Well, the Trump/Biden CNN Presidential debate was a disaster … for Biden. It was the worst debate performance I have even seen. Even worse was the “victory” party where Jill Biden treated President Biden like a little child being potty-trained and shreiked that all Trump does is L:IED. How strange since ALL Biden does is lie. But enough of this.

But how about SuperCore inflation?

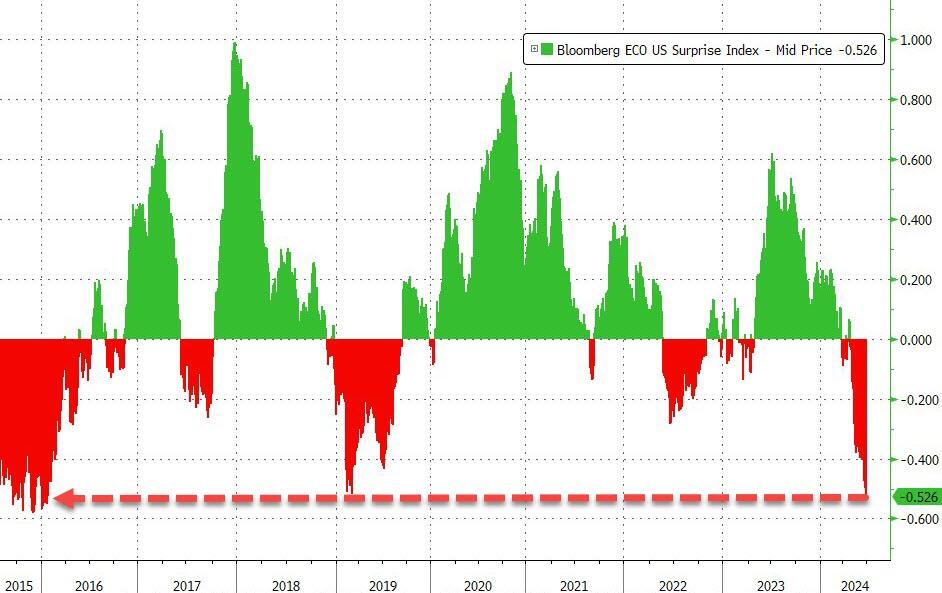

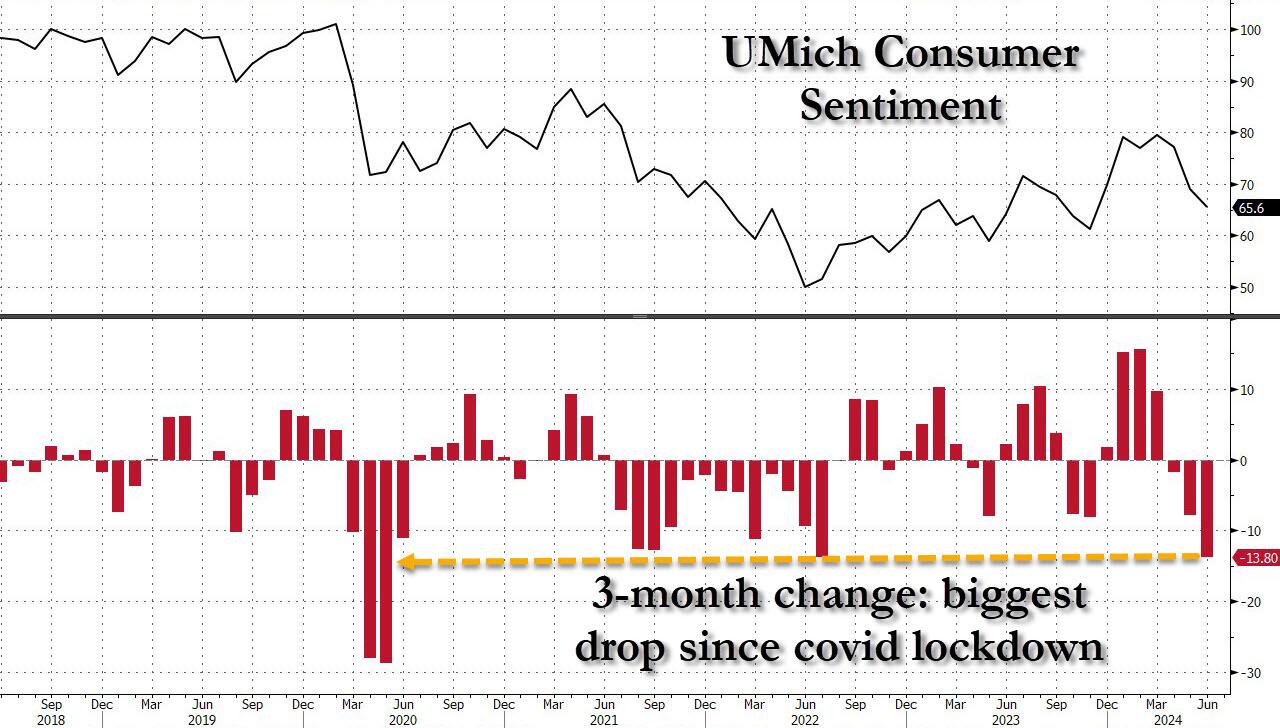

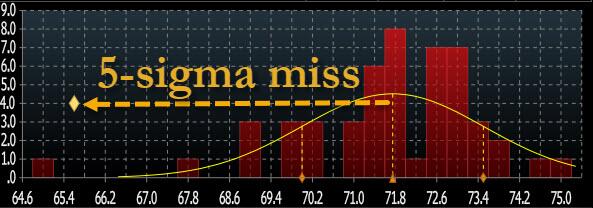

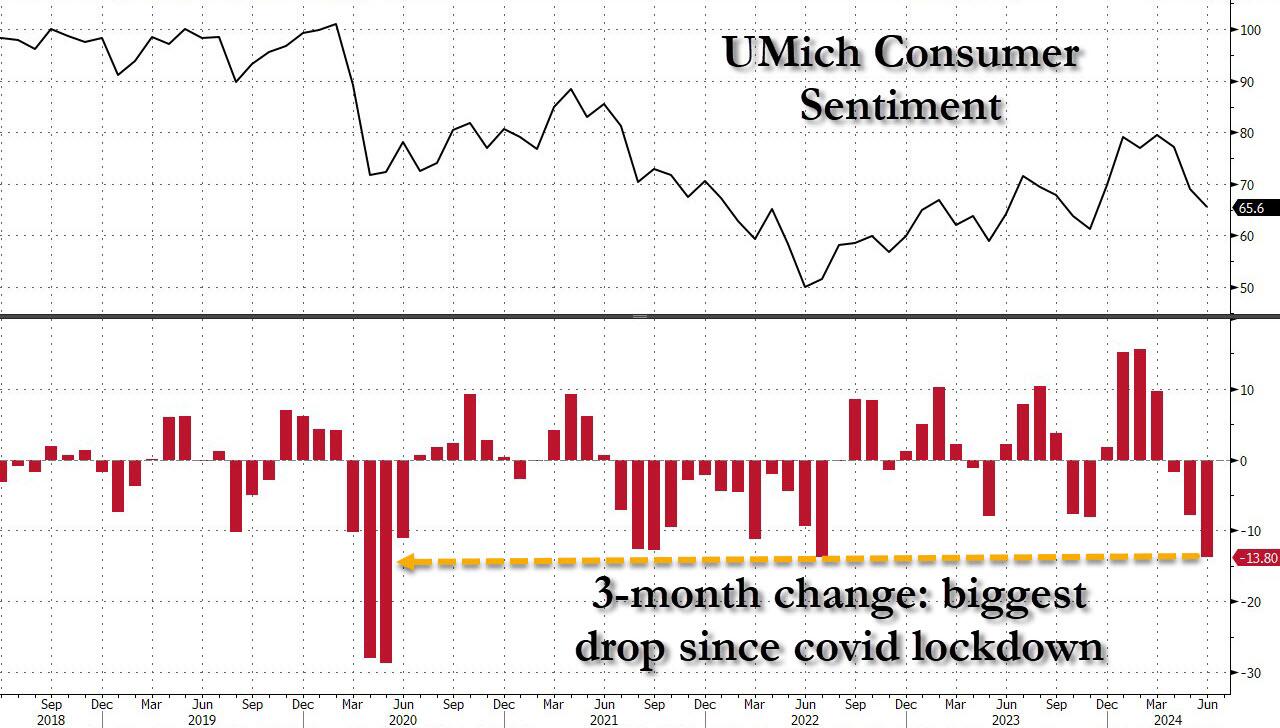

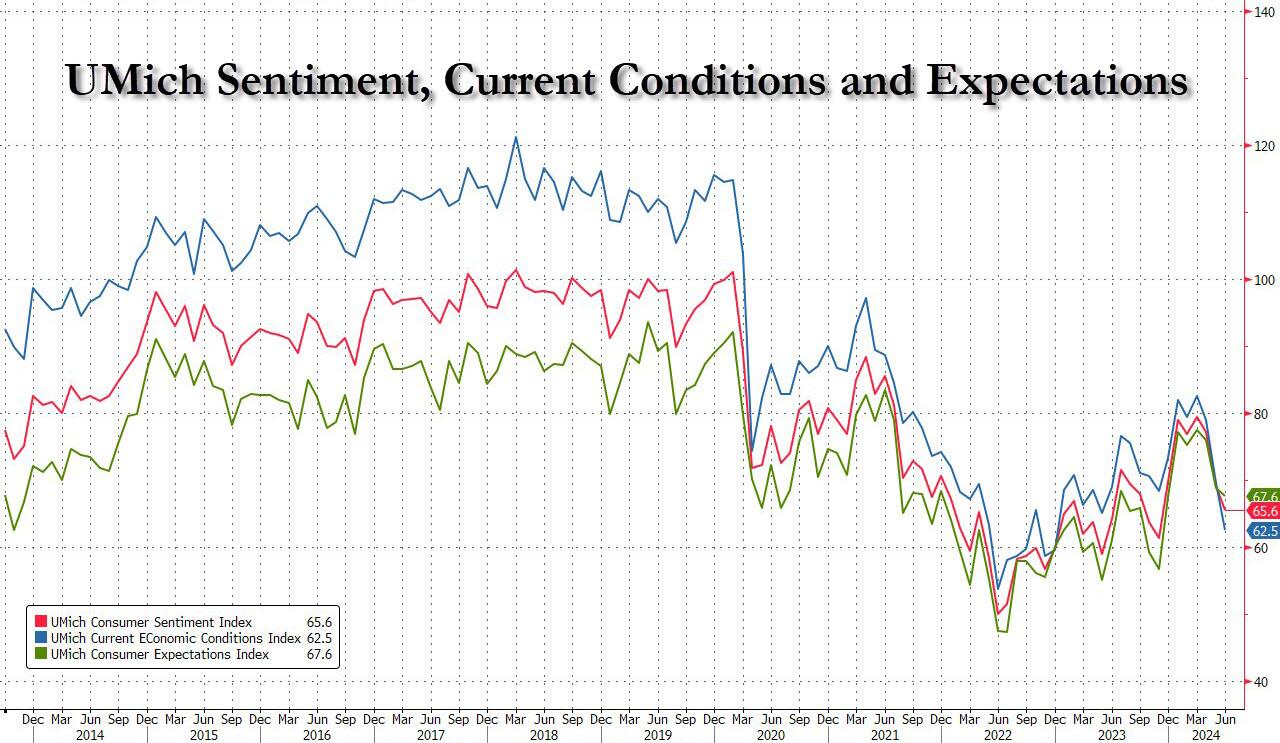

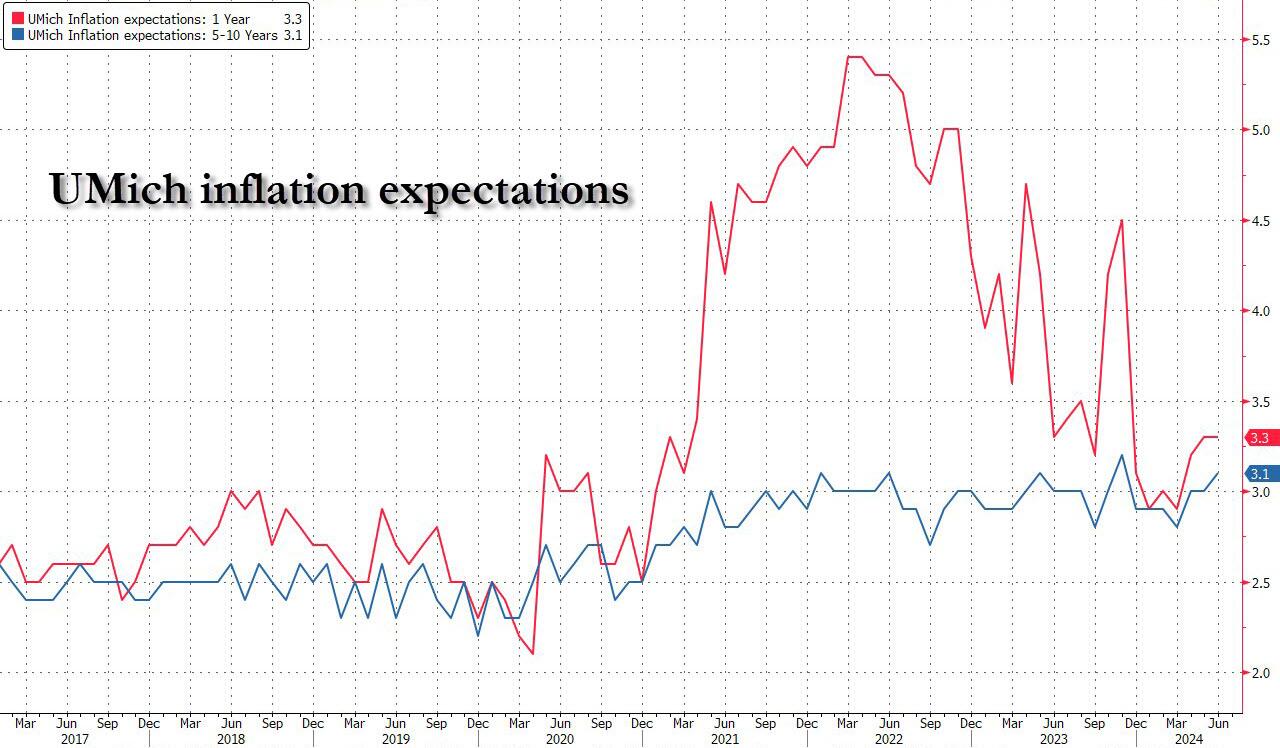

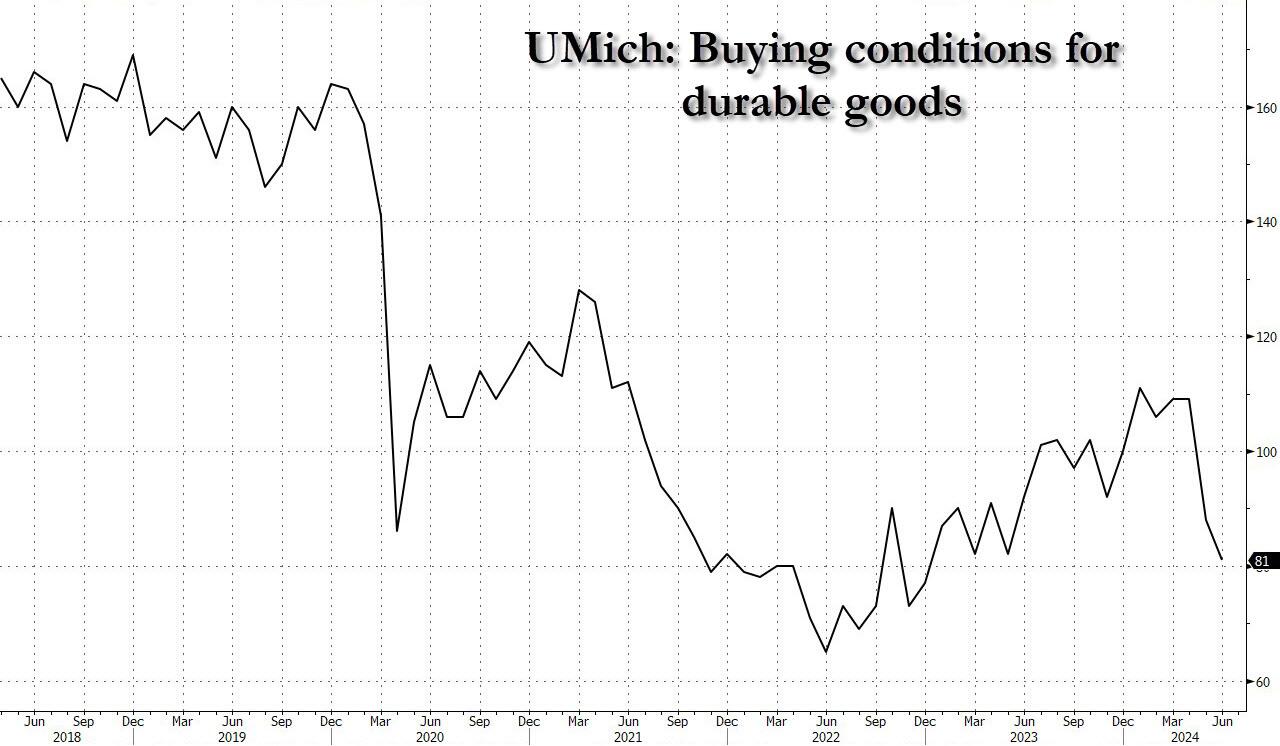

The last month has seen US Macro data collapsing at its fastest rate in years…

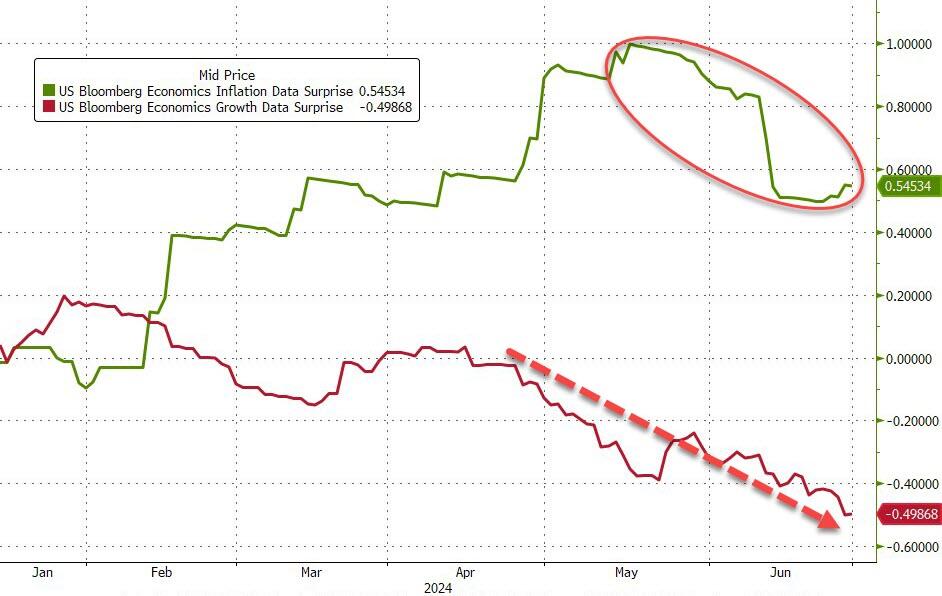

…which, many believe, will also drag down inflation (and it has been)…

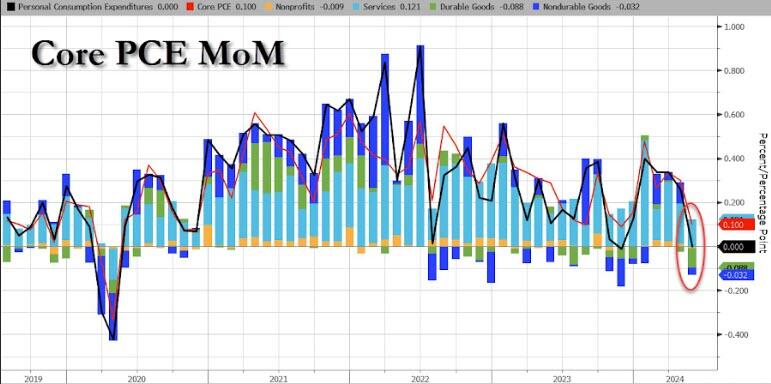

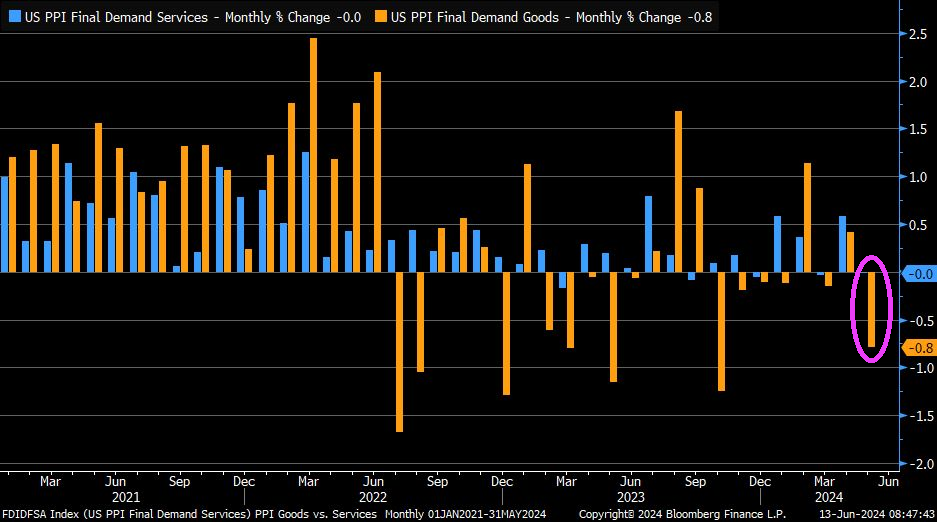

Today, we get to see The Fed’s favorite inflation indicator – Core PCE – which rose 0.1% MoM in May (after a revised +0.3% MoM for April) and in line with expectations. The headline PCE Price Index was unchanged MoM as expected as Durable Goods deflation trumped surging Services costs…

On a YoY basis, both headline and core PCE declined…

On a YoY basis, Durable Goods deflation is at its strongest in at least a decade…

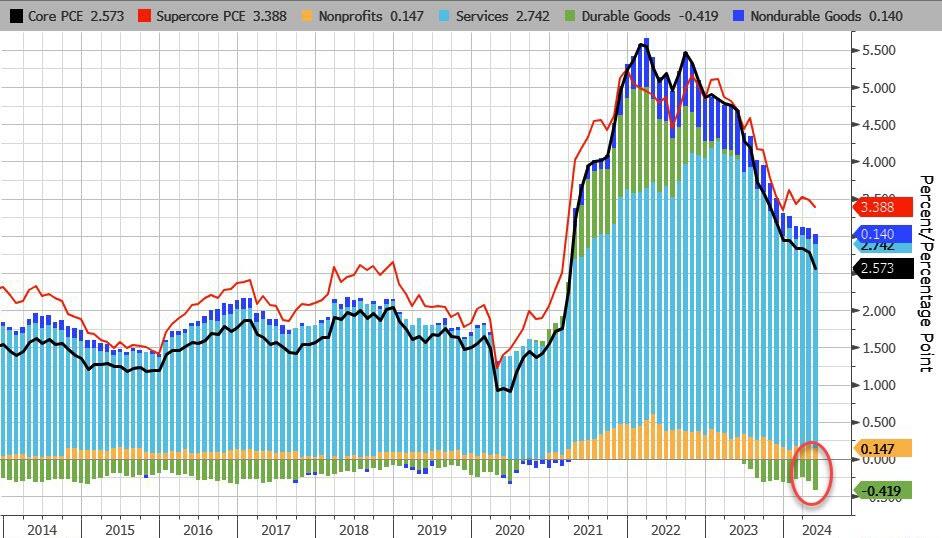

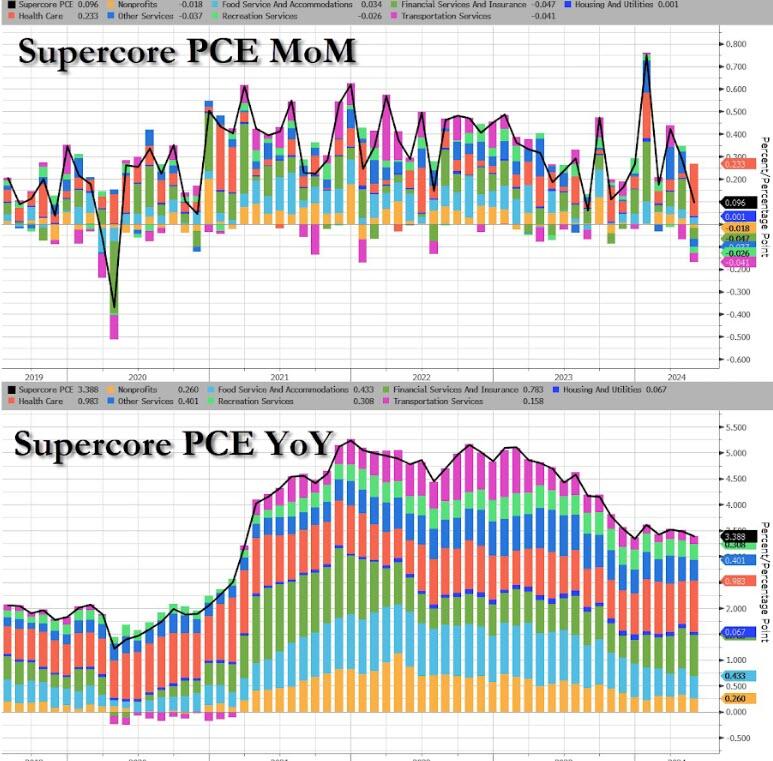

More notably, the so-called SuperCore PCE rose 0.1% MoM, which saw YoY slow to 3.39%… which is awkwardly stagnant at elevated levels…

That is the 49th straight monthly rise in SuperCore prices with Healthcare costs soaring…

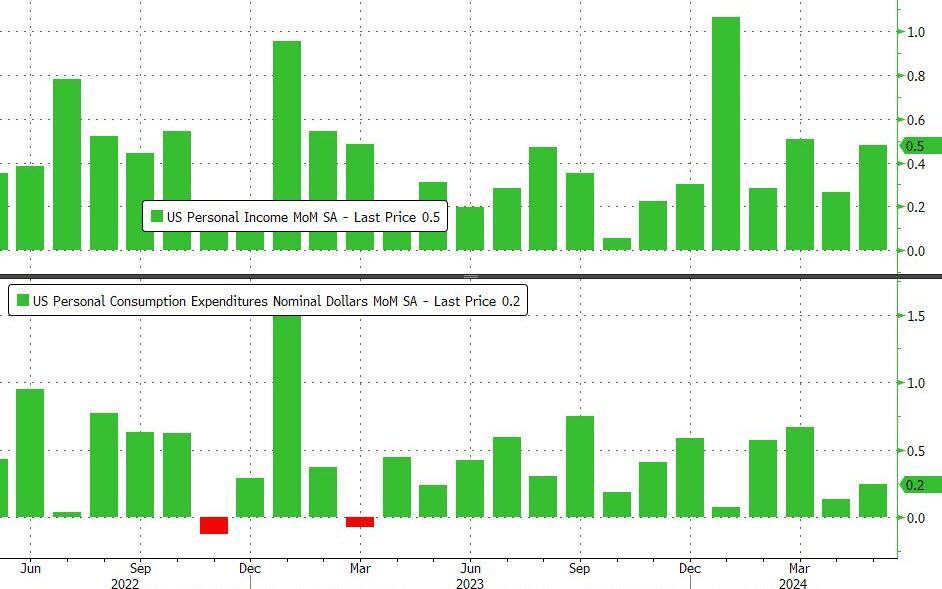

On a MoM basis, Income grew more than expected (+0.5% vs +0.2% exp) while spending rose less than expected (+0.2% MoM vs +0.3% exp)

Which accelerated both income and spending on a YoY basis (with the latter outpacing the former, of course)…

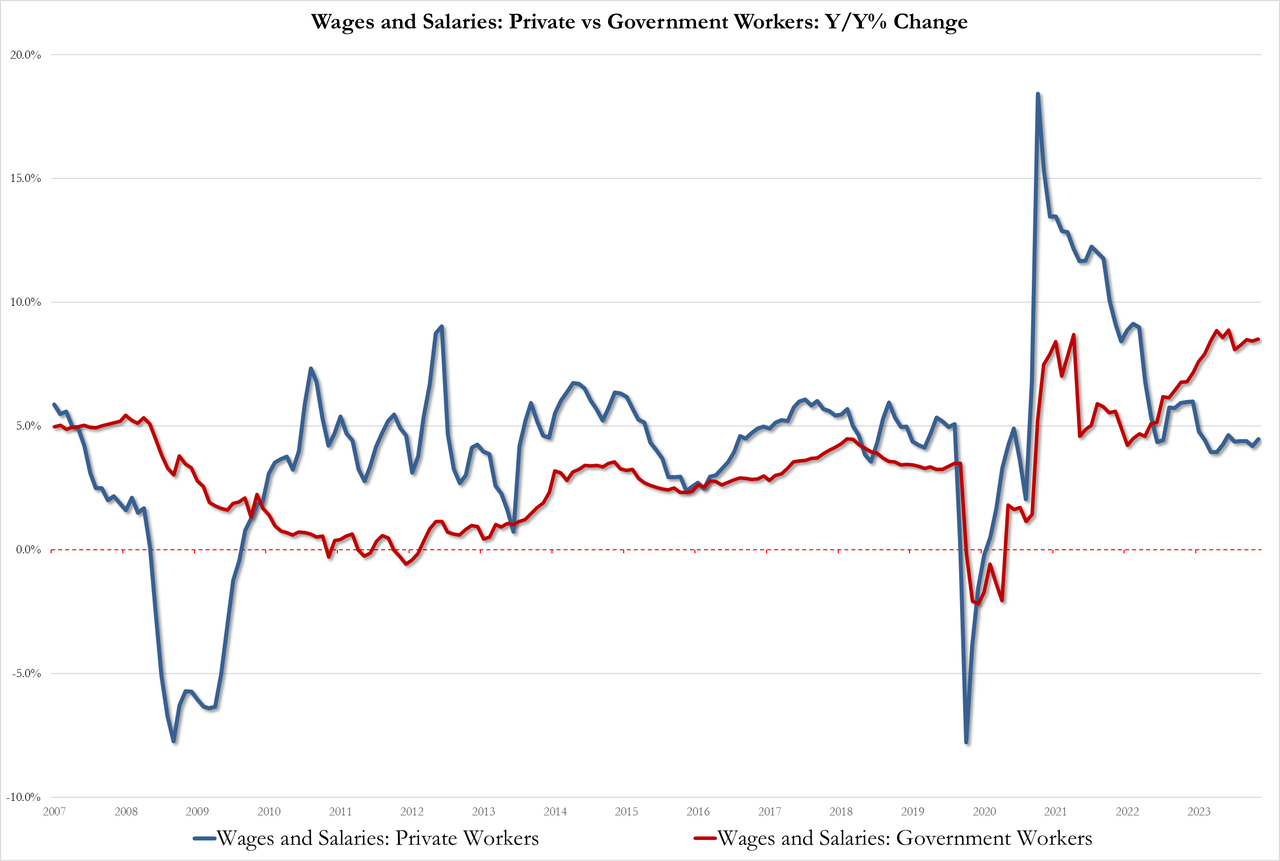

With wage pressures rising once again…

- Government 8.5%, up from 8.4% but below the record high of 8.9%

- Private 4.5% up from 4.2%

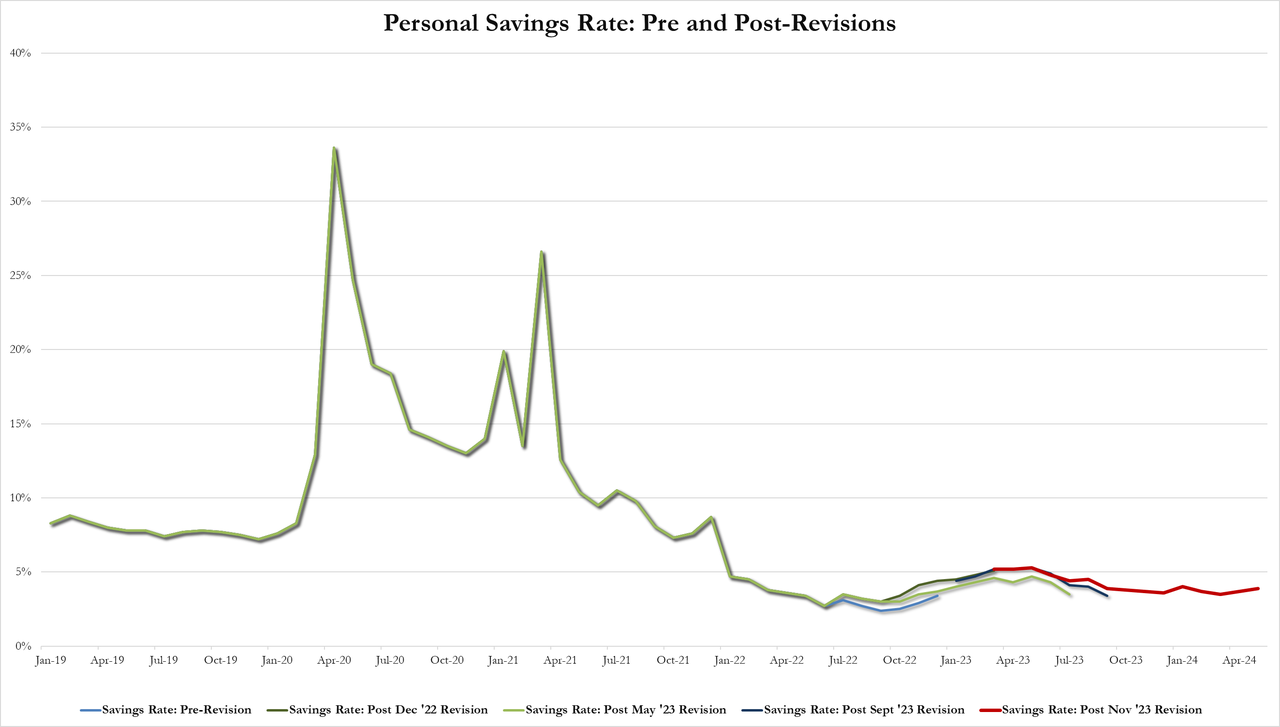

And after a series of revisions, the savings rate ticked up to 3.9% of DPI (from 3.7%) – the highest since January…

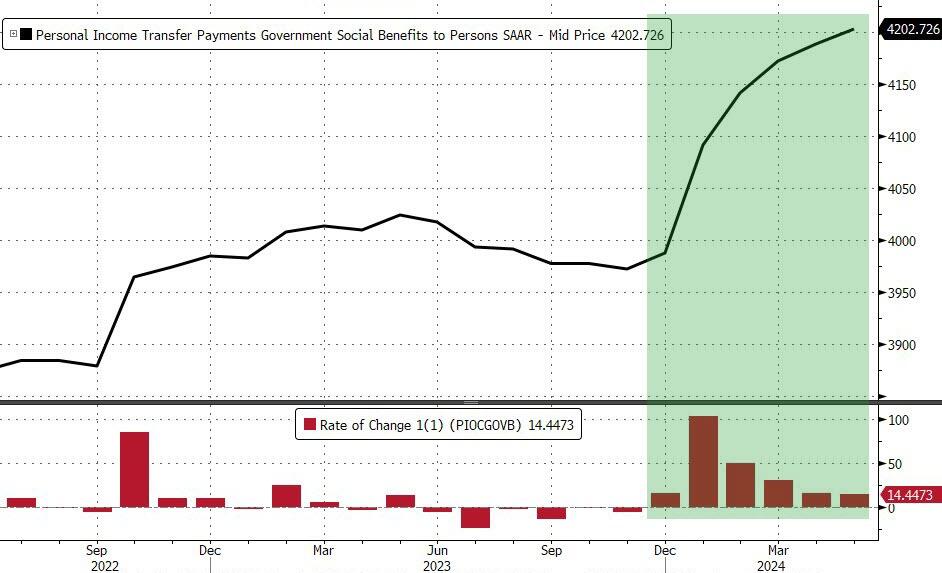

All of which takes place against a background of the sixth straight month of rising government handouts (well it is an election year after all)…

Finally, while acyclical inflationary pressures continue to drift lower, cyclical inflationary pressures remain extremely elevated…

A very mixed bag but nothing screams ‘automatic’ rate-cuts… and SuperCore refuses to budge.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.