A zombie foreclosure refers to a situation where a homeowner vacates their property after receiving a notice of default, expecting they will lose the home in the pending foreclosure. The foreclosure may get canceled for any number of reasons and never completed.

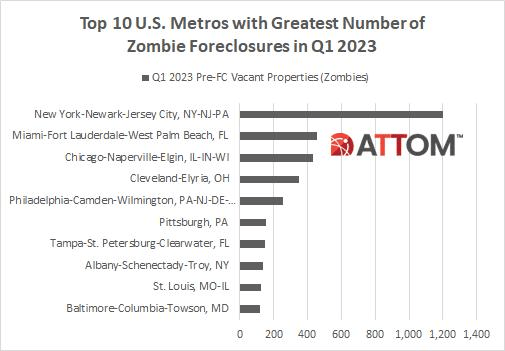

New York City and its surrounding areas lead the nation in zombie foreclosures. Followed by Miami. Chicago and Cleveland. Then Philadelphia.

As The Fed takes away the massive monetary punch bowl, mortgage rates have risen to the highest since November 2008. And with the withdrawal of monetary stimulus (raising Fed Target Rate), mortgage purchase applications have declined.

Here is a photo of The Federal Reserve fighting the housing and mortgage market.

How crazy was The Federal Reserve’s overreaction to the government shutdowns surrounding the Covid epidemic? While most analysts talk about California, I am going to discuss … Cleveland Ohio as an example of how The Fed can destroy markets.

The Case-Shiller home price index for Cleveland rose 31.5% since January 2020 just before The Fed unleashed its massive monetary stimulus on an unsuspecting city.

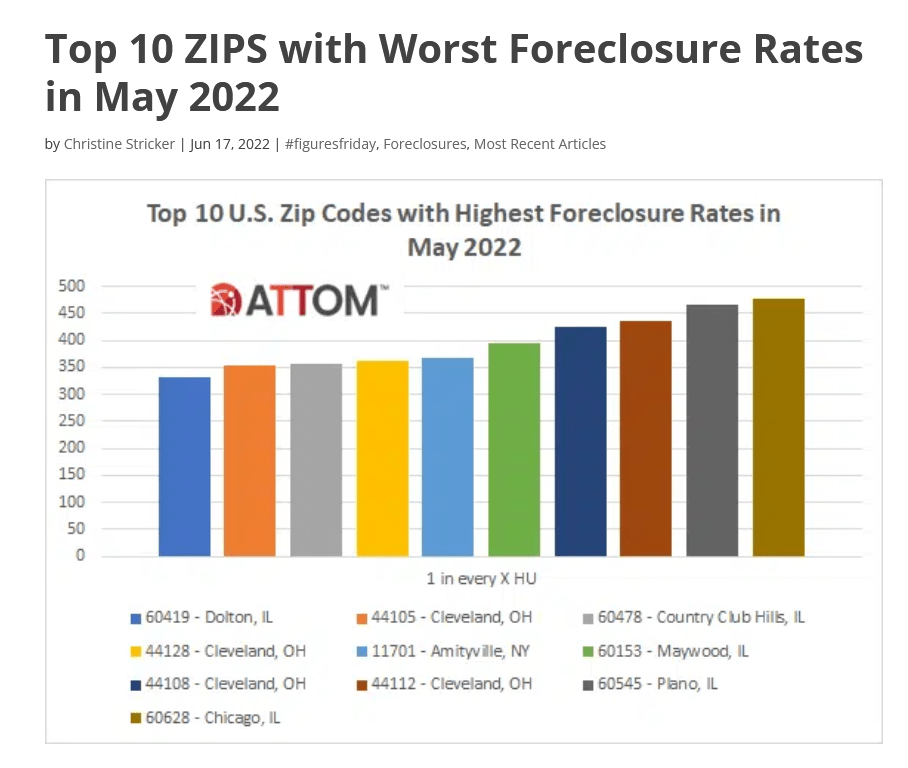

But as The Fed starts to tighten monetary policy after Yellen’s too loose for too long policies followed by Powell, foreclosure rates are soaring in Cleveland. In fact, according to Attom Data, 5 of the top 10 zip codes with the worst foreclosure rates in May 2022 were in Cleveland.

Of course, Cleveland is much like much of the rust belt (except Columbus Ohio). The rust belt is losing population along with heavy tax states like New York and Illinois. Destination states? Texas, Florida, the Carolinas and Tennessee.

Then at the national level, Atlanta Fed’s GDPNow real-time tracker fell to 0% growth.

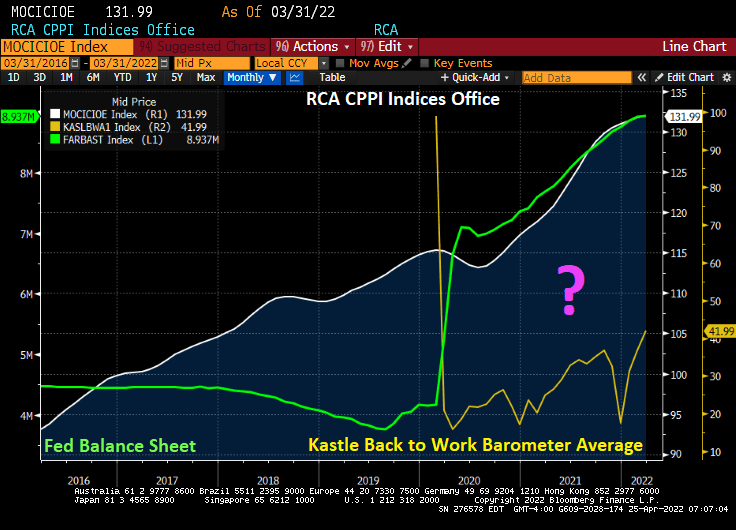

Do you want to see a magic trick? Like how governments shut down the US economy resulting in collapsing office occupancy rates while the price of office buildings rose dramatically (+16.3% since Q2 2020)?

Kastle’s “Back to work barometer” is showing that the 10 city average occupancy rate in the US is now only 42.8% as remote working has caught on. And the fear of yet another Covid mutation is keeping office occupancy below 50%.

Even Washington DC, home of Dr. Anthony Fauci, has only a 37.5% occupancy rate. Of the top 10 cities, Austin TX has the highest office occupancy rate at 62.4%.

So, the magic trick is not why America is so slow to return to the office, but why commercial office prices are rising so fast. Ah, Federal government STIMULYTPO! Aka, The Federal Reserve has been overstimulating the economy since 2008 and particularly since 2020 and Covid.

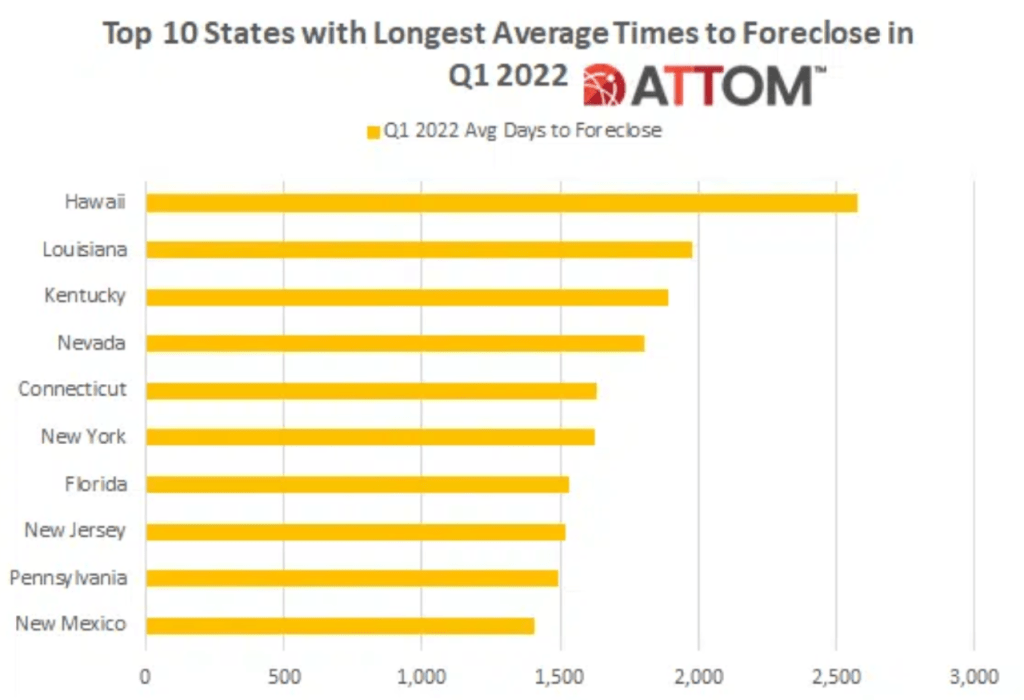

Speaking of a magic trick, here is how government’s make the average time to foreclosure up to over 7 years in Hawaii and 4.4 years in New York. In simple terms, you can buy a home in New York, never make a mortgage payment and live rent free for an average of 4.4 years.

So, the government’s magic trick is to 1) shut down local economies in fear of Covid, 2) provide excessive fiscal and monetary stimulus to combat the shutdown, 3) watch office building prices soar with stimulus as office occupancy remains below 50%.

Do you want to see a magic trick? Watch The Fed try to tighten monetary easing and NOT crash the economy.

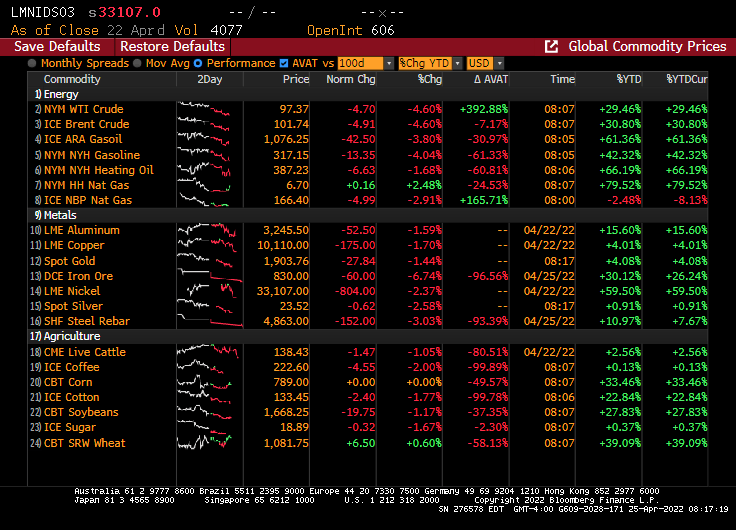

Update for 04/25/2022. 10Y Treasury yields DOWN 8.7 bps.

And commodities are tanking. WTI oil is down 5%, iron ore is down almost 7%.

And the Dow is diving with increased expectations of Fed monetary tightening, but the expectations (green line) have been declining this morning.

As we are all aware, The Federal Reserve launched its monetary “stimulypto” in March 2020 to combat the Covid virus. Coupled with the surge in Federal stimulus, we have seen home prices rise over 20% since February 2020.

Specifically, New York City home prices are up 26.3% since February 2020, Chicago home prices are up 21.7%, and Los Angeles home prices are up 32.5%. Fed monetary stimulypto is up 113% since February 2020.

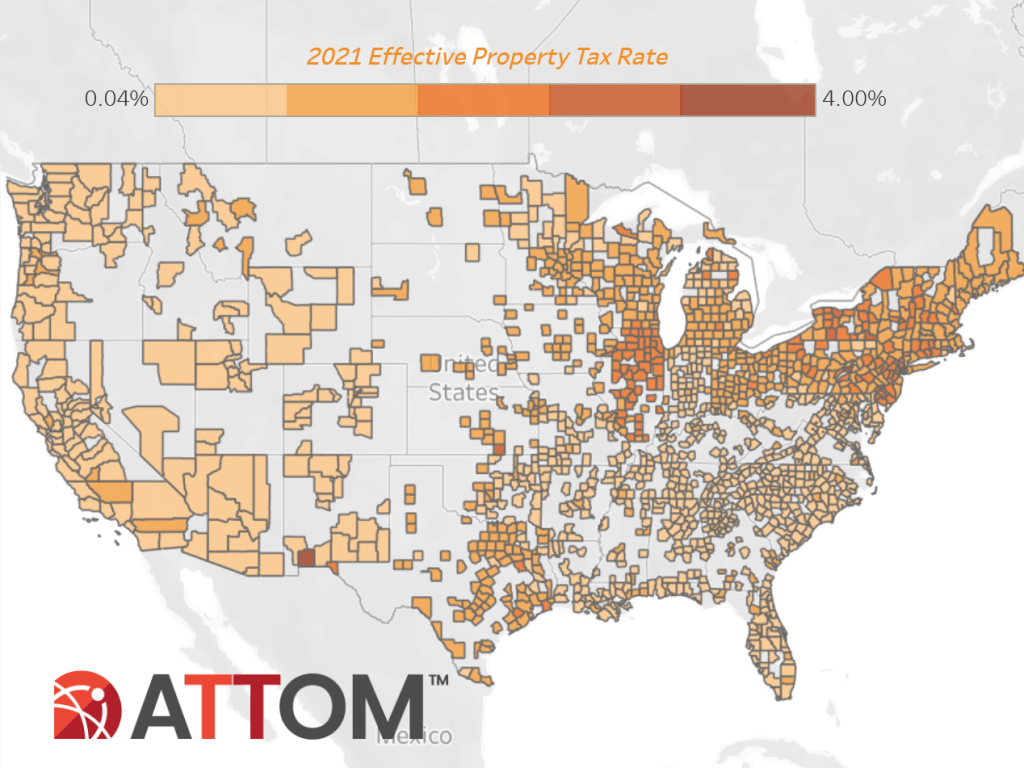

Of course, this has resulted in soaring PROPERTY TAXES as well. According to Attom Data Services, “Among 1,481 U.S. counties with at least 10,000 single-family homes in 2021, 16 had an average single-family-home tax of more than $10,000, including 12 in the New York City metro area. The top five were Kings County (Brooklyn), NY ($13,734); Marin County, CA (outside San Francisco) ($13,719); Westchester County, NY ($13,674); Essex County, NJ ($13,116) and Nassau County, NY ($13,095).”

Of course, not all metro areas raised their property taxes. Major markets with the largest decreases in average property taxes included Pittsburgh, PA (down 35.1 percent); New Orleans, LA (down 20.2 percent); Houston, TX (down 18.7 percent); Dallas, TX (down 12.2 percent) and Austin, TX (down 7.7 percent).

States with the highest effective property tax rates in 2021 were Illinois (1.86 percent), New Jersey (1.73 percent), Connecticut (1.67 percent), Vermont (1.55 percent) and Pennsylvania (1.37 percent).

Even if The Federal Reserve removes its massive monetary stimulypto (MMS), property taxes will remain elevated unless cities reduces their property tax rates. But Democrat-controlled cities tend to be addicted to spending much like The Federal government.

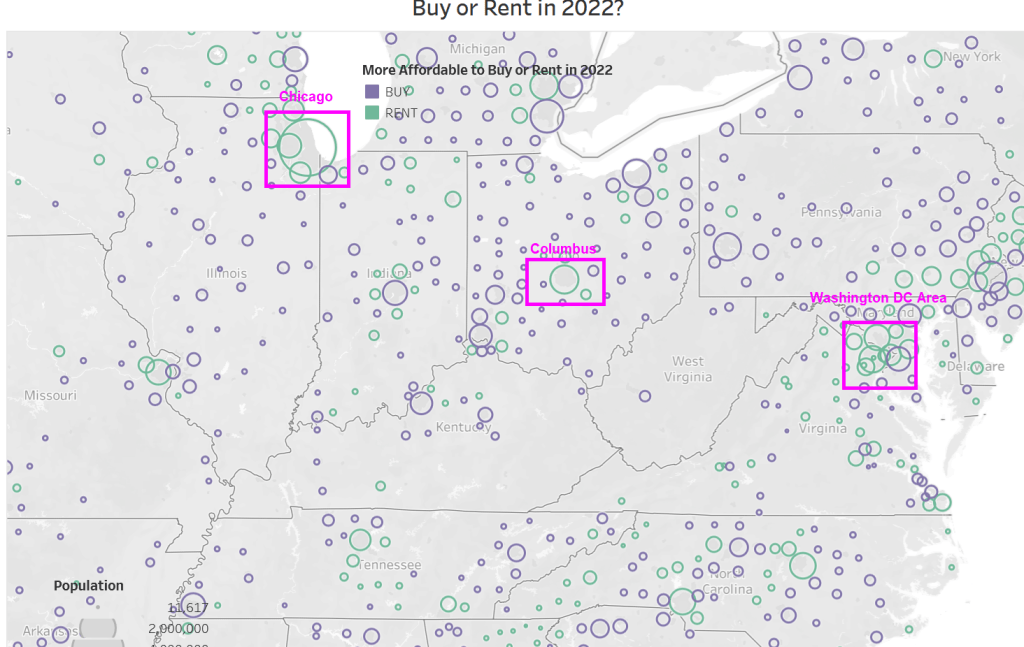

According to Attom, US home prices are growing faster than rents in nearly 90 percent of the nation; but prices are still more affordable in almost 60 percent of U.S. markets; Renting remains more financially viable in most-populous urban areas.

If we look at Attom’s map of affordability, you can see that in western states, it is more affordable to rent. And in megalopolis (Boston, New York, Philadelphia, Washington DC). And Miami. But elsewhere in the eastern states, it is more affordable to buy than to rent.

Of course, any where I live like Phoenix, Fairfax VA, Chicago IL, and Columbus OH it is more affordable to rent than to own.

You will notice that the areas where buying is more affordable than renting tend to be smaller towns with slower growth, while larger cities tend to be more affordable to rent.

You must be logged in to post a comment.