You can always count on government to make things more expensive when they claim they want to help make things more affordable.

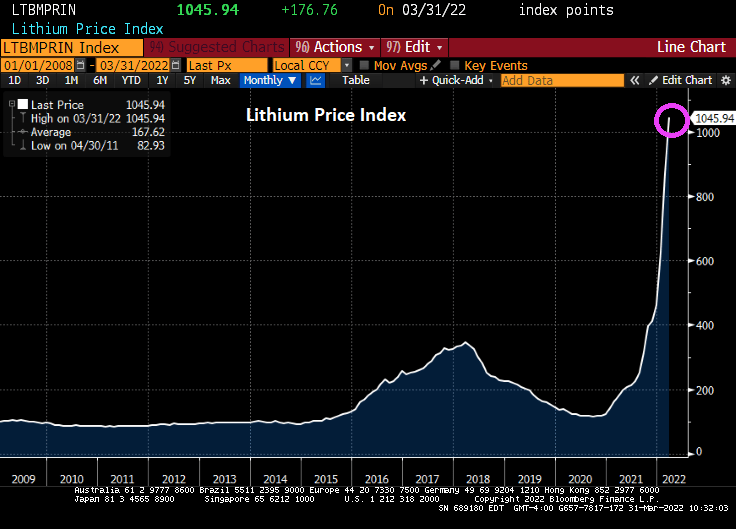

For example, President Biden and his green commandos are helping drive critical electric battery component LITHIUM through the roof!

Lithium hydroxide futures prices are through the roof making already expensive electric cars even MORE expensive. So much for making electric cars affordable!

Of course, The Federal government will now have to subsidize GM and Ford and increase Federal tax credits to encourage consumers to purchase outrageously expensive electric cars.

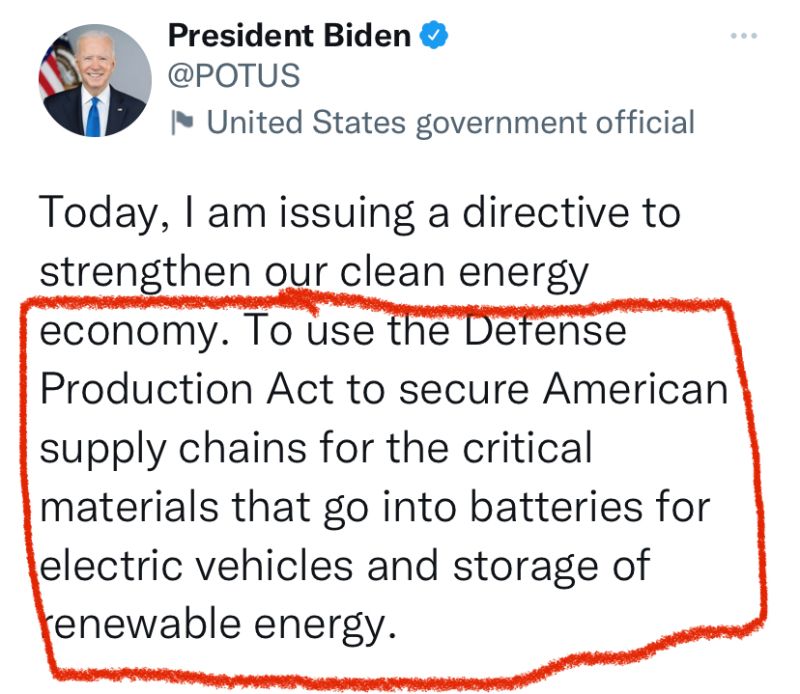

Thanks Joe for issuing your enactment of the Defense Production Act, helping to drive prices insane.

In fairness to Biden and his green commandos like AOC and Bernie Sanders (no relation to me), other nations are going electric car crazy, bidding for a scare resource like lithium. Particularly when there is an abundance of oil in the ground.

I wonder how about members of Congress and the Biden Administration bought lithium ahead of Biden declaring the Defense Production Act to encourage electric car battery production?

You must be logged in to post a comment.