Falling mortgage rates are having a predictible effect on mortgage refinancing applications, but not so much for mortgage purchase applications.

Mortgage applications increased 7.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 20, 2023. This week’s results include an adjustment for the observance of Martin Luther King, Jr. Day.

The Refinance Index increased 3.15 percent from the previous week and was 77 percent lower than the same week one year ago. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 39 percent lower than the same week one year ago.

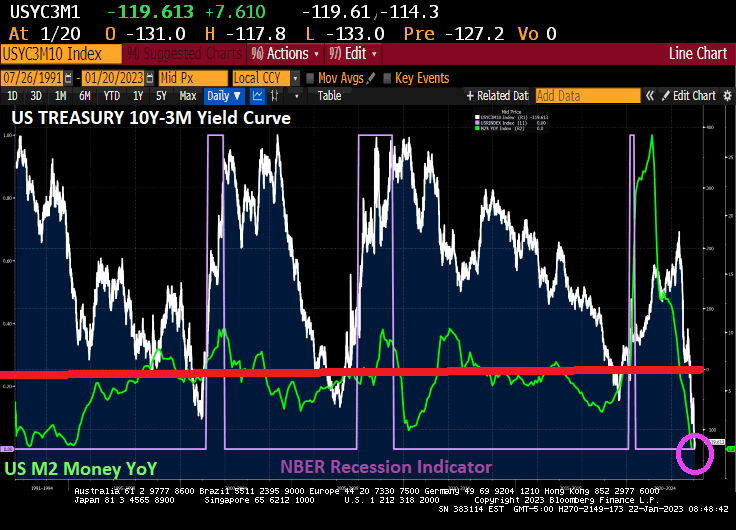

Generally speaking, declining mortgage rates are due to declining 10-year Treasury yields. And 10-year Treasury yields decline as the economy weakens. Of course, M2 Money growth YoY is now 0% as The Fed tightens.

On a humerous note, US Treasury Secretary Janet “The Evil Gnome” Yellen is visiting Africa and lecturing them on prudcnt sovereigh debt management. Seriously. China responded with “Fix the US debt problems before you lecture anyone else.”

You must be logged in to post a comment.