Memorial Day weekend is one where families often travel to meet relatives and friends, or travel to Washington DC to remember those who have died in the service of our country.

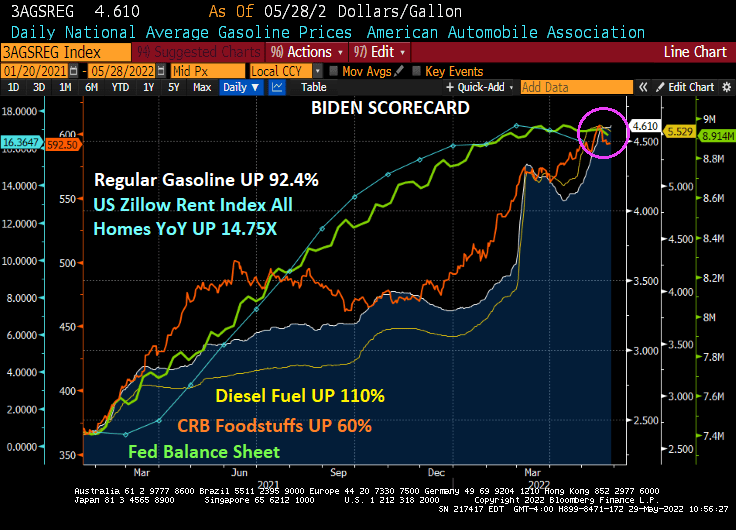

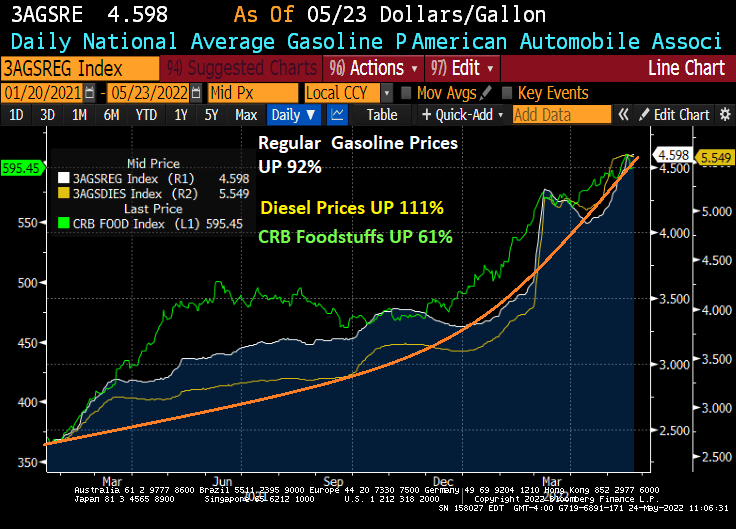

But traveling has gotten a lot more expensive under Biden. Gasoline prices are up 92.4% under Biden, while food prices are up 60%. Those hamburgers and hot dogs for grilling are being replaced by … pizza? Or maybe plant-based products.

Zillow’s Rent Index All Homes YoY was only 0.6234% in February 2021, and has soared to 16.36% YoY under Biden. That is an increase of 14.75x. So, not only is it much more expensive to travel on Memorial Day weekend, but it is far more expensive to stay home in your rental property.

On the currency front, we are seeing the US Dollar falling (greenback line), along with the Yuan/USD cross currency. West Texas Intermediate Crude Cushing OK spot is at $115.07.

At least Venezuela and Iran are benefiting greatly by Biden’s energy policies, even if Americans are suffering. Perhaps this is the new foreign policy of Wynken (US VP Harris), Blynken (US SecState), and Nod (Biden).

Remembering my Uncle Jack Sanders who served in the Battle of The Bulge during World War II, winning an individual Silver Star for bravery and two Purple Hearts. He rose from “buck” private to First Sergeant by the end of WWII.

You must be logged in to post a comment.