While some economists are cheering the post-COVID economic recovery, I am not among them. Rampant inflation and bad economic policies are plaguing the non 1% of the population.

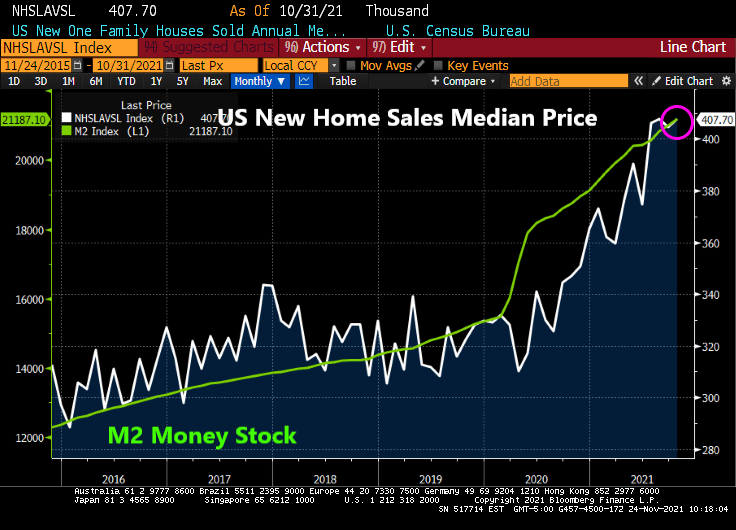

For example, new home sales dropped -23.1% YoY in October. As consumer sentiment for housing crashed to 63 (baseline of 100).

Why are consumers bummed-out about buying housing? How about rapidly accelerating new home prices???

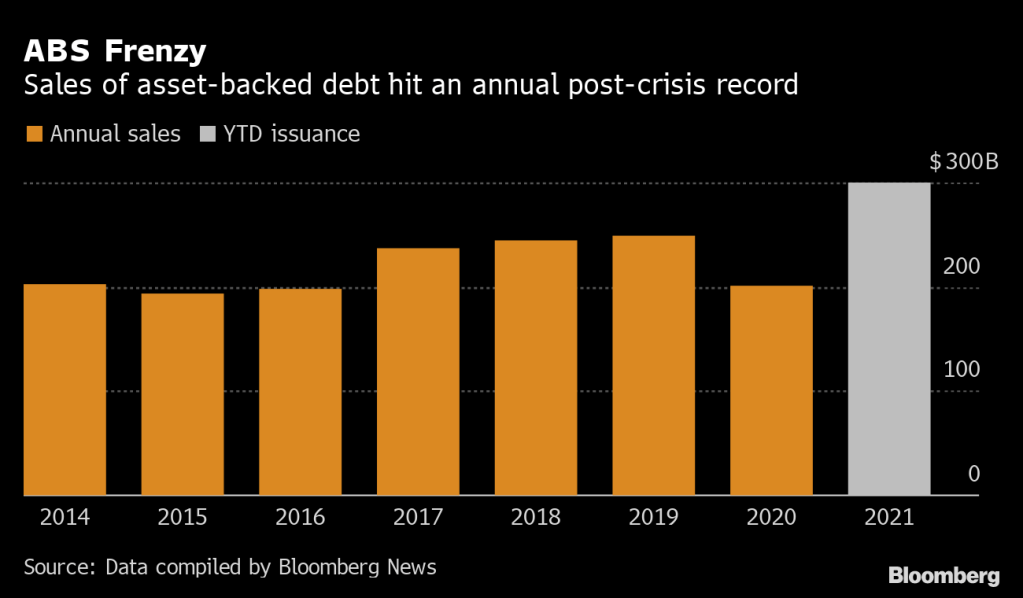

I remember the surge in securitization of loans, receivables, etc during the housing bubble of the mid-to-late 2000s. Today seems like 2007 all over again.

(Bloomberg) — Bankers are repackaging everything from fast food franchises to fitness-center fees into bonds at the fastest clip since the global financial crisis as investors chase yield and inflation protection.

This year’s sales of U.S. asset-backed securities have already surpassed $300 billion, according to data compiled by Bloomberg — and more is expected by year-end. Post-crisis issuance records have also been set in private-label commercial mortgage bonds and collateralized loan obligations, which are also seen accelerating.

“Solar, consumer loans, container lease and whole business transactions to some degree all offer attractive yields and spreads,” said Dave Goodson, head of securitized credit at Voya Investment Management. “These so-called esoteric sectors remain well supported with plenty of money to invest.”

On Monday, Self Esteem Brands, a franchiser of businesses including its flagship gyms Anytime Fitness, priced a $505 million ABS that was backed by franchise agreements, royalties and fees. In whole business securitizations like these, companies mortgage virtually all their assets.

Last month, fried chicken restaurant chain Church’s Chicken sold a $250 million securitization backed by franchise and royalty collateral. Golden Pear Funding recently securitized litigation fees related to financial settlements on everything from personal injury cases to wrongful convictions. And Oasis Financial priced a similar deal linked to payments on medical liens.

Then we have this headline that will send chills through the CMBS market for retail space, particularly at a time when commercial real estate (particularly RETAIL) are trying to recover from COVID lockdowns and the growth of online shopping.

“Retailers Sound Alarm on Organized Theft as States Warn of Rise”

Retailers say shoplifting is getting more brazen in the U.S.: A California Nordstrom store was recently hit by a flash mob of more than 80 people who made off with designer goods, while more than a dozen people pilfered from a Louis Vuitton location in a suburb of Chicago.

On Tuesday, the impact of shoplifting reached Wall Street, with Best Buy Co. shares plunging after the electronics retailer said widespread theft contributed to a decrease in one gauge of profitability. Last month, Walgreens said it would close five San Francisco stores after theft rates there spiked.

Seemingly, no one learns from history. Or as the zen master Yogi Berra once said “It’s like déjà vu all over again.”

Or “You better cut the pizza in four pieces because I’m not hungry enough to eat six.”

President Biden nominated Jerome Powell for a second term as Fed Chair and nominated Lael Brainard as Deputy Chair to replace Richard Clarida. The US House of Overlords (aka, the US Senate) will hold hearings on the nominees (with Elizabeth Warren opposing Powell and supporting Brainard’s nomination).

Treasury yields jumped and U.S. index futures signaled a continued selloff in technology shares as traders pruned bets for a dovish-for-longer Federal Reserve after the renomination of Jerome Powell as its chair.

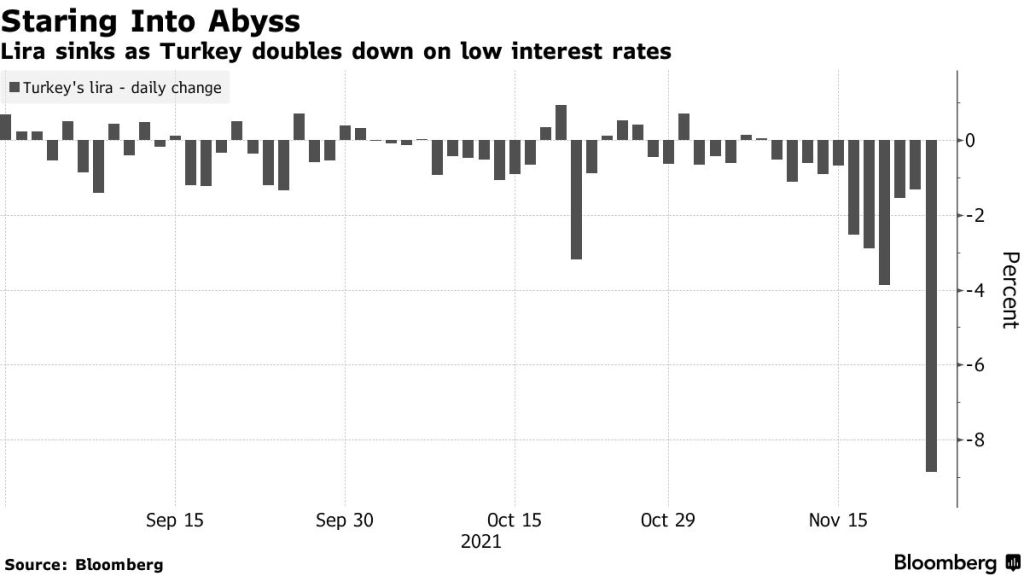

Contracts on the Nasdaq 100 Index fell 0.3% after Monday’s last-hour selloff in technology stocks. The subgroup was the worst performer in Europe Tuesday, sending the region’s benchmark to a three-week low. A currency crisis deepened in Turkey, with the lira weakening past 13 per U.S. dollar. Zoom Video Communications Inc. lost 9% in premarket trading on slowing growth.

Investors are reducing expectations for a deeper dovish stance by the Fed after Powell was selected for a second term. The chair himself sought to strike a balance in his policy approach saying the central bank would use tools at its disposal to support the economy as well as to prevent inflation from becoming entrenched.

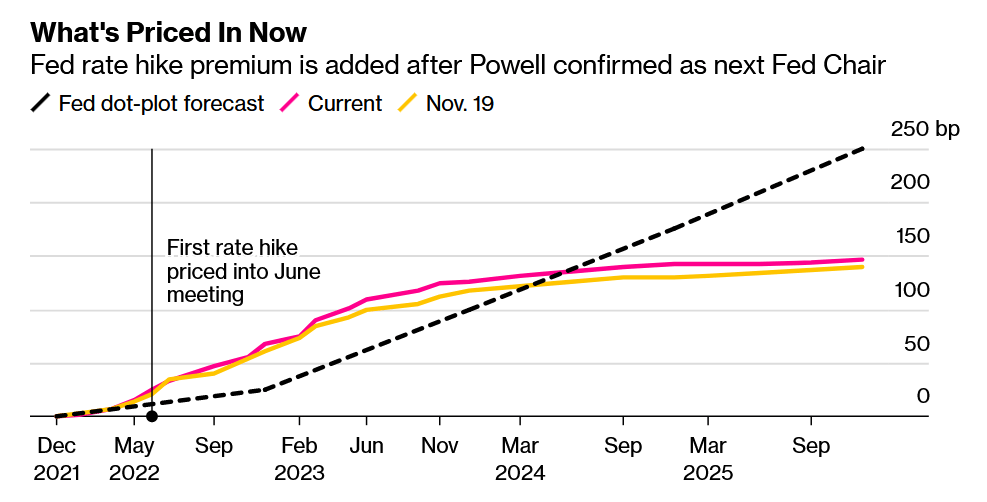

Fed rate hike premium is added after Powell confirmed as next Fed Chair:

Change in Fed’s interest-rate target implied by overnight index swaps and eurodollar futures.

Fed Bank of Atlanta President Raphael Bostic said Monday the U.S. central bank may need to speed up the removal of monetary stimulus and allow for an earlier-than-planned increase in interest rates.

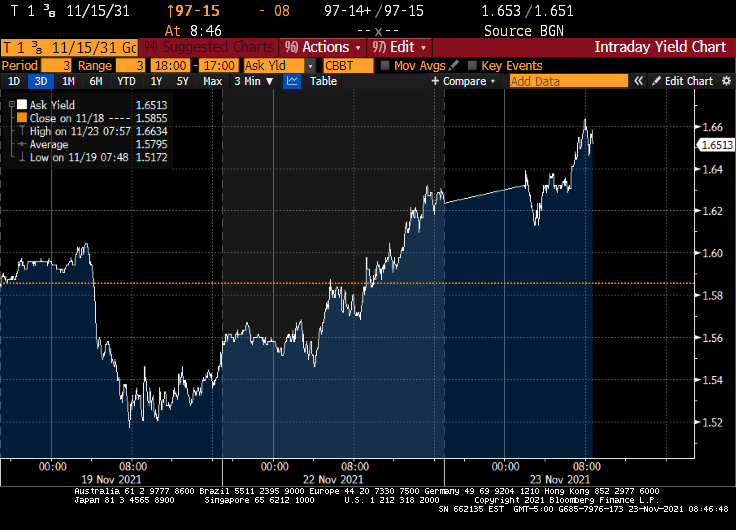

Translation: Markets are pricing in MORE hawkish Powell over uber-dove Brainard. The 10-year Treasury yield has risen from 1.52% to 1.65%

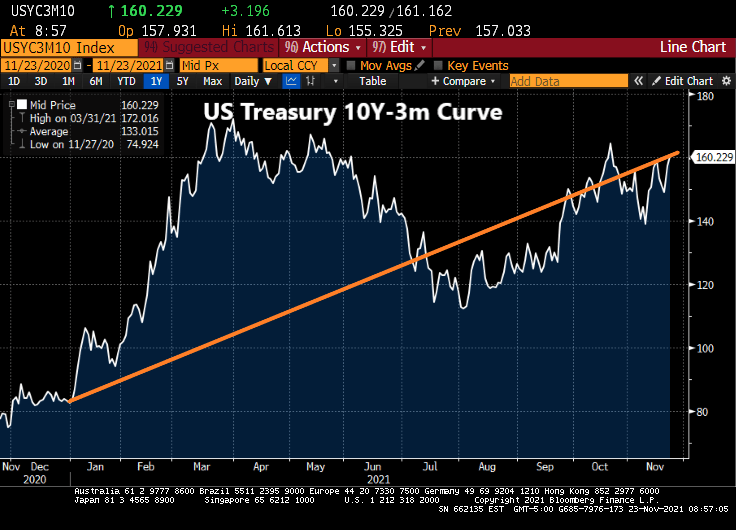

And the 10Y-3M Treasury curve has risen from 83 basis points at the beginning of 2021 to 160 basis points today. I will this the Biden Inflation Effect (BIE).

Let’s see if Powell & Company deliver on removing the excessive stimulus from the market, particularly with midterm elections approaching.

To quote Gomer Pyle USMC, “Surprise, surprise, surprise!”

The humongous spending bill awaiting Joe Manchin to sign off on it will cost almost double what the CBO said it would. Why? Because spending programs in Washington DC never get cancelled, they only grow.

“We estimate the House Build Back Better Act includes roughly $2.4 trillion of spending and tax cuts along with roughly $2.2 trillion of offsets.However, the bill relies on a number of sunsets and expirations to keep the official cost down. If the plan’s temporary policies were made permanent, we find the cost would increase by as much as $2.5 trillion.As a result, the gross cost of the bill would more than double from $2.4 trillion to $4.9 trillion.

The Build Back Better Act relies on a number of arbitrary sunsets and expirations to lower the official cost of the bill. These include extending the American Rescue Plan’s Child Tax Credit (CTC) increase and Earned Income Tax Credit (EITC) expansion for a year, setting universal pre-K and child care subsidies to expire after six years, making the Affordable Care Act (ACA) expansions available through 2025, delaying the requirement that businesses amortize research and experimentation (R&E) costs until 2026, and setting several other provisions – from targeted tax credits to school lunch programs – to expire prematurely.

Excluding changes to the state and local tax (SALT) deduction, we estimate the Build Back Better Act would cost $2.1 trillion as written. We estimate making all of these temporary policies permanent would cost roughly $2.2 trillion, more than doubling the gross cost of the bill to $4.3 trillion through 2031.”

When asked about the Center for a Responsible Budget saying the bill could be twice as expensive, Manchin replies “it’s concerning. Sure. It’s concerning.”

Surprise, surprise, surprise! And it is certainly more expensive than the estimate Biden gave: $0.

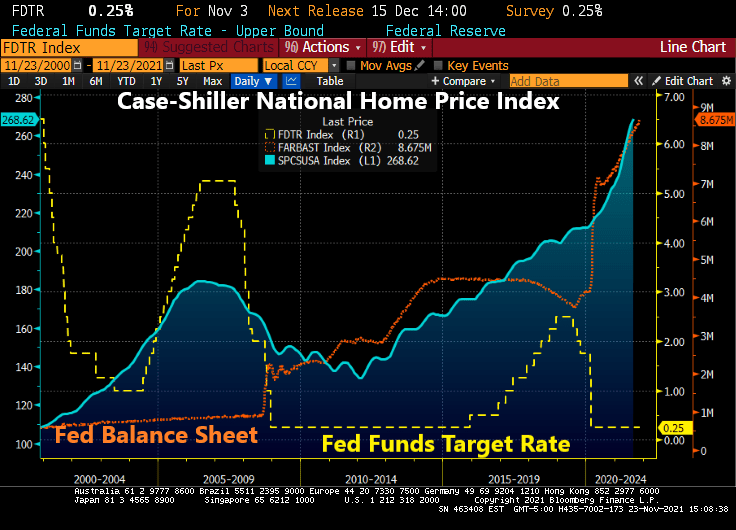

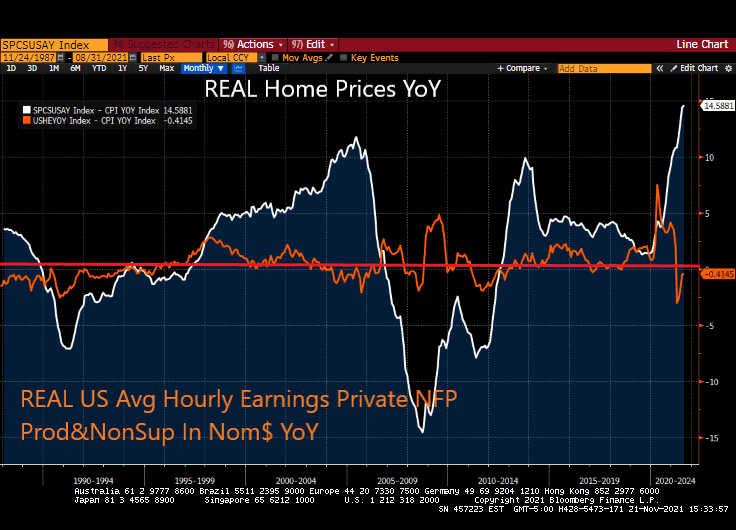

Welcome to The Fed’s Gilded Age … for housing! The gilded age refers to the thin-veneer of gold covering up problems in the late 1800s.

Today’s gilded age is largely fueled by The Federal Reserve’s uber-easy monetary policies combined with absurd Federal government policies. The result? Thanks to inflation, REAL home prices are growing at 14.6% YoY while REAL hourly earnings are declining (-0.41% YoY).

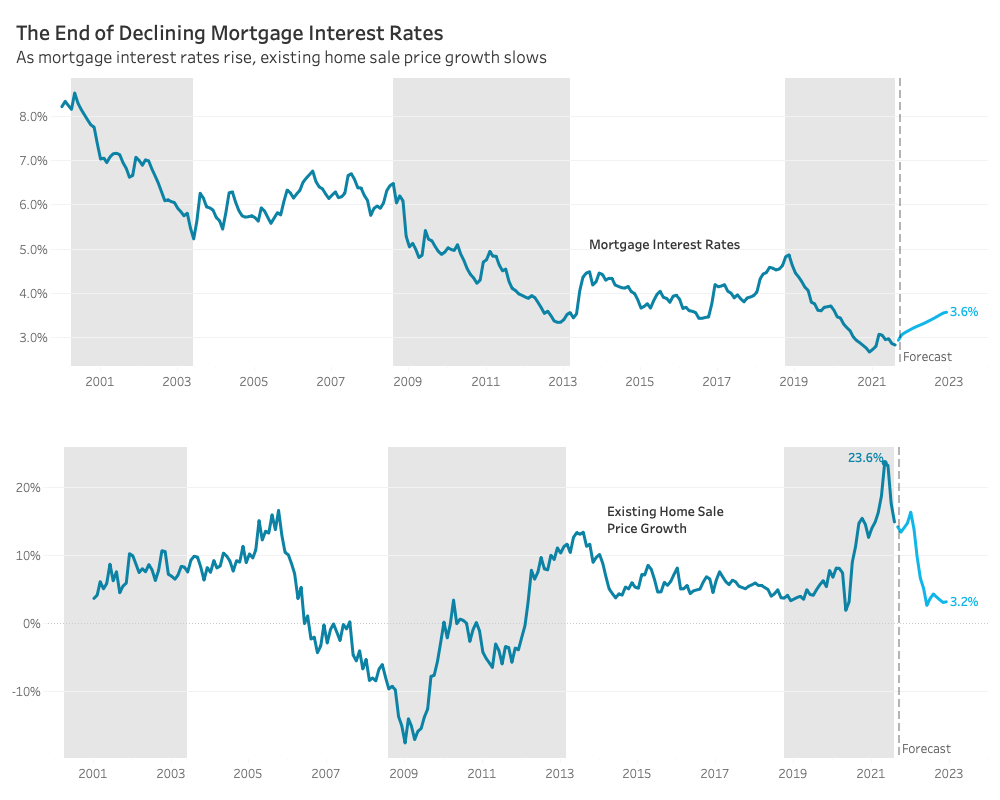

Redfin predicts a more balanced housing market in 2022. Part of their rationale is that they predict mortgage rates will rise to 3.6%. This growth in the mortgage rate is predicted to slow home price growth to 3.2% from double digit growth currently.

While this scenario is plausible, it will require a change in direction of the 10-year Treasury yield which has been declining since 1981. 5.39% YoY inflation may encourage The Fed to raise rates.

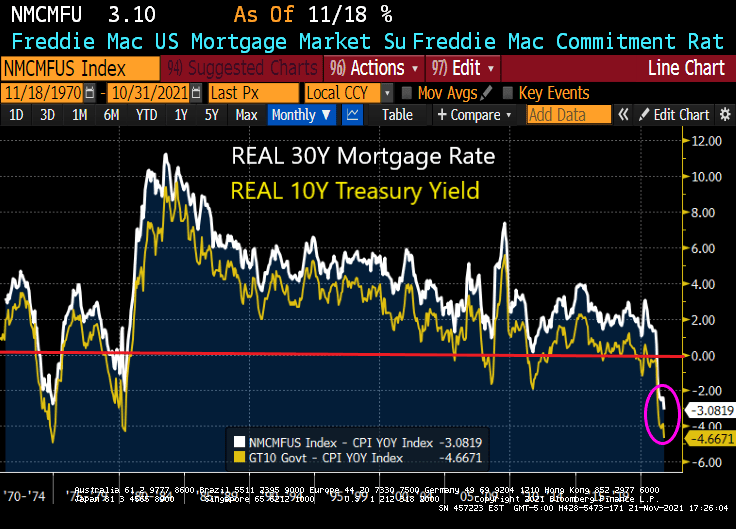

Today’s REAL 30-year mortgage rate is -3.08% while the REAL 10-year Treasury yield is -4.67%. It will require a reduction in inflation AND an increase in the nominal rate to get to 3.6%.

With the Freddie Mac 30-year survey rate at 3.10, will a 50 basis point increase in mortgage rates send the market crashing? Not likely.

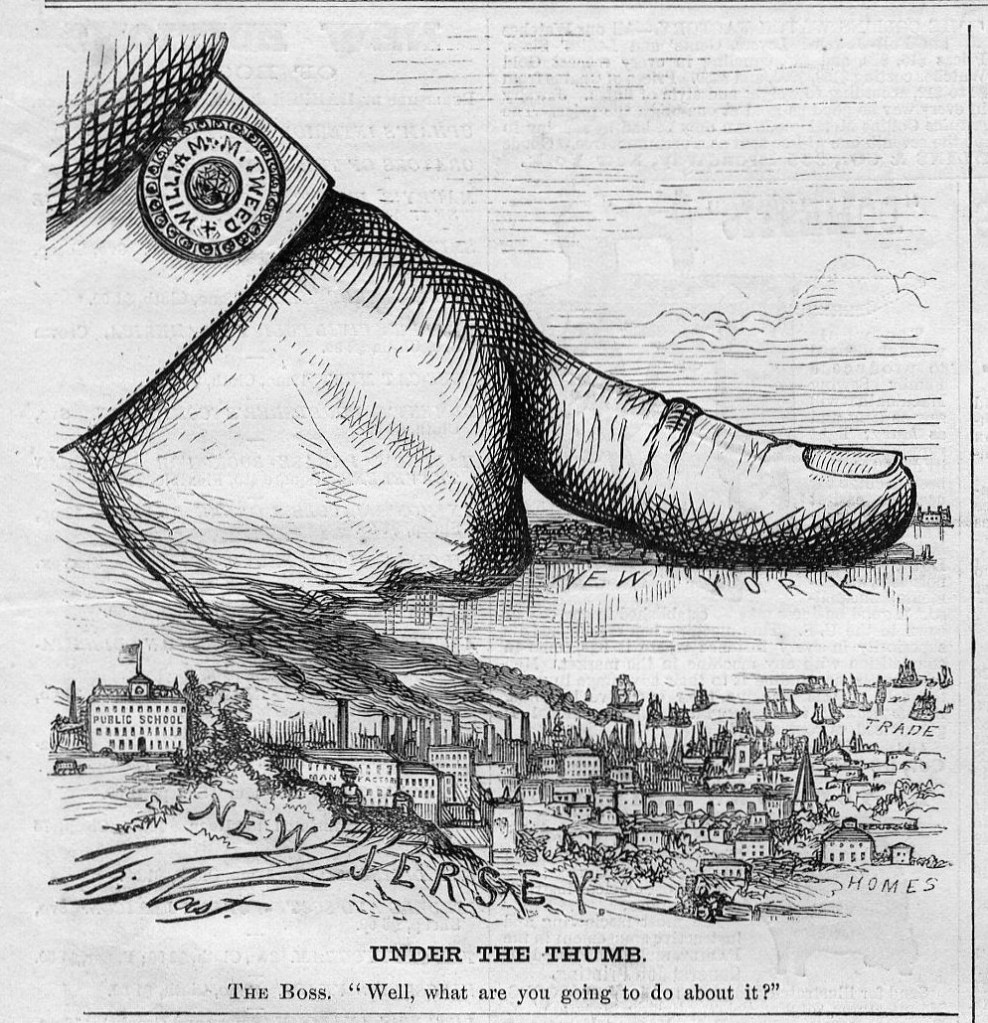

After all, the US economy is under the thumb of The Federal Reserve.

The Marty Stuart/Travis Tritt song “This One’s Gonna Hurt You (For A Long, Long Time)” seems appropriate for the plight of the middle and lower income classes in the face of high inflation. How do you spell the combination of President Biden’s policies and The Fed’s inaction on inflation? T-R-O-U-B-L-E … for the middle and lower income classes.

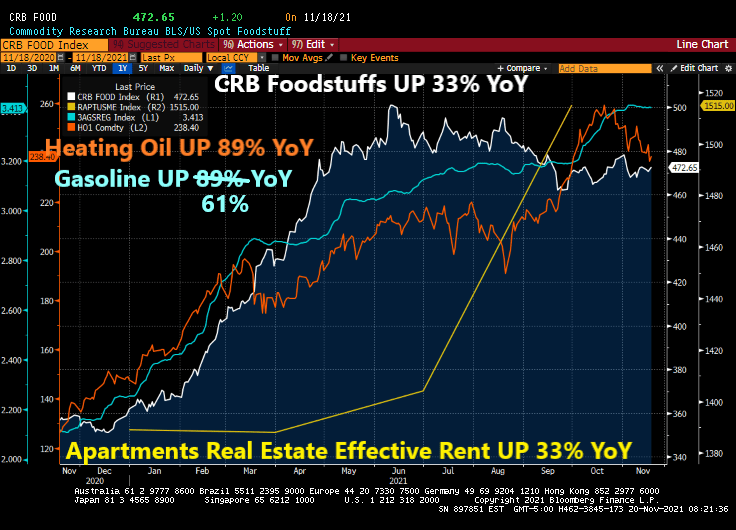

Over the past year, since the election of Joe Biden, the household consumption bundle (food, rent, heating, gasoline) have all risen dramatically in terms of prices. Food is up 33%, heating oil is up 89%, regular gasoline is up 61%, and effective apartment rents are up 33%.

Meanwhile, the 1% are sitting high on a mountain top obvious to the pain caused by The Federal Reserve and Biden Administration. Here is the growth in wealth by the 1% since the housing bubble burst and financial crisis compared with the bottom 50%.

A problem facing renters is the rapid growth of home prices particularly since the COVID epidemic. At least M2 Money has “slowed” to 12.80% YoY while home prices are raging at almost 20% YoY. But hopefully home price growth will slow with declining M2 growth.

Compendium of Fed Chair Jerome Powell and President Biden on vacation.

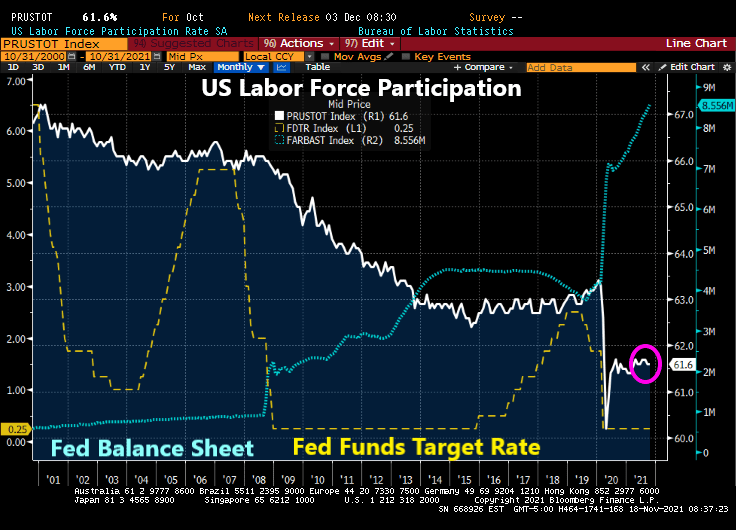

Is the US at full employment? That is, is the US at REALISTIC full employment? And if the US is at realistic full employment, why is The Federal Reserve keeping rates at 25 basis points??

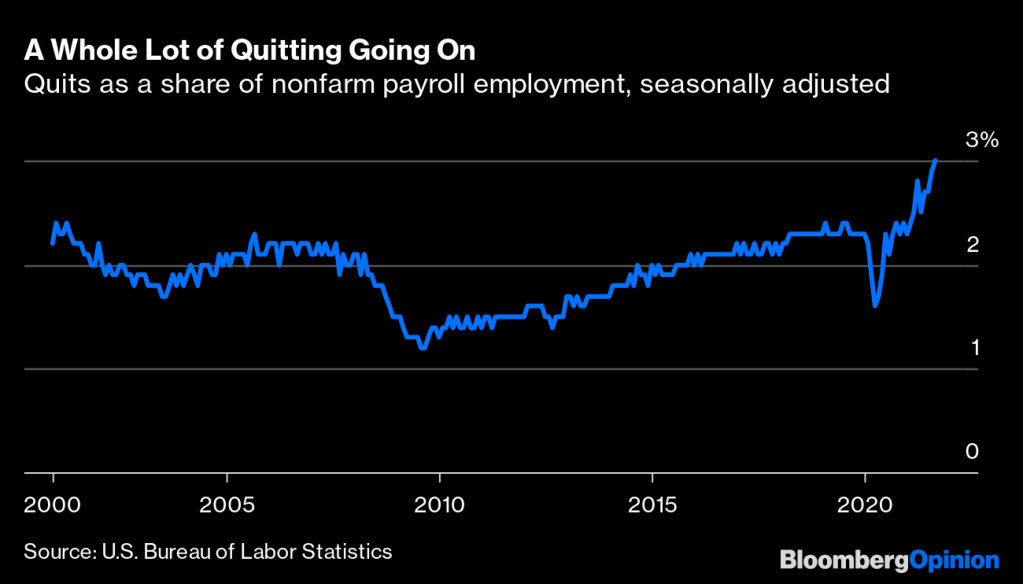

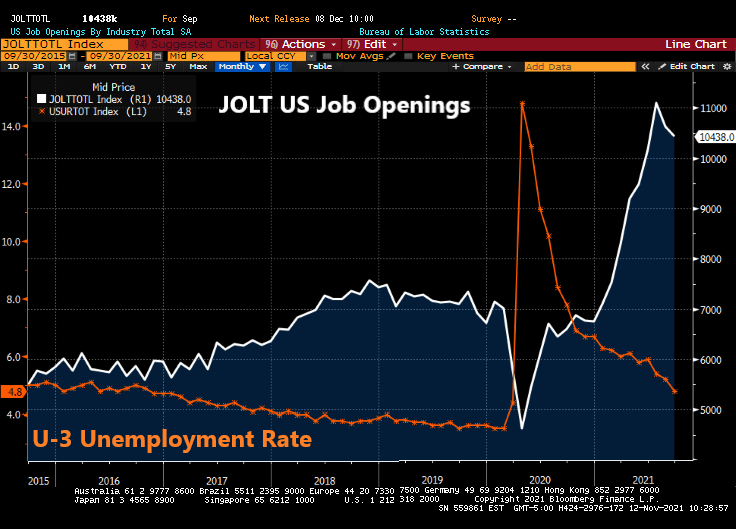

Let’s start with the “quits” data. An estimated 3% of American workers quit their jobs in September, the Bureau of Labor Statistics reported last week.1That’s the highest percentage since the BLS started keeping track two decades ago.

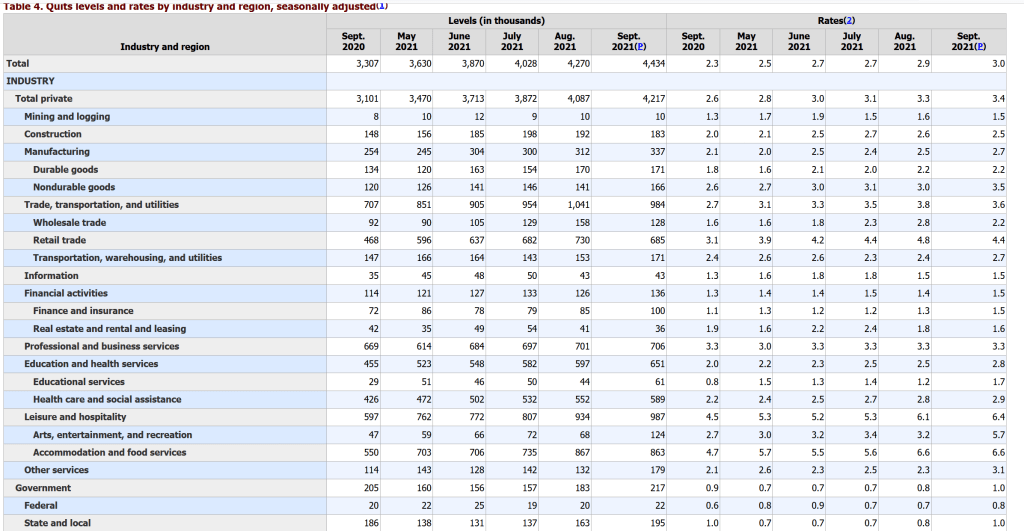

Front-line and low-wage workers are leaving at rates higher than historical norms while higher-paid office workers aren’t. College-educated workers haven’t been quitting or dropping out of the workforce at higher rates than before the pandemic, but less-educated workers have.

The quits rate in professional and business services was just 0.4 percentage points higher in September than before the pandemic in February 2020. In financial activities it was unchanged. In the information sector, made up of telecommunications, publishing, broadcasting, motion pictures, software and most internet companies, the quits rate was down 0.3 percentage points.

The biggest increases in quit rates were in sectors such as leisure and hospitality where office workers are few, working remotely seldom an option and wages low. Within manufacturing, the quits-rate increase has been much bigger in lower-paying nondurable goods (of which food manufacturing is the biggest part) than in higher-paying durable goods.

In particular, fast food restaurants are offering above minimum wage salaries to attract workers. Burger King was even offering college tuition (not to University of Chicago, but to the local community college).

Labor force participation crashed with COVID and has struggled to recover, despite the staggering monetary stimulus. If this a sign that the US is at full employment (or very difficult to entice workers to enter and stay in the labor force)?

I wonder if Biden’s Press Secretary Jen Psaki will argue that inflation is transitory … again?

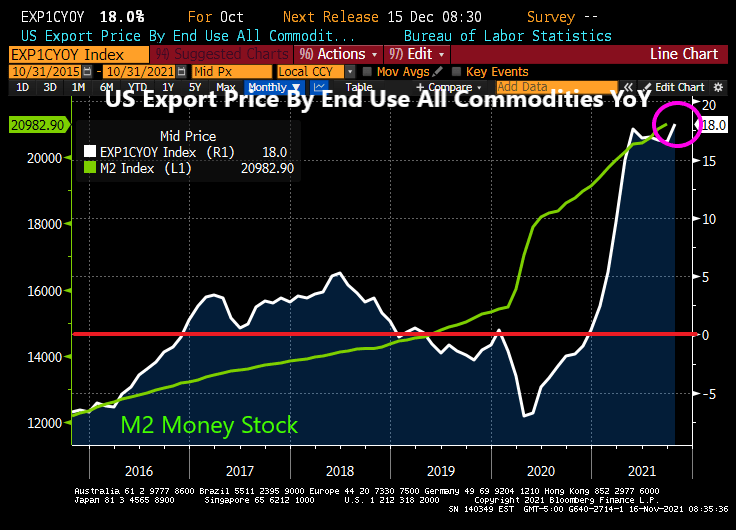

Well, the US is exporting inflation to our trading partners. US Export Prices by end use rose 18% YoY.

Of course, with the Biden Administration shutting down energy pipeline and drilling, it is not surprising.

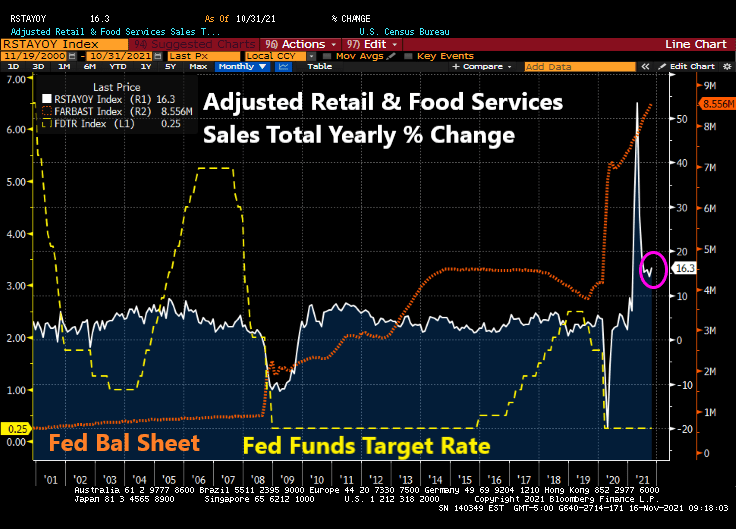

Then we have the advance retail sales numbers for October. Growing at 16.3% YoY with massive monetary stimulus still in play.

Then we have Federal Reserve Bank of St. Louis President James Bullard saying that the central bank should speed up its reduction of monetary stimulus in response to a surge in U.S. inflation.

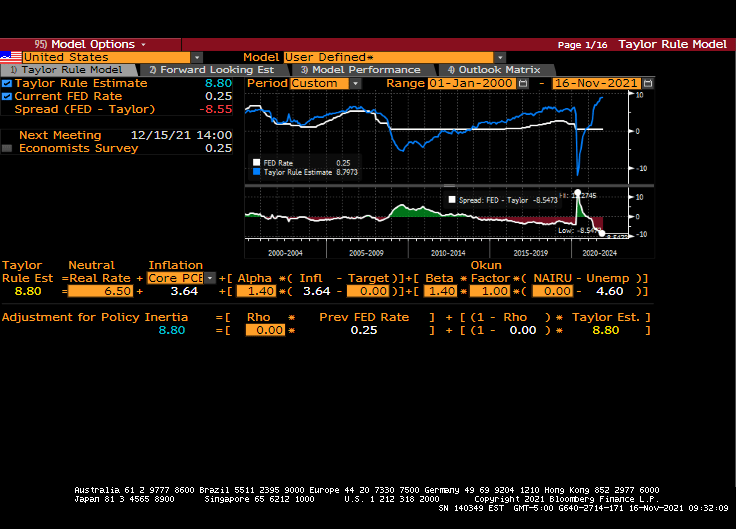

You mean like what Mankiw’s specification of the Taylor Rule model suggests??

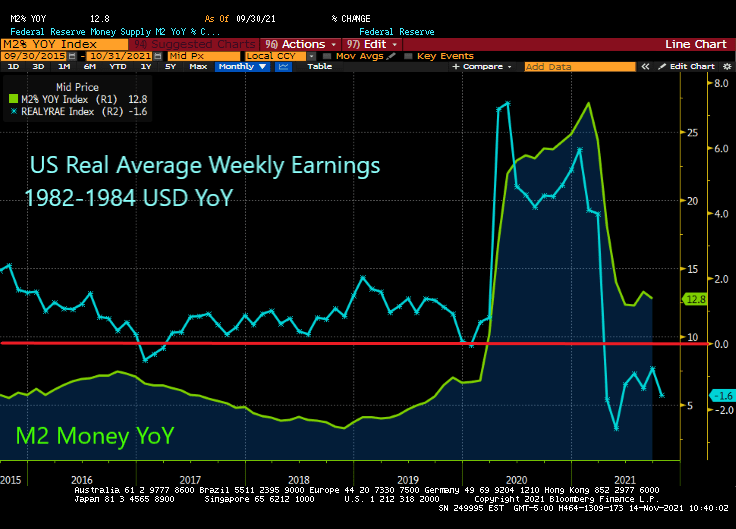

Highlights for Children has a popular segment called “What’s Wrong With This Picture?”

I give you my economics version of “What’s Wrong With This Picture?” It features The Federal Reserve’s M2 Money year–over-year compared with Real Average Weekly Earnings year-over-year.

Yes, M2 Money growth has “slowed” to 12.8% YoY while US Real Average Weekly Earnings YoY is now -1.6%. In other words, while M2 Money is still growing at a rapid pace, real weekly earnings growth is NEGATIVE.

The Fed continues to pump money into a bottle-necked economy while The Federal government pays people NOT to work.

The US Senate has a plan to fix the problem: Biden has nominated Saule Omarova, a dingbat law professor from Cornell (alma matter for The Office’s Andy Bernard), who proposes the following:

(1) Moving all bank deposits from commercial banks to so-called FedAccounts at the Federal Reserve;

(2) Allowing the Fed, in “extreme and rare circumstances, when the Fed is unable to control inflation by raising interest rates,” to confiscate deposits from these FedAccounts in order to tighten monetary policy;

And Ohio Senator Sherrod Brown (D-of course) thinks there is NO MORAL HAZARD PROBLEM with The Fed confiscating bank deposits for its own use?????

If I was attending Omarova’s confirmation hearing, my verdict would be ..

Nothing has been the same since the housing bubble of the 2000s, the resulting banking meltdown and the takeover of the economy by The Federal Reserve.

And since the 2000s housing bubble and financial crisis, The Federal Reserve has taken control of the economy resulting in M2 Money Velocity crashing to historic lows.

You must be logged in to post a comment.