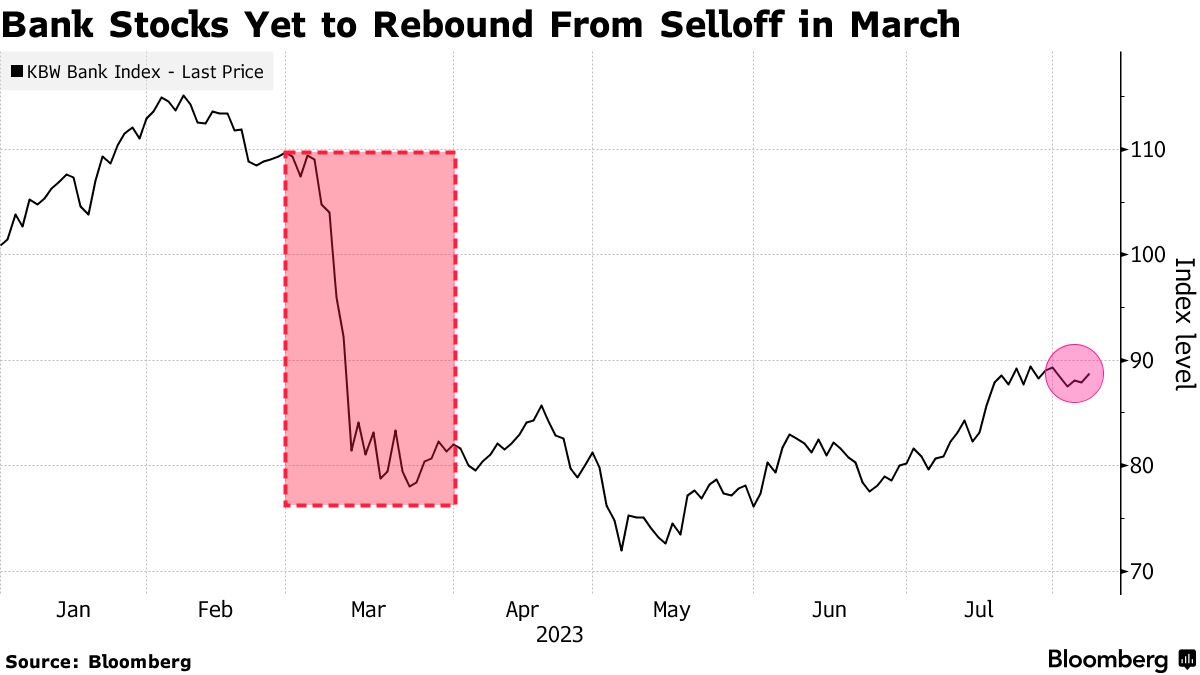

Higher funding costs, potential regulatory capital weaknesses and rising risks tied to commercial real estate are among strains prompting the review, Moody’s said late Monday.

“Collectively, these three developments have lowered the credit profile of a number of US banks, though not all banks equally,” the rating company said.

Moody’s Sees Problems Ahead for US Banks

Rating company issues raft of downgrades, outlook

Source: Moody’s

Shares declined for firms that had their ratings cut, including M&T Bank Corp., down 3.2%, and Webster Financial Corp., which lost 1.3%. Moody’s also adopted a “negative” outlook for 11 lenders, including PNC Financial Services Group, Capital One Financial Corp. and Citizens Financial Group Inc. Among those, PNC was down 2.2% and Capital One lost 2.4%.

Investors, rattled by the collapse of regional banks in California and New York this year, have been watching closely for signs of stress in the industry as rising interest rates force firms to pay more for deposits and bump up the cost of funding from alternative sources. At the same time, those higher rates are eroding the value of banks’ assets and making it harder for commercial real estate borrowers to refinance their debts, potentially weakening lenders’ balance sheets.

“Rising funding costs and declining income metrics will erode profitability, the first buffer against losses,” Moody’s wrote in a separate note explaining the moves. “Asset risk is rising, in particular for small and midsize banks with large CRE exposures.”

Some banks have curbed loan growth, which preserves capital but also slows the shift in their loan mix toward higher-yielding assets, Moody’s said.

Banks that depend on more concentrated or higher levels of uninsured deposits are more exposed to these pressures, especially banks with high levels of fixed-rate securities and loans.

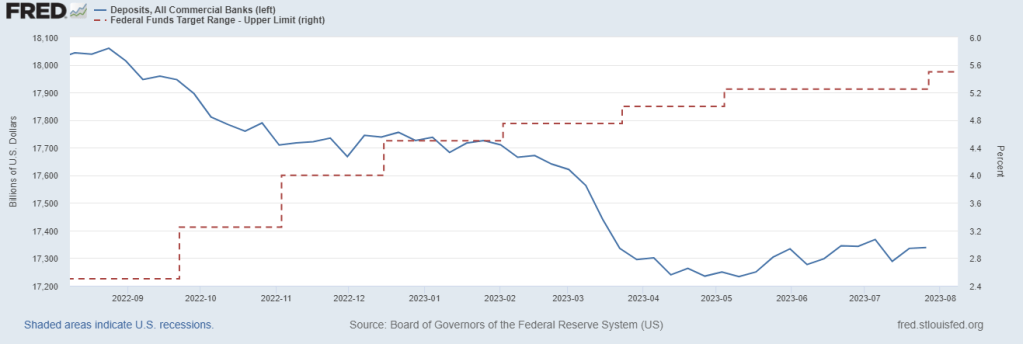

Deposits are declining as The Fed hikes rates.

So, Bidenomics reminds me of the film “Rollerball” where big corporations run the government and run a game akin to Rome’s gladiator fights.

Yes, Bidenomics is an FDR-type massive expansion of government into the private sectors requiring massive Federal spending … and inflation. Except that it beenfits anything BIG and powerful to the detriment of the small and weak.

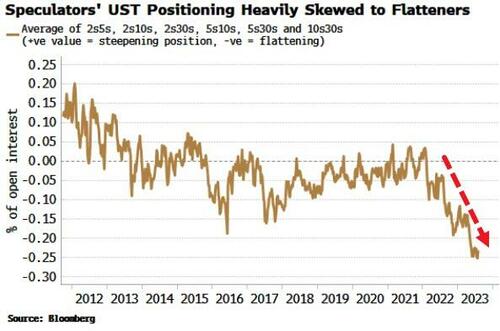

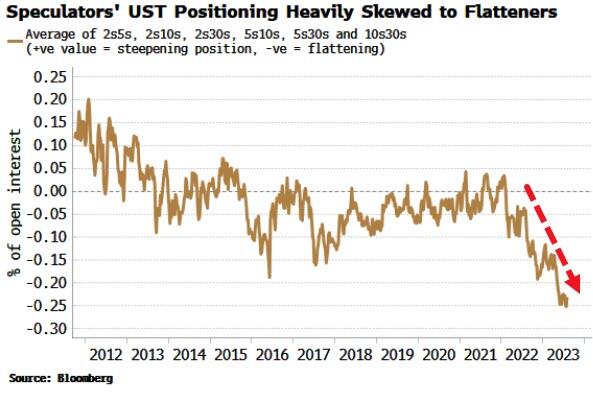

(Bloomberg) Friday’s jobs data sparked a relief rally in bonds and a flatter yield curve, but the pain trade is still for higher yields and a steeper curve – the lesser-spotted bear steepener – with this week’s CPI a potential catalyst.

Last week was a turbulent one for bonds, but the continued softening in payrolls data served to remind the market that supply and fiscal-profligacy fears have to be counter-balanced with an economy that’s in its late-cycle stages.

After the data, 10-year yields took the elevator back down to sub-4.05% after briefly going above 4.20%. They have since clambered back to 4.12%, but their next cue is likely to come from Thursday’s CPI report. Headline is expected to nudge back up to 3.3% (from 3% last month), mainly due to base effects, and core is expected to hold steady at 4.8%.

Still, stronger-than-expected data probably means higher yields in a market more acutely alert to inflation (and therefore supply) risks. As with last week, term premium would likely drive the move, meaning a curve steepening. After relentlessly flattening for the last two years, the pain trade is for a steeper curve. Implicit positioning of speculators from the COT report shows there is a heavy skew to a flatter curve.

The negative carry for most flatteners remains punitive (for 2s10s USTs it’s ~83bps over a year), but the large upside potential from supply/inflation worries and the covering of positions begins to make that look less insurmountable.

Finally, the Bundesbank’s decision to stop paying interest on domestic government deposits – which initially pushed short-term German bonds higher this morning – highlights the broader issue of central banks paying interest on reserves when they are superabundant.

In the days of QE and 0% interest rates, the ECB and Fed at al. remitted money to their treasuries from the income on their bond portfolios.

But now that is reversed as bond income is dwarfed by the cost of paying interest on trillions of bank reserves. Take the Fed, whose debt to the Treasury is now accruing at over $2 billion each week.

This is something that will become more politically contentious, especially as economies continue to slow and cost-of-living pressures bite further.

Bidenomics. The takeover of the US economy by BIG corporations, BIG labor unions, BIG tech, BIG pharma, BIG defense, BIG healthcare, BIG media, BIG banks, BIG tech, BIG … Well, anyting that is BIG and powerful that can buy influence in Congress and the Administration. Except BIG energy which lost out to BIG Progressive DC thinktanks.

Leading to BIG inflation!

But I feel good! Even though inflation expectations are soaring again as gasoline soars again.

If you believe the recovery talk (from the reckless Covid economic and school shutdowns of 2020), all is well in the (economic) garden. For example, M2 Money Velocity (GDP/M2), is almost back to where it was just prior to the 2020 Covid outbreak and resulting government-caused recession. M2 Velocity was 1.425 in Q4 2019 and was 1.289 for Q2 2023. But ever since The Federal Reserve became hyper intervention in the economy (let’s just start with Bernanke’s massive intervention in late 2008 (red line) and the Fed balance sheet expansion), and it was increased dramatically during the Covid shutdown. And is STILL above $8 trillion!

Before Bernanke and the financial crisis of 2008-2009, M2 Money Velocity was above 2.0. But it has been below 2.0 ever since The Fed’s intervention in 2008.

Granholm called China National Energy Administration Chairman Zhang Jianhua, a longstanding senior member of the Chinese Communist Party, for a half-hour one-on-one conversation on Nov. 21, 2021. Granholm’s calendar also shows an earlier phone call had been scheduled with Jianhua for Nov. 19 but a rep for the former Michigan governor said the first call never took place. Then, on Nov. 23, 2021, the White House announced a release of 50 million barrels of oil from the SPR, the largest release of its kind in U.S. history at the time.

According to Fox News, Granholm’s previously-undisclosed talks with China National Energy Administration Chairman Zhang Jianhua — revealed in internal Energy Department calendars obtained by Americans for Public Trust (APT) and shared with Fox News Digital — reveal that the Biden administration likely discussed its plans to release oil from the SPR with China before its public announcement in the US: yes, China’s Communist Party learned what Biden would be doing before the US did.

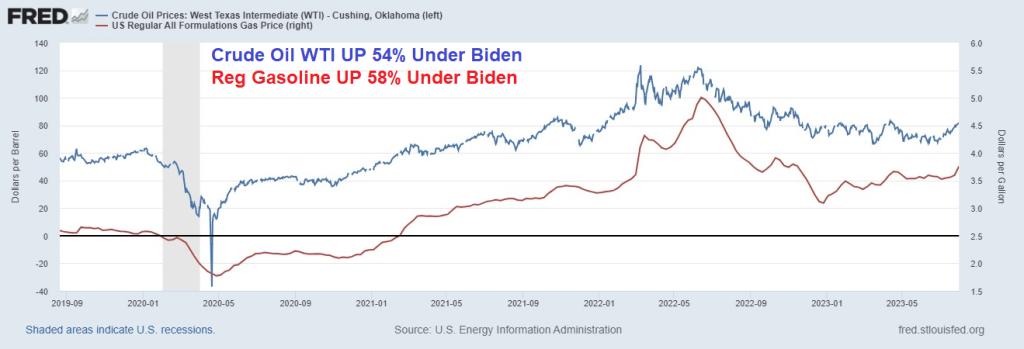

While Biden/Granholm are merrily draining the Strategic Petroleum Reserve, we see that West Texas Intermediate Crude Oil (Cushing) prices are up 54% under Biden and regular gasoline prices are up 58%.

All is sort of well in the garden because The Federal Reserve still has its massive interventionist foot on the gas pedal. Yet, America is on an economic suicide course with its green energy hype.

Frankly, Biden talks like Chance The Gardener from the film “Being There.” Except that Chance the Gardener is a nice person and Biden is reputed to have been the nastiest member of the US Senate. Not to mention the stupidest member of the US Senate. Although I don’t think Chance the Gardener would have taken millions in bribes from foreign countries like China and Ukraine.

Biden The Gardener should be Biden’s re-election slogan! Of course, Chance the Gardener could walk much better than Biden with his dementia shuffle. And Chance was a great gardener, all Biden knows how to do is sell the “Biden Brand” of political influece peddling to foreign countries.

“One of the most cowardly things ordinarily people do, Is to shut their eyes to facts.” – C.S. Lewis

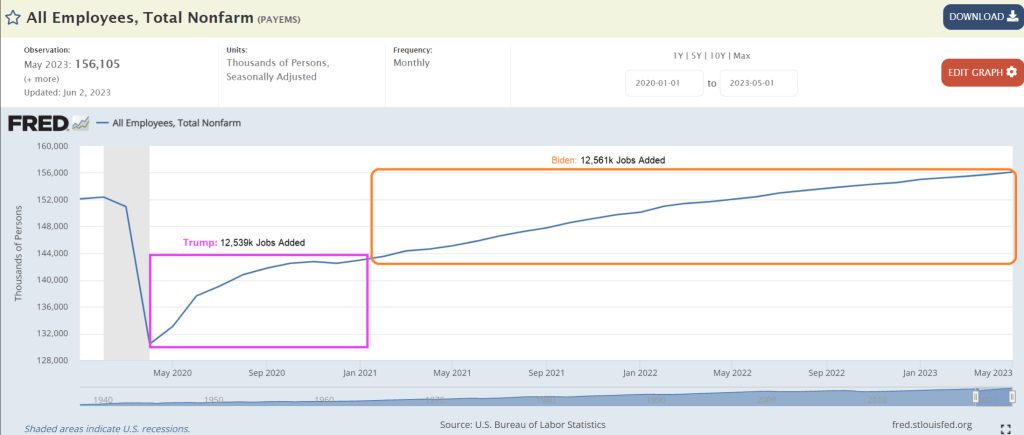

Okay, we know Biden lies constantly and misrepresents facts (hey, he is a politician like Adam Schiff (D-CA). But this graphic praising Bidenomics with Biden having created the most jobs (average per month) since Carter (notice they left out Democrat darling Jimmy Carter!!!). In this absurd graphic, Biden wins by “creating” over 400k jobs per month while Trump lost jobs per month. Riveting … except that it is completely misleading.

Actually, the US economy added 12.53 million jobs after April 2020 (Trump) while Bidenomics created took 2 1/2 years to add 12.56 million jobs. So, Biden took over twice as long to create jobs after Covid than it did under Trump. Simply opening the economy and schools produced that magical claim by Biden. And the National Teacher’s Union and Randi Weingarten worked with Fauci to orchestrate shutting down schools. Blaming Trump for local governments shutting down the economy is pure bunk.

12.53 millions jobs added / 8 months = 1.56 million jobs average per month. Biden? 12.56 million jobs added / 30 months = .43 million jobs average per month. So, Trump averaged more than 3x the job growth post-Covid than Biden.

Here is the “glories of Bidenomics” from the White House. As Biden likes to say, pure malarkey!

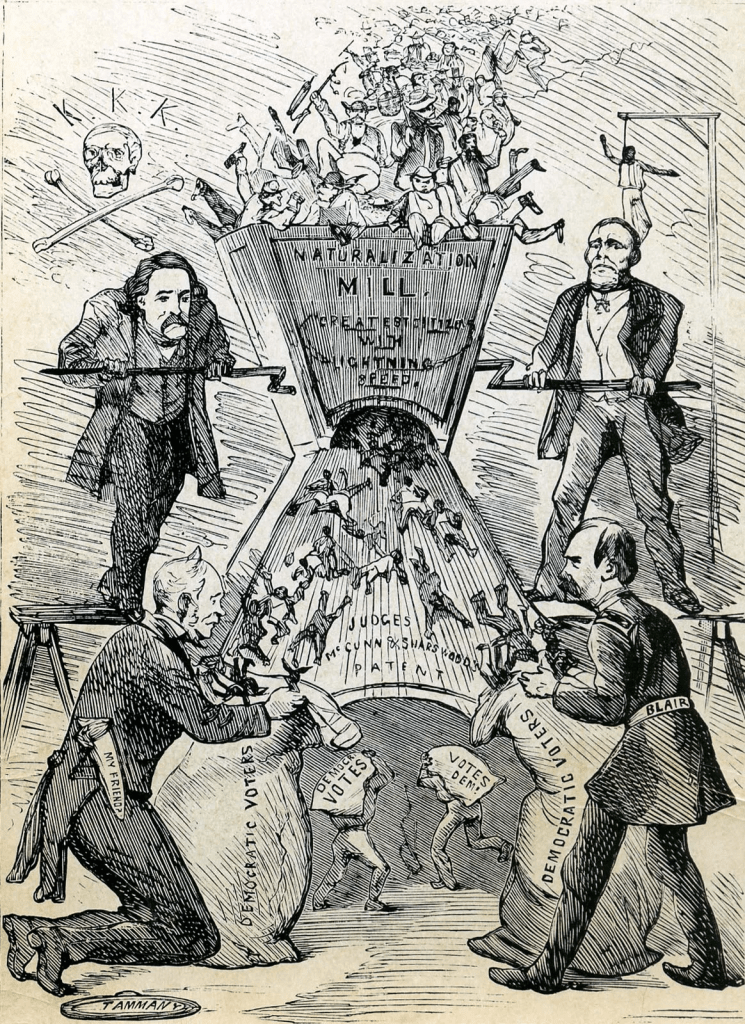

I wonder if the Democrat Party is a rebirth of New York City’s Tammany Hall corrupt political movement of the 1800s? Is Biden Boss Tweed? Or is Obama Boss Tweed with Biden as his nasty, dimwitted henchman?

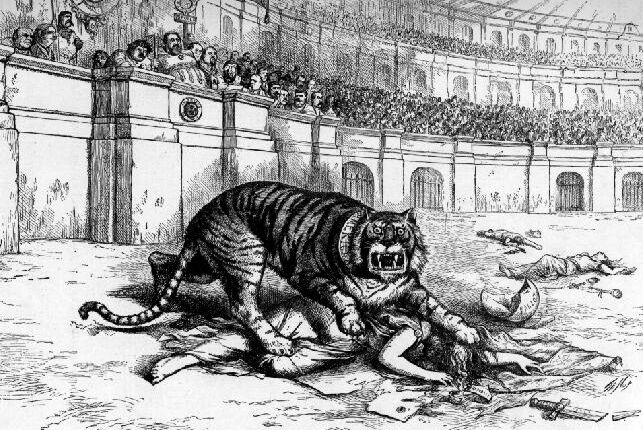

In 1871, Thomas Nast denounces Tammany as a ferocious tiger killing democracy. The image of a tiger was often used to represent the Tammany Hall political movement. Sounds an awful lot like today’s Democrat Party.

Josef Stalin of the old Soviet Union used to be called County Joe. But Biden has so many possible nicknames: Corrupt Joe, Pay-for-play Joe, Sleazy Joe, Bully Joe, etc. How about Green Joe?

Green Joe (or the Nasty Green Giant?) along with his energy goon Jennifer Granholm, have drained the strategic petroleum reserve by 46% while gasoline prices have soared 60% under Bidenomics.

Gasoline prices have rise over 6.5% just since 7/23/2023.

Trump wants to drain the swamp, Biden/Granholm want to drain the strategic petroleum reserve so we can’t go back to fossil fuels. Biden and Granholm as Fossil Fools

Energy Secretary Jennifer “The Evil Pixie’ Granholm demostrating how she will refill the strategic petroleum reserve. Which she never will, of course.

US average hourly earnings continued at 4.4% year-over-year (YoY). However, the last core inflation reading was 4.8% YoY, so real wages continue to decline.

Rent CPI for June was 7.8% YoY.

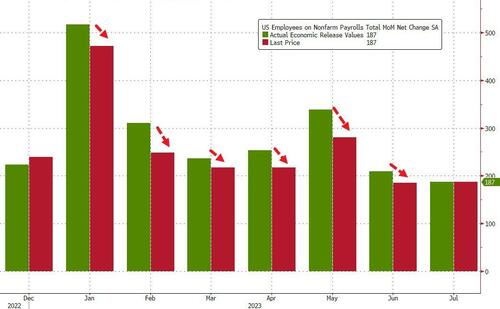

Here is the rest of the story.

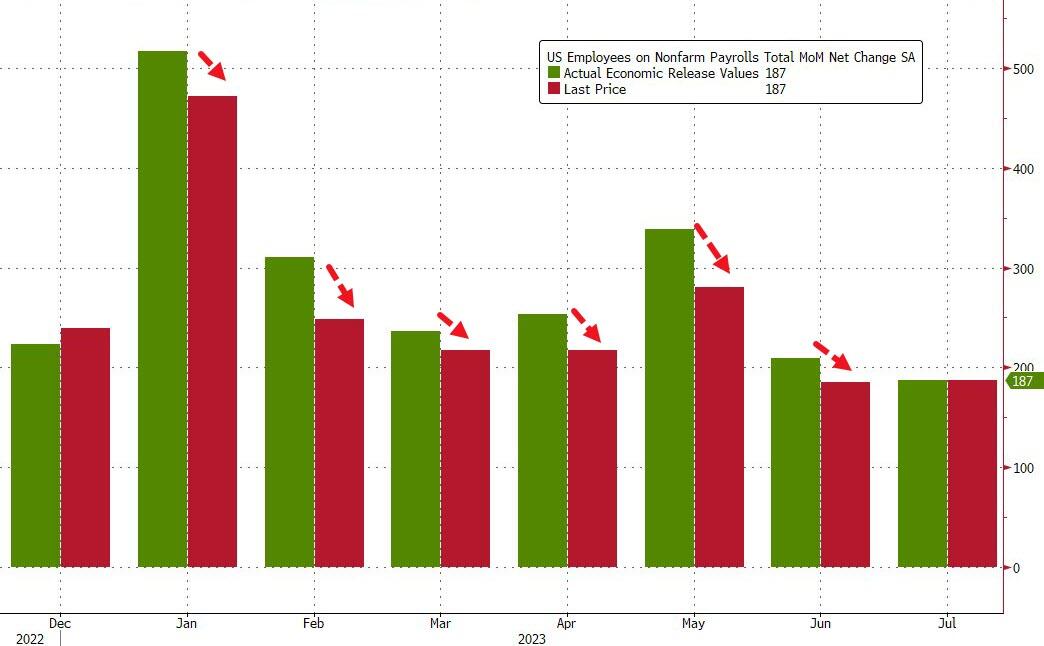

In keeping in with Biden admin’s penchant of constantly fabricating data, both May and June numbers were revised sharply lower of course:

May revised down by 25,000, from +306,000 to +281,000

June was revised down by 24,000, from +209,000 to +185,000.

To show just how ridiculous the data manipulation is, consider this chart – every monthly payrolls report in 2023 has been revised lower.

And on the disappointing jobs report and massive revisions of past data (the REAL inflation plaguing the nation is The Federal goverment lying about data), the US Treasury 2 year yield dropped like Biden on a flight of stairs.

Here are the faces of Washington DC. Lies, corruption, government for sale to highest bidder, cynacism, oppression, fear mongering, etc. This is Biden’s legacy.

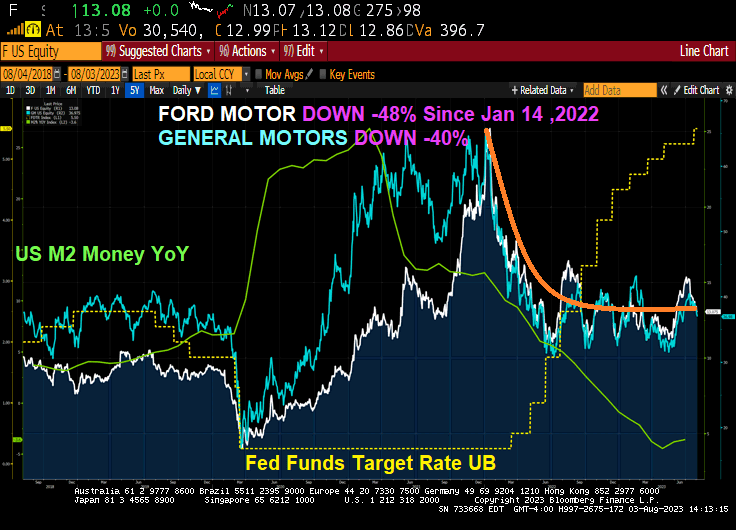

Bidenomics, the term for “Government Gone Wild! in terms of spending and EPA regulations, is a disaster for the US middle class and low wage workers. Even the 1% are now hurting if bought into Biden’s green lunacy. Ford is now down -48% since January 14, 2022 as The Fed started raising rates to fight inflation. GM is down “only” -40%.

So far this year, the division has lost $1.8 billion and this year’s $4.5 billion loss figure blows away last year’s $2.1 billion loss. Ford also announced that its electric F-150 pickup trucks will undergo a price cut, according to Fox.

Ford beat earnings on Thursday and reported adjusted EPS of $0.72, beating expectations of $0.54. It posted revenue of $45 billion and adjusted EBITDA of $3.8 billion, above estimates of $3.15 billion.

The company also raised its guidance, forecasting adjusted EBIT of $11 billion to $12 billion from $9 billion to $11 billion. The company is now guiding for free cash flow of $6.5 billion to $7 billion, from $6 billion.

But reality has sunk in about the company’s comments regarding its EV production schedule and spending plans. Price cuts in the industry, led by Elon Musk and Tesla, have thrown Ford’s production targets into a tailspin and Morgan Stanley noted on Friday morning that “major changes to the EV strategy” could be necessary, according to a wrap up by Bloomberg.

Ford now says it is “throttling back” on plans to ramp up EV production, the wrap up said. It blamed the price war for EVs as part of the cause and told shareholders it would need another year to meet its target of 600,000 EVs produced annually.

Ford CEO Jim Farley said late last week: “The shift to powerful digital experiences and breakthrough EVs is underway and going to be volatile, so being able to guide customers through and adapt to the pace of adoption are big advantages for us. Ford+ is making us more resilient, efficient and profitable, which you can see in Ford Pro’s breakout second-quarter revenue improvement (22%) and EBIT margin (15%).”

CFO John Lawler said yesterday that the company “has ample resources to simultaneously fund disciplined investment in growth and return capital to shareholders – for the latter, targeting 40% to 50% of adjusted free cash flow,” Bloomberg added. He now says Ford is “not providing a date” for producing 2 million EVs per year, which was previously the company’s target for 2026.

Is the company pulling an Intel and “kitchen sinking” its guide for the year, or has Elon Musk’s price cuts over at Tesla really put the legacy automaker on the ropes? Ford reports again on October 26, where we’ll get our next glimpse into its continuing operations this year.

Tesla is down -26% since January 14, 2022. And showing a nice turnaround!

Today, the 10-year Treasury yield is up 11 basis points.

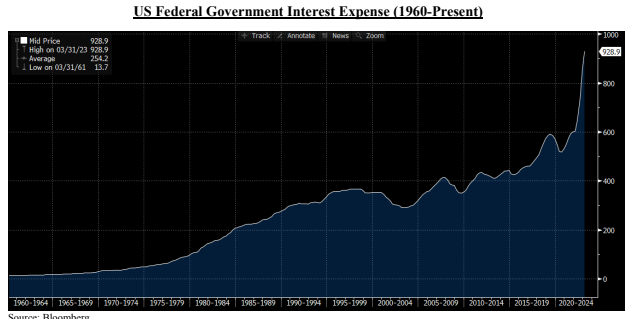

The US Fiscal position is very bad and the US is beginning to look like a third world economy. And with Biden and Democrat AGs filing indictments against Biden primary Presidential oppoonent, that country is Venezeula! Like skyrocketing interest on the Federal debt to pay for green energy hustlers and the Ukraine war.

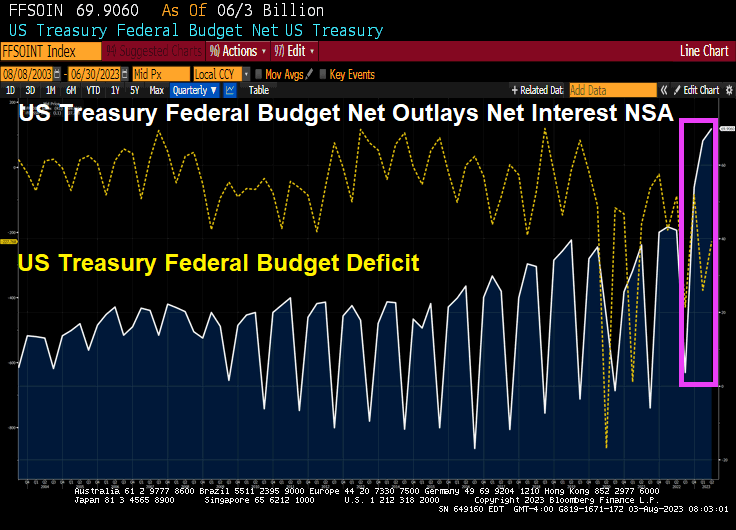

The US Federal Deficit continues to grow as seen in the charts below. A $2.25 Trillion dollar run rate deficit is significantly worse than the $1.3 Trillion that was recorded in Fiscal 2022. This level of deficit is unprecedented in an economy with low unemployment and theoretically no recession. Naturally, we ask just how big the deficit will be if we have either a recession or a crisis? In the dotcom bust, the GFC and the COVID shock, the deficit expanded massively.

Taking Garic’s math one step further, the US incurred a deficit of $1.3T in Fiscal 2022 (September). If the current run rate is sustained that would imply an annualized deficit of $2.9 Trillion.

Of course, one big driver of this deficit is the interest cost incurred by the Government itself. It is rapidly approaching a $1 Trillion dollar run rate which means the Government is spending more in interest than on national defense. As you can see in the schedule below, the Fed’s rate hiking campaign has been very expensive for the US Government since a large portion of the federal debt is in shorter maturities which currently pay ~ 5.3% in interest. As recently as September of 2021, many of these same securities had much lower interest cost – as low as only 10-30 basis points.

Looking at the chart above, we wonder: is there anything about this that looks remotely sustainable? We are at that point in the movie where raising interest rates to fight inflation actually makes things (including inflation) worse. Worse because deficits swell and will need to be monetized.

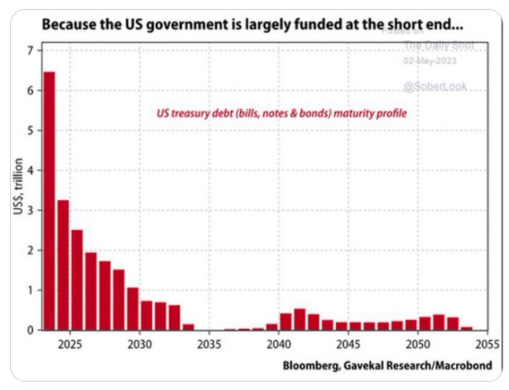

Furthermore, the issue is acute because the US Government uses the short-term bond market to Fund most of its debt. As the chart below from Gavekal Research/Macrobond shows, the Government needs to roll over $6 Trillion of maturing notes in 2023 and $3 Trillion of notes in 2024. This does not take into account any of the roughly $1.2 Trillion of bonds and notes that will be sold into the market by the Fed if Quantitative Tightening continues. Nor does it account for the ever increasing US Federal Deficit which will easily exceed $2.2 Trillion this year.

In short, the US Government has some serious funding challenges particularly when we consider that foreigners have been net sellers of our bonds since 2014.

IT’S THE DEBT, STUPID

On January 19, 2023 the US Federal Government hit its debt ceiling of $31.4 Trillion. Extraordinary spending measures kicked in which allowed the Government to keep operating. This lasted until June when Treasury Secretary Yellen informed Congress that a debt default was imminent if the ceiling was not raised.

After the usual political posturing, Congress did two things: (i) they agreed to place a two year cap on spending increases for a small portion of the budget that amounted to only 7% of the total budget. (like placing a band aid on a gaping wound); and (ii) they agreed to suspend the debt limit and to not replace it with another figure until January of 2025. We do not think they have ever.

Put it differently, let’s call this “Government Gone Wild!”

Bidenomics is where the Attorney General Garland gives Hunter Biden blanket amnesty and arrests Biden’s Presidential opponent. Welcome to the United Venezuelan States of America!e

But while Fitch cited “the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers” as reasons for the downgrade, the Biden administration is of course blaming Donald Trump and his supporters due to one portion of Fitch’s explanation: “a steady deterioration in standards of governance over the last 20 years,” and that “repeated debt-limit political standoffs and last-minute resolutions have eroded confidence in fiscal management.”

Then on Wednesday, Fitch’s Richard Francis told Reuters that the downgrade was ‘due to fiscal concerns and a deterioration in U.S governance as well as polarization which was reflected in part by the Jan. 6 insurrection.’

“It was something that we highlighted because it just is a reflection of the deterioration in governance, it’s one of many,” he said, adding “You have the debt ceiling, you have Jan. 6. Clearly, if you look at polarization with both parties … the Democrats have gone further left and Republicans further right, so the middle is kind of falling apart basically.”

And so of course, the Biden administration is blaming Trump.

“This Trump downgrade is a direct result of an extreme MAGA Republican agenda defined by chaos, callousness, and recklessness that Americans continue to reject,” said Biden re-election campaign spokesman Kevin Munoz. “Donald Trump oversaw the loss of millions of American jobs, and ballooned the deficit with the disastrous tax cuts for the wealthy and big corporations.”

Ah, so now it’s the Trump downgrade™

Meanwhile, White House spox Karine Jean-Pierre also blamed Trump on Tuesday, saying that the White House “strongly” disagrees with the decision, adding “it’s clear that extremism by Republican officials — from cheerleading default, to undermining governance and democracy, to seeking to extend deficit-busting tax giveaways for the wealthy and corporations — is a continued threat to our economy.”

Former Clinton Treasury Secretary Larry Summers called the decision “bizarre and inept,” while former Obama economic advisor Jason Furman called the move “completely absurd.”

On Wednesday, CNBC wheeled out Jared Bernstein, chair of Biden’s Council of Economic Advisers and former Obama official, who similarly blamed Trump.

“I think again the timing issue is is Jermaine here. The deficit went up every year under President Trump. The debt to GDP ratio rocketed under President trump. It has stabilized admittedly at a higher level under this president but we’re doing all we can to try to ameliorate those tensions,” he said.

Bernstein reflected on the “cognitive dissonance” he felt at the downgrade amid the success of ‘Bidenomics’ commenting that “creditworthiness deteriorated significantly under President Trump for good reasons… and under President Biden, it started to track back up…”

Except that’s the exact opposite of what happened. According to the 100% non-partisan “market”, the creditworthiness of US Treasury debt improved almost constantly under President Trump and worsened dramatically almost immediately upon President Biden’s inauguration:

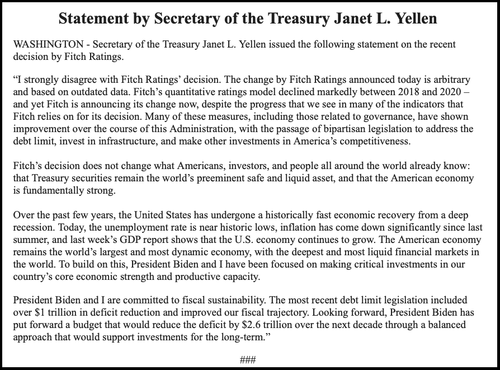

Treasury Secretary Janet Yellen said that the downgrade was “arbitrary and based on outdated data,” adding “Today, the unemployment rate is near historic lows, inflation has come down significantly since last summer, and last week’s GDP report shows that the U.S. economy continues to grow.”

CNN also blamed Trump, penning the headline: Fitch downgrades US debt on debt ceiling drama and Jan. 6 insurrection.”

The stupidity on CNN and Jared Bernstein are appalling. True, the media and Biden Administration are terrified of losing the 2024 Presidential election, but outright lies and misrepresenation are wrong no matter what.

But the claims that the US was downgraded because Trump’s economy lost miilions of jobs is ridiculous.

Actually, the US economy added 12.53 million jobs after April 2020 (Trump) while Bidenomics created took 2 1/2 years to add 12.56 million jobs. So, Biden took over twice as long to create jobs after Covid than it did under Trump. Simply opening the economy and schools produced that magical claim by Biden. And the National Teacher’s Union and Randi Weingarten worked with Fauci to orchestrate shutting down schools. Blaming Trump for local governments shutting down the economy is pure bunk.

Bidenomics and massive Federal spending is the cause for the downgrade. Not Trump.

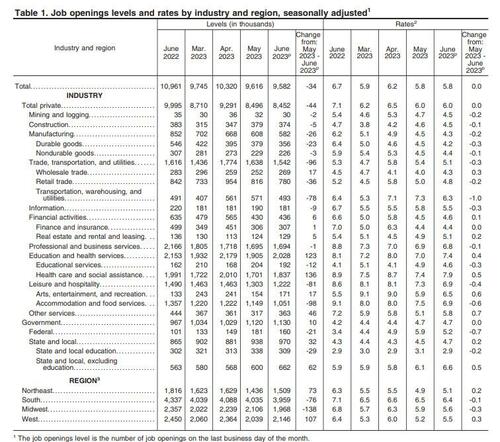

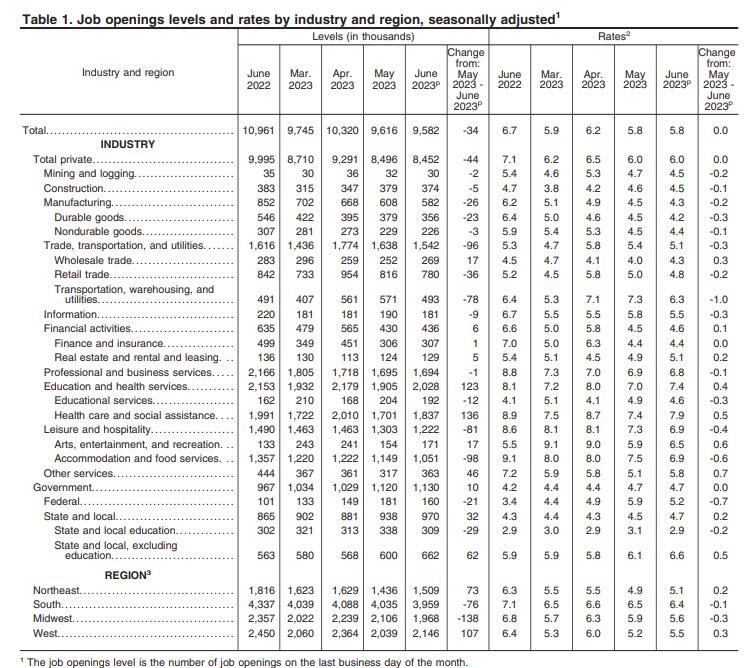

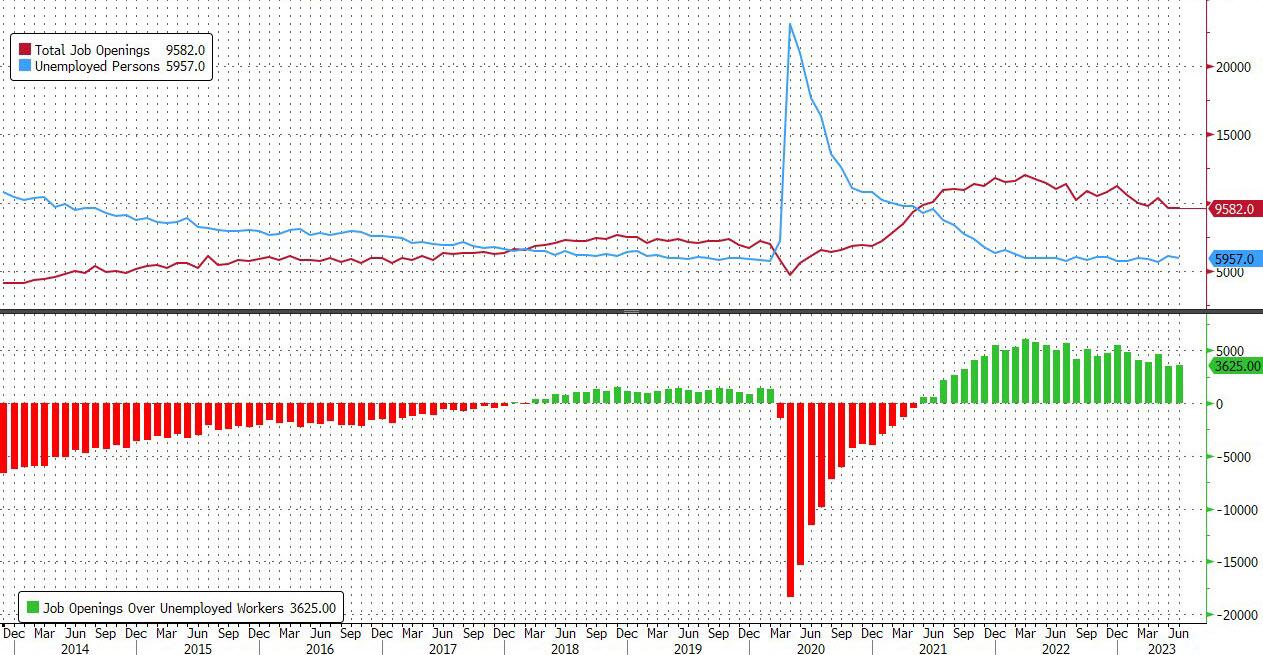

The number was about 1.4 million below the 11 million from a year ago and below the consensus estimate of 9.6 million, a rare miss in a series which has been best known for decisively beating Wall Street’s expectations.

According to the BLS, the largest increases in job openings was in health care and social assistance (+136,000) and in state and local government, excluding education (+62,000). Job openings decreased in transportation, warehousing, and utilities (-78,000), state and local government education (-29,000), and federal government (-21,000)

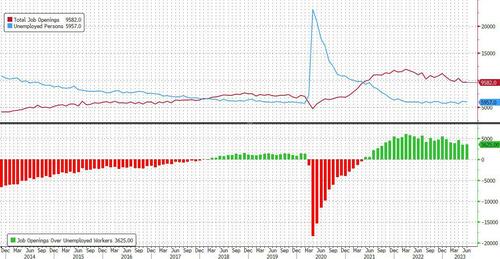

The slide in the number of job openings meant that after rising to the highest since January 2023 in April, in June the number of job openings was just 3.7625 million more than the number of unemployed workers, the lowest since Sept 2021.

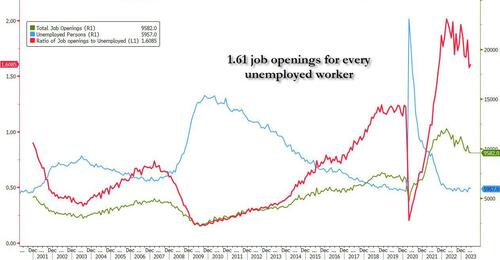

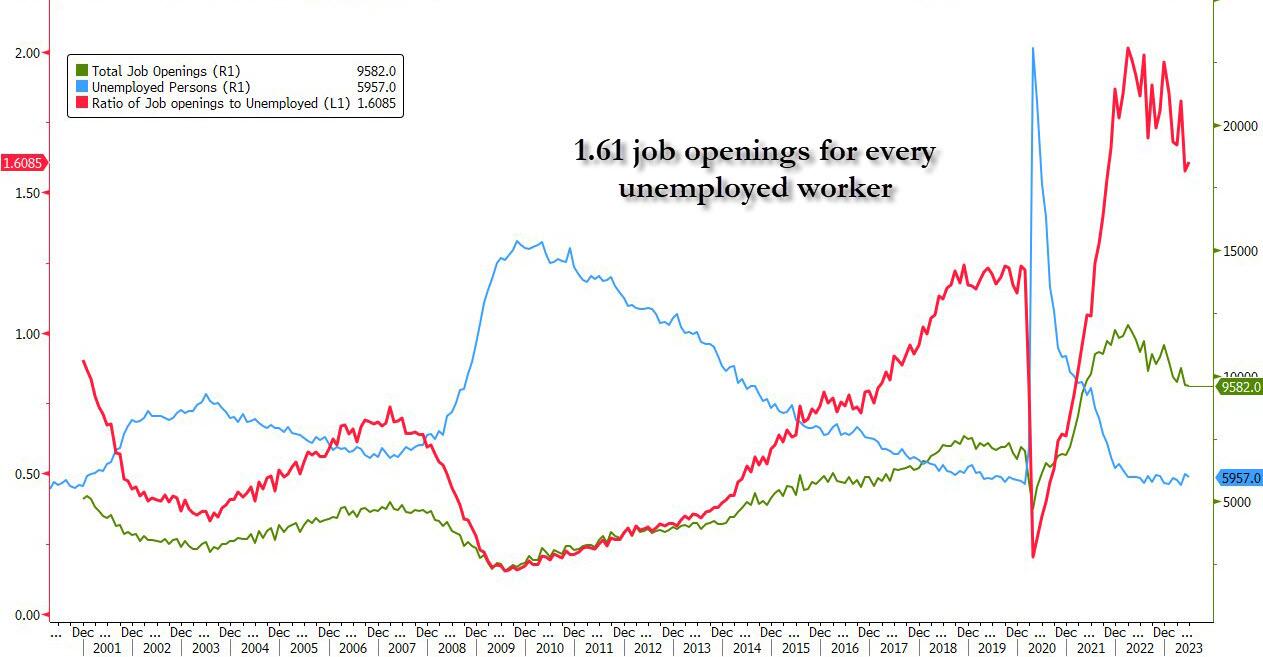

Said otherwise, after rising to 1.82 openings for every worker in April, in June the number dropped to just 1.61, which would have been the lowest level since Oct 2021 if it weren’t for last month’s sharp downward revision.

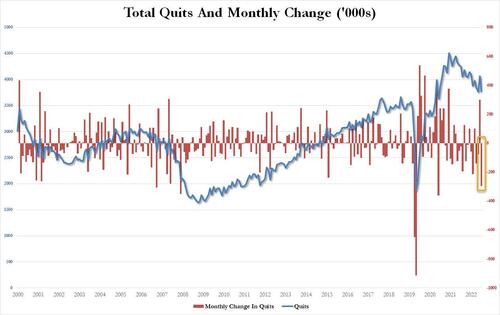

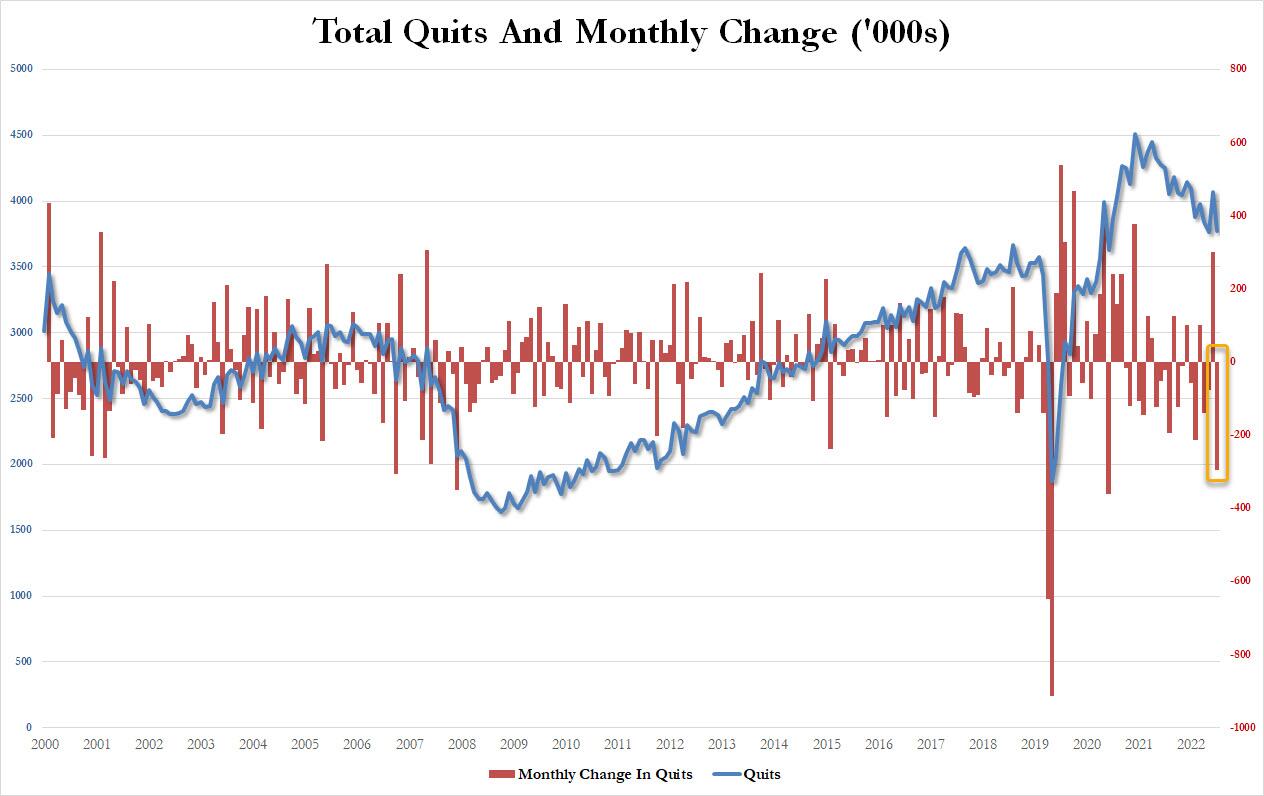

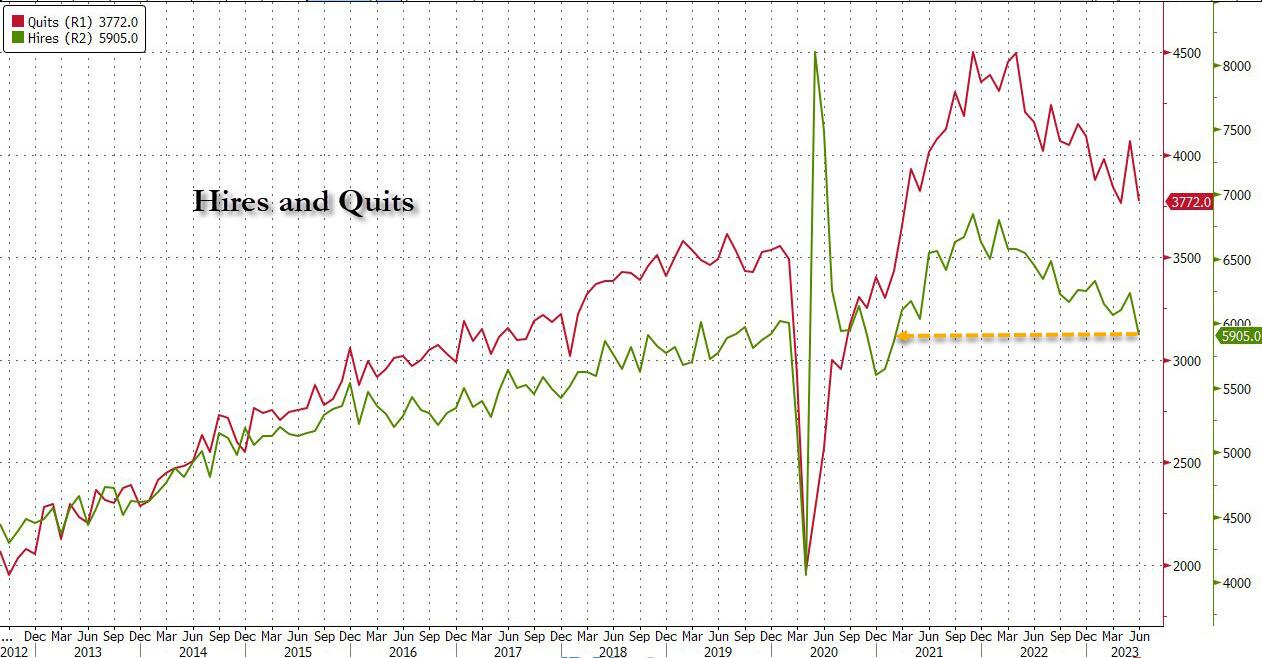

Yet even as the number of job openings dropped only modestly from the (sharply) downward revised print for May (because under Biden, no number is ever revised stronger), conflicting data remained and in June, the number of people quitting their jobs – an indicator traditionally associated with labor market strength as it shows workers are confident they can find a better wage elsewhere – unexpectedly tumbled by 295K to just 3.772MM, the biggest monthly drop since May 2021.

According to the BLS, the number of quits decreased in several industries, with the largest decreases in retail trade (-95,000), health care and social assistance (-75,000), and construction (-51,000). The number of quits increased in arts, entertainment, and recreation (+20,000).

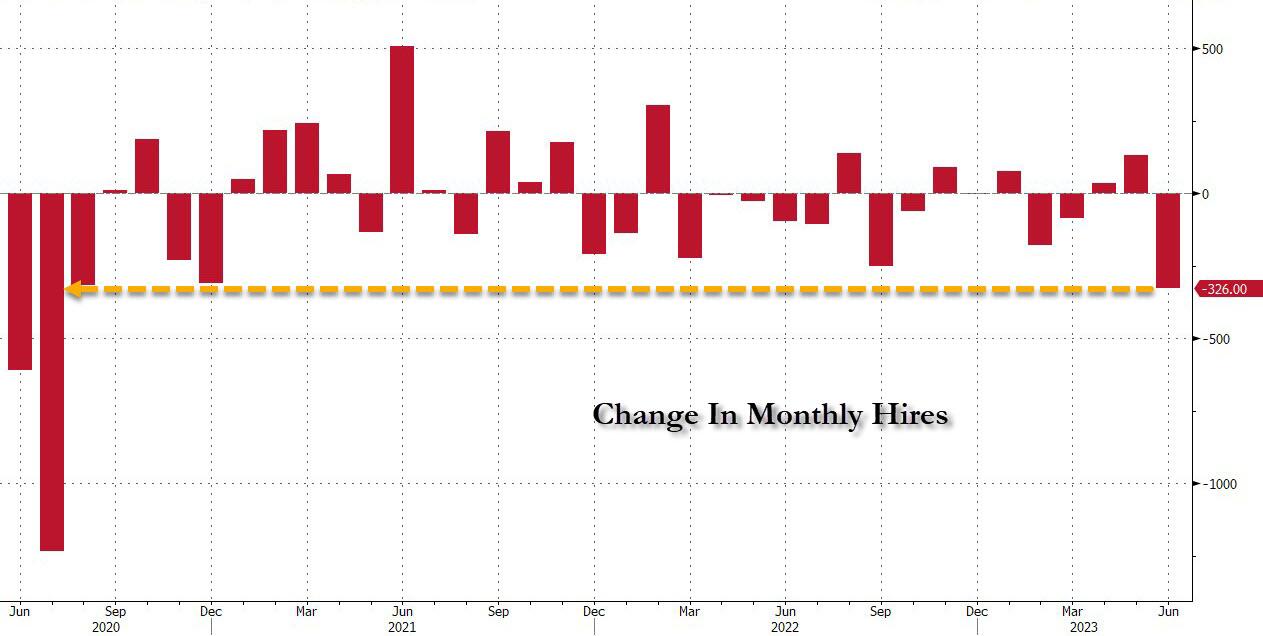

And just in case some still believe Biden’s strong jobs lie, the number of hires also tumbled in June, crashing by 326K – the biggest monthly drop since July 2020…

… to 5.905MM, the lowest since February 2021.

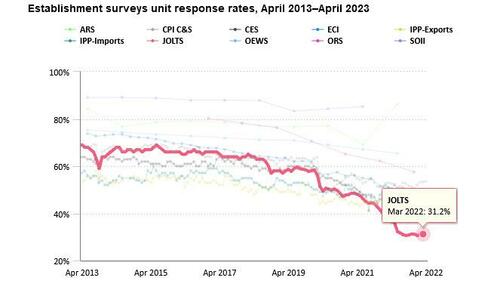

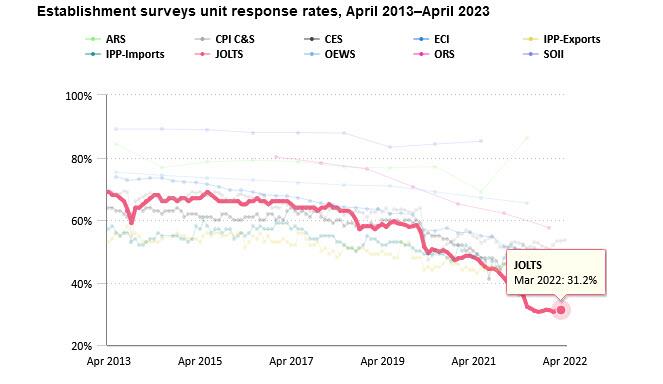

Of course, as we have explained on multiple occasions previously, none of the above data actually matters or is credible for the simple reason that the response rate of the JOLTS survey is stuck at a record low 31.2%. Which means that only those who actually have job openings to report do so, while two-thirds of employers are either non-responsive or their mail is quietly lost in the mail.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.