Mortgage applications increased 3.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 9, 2022.

The Refinance Index increased 3 percent from the previous week and was 85 percent lower than the same week one year ago. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 38 percent lower than the same week one year ago.

You can see the impact of seasonalilty on mortgage purchase applications (white line). They peaked in the week of May 6, 2022 and have been generally declining since. While refi applications (orange line) increased over the past week, they have been pummelled by The Fed tightening.

It is quiet today as investors wait for The Fed to announce a 50 basis point rate increase. Fed Funds Futures point to almost another 100 basis point hike by May 5, 2023, then a slow decline in The Fed Funds target rate (upper bound).

And here is Sam Bankman-Fried and his high-powered legal defense.

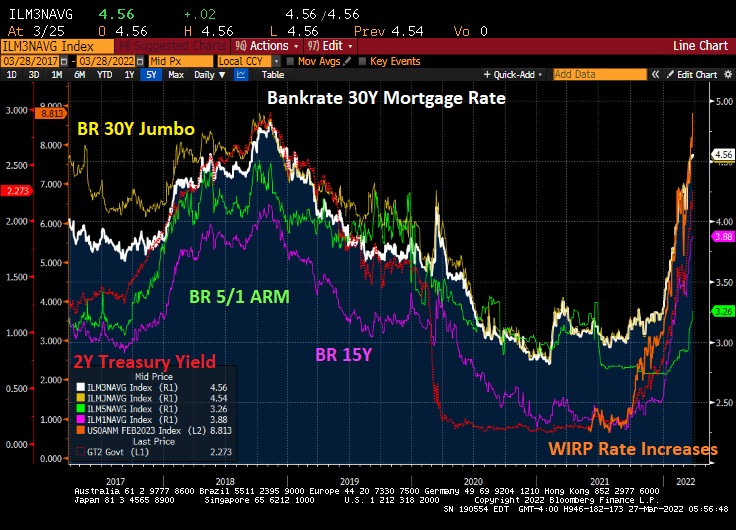

Raging US inflation is resulting in Federal Reserve monetary tightening, causing the 30-year US mortgage rate to hit it highest level since November 2008 (the beginning of Fed Quantitative Easing). Bankrate’s 30-year mortgage rate just hit 6.28%, the highest rate in 14 years.

The Biden Administration will be remembered for crippling inflation, the highest in 40 years AND the highest mortgage rate in 14 years.

And with Fed chatter about hiking rates, Dr T (me) predicts pain for the mortgage market.

The reason why the fear of ARMs is unwarranted is that ARMs generally have CAPS on rate increases, either in a given period or over the life of the loan. Of course, READ the loan terms to ensure that the ARMs has restrictive caps on rate increases.

Currently, the 5/1 ARM is at 3.26% while the 30-year FRM is at 4.56%, a spread of 130 basis points.

Mortgage rates of all flavors are rising rapidly with the expectation of Federal Reserve Quantitative Tightening (QT). There are several headwinds that could counter The Fed’s QT efforts such as low GDP growth (Atlanta Fed’s GDPNow real-time GDP tracker is at 0.9% for Q1), the Russia-Ukraine invasion, approaching midterm elections, etc. But as of today, The Fed seems on a collision course with rising mortgage rates.

With the increasing likelihood of Fed rate hikes over the next year, we are seeing an increase in US ARM loan share from 4% to 7.9%, almost a doubling of ARM share. But FRMs are still over 90% of all mortgage originations.

Lending institutions would prefer consumers to use ARMs rather than FRMs since ARMs allow for the transfer on long-term interest rate risk to the borrower, while the FRM sticks the lender with long-term interest rate risk. Hence, we have Fannie Mae and Freddie Mac, the Government Sponsored Enterprises (GSEs) that allow lenders to originate FRMs and sell them to F&F. We are the only country with twin GSEs.

So, while most consumers would be better-off with an adjustable-rate mortgage, the structure of the mortgage market (particularly after the financial crisis) encourages lenders to originate FRMs and sell them to Fannie Mae and Freddie Mac.

But FEAR drives many US mortgage borrowers into the FRM space rather than getting an ARM with a lower interest rate, even if ARM caps would prevent the mortgage rate from rising more than 100 basis points over the life of the loan.

If you look at the following chart, you can see multifamily (5+ unit) starts remain elevated (pink box) which is not surprising given that home prices at growing at 19.1% YoY nationally (orange circle) and REAL hourly earnings have declined (yellow triangle) thanks to reemergence of inflation after 40 years.

Then we have the humming dragon, rising mortgage rates, that will reduce housing affordability even further.

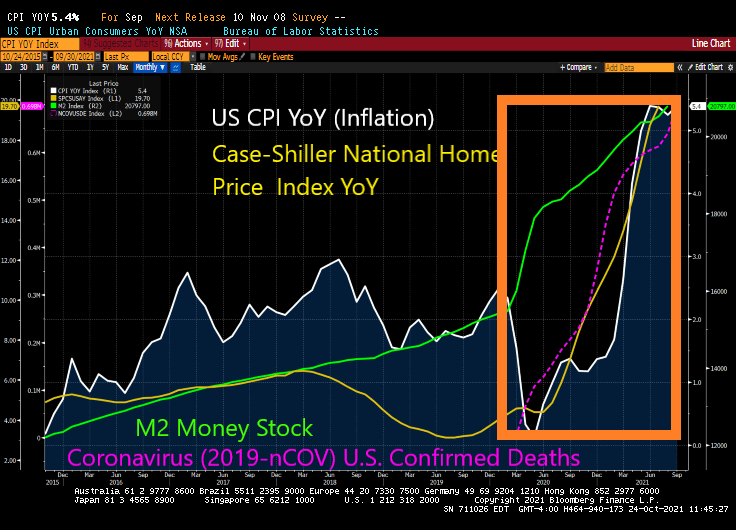

The Federal Reserve is helping to create inflation, particularly since their unorthodox surge in money supply around the Covid outbreak in early 2020. Home prices as of the latest Case-Shiller report are rising at nearly 20% year-over-year.

To add to the problem of The Fed’s overzealous money printing we have The Biden Administration (and puppy-torturer/killer Anthony Fauci) issuing Covid vaccine edicts that are wreaking havoc in labor markets further clogging the economic pipelines.

Between The Fed ZIRP policies and Biden/Fauci’s vax mandates, we are starting to see the rise (again) of the infamous MORTGAGE TILT EFFECT!

The Tilt Effect comes about as expected inflation gets priced into mortgage rates, the mortgage payment rises as the mortgage rate rises (of course), but the higher mortgage payment occurs with EXPECTED inflation in the future.

But not quite yet. Despite CPI inflation growing at 5.4% YoY, Freddie Mac’s 30-year mortgage survey rate is only 3.01% … for now.

As inflation continues to rise (thanks to ongoing Fed ZIRP policies and governments mandating Covid vaccine in order to keep your job, we should eventually see mortgage rates rise … leading to a return of THE TILT EFFECT. Which in turns make housing even MORE unaffordable.

We have tried numerous mortgage contracts in the past (mostly to offset Carter-era inflation) such as the PLAM (price-level adjusted mortgage) and the GPM (graduated payment mortgage). Now we have the PLUM (price level unadjusted mortgage) which is subject to the TILT EFFECT.

Phil Hall of Benzinga wrote a series of excellent articles in four parts for MortgageOrb (although “The Orb” has removed his name). Here are the links to his stories.

After re-reading these excellent articles on the housing bubble and crash, I thought I would take the opportunity to present a few charts to highlight the housing bubble, pre-crash and post-crash.

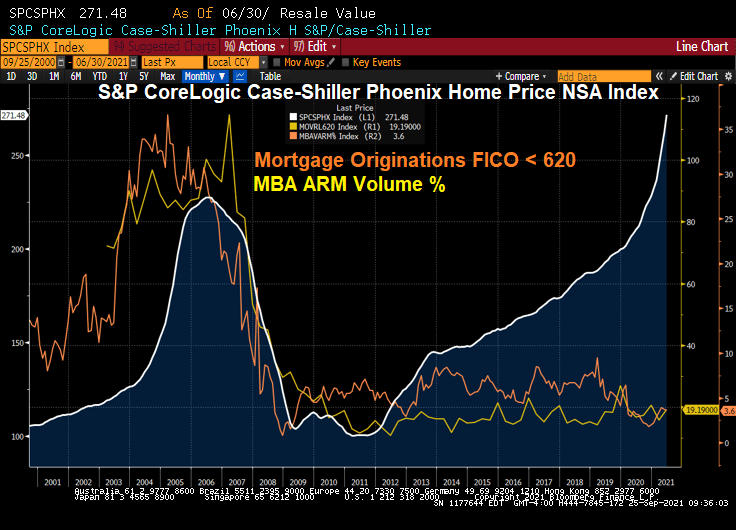

Here is a graph of Phoenix AZ home prices. Note the bubble that peaked in mid 2006. The Phoenix bubble correlates with the large volume of sub-620 FICO lending and Adjustable-rate mortgage (ARM) lending. Bear in mind, many of the ARMs prior to 2010 were NINJA (no income, no job) ARM loans.

What happened? Serious delinquenices at the national levels spiked as The Great Recession set in and unemployment spiked.

Since the housing bubble burst and surge in serious mortgage delinquencies, The Federal Reserve entered the economy with a vengeance. And have never left, and increased their drowning of markets with liquidity.

The Fed whip-sawing of interest rates in response to the 2001 recession was certainly a problem. They dropped The Fed Funds Target rate like a rock, then homebuilding went wild nationally and home prices soared thanks to Alt-A (NINJA) and ARM lending. But now The Fed is dominating markets like a gigantic T-Rex.

Oddly, then Fed Chair Ben Bernanke never saw the bubble coming. Or the burst.

Speaking of pizza, Donato’s from Columbus Ohio is my favorite. Founder’s Favorite is my favorite, but they do offer the dreaded Hawaiian pizza (ham, pineapple, almonds and … cinnamon?)

You must be logged in to post a comment.