies and spending (flooding the economy with stimulus spending helping to drive up prices). Even Democrat US Senator Elizabeth Warren gets it.

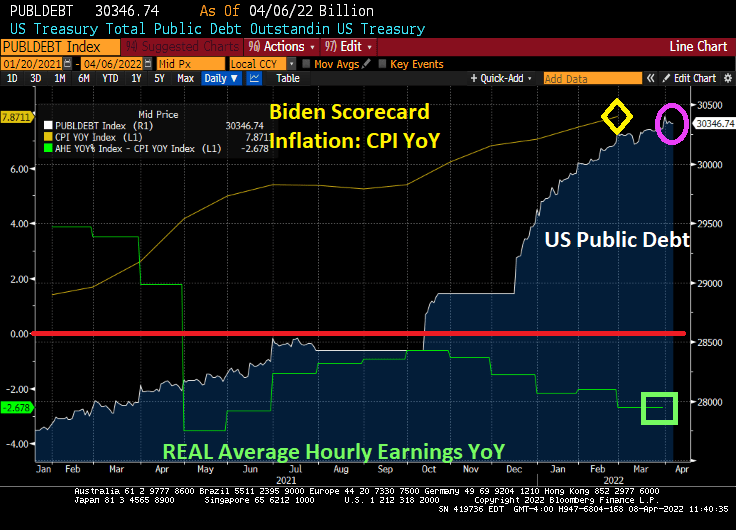

Here is Biden’s inflation scorecard in one chart. Under Inflation Joe, foodstuffs are up 58%, gasoline is up 72%, diesel fuel is up 154%, and green energy element Lithium is up 645% (no wonder electric car manufacturer Telsa is raising their prices 10%). Of course, The Federal Reserve keeps on expanding its balance sheet, UP 50.3% under Inflation Joe.

House price growth is up 69% and the 30-year mortgage rate is UP 83.3% and currently is at 5.28%. The orange line is the growth path.

Yes, prices have risen even more after Russia Invaded Ukraine on February 24, 2022. But most of the inflation was baked-in prior to the Russian invasion. Sorry Jen Psaki, but you are wrong about inflation being all Putin’s fault.

There is one song that sums up the mortgage banking industry with proposed tightening of Fed monetary stimulypto: T-R-O-U-B-L-E.

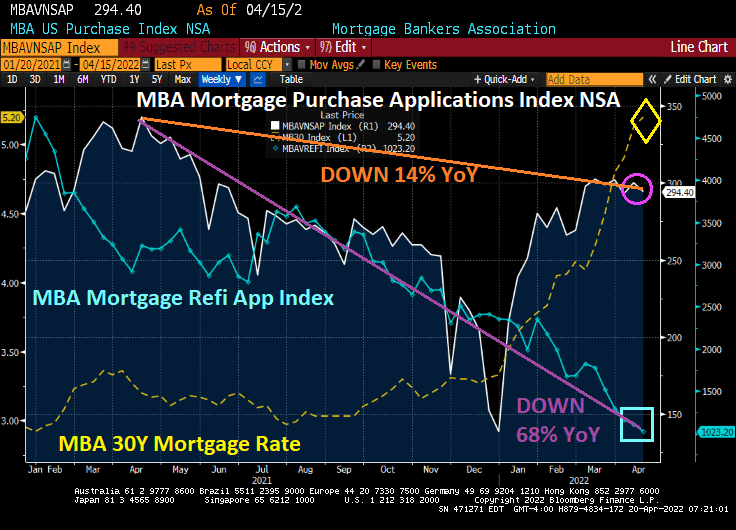

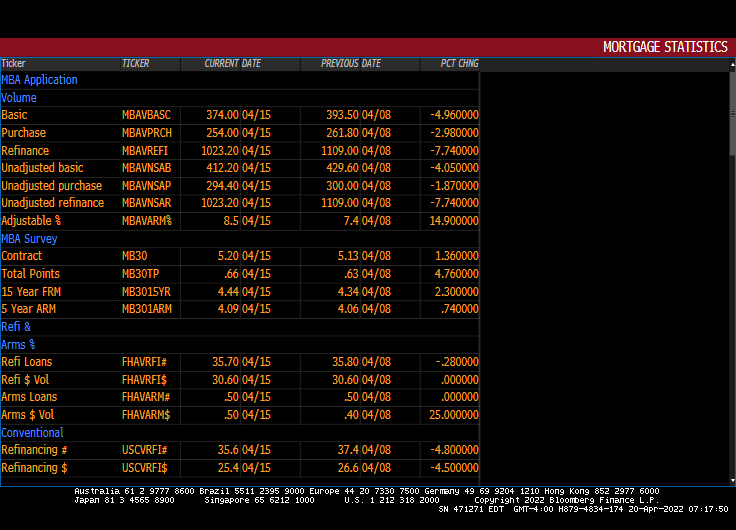

Mortgage applications decreased 5.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 15, 2022.

The Refinance Index decreased 8 percent from the previous week and was 68 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 14 percent lower than the same week one year ago.

All together now, mortgage rates are up 76% under Biden.

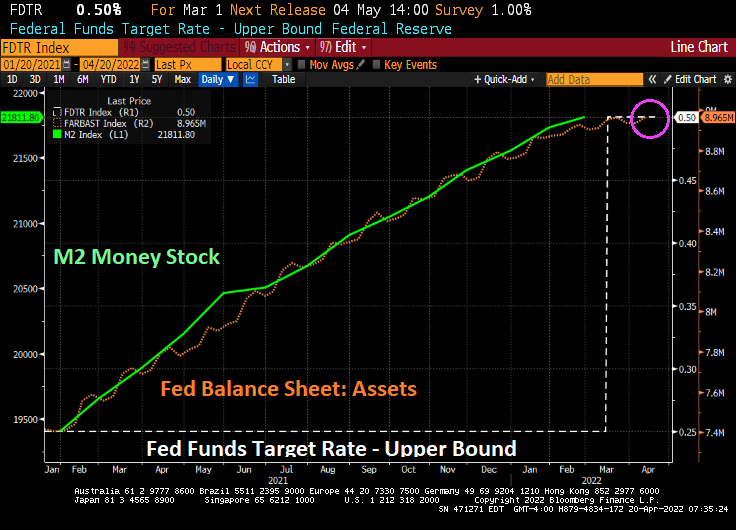

And yes, The Federal Reserve STILL has its enormous foot on the monetary gas pedal (with hints that they will remove it “soon.”

The number of ARMs increased 14.9% from the previous week.

Fortunately, I refinanced my home mortgage while Trump was still President. When Biden was installed as President, the 30-year mortgage rate was 2.88% (according to Bankrate). It has now risen to 5.25%.

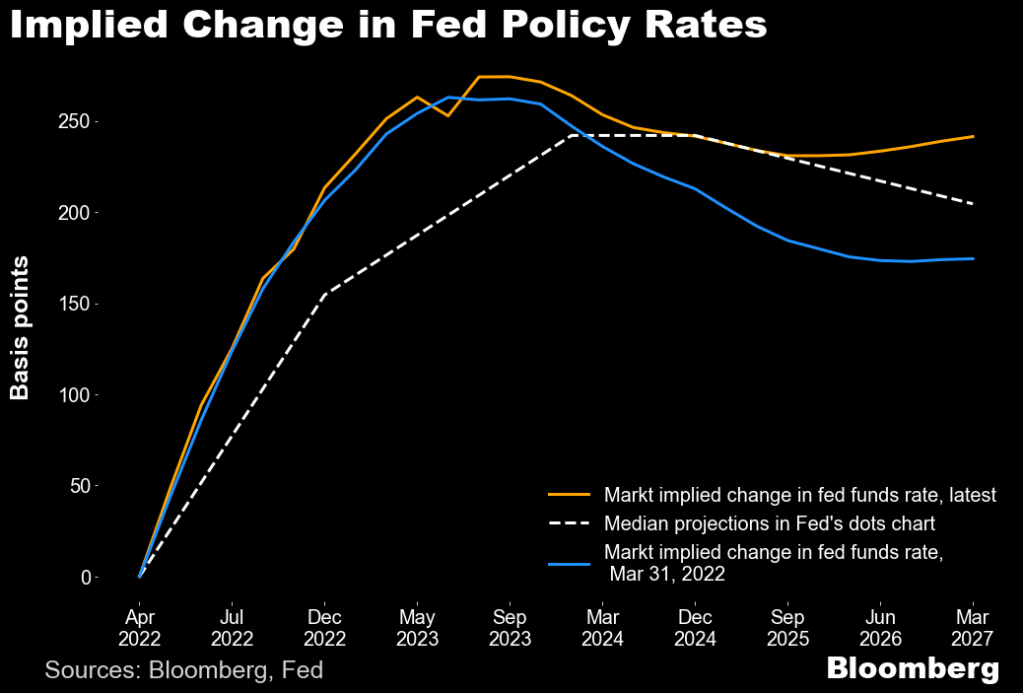

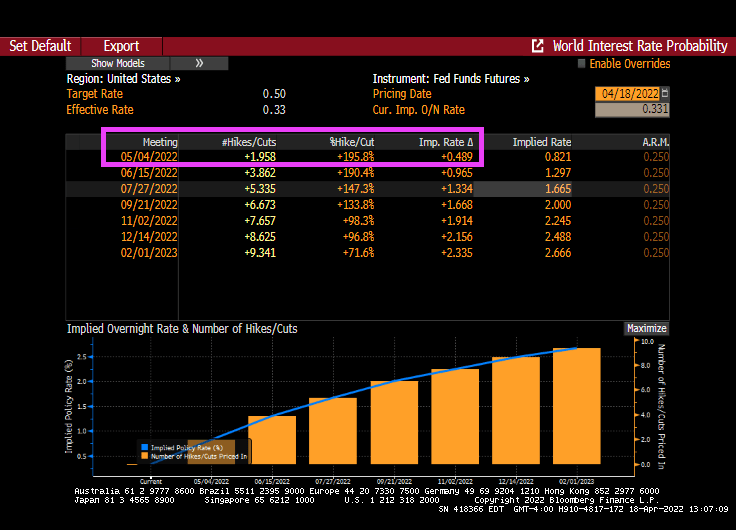

The Federal Reserve is now expected to raise their target rate as much as 50 basis points at the next meeting on May 4, 2022. This chart shows the anticipated rate hikes coming our way, peaking in summer 2023.

Fed Funds Futures are pricing in a 50 bps rise at the May meeting.

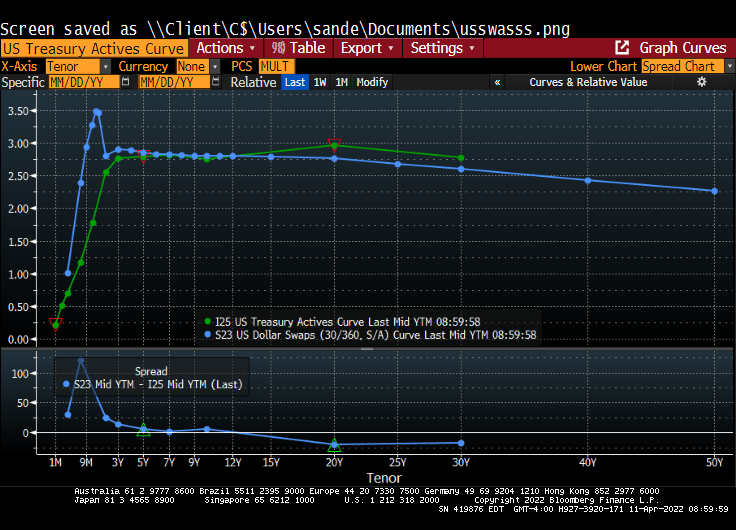

The good news is that the US Treasury actives curve is upward sloping, but is showing fatigue in the forward rates between 7Y and 10Y.

On the hard asset front, precious metals are up over 1% with silver and platinum leading the way.

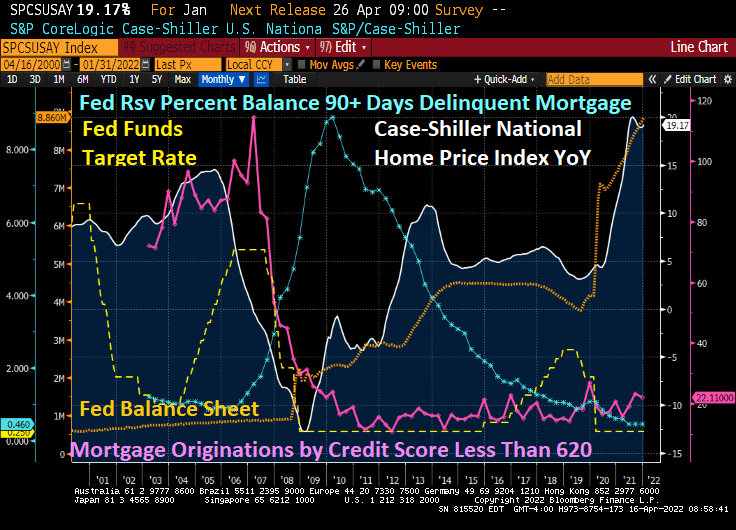

The book and movie “The Big Short” revolved around the 2005-2007 housing bubble driven by lending to borrowers with subprime credit (and little or no underwriting). As we know, Bear Stearns, Lehman Brothers and other investment banks too large positions in subprime asset-backed securities (SABS) that became highly toxic once the demand for high-yield subprime ABS dried up. The decline in US home prices coupled with soaring 90-day mortgage delinquencies led to the failure of Bear Stearns and Lehman Brothers along with Fannie Mae and Freddie Mac being put into conservatorship by their regulator.

Fast forward to today. Mortgage originations by credit scores of 620 or less have shriveled while home price growth YoY is even higher than the subprime mortgage crisis of 2005-2007. So, is the US facing another “Big Short” scenario? Yes and no.

The answer is no in that lenders have tightened their credit box sufficiently so that investment banks are no longer buying large quantities of subprime credit paper. The answer is yes if we consider that the current housing bubble is fueled by extraordinary monetary stimulus due to Covid (as well as rampant Federal government stimulus spending).

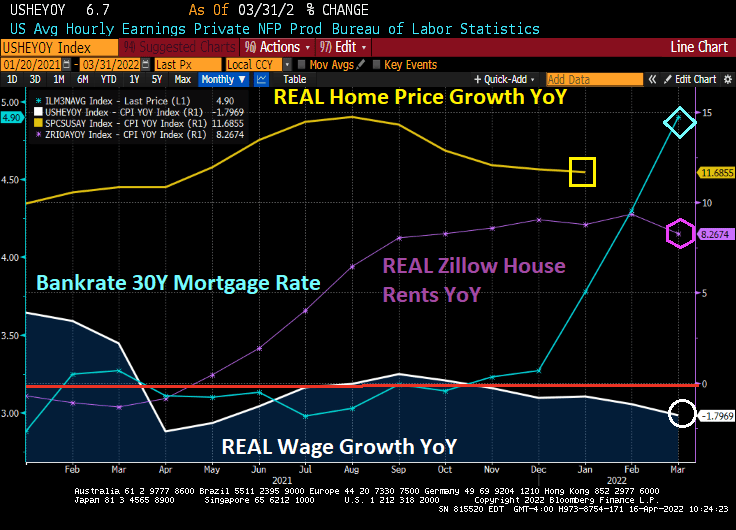

Following the Federal Reserve of Dallas’ lead, here is a chart of REAL home price growth YoY against REAL average hourly earnings YoY. I added REAL Zillow house rents YoY as well.

Look at the affordability gap during the Subprime Bubble of 2004-2006 and then the Fed Bubble of 2020 to today. Both bubbles show a disconnect between REAL home prices and REAL wages. REAL Zillow home rents are not as high as REAL home price growth, but still how a huge gap in rent affordability.

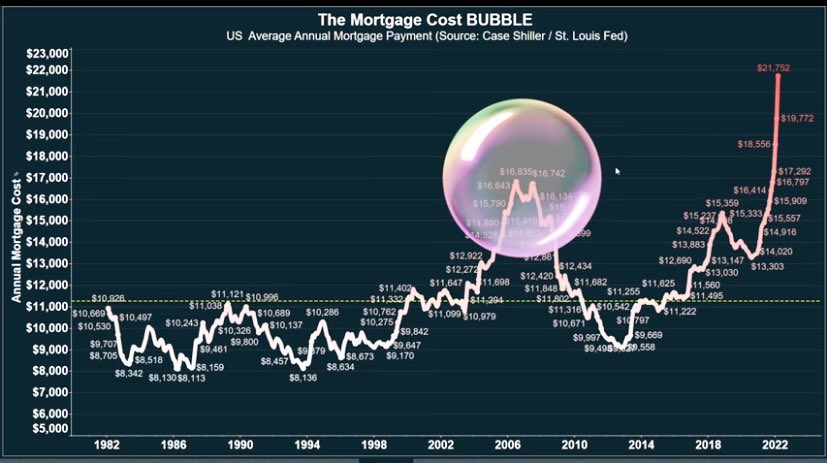

So, what can upset the apple cart? How about Jay and The Gang jacking up mortgage rates making home affordability even worse (unless it slows home price growth).

Thanks to The Fed’s propose quantitative tightening, mortgage rates are soaring and mortgage costs along with them. Mortgage costs, thanks to The Fed driving up housing prices AND mortgage rates, are substantially higher than during the subprime mortgage housing bubble.

The Fed’s whipsaw approach helped crash home prices during the subprime mortgage crisis by dropping rates too fast at first (helping to ignite a housing bubble) then raising rates too fast (helping to crash housing prices).

The good news is that US industrial production rose 0.9% in March. The bad news? US capacity utilization rose to 78.3% indicating that the labor market is overheating.

Notice that prior to Covid, The Fed began rising raising its target rate as capacity utilization was increasing towards 80%. But once The Fed Funds Target rate (upper bound) hit 2.50%, capacity utilization started to cool off. Then Covid stuck.

Since Covid struck and The Fed massively expanded its balance sheet, capacity utilization has increased. But this time around, The Fed has been sloth-like in its removal of monetary stimulus.

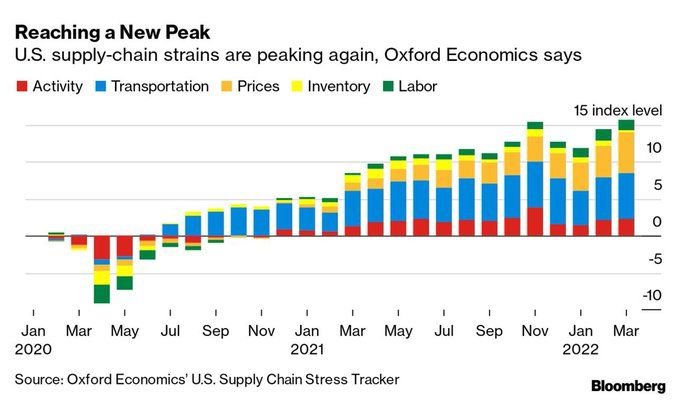

Of course, The Fed has been slow to cool inflation which is the highest in 40 years. And supply-chain strains are peaking again (isn’t Mayor Pete in charge of infrastructure?) This is helping to drive prices up.

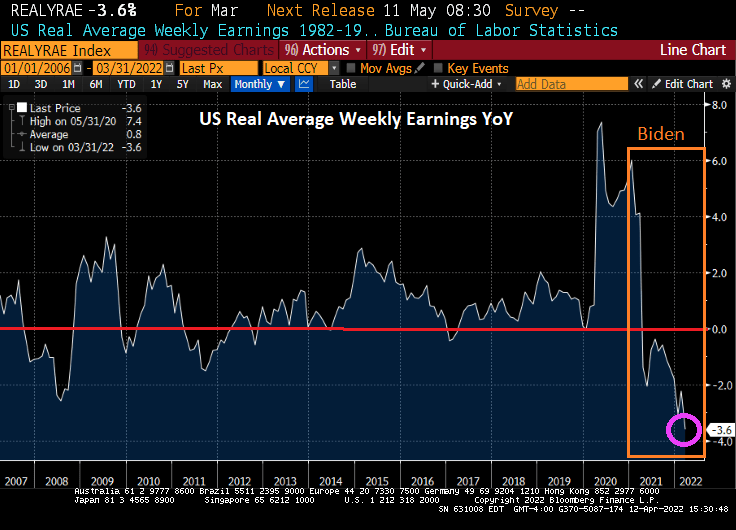

And don’t forget that REAL average weekly earnings YoY are falling.

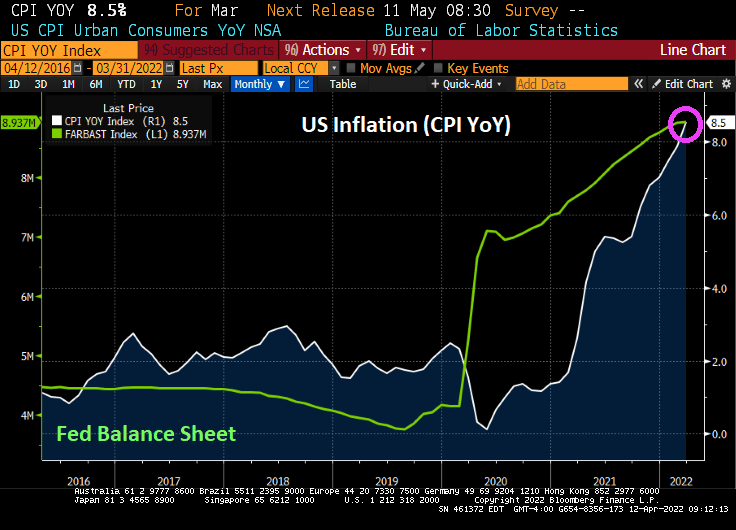

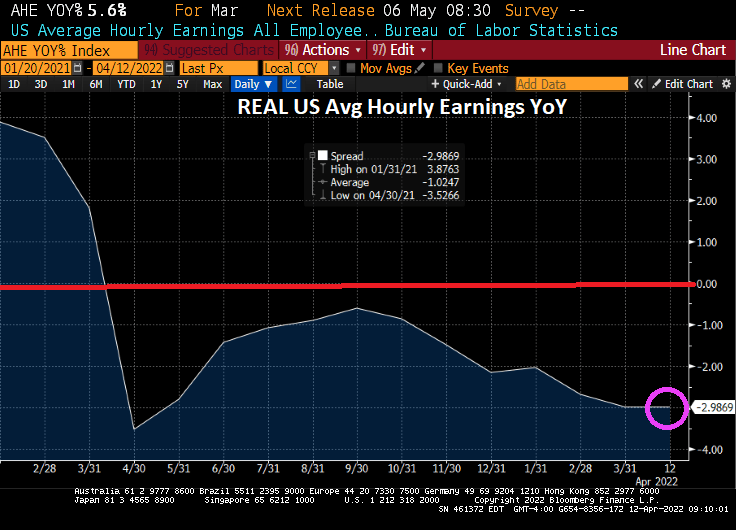

With 8.5% YoY inflation, REAL average hourly earnings growth fell to -3% YoY.

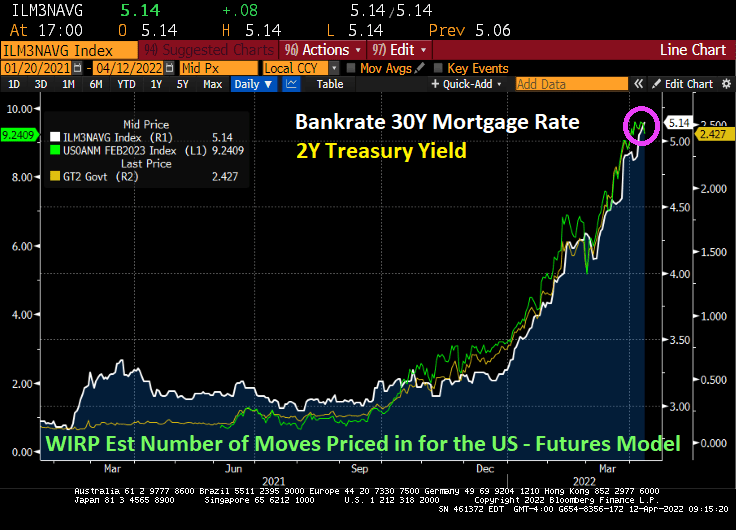

And with The Fed intent on extinguishing their part of the inflation, Bankrate’s 30Y mortgage rate rose to 5.14%.

Energy is the biggest culprit (fuel oil up 70.1% YoY) thanks to the double whammy of 1) Russia’s invasion of Ukraine and 2) Biden’s restrictions on oil and natural gas production. Food at home is up 10% YoY.

Here is a colorful chart of MoM growth in prices.

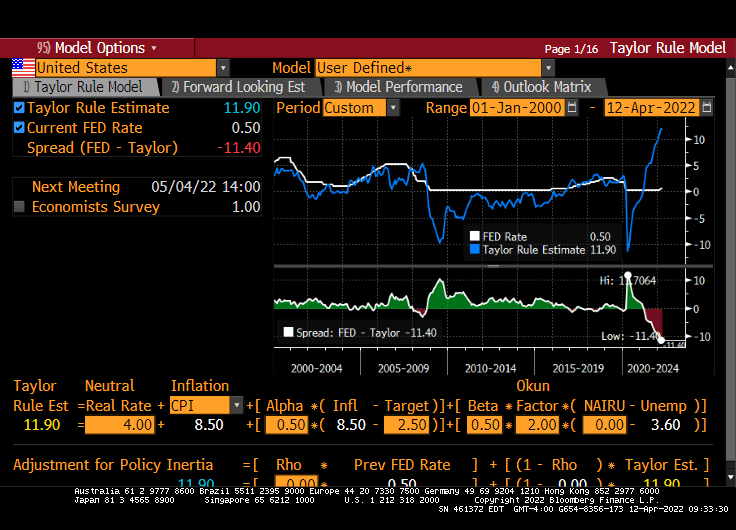

The Taylor Rule model now says that The Fed Funds Target Rate should be 11.90%. Hence, Fed Stimulypto is still in place with the signal that rates will increase.

How about WTI Crude and Brent Crude soaring over 4% today?

Once again, the Four Horsemen of the Inflation Apocalypse (Biden, Powell, Pelosi, Schumer) overstimulated the economy and financial markets with excessive monetary stimulus (Powell) and excessive Federal spending (Biden, Pelosi, Schumer) where demand soared for products and supply naturally hasn’t caught up.

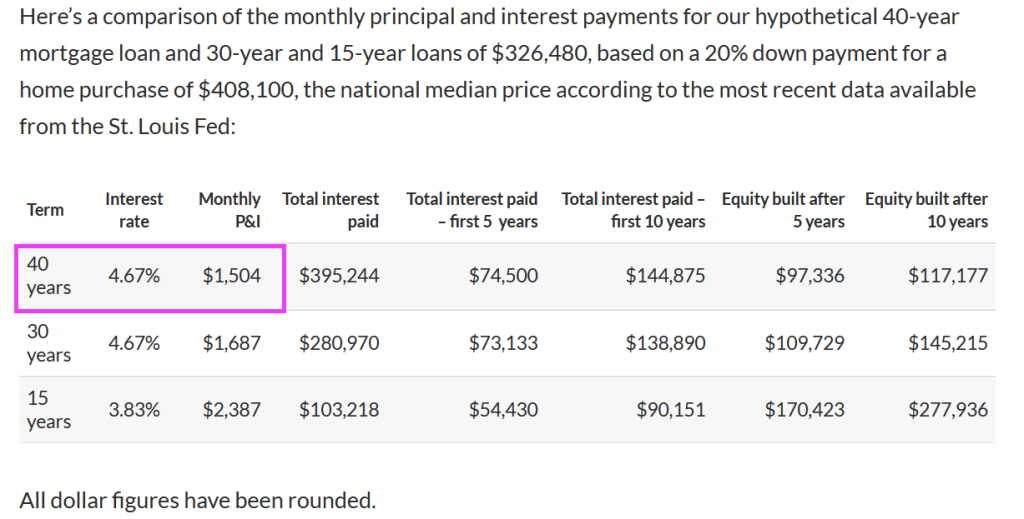

To make a long story short, a 40-year mortgage, by stretching the payment out from 30 to 40 years, means that the mortgage mortgage payment declines from $1,687 to $1,504.

Given that the US Treasury yield curve only goes out to 30 years, lenders (and Fannie Mae and Freddie Mac) will have to use the US Dollar Swaps curve to price mortgages. And since the swaps curve is downward sloping, we could see 50-year mortgages at a lower rate than 30-year mortgages, ceteris paribus.

But with The Fed planning on taking away the monetary punchbowl, mortgage rates are rising making housing even more unaffordable.

But most things are not equal. The 40-year mortgage results in a slower paydown of the mortgage, increasing the lender’s exposure to property value declines. A 50-year mortgage would even be worse.

But the real problem with the 40-year mortgage is that it can lead to even MORE unaffordable housing. Yes, going from 30-year to 40-year mortgages lowers the mortgage payment, but a 40-year mortgage could increase the demand for housing. And since we already have soaring home prices since Covid (thanks to Fed monetary policy AND Federal government stimulus), we could actually see a worsening of the housing bubble). Particularly since REAL average earnings are declining.

What a mess that has been created by the government’s pursuit of “affordable housing.” Ideally, the Federal government could help raise household earnings through lowering of Federal tax rates, but the Biden Administration wants to raise taxes. Alternatively, lenders (and Fannie Mae and Freddie Mac) could lower lending standards (e.g., lowering required credit scores), or reduce downpayments to 0%. Lowering credit standards and reducing required downpayments are also inflationary and pose serious potential problems with default risk.

Not to mention that a 40-year mortgage increases the duration risk for owner’s of the 40-year mortgage.

And don’t forget that local governments frown on multifamily (apartment) construction (the Not In My Backyard [NIMBY] problem contributing to rising housing prices.

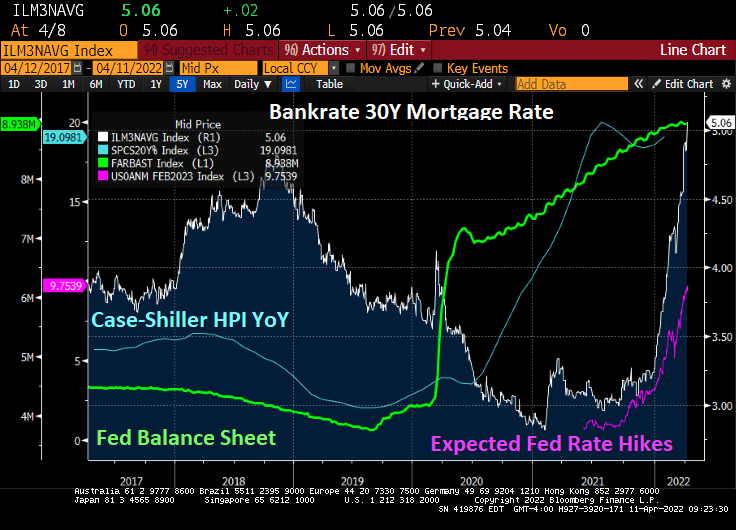

As the US Treasury 2-year yield hits 2.507% (up from 0.128% when Biden was installed as President) and the number of Fed rate hikes over by February 2023 hits 9.6, Bankrate’s 30-year mortgage rate breached the 5% mark at 5.04%.

The most recent data from on existing home sales show YoY sales in negative territory as The Fed begins in monetary fireball tightening.

St Louis Fed’s Bullard said The Fed is “behind the curve.” Ya think??

The Fed’s minutes from the most recent meeting indicates that The Fed will shedding $95 billion a month from it swollen balance sheet. At almost $9 trillion mostly populated by Treasuries will be the first asset to run-off the balance sheet (there is almost $1 trillion of Treasuries maturing in 2022 and $856 billion maturity in 2023, etc), The Fed plans to shrink the balance sheet while, at the same, raising The Fed Funds target rate from it near zero levels.

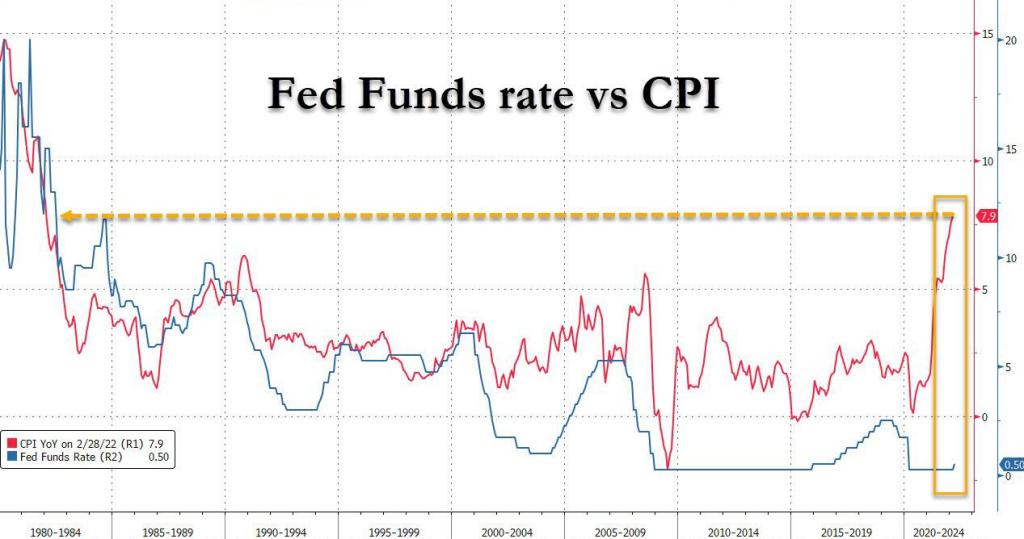

The Federal Reserve has ignoring rules like the Taylor Rule since the financial crisis of 2008-2009, but seemingly are paying attention to the Taylor Rule because of 7.9% inflation. The Taylor Rule is suggesting a 20.42% Fed Funds target while the current target rate is 0.50%. Now THAT would be a real shock to the economy.

Its official! I submitted my resignation from George Mason University effective June 1, 2022. I will miss teaching the students, past and present.

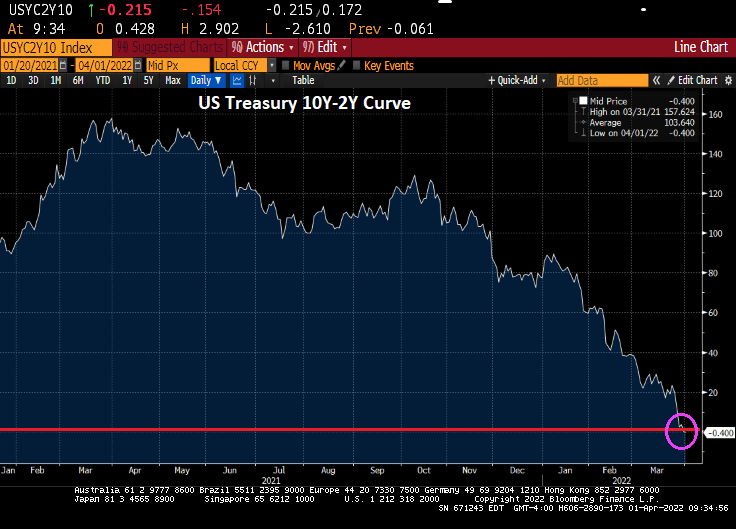

But back to the US Treasury yield curve. It remains in reversion (meaning shorter-term Treasuries have higher yields than longer-term Treasuries, usually a sign of impending recession. The Fed has actually started quantitative tightening (QT) and the growth rate of Treasury note and bond purchases has slowed to a crawl.

Meanwhile, Bankrate’s 30-year mortgage rate rose slightly to 4.91%.

Meanwhile, President Joe “The Big Guy” Biden has ordered carmakers to increase their average fuel economy to about 49 miles (78.8 kilometers) per gallon by 2026. Of course, this is intended to kill-off gasoline-powered autos and make all cars electric or hybrid like the Toyota Prius.

This can be the Democrat’s midterm election slogan: “Making living in the USA unaffordable!”

The middle-class unaffordable Ford F-150 Lightning at nearly $100,000. Thanks Joe!

Alternatively, you can buy a Buick Envision (made only in Shanghai China) with up to 24 city / 31 highway MPG. Well, kiss that baby goodbye under Biden’s new MPG mandate.

Wasting away again in Biden/Pelosiville, looking for my lost inexpensive gasoline and food. Some people say that Putin is to blame, but we know its Biden/Pelosi’s fault.

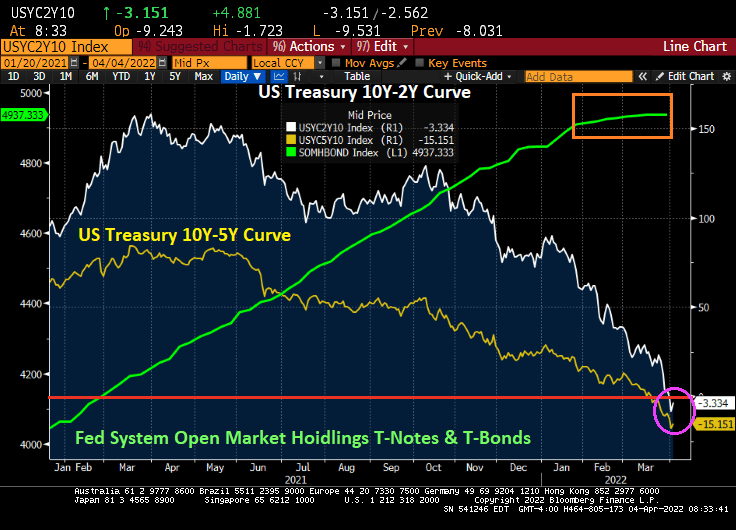

The US Treasury 10Y-2Y yield curve just inverted, generally a precursor to a recession. Called it, nothing but net!

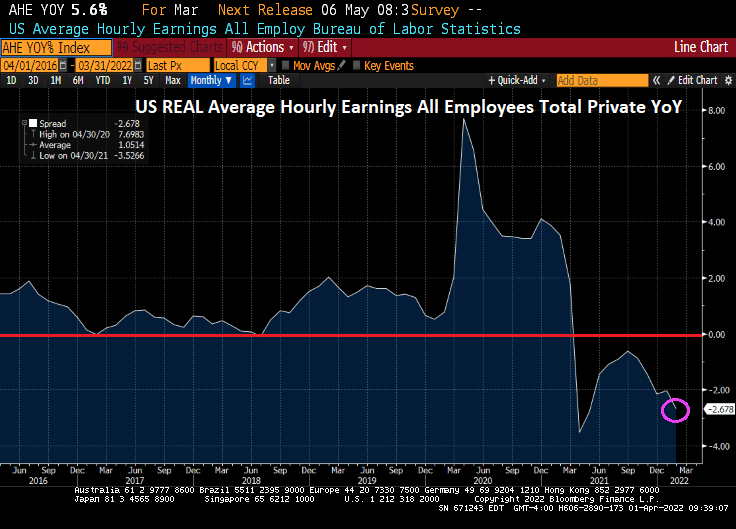

Meanwhile, today’s jobs report shows that Bidenflation is crushing America’s wage growth. While average hourly earnings grew to 5.6% YoY, we are still seeing inflation growing at 7.9% YoY meaning that inflation is reeling hurting the middle class and lower-income households.

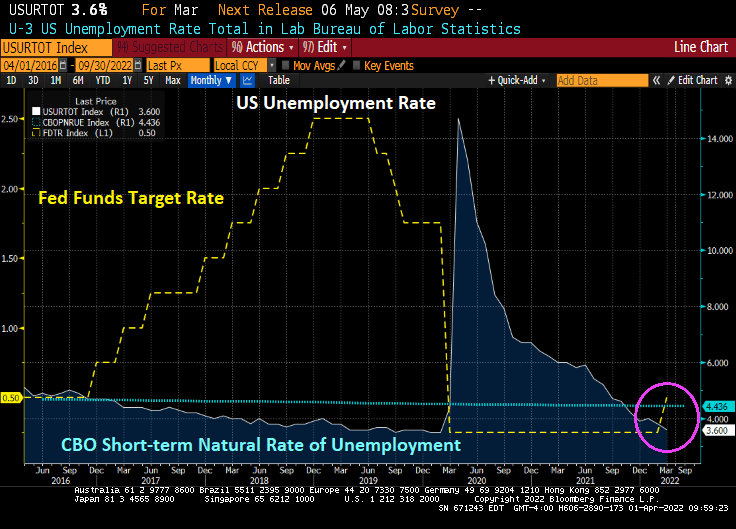

The good news is that the U-3 unemployment rate fell to 3.6%, almost back to the Trump-era unemployment rate of 3.5% prior to the Covid outbreak. And the unemployment rate remains below the CBO’s short-term natural rate of unemployment indicating that the labor market is OVERHEATED.

Today’s jobs report was pretty good, as we would expect from a recovery caused by governments shutting down economies, then reopening them. 431k jobs were added, but less than last month’s jobs added of 678k and less than the forecast 490k.

The number of people NOT in the labor force fell slightly, but it still around 100 million. The number of people holding multiple jobs to overcome Bidenflation rose to 7.5 million.

On the mortgage front, Bankrate’s 30-year mortgage rate rose to 4.90% as the 2-year Treasury rate (yellow) rises and the number of expected Fed rate hikes over the coming year is 9.26%.

You must be logged in to post a comment.