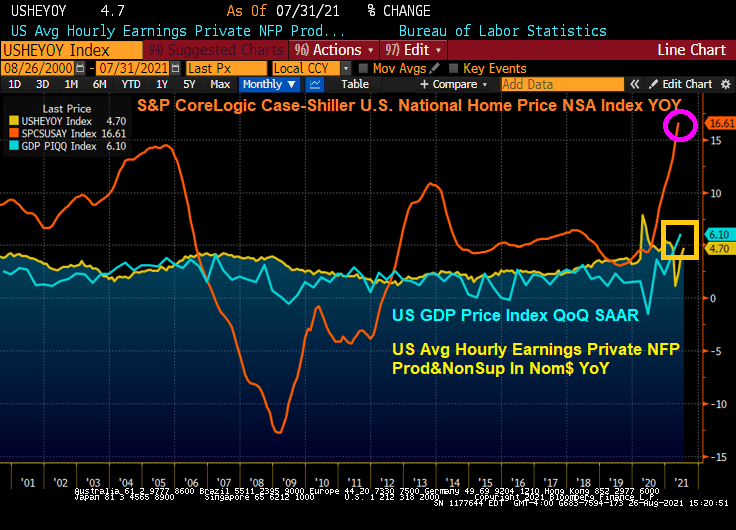

Looks an awful lot like 2005 before the housing price crash, financial crisis and Great Recession. US home prices, HOUSING inflation, is growing at 16.61% YoY, GDP Price index QoQ (annualized) is growing at 6.10%, and average hourly earnings is growing at 4.20% YoY.

Let’s see what happens in Jackson Hole this weekend!

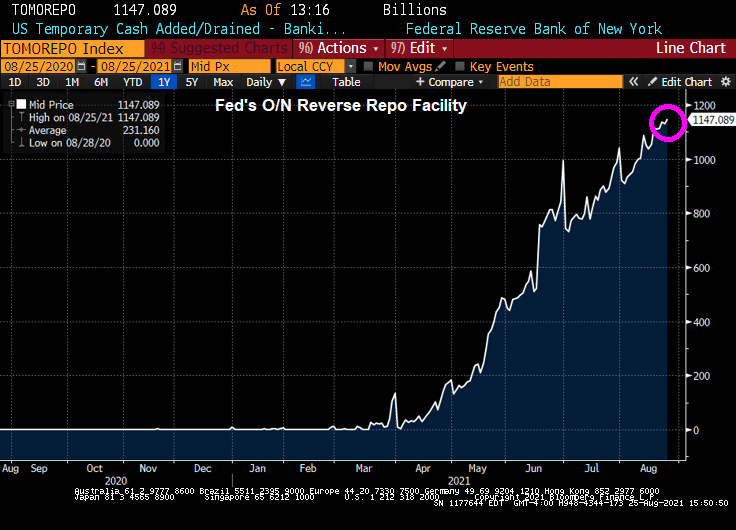

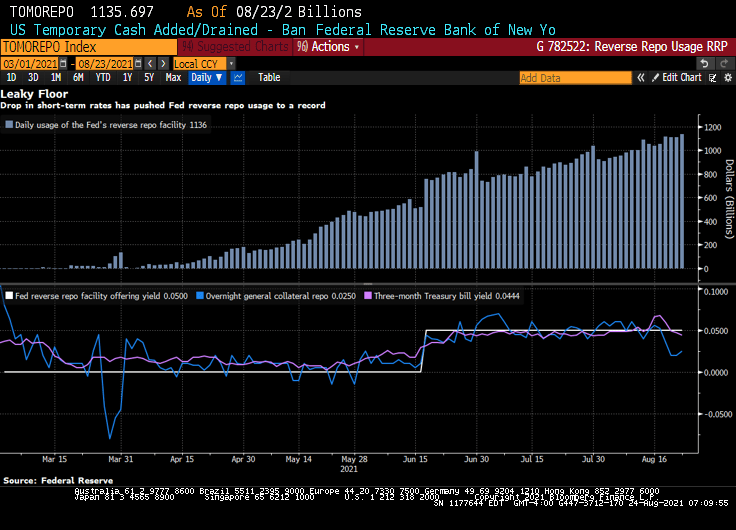

(Bloomberg) — Usage at the Federal Reserve’s facility for overnight reverse repurchase agreements Wednesday rose to a new all-time high.

Seventy-seven participants took $1.147 trillion, which exceeded Tuesday’s volume of $1.13 trillion, and the previous record of $1.136 trillion reached on Aug. 23.

The facility pays an overnight rate of 0.05%, helping to temporarily reduce the quantity of reserve balances in the banking system.

Nothing has been the same since late 2008 and shock troops from The Federal Reserve and their seemingly never-ending monetary stimulus.

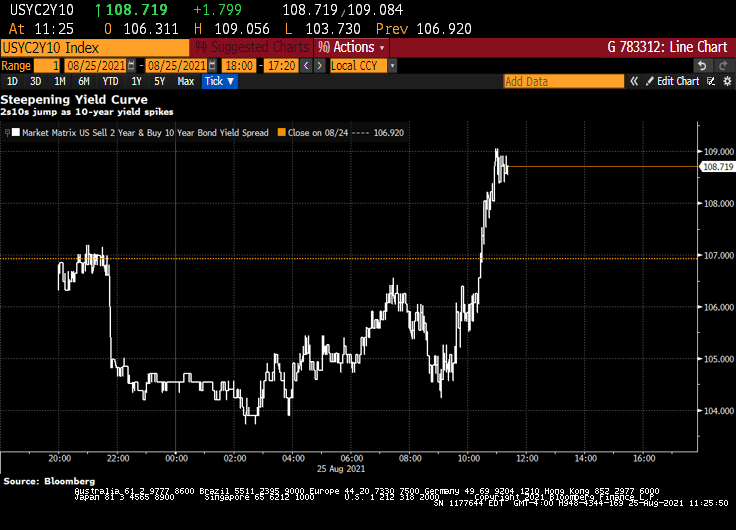

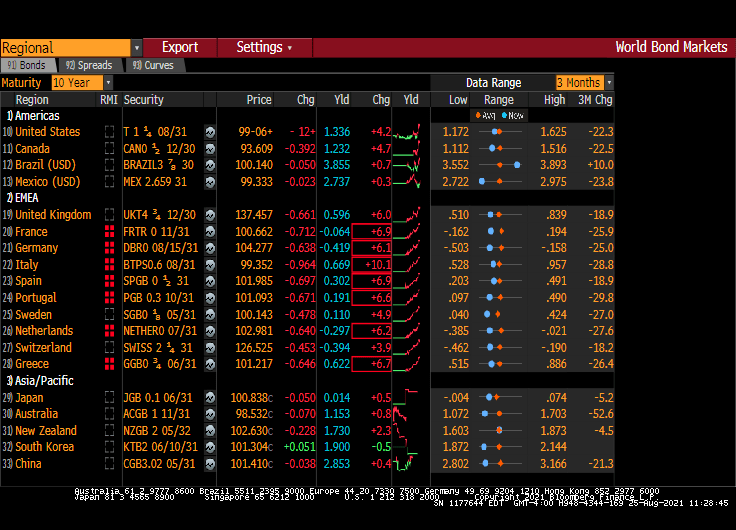

U.S. 10-year yields are spiking upwards in what was supposed to be a sleepy day before the Fed’s Jackson Hole conference. The 2s10s curve is the steepest in two weeks. Eurodollar yields too have risen sharply and are up 6-7 bps in the blue and gold packs.

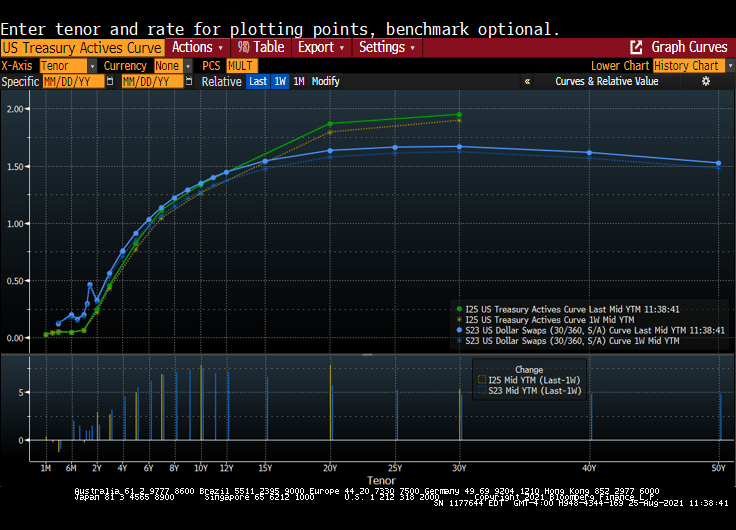

Over the last week, we have seen a steepening in the US Treasury Actives curve and the US Dollar Swaps curve.

This may be linked to the range breach in German 10-years and Italian 10-years. In fact, France, Spain, Portugal, Netherlands and Greece has all seen 6 bps leaps in 10-year sovereign yields today.

Does this mean that Chairman Mao Powell is likely to announce the paring-back of Fed monetary stimulus at J-Hole?

Mortgage applications increased 1.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 20, 2021.

The Refinance Index increased 1 percent from the previous week and was 3 percent higher than the same week one year ago. You can clearly see the Refi Wave associated with the Covid outbreak and sudden Fed monetary stimulus resulting in a lowering of 30-year mortgage rates.

The seasonally adjusted Purchase Index increased 3 percent from one week earlier. Notice the general slowdown in purchase applications with soaring home prices.

The unadjusted Purchase Index increased 1 percent compared with the previous week and was 16 percent lower than the same week one year ago.

Powell and The Fed’s policies have veered from their mandate requiring Chairman Powell to meet 350 times with Congress to sell The Fed’s policies.

Bloomberg) — The Federal Reserve’s floor for overnight funding markets is proving to be no match for the deluge of cash.

Money-market securities ranging from Treasury bills to repurchase agreements continue to trade below 0.05% — the offering rate on the overnight reverse repo facility, which is supposed to act like a floor for the front end. The Fed at its June meeting had raised the rate by five basis points to help support the smooth functioning of short-term funding markets.

Still, usage of the tool climbed to a record $1.136 trillion on Monday, eclipsing the previous high of $1.116 trillion on Aug. 18.

Demand for the so-called RRP facility has surged as a flood of dollars threatens to overwhelm funding markets. That’s in part a result of the central bank’s long-standing asset purchases and drawdowns of the Treasury’s cash account, which is pushing reserves into the system. As a result, liquidity has been swelling, especially as the Treasury cuts supply to create more borrowing room under the debt ceiling.

The pressure pushing down overnight rates toward zero is proving a major headache for money-market funds. It hampers their ability to invest profitably, and can lead to further disruptions as they begin to waive fees to avoid passing on negative rates to shareholders. A number of firms including Vanguard Group shut down prime money-market funds last year after struggling to cover operating costs in the low-interest-rate environment.

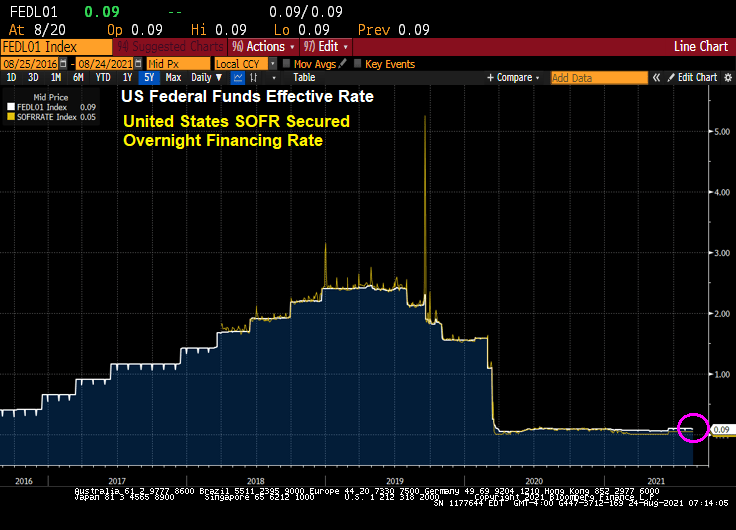

Yes, overnight rates such as the US SOFR rate, are near zero.

Powell’s Charm Offensive in Congress Positions Him to Keep Job

Perhaps that is why Federal Reserve Chair Jerome Powell is acting as a lobbyist with Congress for The Fed’s nontraditional approach to monetary policy.

(Bloomberg) Since he took the helm of the Fed in February 2018, through June of this year, he’s held at least 350 meetings, dinners or phone calls with members of Congress, according to his monthly calendars. That’s almost nine per month, and many of those included more than one lawmaker. The tally doesn’t count at least 16 appearances as chair before numerous congressional committees.

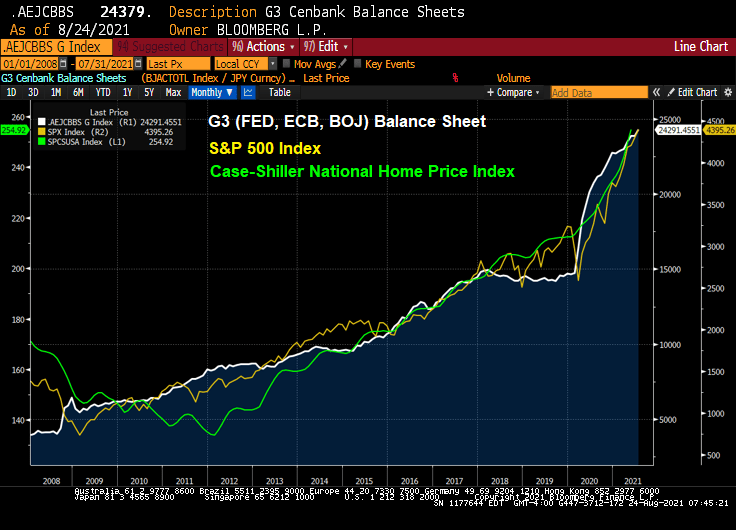

Well, the stock market has zoomed-up since Bernanke and The Fed adopted zero-interest rate (ZIRP) policies and the now famous quantitative easing (QE) policies in late 2008.

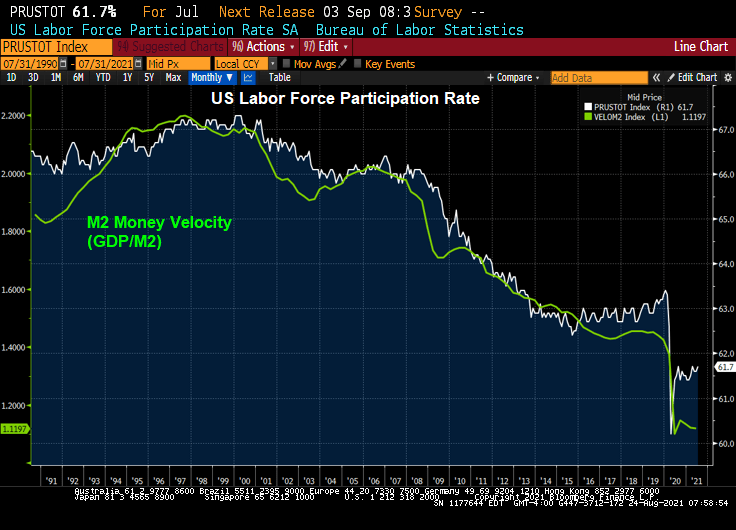

Congress member Alexandria Ocasio-Cortez asked Fed Chair Powell about the Fed helping with US unemployment. We are already at zero rates (on the short-end), and Congress should look at their policies on why labor force participation is slow to recover from the Covid epidemic.

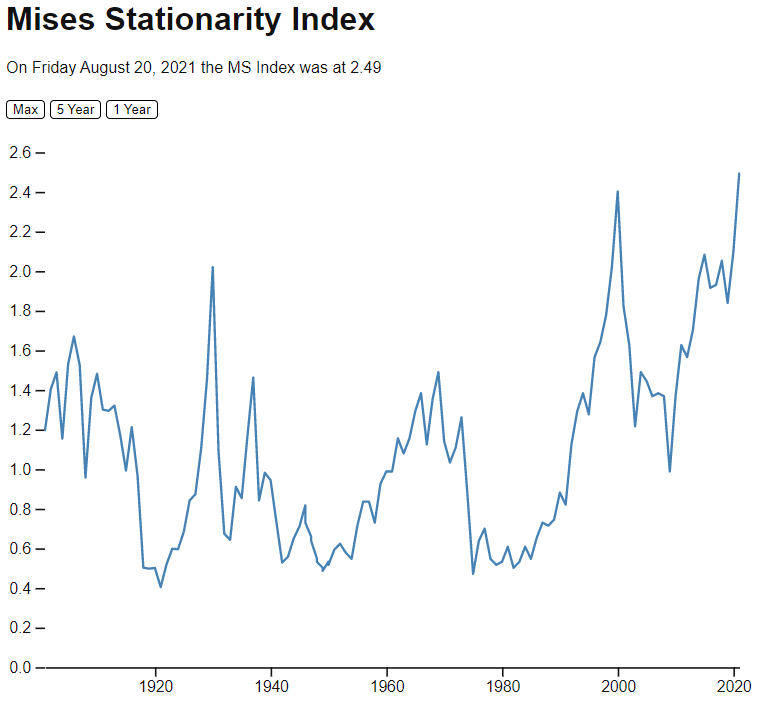

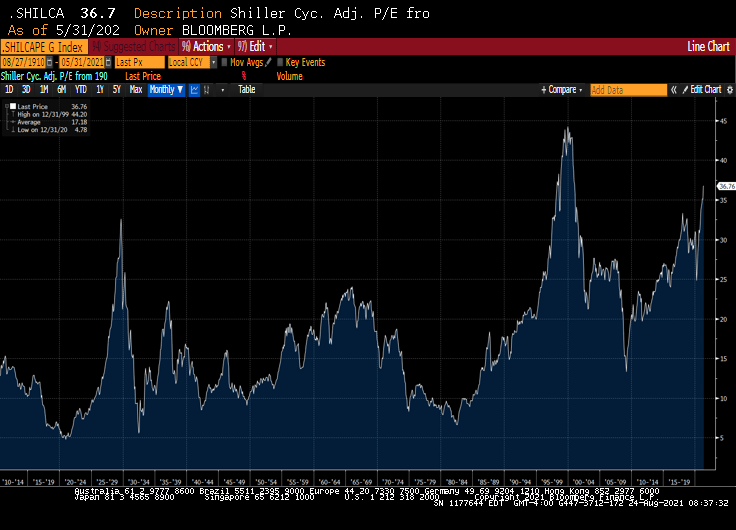

The Mises Stationarity Index is different than the Shiller CAPE index, which is showing equities as being overpriced, but not yet in dot.com bubble zone.

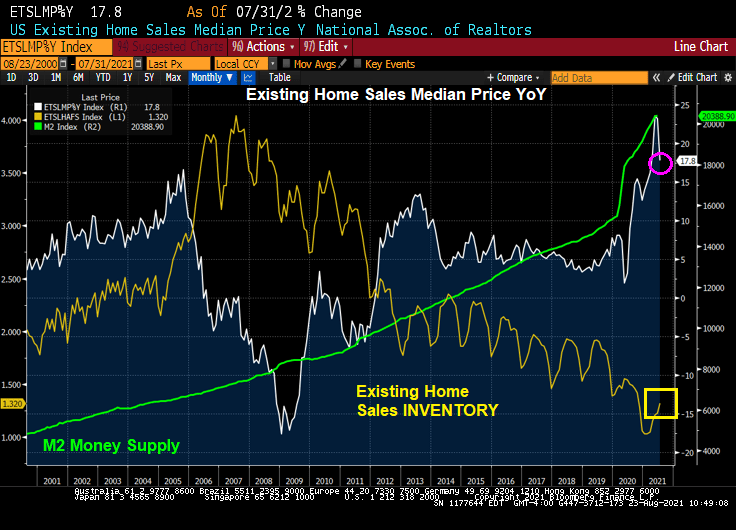

US existing home sales in July rose to 5.99 million SAAR, beating expectations. But the inventory of home available for sale remains low by historic standards.

The median price of existing homes declined to 17.8% YoY with The Federal Reserve pumping money into the system like there is no tomorrow.

Bloomberg had the following headline: “Sales of Existing Homes in U.S. Rise as Inventory Picks Up.” While that is a true statement, existing home sales inventory is still down 12% YoY.

I wonder if the attendees at the Jackson Hole Fed conference will be discussing the gut-wrenching home price growth? Rumor has it that Fed Chair Powell will use J-Hole as a platform to suggest paring back on the monetary stimulus.

The KC Fed Jackson Hole conference is a US policy makers’ Davos, an uber-elite US location. You would think that the KC Fed would hold their conference in Kansas City or Omaha, Nebraska as a show of support for the working men and women. But nooooo. They have to hold it where Liz Cheney (GOPe, WYO) lives. And other elites have expensive vacation homes.

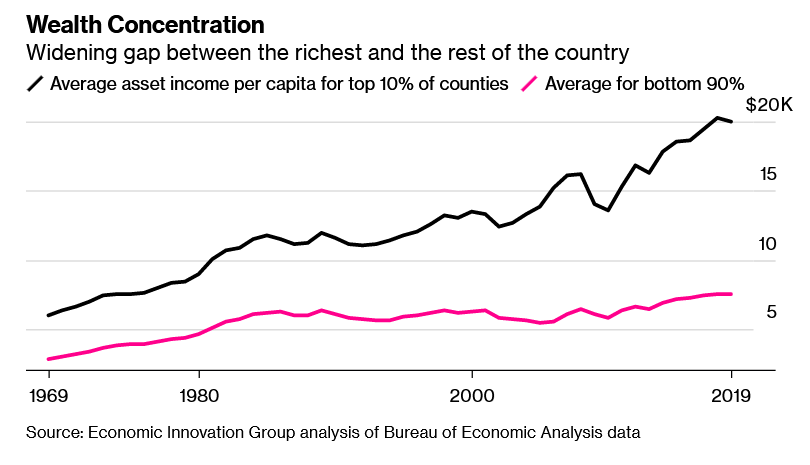

(Bloomberg) — When U.S. Federal Reserve officials head to their annual mountain retreat next week to talk economic inequality, they’ll be sitting in the country’s wealthiest county.

Wyoming’s Teton County, home to Jackson Hole, has the nation’s highest per-capita income from assets, according to a study by the Economic Innovation Group. The analysis found a sharp increase in geographic concentration of asset ownership over the past decades.

Jackson Hole, a rural community near the majestic Grand Teton national park and renowned ski slopes, has attracted the ultra-rich in recent years, pulling away from the rest of the country.

The EIG report, released Wednesday, specifically looked at income from interests, dividends and rents. The gap between counties with the lowest and highest asset income per capita rose sixfold between 1990 and 2019, as income skyrocketed in centers of finance, technology, mining and recreation.

Income from assets — a measure of wealth that excludes wages and government assistance programs — make for about a fifth of personal income nationwide.

It’s soared in places like New York City and the San Francisco Bay Area. Meanwhile, across Appalachia, the Deep South and much of the Midwest, it stagnated, representing a negligible source of income.

“I was pretty shocked that so much of the country has derived so little benefit from the boom in asset prices and asset values that we’ve seen over the past couple of decades,” Kenan Fikri, research director at EIG, said in an interview.

Asset ownership offers people something to fall back on during periods of economic uncertainty that could result from unemployment, illness, or, as it has been the case for many Americans over the past year, a pandemic. But for those who live paycheck to paycheck, saving and investing is hardly an option.

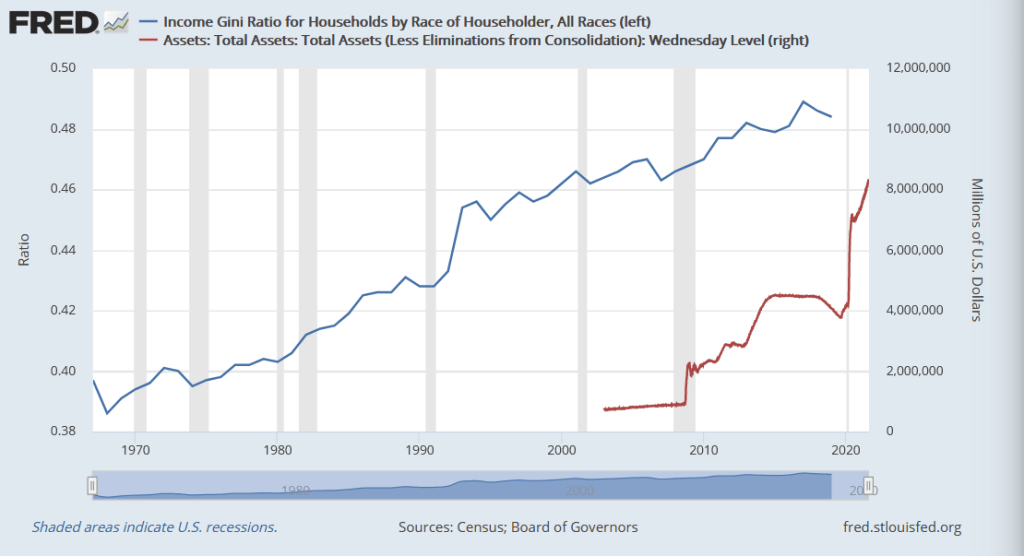

Income inequality as measured by the GINI ratio? It has risen steadily since Fed’s massive balance sheet expansion. Then again, it has been rising steadily since the 1960s with the largest jump in income inequality occurring when Bill Clinton, the Arkansas populist, was President.

Bad optics for policymakers, unless that truly don’t care about the middle-class.

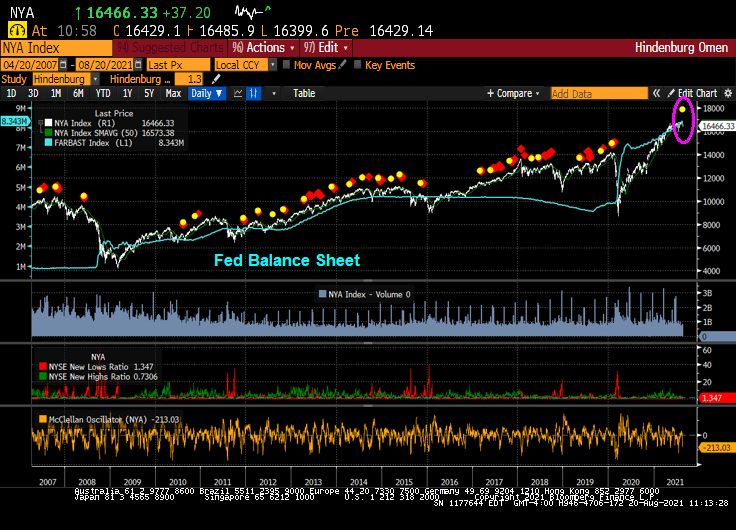

The famous Hindenburg Omen, the technical indicator that predicted the 2008 correction in the stock market, has just flashed “ALARM” again.

To be sure, there hasn’t been a major correction in the stock market since the financial crisis, primarily because The Federal Reserve has constantly goosed the markets since late 2008.

Just as the Shiller CAPE ratio is signalling ALARM!

As is the Buffet Indicator.

I have no doubts that the Fed will withdraw its monstrous stimulus from the market after the Jackson Hole Fed conference. … NOT!!!!

Maverick Capital posted this nugget today showing The Buffet Indicator (US equity market cap/GDP) and US Corporate Profits / GDP. All I can say is “simply unsustainable.”

Headline! “Fed’s Kaplan says delta variant could cause him to rethink his tapering view”

Face it, the Federal Reserve may alter its growth path on asset purchases of Treasuries and Agency Mortgage-backed Securities, but it is doubtful that they will pare back their balance sheet. Call it “A Never-ending balance sheet for you” world.

Why? Seemingly never-ending Covid crisis, etc.

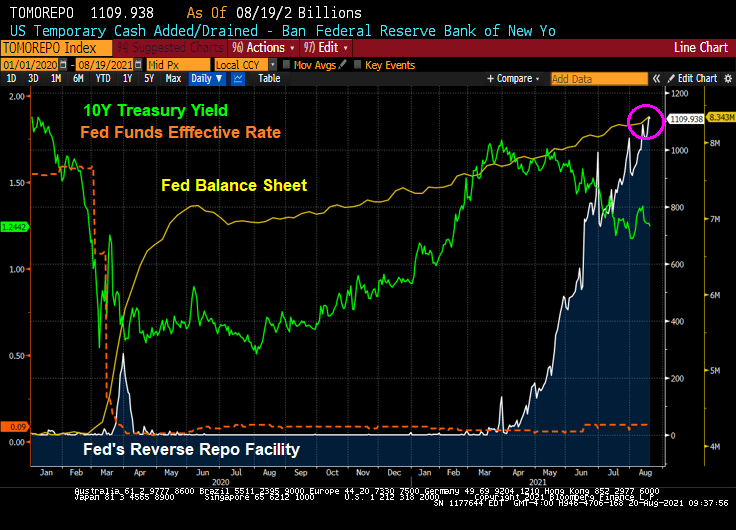

Let’s look at US Treasury yields today. The 10-year Treasury yield is up slightly to 1.25% as of 10am EST.

Here is a chart of the 10-year Treasury yield, Fed Funds effective rate, Fed Balance sheet and reverse repos since the Covid outbreak and Fed massive intervention. Bottom line, the have repressed the short-term interest rates and put downward pressure on the 10-year Treasury yield.

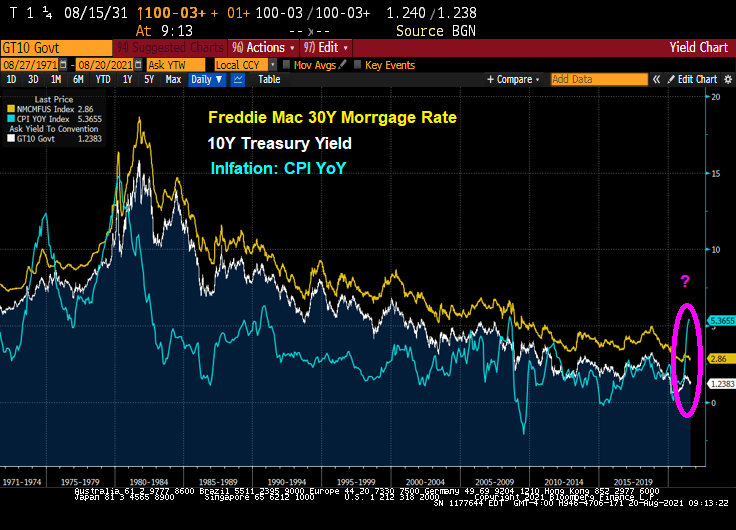

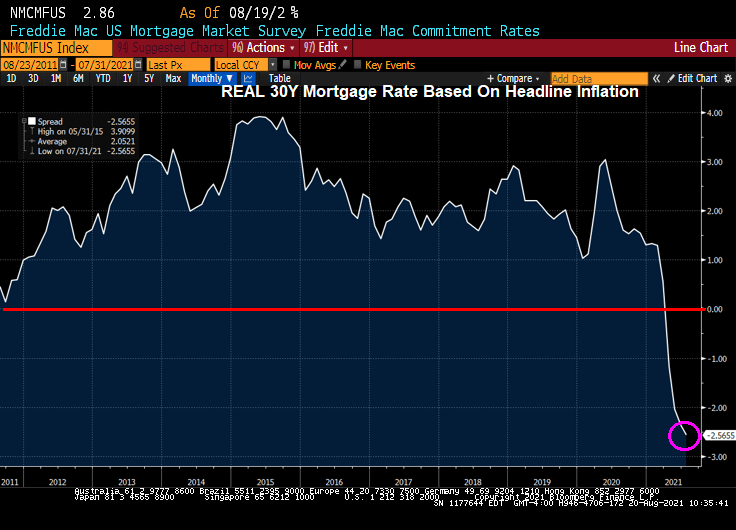

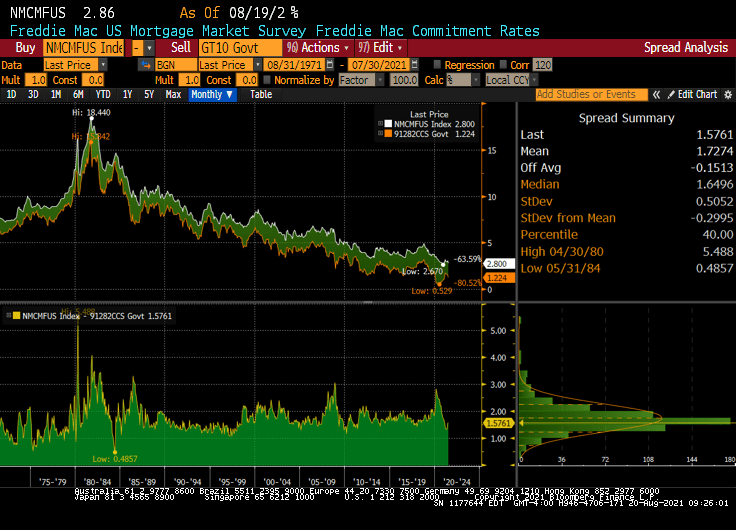

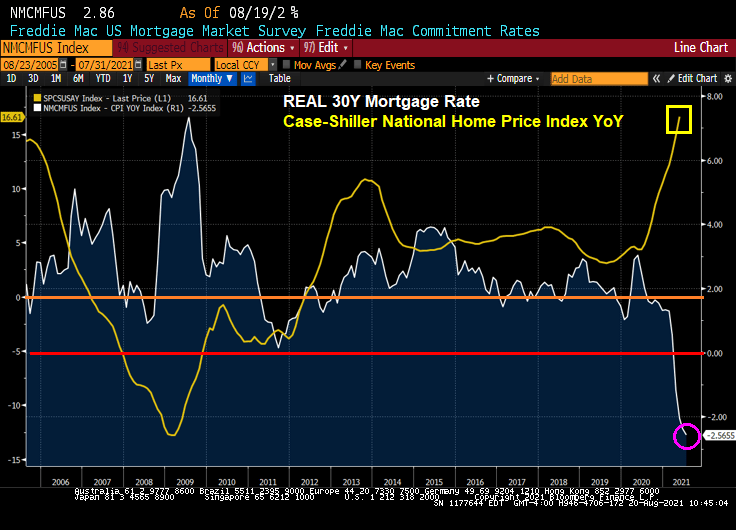

As the 10-year Treasury yield remains repressed DESPITE HIGHEST INFLATION RATE SINCE 2008, the Freddie Mac 30-year mortgage rate remains repressed as well. Yes, that mean NEGATIVE REAL MORTGAGE RATES.

This produces a REAL mortgage rate of -2.56%.

The spread of mortgage rates over the 10-year Treasury yield is about 173 basis point since 1971.

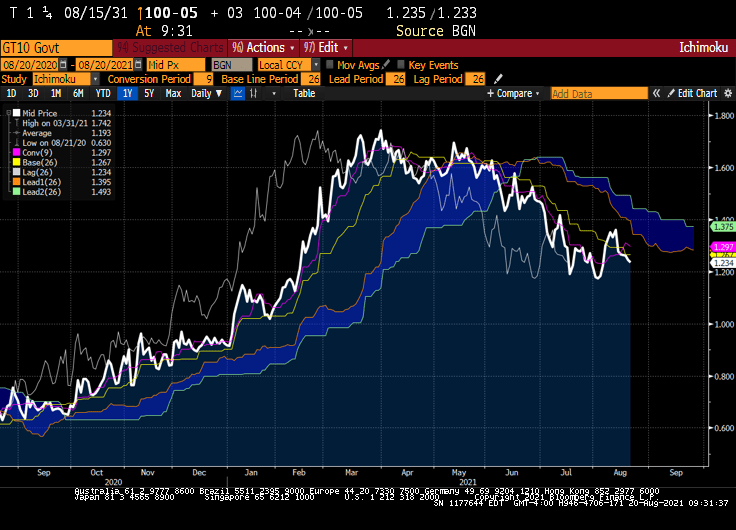

Where will Treasury yields go from hear? If we believe technical analysis like the Ichimoku Cloud, the 10-year Treasury rate will likely rise.

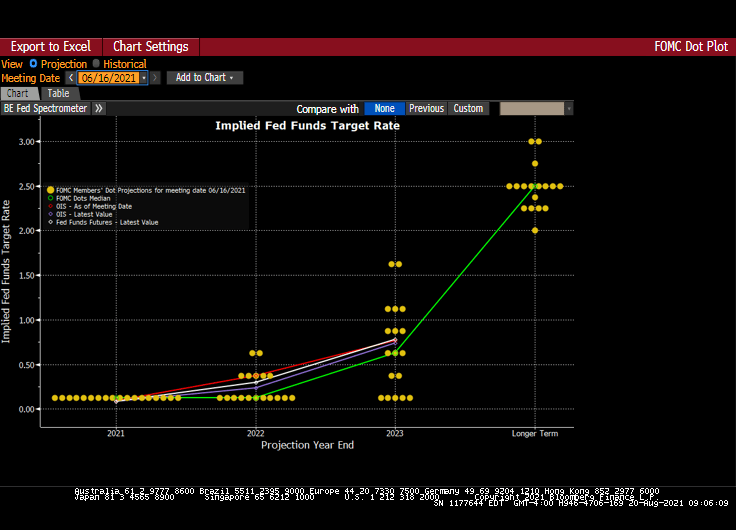

And The Fed’s Dots project also see rates rising (at least on the short-end.

Negative real mortgage rates and blistering home price growth?

Will the attendees at the KC Fed Jackson Hole conference discuss these matters? Or will it just be a Federal Reserve Soul Shake (dance)?

You must be logged in to post a comment.