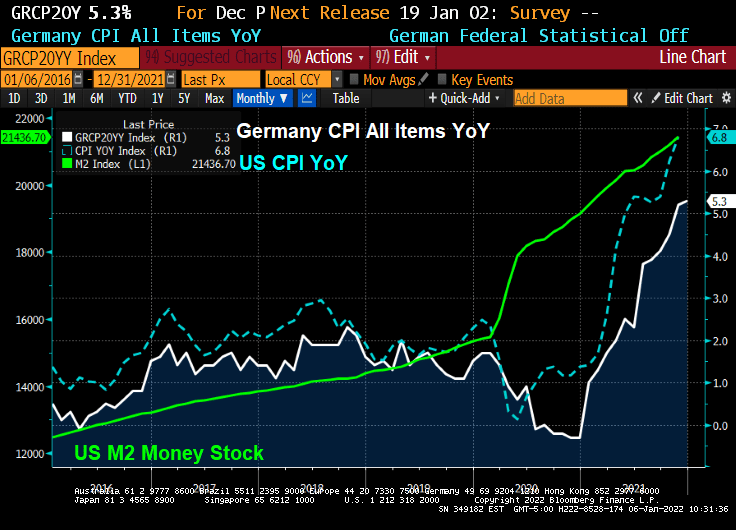

The world has become a wild and wacky place since COVID was unleashed on an unsuspecting population. Since the massive spending spree by The Federal government in the USA coupled with extraordinary monetary stimulus from The Federal Reserve, US inflation has shot up to 6.8% YoY.

German is also having an inflation moment. With their CPI YoY running at 5.3%, faster than the anticipated 5.1%.

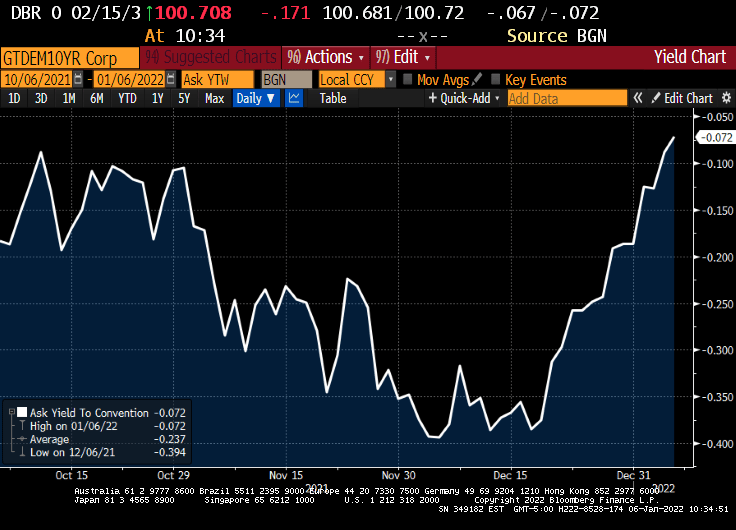

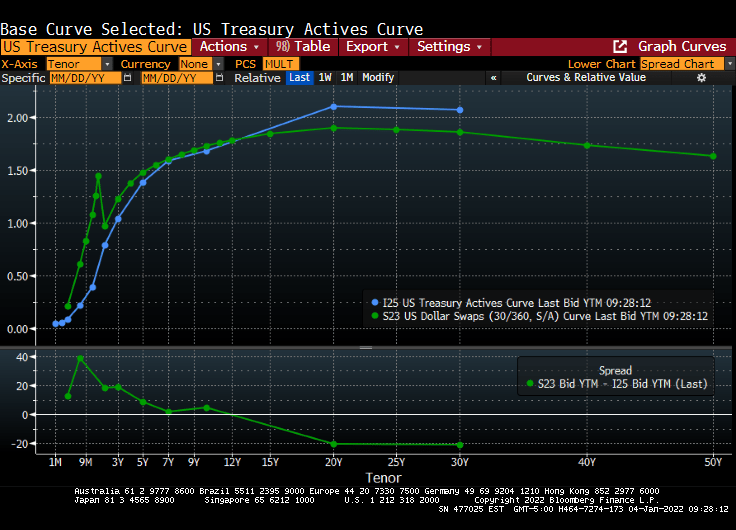

At least the German 10-year sovereign yield is ALMOST back to 0%.

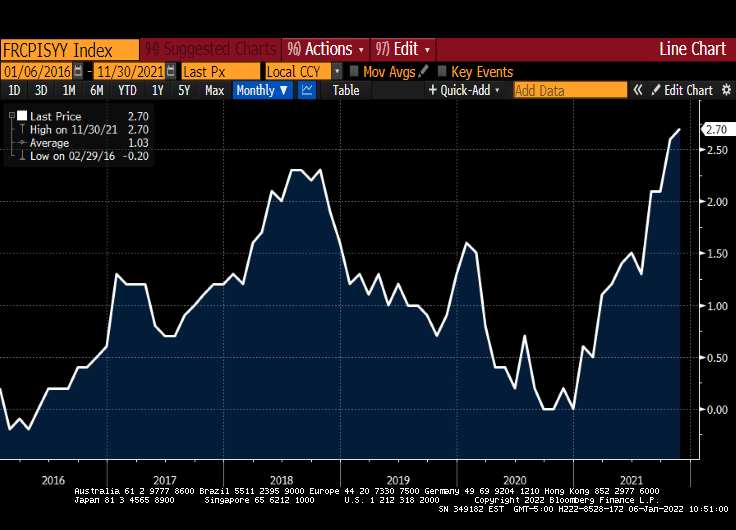

France, on the other hand, is seeing inflation rising to 2.70% YoY.

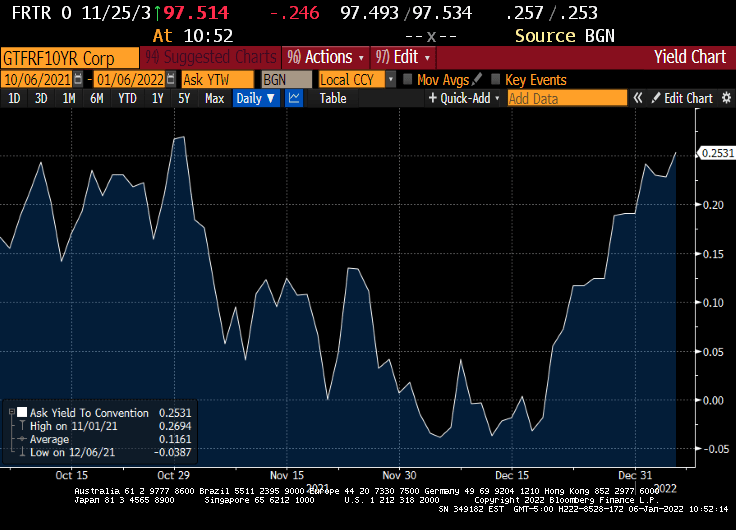

While the French 10Y sovereign yield rose to 0.2531%.

France’s Macron certainly likes to have his photo taken as if he wants to go 10 rounds with UK’s Tyson Fury.

You must be logged in to post a comment.