Welcome to the wonderful world of Bidenomics, giving the US 40 year highs in inflation leading The Federal Reserve to remove its enormous monetary stimulus (known as “The Punch Bowl.”

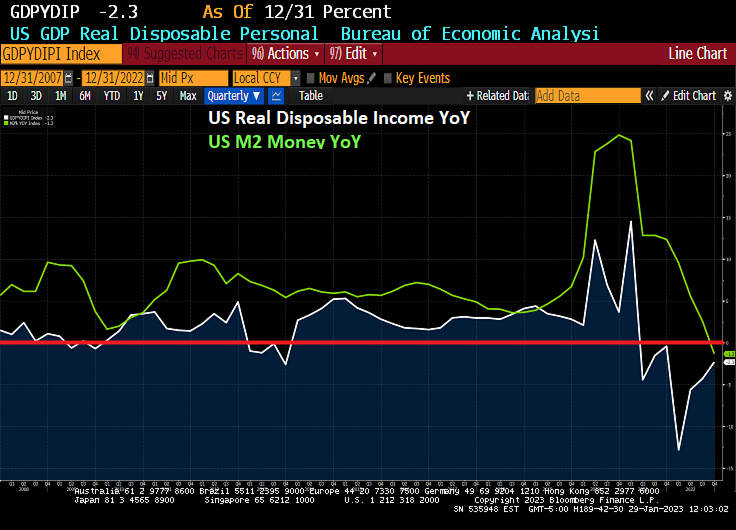

I previously pointed out that US Real GDP was actually less than 1% year-over-year (YoY) in 2022, hardly a fantastic number given the trillions in Biden/Pelosi/Schumer spending (Omnibus, Infrastructure, etc) and Powell/Fed’s whopping monetary stimulus in 2020. But real disposable income, the amount households have left to spend after adjusting for inflation, had been falling for 7 straight months.

In fact, REAL disposable personal income peaked in March 2021, shortly after Biden was sworn-in as President in Janaury 2021 at $19,213.9 billion (or $19.214 TRILLION). As of December 2022, real personal disposable income had fallen to $15,213.0 or $15.213 TRILLION. That is a loss of $4 TRILLION since March 2021. Or a -21% Loss in Real Disposable Income.

There was a hilarious film with Hillary Swank and Aaron Ekhart called “The Core” where earth’s core stops spinning and the earth gets cooked by the Sun’s rediation. Now we learn that the Earth’s inne core has actually stop spinning. This time, however, all that has happened is that Joe Biden is President which is almost as bad,

But also related to “The Core” is that the important Personal Consumption Expenditures (PCE) are out for December along with PCE price deflator numbers. In short, personal income was up 0.2% month-over-month (MoM) in December while personal spending was down -0.2%. REAL personal spending was down -0.3% MoM.

But the all important PCE deflators numbers were down all well. The REAL PCE price index (or deflator) was down to 5.0% YoY in Decmember while REAL CORE price index was down to 4.40%. All this is happening as M2 Money growth has stop spinning (down to -1.3% YoY in December).

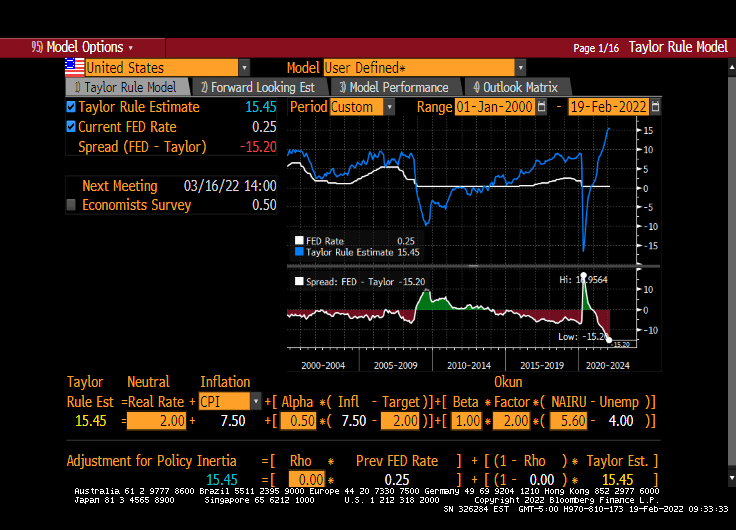

Based on a CORE PCE YoY of 4.40%, the Taylor Rules suggest that The Fed Fund Target rate should be … 10%. However, the current Fed Funds Target rate is only 4.50%, so The Fed is not even half way there.

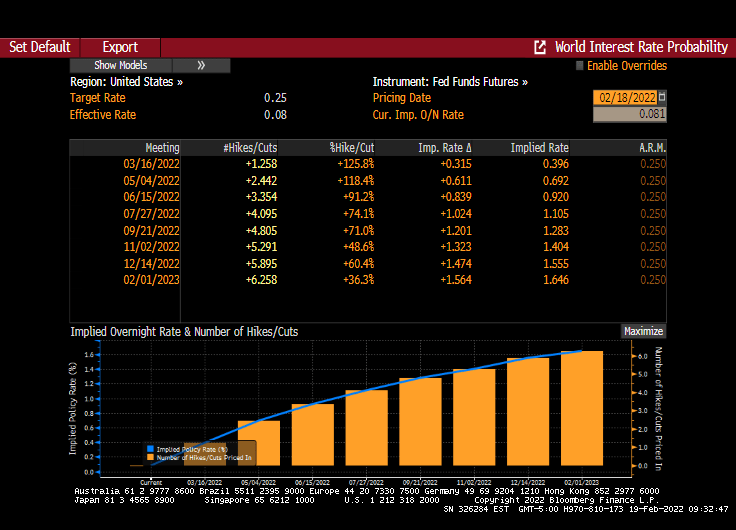

Fed Funds Futures are pointing to a peak rate of 4.90% by the June ’23 FOMC meeting, then a pivot (despite denials from Fed talking heads).

Of course, The Fed doesn’t follow the Taylor Rule or any other transparent rule for rate management. Rather, Fed Chair Powell like former Chair (and current Treasury Secretary Janet Yellen) follow a more seat-of-the-pants approach.

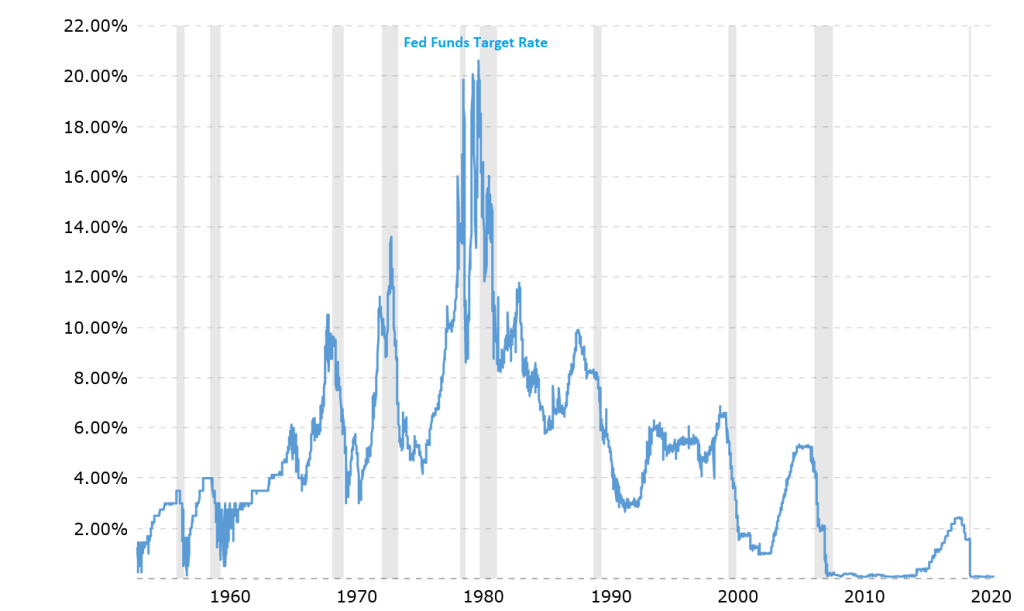

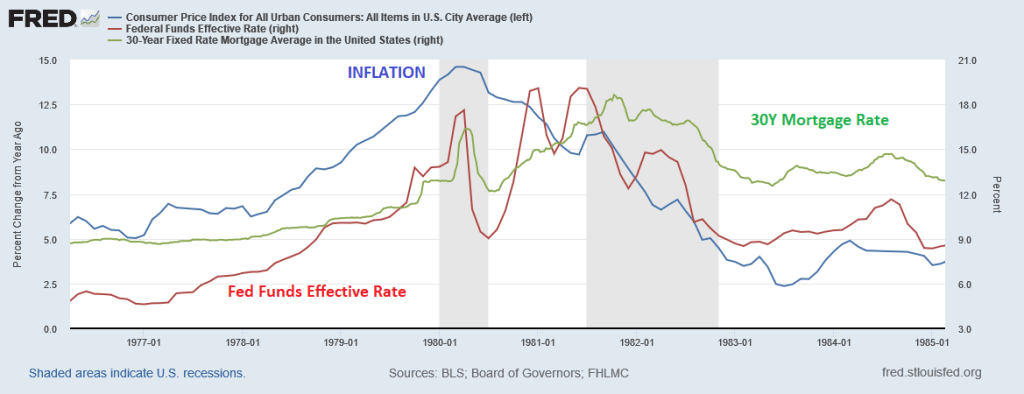

In August 1979, when Paul Volcker became chairman of the Federal Reserve Board, the annual average inflation rate in the United States was 11%. Inflation peaked in 1980 at 14.6%. Volcker raised the federal funds rate from 11.2% in 1979 to 20% in June of 1981.

Inflation (defined as CPI YoY) declined from over 14.6% in 1980 to 3.6% by 1985. But 30-year mortgage rates resumed their upward trajectory and peaking in October 1981 at 18.63 before beginning a gradual decline as inflation was tamed.

But will Powell enact another Volcker moment by raising the target rate abruptly?

The bank is joining others on Wall Street in ramping up bets for faster policy tightening, after U.S. consumer prices posted the biggest jump since 1982 in January. Goldman Sachs Group Inc. is forecasting seven hikes this year, up from its earlier prediction of five.

“We now look for the Fed to hike 25bp at each of the next nine meetings, with the policy rate approaching a neutral stance by early next year,” the JPMorgan team, led by chief economist Bruce Kasman, said in a research note.

January U.S. inflation readings “surprised materially to the upside,” the economists wrote. “We now no longer see deceleration from last quarter’s near-record pace.”

On inflation, the economists said a “feedback loop” may be taking hold between strong growth, cost pressures, and private sector behavior that will continue even as the intensity of current price pressures in the energy sector eventually fade.

Strong growth? 1.3% is strong growth??

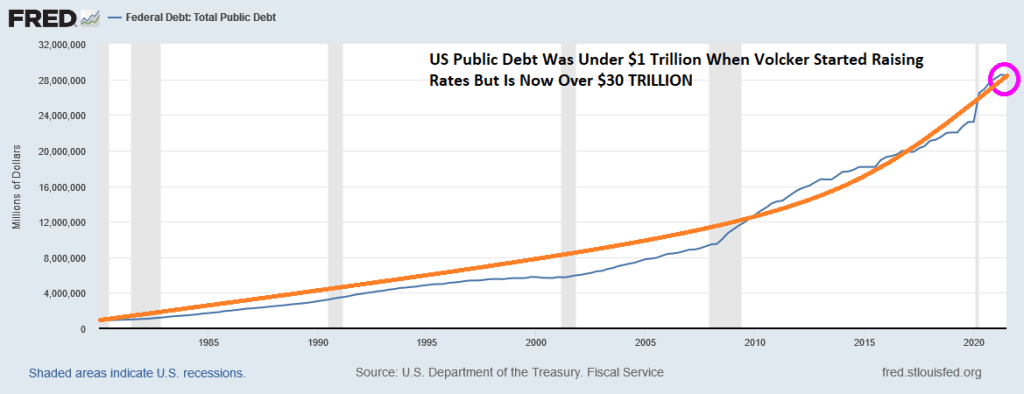

Be that as it may, the US economy is at a different place today than under President Jimmy Carter. When Volcker started raising The Fed Funds Target rate, US public debt was still under $1 trillion. It has ballooned to over $30 trillion today.

9 rate increases is above what is being priced in The Fed Funds FUTURES market which is 6 rate increases over the coming year.

With 7.5% inflation, the Taylor Rule suggests a target rate of 15.45%. Talk about “Shock and Awful!”

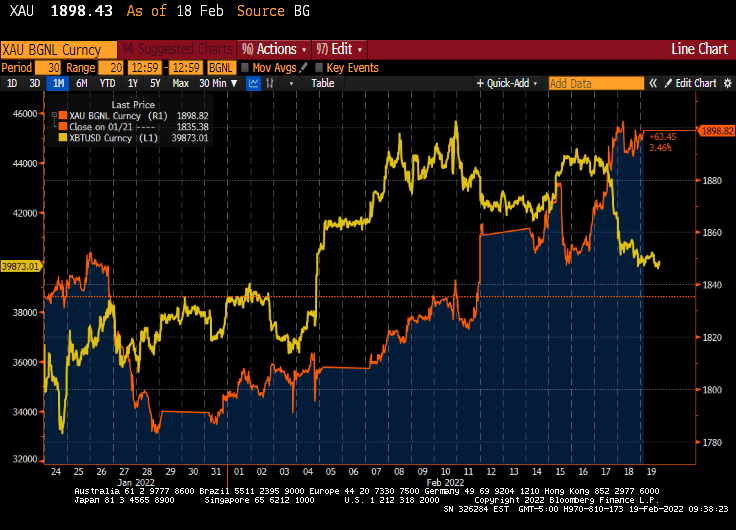

We are starting to see GOLD (gold) surging and Bitcoin (yellow) falling as The Fed prepares “shock and awful” rate hikes and Biden continues to beat the war drums over Russia invading Ukraine.

If The Fed actually raises rates 9 times and dramatically pares back its massive monetary stimulus, it will be “shock and awful.”

You must be logged in to post a comment.